Recognition: unknown

A Systematic Review of Recent Advancements in PINN Augmented Deep Learning and Mathematical Modeling for Efficient Portfolio Management

Pith reviewed 2026-05-07 06:00 UTC · model grok-4.3

The pith

Physics-informed neural networks embed finance principles directly into deep learning to ensure portfolio forecasts comply with regulations.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper establishes that physics-informed neural networks augment deep learning and mathematical modeling for portfolio management by directly integrating physics and finance principles into the network's learning process, thereby generating precise forecasts that align with financial regulations and processes, and it provides an overview of the advantages, disadvantages, and open issues across these approaches.

What carries the argument

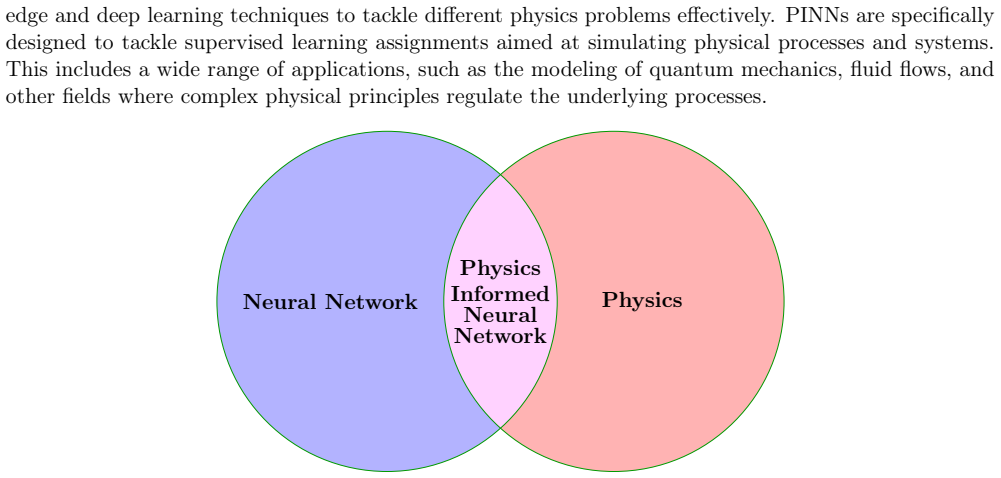

Physics-informed neural networks (PINNs), neural networks modified to include physics and finance principles as constraints or additional loss terms during training so that outputs remain consistent with domain laws.

Load-bearing premise

The review assumes its selection of literature is comprehensive and representative of the field and that PINNs do produce forecasts aligned with financial regulations.

What would settle it

A literature search using the review's implied keywords that returns many additional relevant papers on PINNs in portfolio management not covered here would falsify comprehensiveness, or a controlled test showing PINN outputs for a portfolio violating a specific financial regulation would falsify the alignment claim.

Figures

read the original abstract

In finance, portfolio management is a traditional yet difficult problem that has drawn attention from practitioners and researchers for many years. However, there are still difficult technological problems that need to be solved. In the world of finance, managing a portfolio has never been easy. Selecting portfolios in a volatile market is made easier with the help of portfolio management. The goal of this review study is to present the concept of physics-informed neural networks because they provide a novel approach to directly incorporating physics and finance principles into the neural network's learning process. By doing so, physics-informed neural networks ensure that their forecasts are in line with established financial regulations and processes in addition to offering precise forecasts. Furthermore, this article provides an overview of the current state of research in portfolio optimization with the support of mathematical models, deep learning models and physics-informed neural networks. In addition, the advantages and disadvantages of various deep learning and mathematical modelling are discussed. Researchers and business professionals alike should find the data useful for advancing the field of investment management and trying out new portfolio management strategies. For this purpose, in this review work, emphasis is given to these factors. Finally, a few challenging issues and potential future directions are discussed, encouraging readers to consider fresh ideas in this field of study.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper presents itself as a systematic review of recent advancements in physics-informed neural networks (PINNs) combined with deep learning and mathematical modeling for portfolio management. It claims that PINNs provide a novel approach to directly embedding physics and finance principles into neural network training, producing forecasts aligned with financial regulations and processes. The review covers the current state of portfolio optimization using mathematical models, deep learning models, and PINN-based methods; discusses advantages and disadvantages of these approaches; and outlines challenging issues and future research directions for researchers and practitioners.

Significance. If the central claims hold and the review is properly executed with representative literature, this work could be significant in highlighting how PINNs can integrate domain knowledge from physics and finance to improve robustness and regulatory compliance in portfolio strategies. It has potential value in guiding the adoption of hybrid ML-mathematical methods in volatile financial markets, provided concrete mechanisms from the surveyed papers are documented.

major comments (2)

- [Abstract] Abstract: The manuscript describes itself as a 'systematic review' but supplies no search protocol, databases queried, inclusion/exclusion criteria, PRISMA-style flow, or final count of reviewed papers. This omission is load-bearing because the paper's primary contribution is positioned as a reliable overview of the literature; without these elements the representativeness of the surveyed works cannot be assessed.

- [Abstract] Abstract: The assertion that PINNs 'ensure that their forecasts are in line with established financial regulations and processes' is stated without citing any specific mechanisms (e.g., particular PDE constraints, boundary conditions, or loss-term formulations) drawn from the reviewed studies. No concrete examples or references to how these enforce regulatory alignment are provided, undermining the novelty claim.

minor comments (2)

- [Abstract] Abstract: The opening sentences contain redundant statements about the difficulty of portfolio management ('difficult problem', 'difficult technological problems', 'has never been easy') that should be streamlined for conciseness and clarity.

- [Abstract] Abstract: The abstract promises discussion of advantages and disadvantages of deep learning and mathematical modelling approaches but provides no preview of specific findings or examples from the literature, leaving the reader without a clear sense of the review's concrete contributions.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments on our manuscript. These observations highlight important aspects of transparency and substantiation that will strengthen the paper. We address each major comment point by point below, indicating the revisions we will make.

read point-by-point responses

-

Referee: [Abstract] Abstract: The manuscript describes itself as a 'systematic review' but supplies no search protocol, databases queried, inclusion/exclusion criteria, PRISMA-style flow, or final count of reviewed papers. This omission is load-bearing because the paper's primary contribution is positioned as a reliable overview of the literature; without these elements the representativeness of the surveyed works cannot be assessed.

Authors: We agree that explicit documentation of the systematic review process is essential for establishing the reliability and representativeness of the surveyed literature. In the revised manuscript we will insert a dedicated 'Review Methodology' section immediately following the introduction. This section will specify the databases queried (Web of Science, Scopus, arXiv, IEEE Xplore, and Google Scholar), the Boolean search strings employed, the time window (2018–2024), the inclusion criteria (peer-reviewed articles or preprints that combine PINNs with portfolio optimization or risk management), the exclusion criteria (purely theoretical physics papers without financial application, non-English works, and duplicates), a PRISMA flow diagram, and the final count of included studies (currently 47). These additions will allow readers to evaluate coverage and will be cross-referenced in the abstract and conclusion. revision: yes

-

Referee: [Abstract] Abstract: The assertion that PINNs 'ensure that their forecasts are in line with established financial regulations and processes' is stated without citing any specific mechanisms (e.g., particular PDE constraints, boundary conditions, or loss-term formulations) drawn from the reviewed studies. No concrete examples or references to how these enforce regulatory alignment are provided, undermining the novelty claim.

Authors: We acknowledge that the current abstract and discussion sections state the regulatory-alignment benefit at a high level without anchoring it to concrete formulations from the literature. In the revised version we will expand the subsection on PINN-based portfolio methods to include explicit examples drawn from the reviewed papers. For instance, we will describe how certain works embed the Black–Scholes PDE as a soft constraint in the loss function to enforce no-arbitrage consistency (a regulatory expectation in derivative pricing), how others incorporate Value-at-Risk or expected-shortfall terms directly into the physics-informed loss to satisfy Basel-style risk limits, and how boundary conditions reflecting regulatory capital requirements are imposed. Each example will be accompanied by the corresponding reference and a brief description of the loss-term formulation. These additions will be summarized concisely in the abstract as well. revision: yes

Circularity Check

No circularity: review paper with no original derivations or self-referential predictions

full rationale

This manuscript is explicitly framed as a literature review surveying mathematical models, deep learning, and PINNs for portfolio management. The provided abstract and structure contain no equations, fitted parameters, predictions, or derivation chains that could reduce to inputs by construction. Claims about PINNs incorporating physics/finance principles rest on descriptions of external prior work rather than internal definitions or self-citations that bear the central argument. No self-definitional loops, fitted-input-as-prediction patterns, or uniqueness theorems imported from the authors' own prior papers appear. The review's value (or lack thereof) hinges on the completeness of its literature coverage and citation quality, not on any tautological reduction within its own logic. This is the expected outcome for a non-original survey article.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Option return predictability with machine learning and big data,

T. G. Bali, H. Beckmeyer, M. Moerke, and F. Weigert, “Option return predictability with machine learning and big data,”The Review of Financial Studies, vol. 36, no. 9, pp. 3548–3602, 2023

2023

-

[2]

Portfolio models with return forecasting and transaction costs,

J. R. Yu, W. J. P. Chiou, W. Y. Lee, and S. J. Lin, “Portfolio models with return forecasting and transaction costs,”International Review of Economics & Finance, vol. 66, pp. 118–130, 2020

2020

-

[3]

Robust active portfolio management,

E. Erdogan, D. G. Goldfarb, and G. Iyengar, “Robust active portfolio management,”Journal of Computational Finance, vol. 11, no. 4, p. 71, 2008

2008

-

[4]

Portfolio selection in the presence of systemic risk,

A. Biglova, S. Ortobelli, and F. J. Fabozzi, “Portfolio selection in the presence of systemic risk,” Journal of Asset Management, vol. 15, no. 5, pp. 285–299, 2014

2014

-

[5]

Deep reinforcement learning for trading,

Z. Zhang, S. Zohren, and R. Stephen, “Deep reinforcement learning for trading,”The Journal of Financial Data Science, vol. 2, no. 2, pp. 25–40, 2020

2020

-

[6]

Stochastic evolution equations for large portfolios of stochastic volatility models,

B. Hambly and N. Kolliopoulos, “Stochastic evolution equations for large portfolios of stochastic volatility models,”SIAM Journal on Financial Mathematics, vol. 8, no. 1, pp. 962–1014, 2017

2017

-

[7]

Portfolio optimization with entropic value-at-risk,

A. Ahmadi Javid and M. Fallah Tafti, “Portfolio optimization with entropic value-at-risk,”European Journal of Operational Research, vol. 279, no. 1, pp. 225–241, 2019

2019

-

[8]

Sensitivity analysis for mean-variance portfolio problems,

M. J. Best and R. R. Grauer, “Sensitivity analysis for mean-variance portfolio problems,”Manage- ment science, vol. 37, no. 8, pp. 980–989, 1991. 22

1991

-

[9]

Large-scale portfolio optimization using multiobjective dynamic mutli- swarm particle swarm optimizer,

J. J. Liang and B. Y. Qu, “Large-scale portfolio optimization using multiobjective dynamic mutli- swarm particle swarm optimizer,” in2013 IEEE Symposium on Swarm Intelligence (SIS), 2013, pp. 1–6

2013

-

[10]

Portfolio selection with transaction costs,

M. H. Davis and A. R. Norman, “Portfolio selection with transaction costs,”Mathematics of opera- tions research, vol. 15, no. 4, pp. 676–713, 1990

1990

-

[11]

Systemic risk-driven portfolio selection,

A. Capponi and A. Rubtsov, “Systemic risk-driven portfolio selection,”Operations Research, vol. 70, no. 3, pp. 1598–1612, 2022

2022

-

[12]

Deep learning for portfolio optimization,

Z. Zhang, S. Zohren, and S. Roberts, “Deep learning for portfolio optimization,”The Journal of Financial Data Science, vol. 2, pp. 8–20, 2020

2020

-

[13]

Machine learning and portfolio optimization,

G.-Y. Ban, N. El Karoui, and A. E. Lim, “Machine learning and portfolio optimization,”Management Science, vol. 64, no. 3, pp. 1136–1154, 2018

2018

-

[14]

Stochastic optimal control of ultradiffusion processes with application to dynamic portfolio management,

M. D. Marcozzi, “Stochastic optimal control of ultradiffusion processes with application to dynamic portfolio management,”Journal of computational and applied mathematics, vol. 222, no. 1, pp. 112– 127, 2008

2008

-

[15]

Optimal bond portfolios,

I. Ekeland and E. Taflin, “Optimal bond portfolios,”Paris-Princeton Lectures on Mathematical Fi- nance, vol. 1919, pp. 51–102, 2007

1919

-

[16]

Optimal contract for a fund manager with capital injections and endogenous trading constraints,

S. Nadtochiy and T. Zariphopoulou, “Optimal contract for a fund manager with capital injections and endogenous trading constraints,”SIAM Journal on Financial Mathematics, vol. 10, no. 3, pp. 698–722, 2019

2019

-

[17]

Implementation of stochastic yield curve duration and portfolio immunization strate- gies,

S. Duedahl, “Implementation of stochastic yield curve duration and portfolio immunization strate- gies,”Journal of Mathematical Finance, vol. 6, no. 3, pp. 401–415, 2016

2016

-

[18]

Portfolio optimization within a wasserstein ball,

S. M. Pesenti and S. Jaimungal, “Portfolio optimization within a wasserstein ball,”SIAM Journal on Financial Mathematics, vol. 14, no. 4, pp. 1175–1214, 2023

2023

-

[19]

Application of maximal monotone operator method for solving hamilton–jacobi–bellman equation arising from optimal portfolio selection problem,

C. I. Udeani and D. Ševčovič, “Application of maximal monotone operator method for solving hamilton–jacobi–bellman equation arising from optimal portfolio selection problem,”Japan Jour- nal of Industrial and Applied Mathematics, vol. 38, no. 3, pp. 693–713, 2021

2021

-

[20]

Inter-temporal mutual-fund management,

A. Bensoussan, K. C. Cheung, Y. Li, and S. C. P. Yam, “Inter-temporal mutual-fund management,” Mathematical Finance, vol. 32, no. 3, pp. 825–877, 2022

2022

-

[21]

Real options games in complete and incomplete markets with several decision makers,

A. Bensoussan, J. D. Diltz, and S. Hoe, “Real options games in complete and incomplete markets with several decision makers,”SIAM Journal on Financial Mathematics, vol. 1, no. 1, pp. 666–728, 2010

2010

-

[22]

Portfolio selection in stochastic environments,

J. Liu, “Portfolio selection in stochastic environments,”The Review of Financial Studies, vol. 20, no. 1, pp. 1–39, 2007

2007

-

[23]

Systemic risk and stability in financial networks,

D. Acemoglu, A. Ozdaglar, and A. Tahbaz-Salehi, “Systemic risk and stability in financial networks,” American Economic Review, vol. 105, no. 2, pp. 564–608, 2015

2015

-

[24]

Portfolio selection,

H. Markowitz, “Portfolio selection,”The Journal of Finance, vol. 1, pp. 71–91, 1952

1952

-

[25]

Simple criteria for optimal portfolio selection,

E. J. Elton, M. J. Gruber, and M. W. Padberg, “Simple criteria for optimal portfolio selection,”The Journal of finance, vol. 31, no. 5, pp. 1341–1357, 1976

1976

-

[26]

A mean-variance-skewness portfolio optimization model,

H. Konno and K.-i. Suzuki, “A mean-variance-skewness portfolio optimization model,”Journal of the Operations Research Society of Japan, vol. 38, no. 2, pp. 173–187, 1995

1995

-

[27]

Mean-absolute deviation portfolio optimization model and its applica- tions to tokyo stock market,

H. Konno and H. Yamazaki, “Mean-absolute deviation portfolio optimization model and its applica- tions to tokyo stock market,”Management science, vol. 37, no. 5, pp. 519–531, 1991. 23

1991

-

[28]

Asymmetric risk measures and tracking models for portfolio optimization under uncer- tainty,

A. J. King, “Asymmetric risk measures and tracking models for portfolio optimization under uncer- tainty,”Annals of Operations Research, vol. 45, pp. 165–177, 1993

1993

-

[29]

On a free boundary problem that arises in portfolio management,

S. R. Pliska and M. J. Selby, “On a free boundary problem that arises in portfolio management,” Philosophical Transactions of the Royal Society of London. Series A: Physical and Engineering Sci- ences, vol. 347, no. 1684, pp. 555–561, 1994

1994

-

[30]

A dynamic approach for the evaluation of portfolio performance under risk conditions,

C. Alexakis, D. Balios, S. Stavrakiet al., “A dynamic approach for the evaluation of portfolio performance under risk conditions,”Invest. Manag. Financ. Innov, vol. 4, pp. 16–24, 2007

2007

-

[31]

Portfolio optimization with linear and fixed transaction costs,

M. S. Lobo, M. Fazel, and S. Boyd, “Portfolio optimization with linear and fixed transaction costs,” Annals of Operations Research, vol. 152, pp. 341–365, 2007

2007

-

[32]

Time series momentum and volatility scaling,

A. Y. Kim, Y. Tse, and J. K. Wald, “Time series momentum and volatility scaling,”Journal of Financial Markets, vol. 30, pp. 103–124, 2016

2016

-

[33]

Fuzzy mathematical programming for portfolio management,

T. Leon, V. Liern, and E. Vercher, “Fuzzy mathematical programming for portfolio management,” inFinancial Modelling. Springer, 2000, pp. 241–256

2000

-

[34]

Quantitative approach to project portfolio management: proposal for slovak companies,

P. Kral, V. Valjaskova, and K. Janoskova, “Quantitative approach to project portfolio management: proposal for slovak companies,”Oeconomia Copernicana, vol. 10, no. 4, pp. 797–814, 2019

2019

-

[35]

Equity portfolio diversification,

W. N. Goetzmann and A. Kumar, “Equity portfolio diversification,”Review of Finance, vol. 12, no. 3, pp. 433–463, 2008

2008

-

[36]

Portfolio selection under systemic risk,

W. Lin, J. Olmo, and A. Taamouti, “Portfolio selection under systemic risk,”Journal of Money, Credit and Banking, 2024

2024

-

[37]

Optimal brokerage contracts in almgren–chriss model with multiple clients,

G. A. Alvarez, S. Nadtochiy, and K. Webster, “Optimal brokerage contracts in almgren–chriss model with multiple clients,”SIAM Journal on Financial Mathematics, vol. 14, no. 3, pp. 855–878, 2023

2023

-

[38]

Optimal control of conditional value-at-risk in continuous time,

C. W. Miller and I. Yang, “Optimal control of conditional value-at-risk in continuous time,”SIAM Journal on Control and Optimization, vol. 55, no. 2, pp. 856–884, 2017

2017

-

[39]

Multiobjective portfolio optimization: bridging mathematical theory with asset management practice,

P. Xidonas, C. Hassapis, G. Mavrotas, C. Staikouras, and C. Zopounidis, “Multiobjective portfolio optimization: bridging mathematical theory with asset management practice,”Annals of Operations Research, vol. 267, pp. 585–606, 2018

2018

-

[40]

H. M. Markowitz and G. P. Todd,Mean-variance analysis in portfolio choice and capital markets. John Wiley & Sons, 2000, vol. 66, no. 4

2000

-

[41]

The fundamental approximation theorem of portfolio analysis in terms of means, variances and higher moments,

P. A. Samuelson, “The fundamental approximation theorem of portfolio analysis in terms of means, variances and higher moments,”The Review of Economic Studies, vol. 37, no. 4, pp. 537–542, 1970

1970

-

[42]

Jorion,Value at Risk: The New Benchmark for Controlling Market Risk

P. Jorion,Value at Risk: The New Benchmark for Controlling Market Risk. McGraw-Hill, 1997. [Online]. Available: https://books.google.co.in/books?id=u8efQgAACAAJ

1997

-

[43]

Optimization of conditional value-at-risk,

R. T. Rockafellar, S. Uryasevet al., “Optimization of conditional value-at-risk,”Journal of risk, vol. 2, pp. 21–42, 2000

2000

-

[44]

A mean-absolute deviation-skewness portfolio optimiza- tion model,

H. Konno, H. Shirakawa, and H. Yamazaki, “A mean-absolute deviation-skewness portfolio optimiza- tion model,”Annals of Operations Research, vol. 45, no. 1, pp. 205–220, 1993

1993

-

[45]

A minimax portfolio selection rule with linear programming solution,

M. R. Young, “A minimax portfolio selection rule with linear programming solution,”Management science, vol. 44, no. 5, pp. 673–683, 1998

1998

-

[46]

The characteristics of portfolios selected by n-degree lower partial moment,

D. N. Nawrocki, “The characteristics of portfolios selected by n-degree lower partial moment,”Inter- national Review of Financial Analysis, vol. 1, no. 3, pp. 195–209, 1992

1992

-

[47]

Non-separation in the mean–lower-partial-moment portfolio opti- mization problem,

A. J. Brogan and S. Stidham Jr, “Non-separation in the mean–lower-partial-moment portfolio opti- mization problem,”European Journal of Operational Research, vol. 184, no. 2, pp. 701–710, 2008. 24

2008

-

[48]

A machine learning approach to volatility forecasting,

K. Christensen, M. Siggaard, and B. Veliyev, “A machine learning approach to volatility forecasting,” Journal of Financial Econometrics, vol. 21, no. 5, pp. 1680–1727, 2023

2023

-

[49]

Portfolio optimization with return prediction using deep learning and machine learning,

Y. Ma, R. Han, and W. Wang, “Portfolio optimization with return prediction using deep learning and machine learning,”Expert Systems with Applications, vol. 165, p. 113973, 2021

2021

-

[50]

Matrix evolutions: Synthetic correlations and explainable machine learning for constructing robust investment portfolios,

J. Papenbrock, P. Schwendner, M. Jaeger, and S. Krügel, “Matrix evolutions: Synthetic correlations and explainable machine learning for constructing robust investment portfolios,”The Journal of Financial Data Science, vol. 3, no. 2, pp. 51–69, 2021

2021

-

[51]

Real-time portfolio management system utilizing machine learning techniques,

P. K. Aithal, M. Geetha, U. Dinesh, B. Savitha, and P. Menon, “Real-time portfolio management system utilizing machine learning techniques,”IEEE Access, vol. 11, pp. 32595–32608, 2023

2023

-

[52]

Portfolio selection under non-gaussianity and systemic risk: A machine learning based forecasting approach,

W. Lin and A. Taamouti, “Portfolio selection under non-gaussianity and systemic risk: A machine learning based forecasting approach,”International Journal of Forecasting, 2023

2023

-

[53]

Empirical asset pricing via machine learning,

S. Gu, B. Kelly, and D. Xiu, “Empirical asset pricing via machine learning,”The Review of Financial Studies, vol. 33, no. 5, pp. 2223–2273, 2020

2020

-

[54]

A multi-layer and multi- ensemble stock trader using deep learning and deep reinforcement learning,

S. Carta, A. Corriga, A. Ferreira, A. S. Podda, and D. R. Recupero, “A multi-layer and multi- ensemble stock trader using deep learning and deep reinforcement learning,”Applied Intelligence, vol. 51, pp. 889–905, 2021

2021

-

[55]

Deep direct reinforcement learning for financial signal representation and trading,

Y. Deng, F. Bao, Y. Kong, Z. Ren, and Q. Dai, “Deep direct reinforcement learning for financial signal representation and trading,”IEEE transactions on neural networks and learning systems, vol. 28, no. 3, pp. 653–664, 2016

2016

-

[56]

Deep reinforcement learning for market making in corporate bonds: beating the curse of dimensionality,

O. Guéant and I. Manziuk, “Deep reinforcement learning for market making in corporate bonds: beating the curse of dimensionality,”Applied Mathematical Finance, vol. 26, no. 5, pp. 387–452, 2019

2019

-

[58]

Financial portfolio optimization with online deep reinforcement learn- ing and restricted stacked autoencoder—deepbreath,

F. Soleymani and E. Paquet, “Financial portfolio optimization with online deep reinforcement learn- ing and restricted stacked autoencoder—deepbreath,”Expert Systems with Applications, vol. 156, p. 113456, 2020

2020

-

[59]

Portfolio management via two-stage deep learning with a joint cost,

H. Yun, M. Lee, Y. S. Kang, and J. Seok, “Portfolio management via two-stage deep learning with a joint cost,”Expert Systems with Applications, vol. 143, p. 113041, 2020

2020

-

[60]

Stock price prediction using the rnn model,

Y. Zhu, “Stock price prediction using the rnn model,” inJournal of Physics: Conference Series, vol. 1650, no. 3. IOP Publishing, 2020, p. 032103

2020

-

[61]

A Deep Reinforcement Learning Framework for the Financial Portfolio Management Problem

Z. Jiang, D. Xu, and J. Liang, “A deep reinforcement learning framework for the financial portfolio management problem,”arXiv preprint arXiv:1706.10059, 2017

work page Pith review arXiv 2017

-

[62]

Adversarial deep reinforcement learning in portfolio management,

Z. Liang, H. Chen, J. Zhu, K. Jiang, and Y. Li, “Adversarial deep reinforcement learning in portfolio management,” 2018

2018

-

[63]

Testing different reinforcement learning configurations for financial trading: Introduction and applications,

F. Bertoluzzo and M. Corazza, “Testing different reinforcement learning configurations for financial trading: Introduction and applications,”Procedia Economics and Finance, vol. 3, pp. 68–77, 2012

2012

-

[64]

Deep learning for decision making and the optimization of socially responsible investments and portfolio,

N. N. Vo, X. He, S. Liu, and G. Xu, “Deep learning for decision making and the optimization of socially responsible investments and portfolio,”Decision Support Systems, vol. 124, p. 113097, 2019

2019

-

[65]

Adaptive portfolio asset allo- cation optimization with deep learning,

S. Obeidat, D. Shapiro, M. Lemay, M. K. MacPherson, and M. Bolic, “Adaptive portfolio asset allo- cation optimization with deep learning,”International Journal on Advances in Intelligent Systems, vol. 11, no. 1, pp. 25–34, 2018. 25

2018

-

[66]

A universal end-to-end approach to portfolio optimization via deep learning,

C. Zhang, Z. Zhang, M. Cucuringu, and S. Zohren, “A universal end-to-end approach to portfolio optimization via deep learning,”arXiv preprint arXiv:2111.09170, 2021

-

[67]

Intelligent investment portfolio management using time- series analytics and deep reinforcement learning,

S. Chavan, P. Kumar, and T. Gianelle, “Intelligent investment portfolio management using time- series analytics and deep reinforcement learning,”SMU Data Science Review, vol. 5, no. 2, p. 7, 2021

2021

-

[68]

Deep learning approach for short-term stock trends prediction based on two-stream gated recurrent unit network,

D. L. Minh, A. Sadeghi-Niaraki, H. D. Huy, K. Min, and H. Moon, “Deep learning approach for short-term stock trends prediction based on two-stream gated recurrent unit network,”Ieee Access, vol. 6, pp. 55392–55404, 2018

2018

-

[69]

Research on quantitative investment strategies based on deep learn- ing,

Y. Fang, J. Chen, and Z. Xue, “Research on quantitative investment strategies based on deep learn- ing,”Algorithms, vol. 12, no. 2, p. 35, 2019

2019

-

[70]

Leveraging deep learning with lda-based text analytics to detect automobile insurance fraud,

Y. Wang and W. Xu, “Leveraging deep learning with lda-based text analytics to detect automobile insurance fraud,”Decision Support Systems, vol. 105, pp. 87–95, 2018

2018

-

[71]

Distributed deep learning based lan- guage technologies to augment anti money laundering investigation

J. Han, U. Barman, J. Hayes, J. Du, E. Burgin, and D. Wan, “Distributed deep learning based lan- guage technologies to augment anti money laundering investigation.” Association for Computational Linguistics, 2018, pp. 37–42

2018

-

[72]

Macroeconomic indicator forecasting with deep neural networks,

A. Smalter Hall and T. R. Cook, “Macroeconomic indicator forecasting with deep neural networks,” Federal Reserve Bank of Kansas City Working Paper, no. 17-11, 2017

2017

-

[73]

Exploring the use of deep neural networks for sales forecasting in fashion retail,

A. L. Loureiro, V. L. Miguéis, and L. F. Da Silva, “Exploring the use of deep neural networks for sales forecasting in fashion retail,”Decision Support Systems, vol. 114, pp. 81–93, 2018

2018

-

[74]

Tackling business intelligence with bioinspired deep learning,

J. Fombellida, I. Martín Rubio, S. Torres Alegre, and D. Andina, “Tackling business intelligence with bioinspired deep learning,”Neural Computing and Applications, vol. 32, pp. 13195–13202, 2020

2020

-

[75]

Credit risk analysis using machine and deep learning models,

P. M. Addo, D. Guegan, and B. Hassani, “Credit risk analysis using machine and deep learning models,”Risks, vol. 6, no. 2, p. 38, 2018

2018

-

[76]

Prediction of stock value using pattern matching algorithm based on deep learning,

Y. H. Go and J. K. Hong, “Prediction of stock value using pattern matching algorithm based on deep learning,”International Journal of Recent Technology and Engineering, vol. 8, no. 2, pp. 31–35, 2019

2019

-

[77]

Portfolio formation with preselection using deep learning from long-term financial data,

W. Wang, W. Li, N. Zhang, and K. Liu, “Portfolio formation with preselection using deep learning from long-term financial data,”Expert Systems with Applications, vol. 143, p. 113042, 2020

2020

-

[78]

A study on novel filtering and relationship between input-features and target-vectors in a deep learning model for stock price prediction,

Y. Song, J. W. Lee, and J. Lee, “A study on novel filtering and relationship between input-features and target-vectors in a deep learning model for stock price prediction,”Applied Intelligence, vol. 49, pp. 897–911, 2019

2019

-

[79]

Deep-learning solution to portfolio selection with serially dependent returns,

K. H. Tsang and H. Y. Wong, “Deep-learning solution to portfolio selection with serially dependent returns,”SIAM Journal on Financial Mathematics, vol. 11, no. 2, pp. 593–619, 2020

2020

-

[80]

Deep investment in financial markets using deep learning models,

S. Aggarwal and S. Aggarwal, “Deep investment in financial markets using deep learning models,” International Journal of Computer Applications, vol. 162, no. 2, pp. 40–43, 2017

2017

-

[81]

A survey of forex and stock price prediction using deep learning,

Z. Hu, Y. Zhao, and M. Khushi, “A survey of forex and stock price prediction using deep learning,” Applied System Innovation, vol. 4, no. 1, p. 9, 2021

2021

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.