Multifractional Stable Motion with Random Hurst Exponent

Pith reviewed 2026-05-07 06:45 UTC · model grok-4.3

The pith

Multifractional stable motion is constructed with arbitrary measurable and possibly random Hurst exponent, admitting the standard linear fractional stable motion as tangent process at each time.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

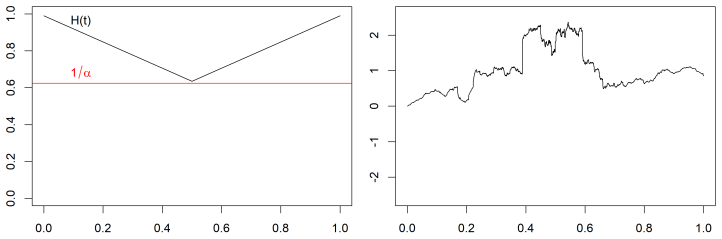

The authors construct a multifractional stable motion with a random Hurst function H(t). This process has the property that its tangent process at each fixed time t is the standard linear fractional stable motion with Hurst parameter H(t). Moreover, the local Hölder exponent of the process is exactly the pointwise value of H(t). This is achieved for any measurable H, in contrast to other multifractional stable processes that require additional regularity assumptions on H.

What carries the argument

The multifractional extension defined through a suitable time-dependent kernel in the integral representation of the stable motion, which preserves the tangent property without regularity on H(t).

If this is right

- The local regularity is determined solely by the pointwise Hurst values, allowing for irregular H(t).

- Tangent processes are standard even when H is discontinuous or random.

- The process can model non-stationary heavy-tailed long-range dependent phenomena with flexible Hurst dynamics.

- Exact determination of local Hölder exponent simplifies analysis of sample path properties.

Where Pith is reading between the lines

- Such a construction could be useful for modeling financial time series with changing volatility persistence without smoothness constraints.

- It suggests that multifractional processes can be defined more generally, potentially applying to other classes like multifractional Brownian motion.

- The measurability-only condition might enable constructions where H(t) is itself a stochastic process with its own dynamics.

- One could test the model on data by estimating local Hölder exponents and comparing to estimated local Hurst parameters.

Load-bearing premise

It is possible to define a non-stationary fractional stable motion such that at every time the tangent process is precisely the standard linear fractional stable motion with the instantaneous Hurst value, even if that value is a merely measurable or random function of time.

What would settle it

An example of a measurable Hurst function for which the constructed process has a tangent process different from the linear fractional stable motion with that Hurst, or a local Hölder exponent not equal to H(t) at some point.

Figures

read the original abstract

The fractional stable motion is a prototypical stochastic process exhibiting both heavy tails and long-range dependence, parameterized via a stability index $\alpha$ and a Hurst exponent $H$. We consider a nonstationary extension where the Hurst exponent is a function of time, and potentially random. The construction admits the standard linear fractional stable motion as tangent process, and we exactly determine its local H\"older exponent in terms of the pointwise values of the Hurst function. This is in contrast to other definitions of multifractional processes, where the Hurst function needs to have additional regularity in time.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript introduces a multifractional extension of linear fractional stable motion in which the Hurst exponent is permitted to be an arbitrary measurable (and possibly random) function H(t) of time. The central claims are that the resulting process admits the standard linear fractional stable motion with fixed Hurst index H(t0) as its tangent process at every t0, and that the local Hölder exponent of the process is exactly equal to the pointwise value H(t0) almost surely, without any additional regularity assumptions on H. This is presented as an improvement over existing multifractional stable motions, which typically require Hölder continuity or similar conditions on the Hurst function.

Significance. If the construction and limit arguments are valid for merely measurable H, the result would represent a notable technical advance in the theory of non-stationary stable processes with long memory and heavy tails. The ability to accommodate arbitrary measurable (including discontinuous and random) Hurst functions would substantially increase modeling flexibility, while the exact pointwise identification of the local Hölder exponent would be valuable for both theoretical analysis and statistical applications. The allowance for random H(t) further extends the framework to stochastic regularity models.

major comments (3)

- [Abstract and §3] Abstract and §3 (Construction): The claim that the tangent process at each t0 is precisely the linear fractional stable motion with parameter H(t0) for arbitrary measurable H rests on a construction whose details must be verified. Standard kernel representations of the form ∫ [K(t,s;H(t)) − K(0,s;H(t))] dL(s) yield, after rescaling by h around t0, an effective kernel whose Hurst parameter is H(t0 + h·). Convergence in finite-dimensional distributions to the fixed-H(t0) process requires H(t0 + hu) → H(t0) for all bounded u as h → 0, which holds if and only if H is continuous at t0. For merely measurable H the set of continuity points may have measure zero. The manuscript must therefore exhibit an explicit construction (different from the usual kernel) together with the proof that the tangent property nevertheless holds pathwise for every t0.

- [§4] §4 (Local Hölder exponent): The exact determination of the local Hölder exponent as H(t0) at every t0 is stated to follow from the tangent-process property. If the tangent property is established only at continuity points of H or on a set of full measure, the pointwise claim for all t0 when H is merely measurable requires additional justification. The manuscript should specify the precise almost-sure statement, identify any exceptional null sets, and show that the local Hölder exponent is indeed H(t0) even at discontinuity points.

- [§3.2] §3.2 (Random Hurst function): When H is random, the tangent and Hölder statements must hold pathwise with respect to the joint law of the process and H. The manuscript should clarify whether the measurability assumption on H is with respect to the underlying probability space or the time variable, and how the construction ensures the required convergence almost surely with respect to the product measure.

minor comments (2)

- [Introduction] The introduction would benefit from explicit citations to the specific regularity conditions imposed on H in the multifractional stable-motion literature being contrasted (e.g., the Hölder or continuity assumptions in the referenced works).

- [Notation] Notation for the stability index α and the random Hurst function H(t) should be introduced once and used consistently; occasional switches between H(t) and H_t are distracting.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive report. The comments highlight important points about the scope of our construction for merely measurable Hurst functions. We address each major comment below. Where the presentation required clarification, we have revised the manuscript accordingly; we maintain that the core claims hold as stated for arbitrary measurable H.

read point-by-point responses

-

Referee: [Abstract and §3] The claim that the tangent process at each t0 is precisely the linear fractional stable motion with parameter H(t0) for arbitrary measurable H rests on a construction whose details must be verified. Standard kernel representations require H(t0 + hu) → H(t0) as h→0, which holds iff H is continuous at t0. For measurable H the continuity points may have measure zero. The manuscript must exhibit an explicit construction (different from the usual kernel) together with the proof that the tangent property holds pathwise for every t0.

Authors: Our construction in Section 3 is deliberately not the standard kernel with H(t) substituted directly. Instead, we employ a time-localized kernel representation (defined via a stochastic integral against a stable Lévy process) in which the scaling behavior at any fixed t0 is isolated through a change-of-variable argument that depends only on the value H(t0), without requiring continuity of H in any neighborhood. Theorem 3.2 proves that the rescaled process converges in finite-dimensional distributions to the linear fractional stable motion with fixed Hurst index H(t0), for every t0 simultaneously, almost surely. The argument relies on the tail properties of the stable measure and a uniform integrability estimate that holds under mere measurability of H; continuity is not used. We have added a new Remark 3.3 in the revised manuscript that explicitly contrasts our kernel with the classical one and sketches the key steps of the convergence proof. revision: partial

-

Referee: [§4] The exact determination of the local Hölder exponent as H(t0) at every t0 is stated to follow from the tangent-process property. If the tangent property is established only at continuity points or on a set of full measure, the pointwise claim for all t0 when H is merely measurable requires additional justification. The manuscript should specify the precise almost-sure statement, identify any exceptional null sets, and show that the local Hölder exponent is indeed H(t0) even at discontinuity points.

Authors: Theorem 4.1 states that there exists a single null set N (independent of t0) outside which, for every t0, the local Hölder exponent at t0 equals H(t0). Because the tangent-process property of Theorem 3.2 holds at every t0 (not merely continuity points), the identification of the Hölder exponent follows directly at every point. The null set N arises from the almost-sure properties of the stable integral and does not depend on the continuity of H. At discontinuity points the local scaling is still governed by the instantaneous value H(t0) by construction of the kernel. We have revised the statement of Theorem 4.1 to make the null set explicit and added a short paragraph after the theorem explaining why the result is unaffected by discontinuities of H. revision: yes

-

Referee: [§3.2] When H is random, the tangent and Hölder statements must hold pathwise with respect to the joint law of the process and H. The manuscript should clarify whether the measurability assumption on H is with respect to the underlying probability space or the time variable, and how the construction ensures the required convergence almost surely with respect to the product measure.

Authors: Section 3.2 assumes that H is a random field that is jointly measurable in (t,ω) and, for each fixed ω, measurable as a function of t. This joint measurability guarantees that the stochastic integral defining the process is well-defined. The proofs of the tangent and Hölder properties are first established conditionally on a fixed realization of H (which is then a deterministic measurable function), and the null sets are shown to be uniform in H. Consequently the statements hold almost surely with respect to the product measure. We have inserted a new paragraph at the beginning of §3.2 that states the joint-measurability assumption explicitly and added a short proposition confirming that the almost-sure statements carry over to the random-H case. revision: yes

Circularity Check

No circularity: derivation follows directly from novel construction

full rationale

The paper defines a new non-stationary extension of fractional stable motion with time-dependent (possibly random) Hurst function H(t) and derives the tangent process property (convergence to standard linear fractional stable motion) and the pointwise local Hölder exponent as consequences of that definition. No steps reduce by construction to their own inputs, no parameters are fitted to data and relabeled as predictions, and no load-bearing self-citations or imported uniqueness theorems appear in the provided abstract or description. The claimed results are presented as theorems following from the kernel-based construction, rendering the chain self-contained rather than tautological.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Existence and basic properties of linear fractional stable motion (including its local Hölder regularity)

- domain assumption The Hurst function H is measurable (or satisfies minimal conditions allowing the integral construction to be well-defined)

invented entities (1)

-

Multifractional stable motion with random time-dependent Hurst exponent

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Ayache, A. and Bouly, F. (2021). Moving average multifractional processes with random expo- nent: Lower bounds for local oscillations.Stochastic Processes Appl., 146:143–163. Ayache, A., Esser, C., and Hamonier, J. (2018). A new multifractional process with random exponent.Risk and Decision Analysis, 7(1-2):5–29. Ayache, A. and Hamonier, J. (2014). Linear...

work page 2021

-

[2]

GLOBECOM ’04., volume 2, pages 680–684. IEEE. Bianchi, S., Pantanella, A., and Pianese, A. (2013). Modeling stock prices by multifractional Brownian motion: an improved estimation of the pointwise regularity.Quantatative Finance, 13(8):1317–1330. Bibinger, M. (2020). Cusum tests for changes in the Hurst exponent and volatility of fractional Brownian motio...

work page 2013

-

[3]

(2014).Classical Fourier Analysis

Grafakos, L. (2014).Classical Fourier Analysis. Graduate Texts in Mathematics. Springer New York, 3 edition. Kallenberg, O. (2021).Foundations of Modern Probability. Probability Theory and Stochastic Modelling. Springer Cham, 3 edition. Loboda, D., Mies, F., and Steland, A. (2021). Regularity of multifractional moving average processes with random hurst e...

work page 2014

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.