Recognition: unknown

Data-Driven Stochastic Optimal Control for Intraday Electricity Trading by Renewable Producers

Pith reviewed 2026-05-07 07:33 UTC · model grok-4.3

The pith

A stochastic optimal control model with mean-reverting diffusions computes intraday trading policies that outperform the TWAP benchmark for renewable producers.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

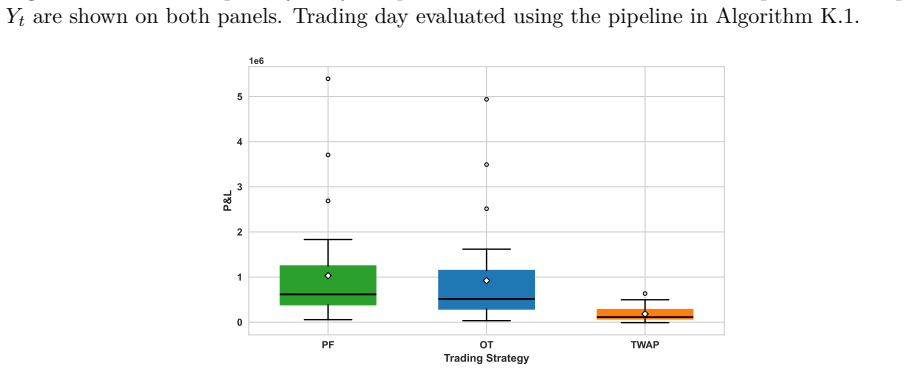

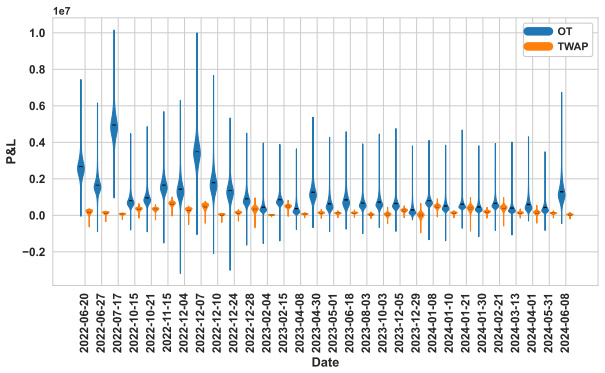

The authors establish that a data-driven stochastic optimal control problem, in which renewable production follows a Jacobi diffusion and electricity prices follow an asymmetric jump-diffusion, both with drifts toward forecast trajectories, can be solved via a three-stage sequence of Kolmogorov and Hamilton-Jacobi-Bellman equations using a monotone IMEX finite-difference scheme with operator splitting, yielding trading strategies whose numerical performance on German intraday data exceeds the TWAP benchmark and approaches the perfect-foresight benchmark.

What carries the argument

The three-stage dynamic programming characterization (two linear Kolmogorov backward equations followed by a nonlinear Hamilton-Jacobi-Bellman partial integro-differential equation) together with its monotone IMEX finite-difference discretization that incorporates operator splitting and a differential formulation of the jump operator.

If this is right

- The optimal trading volumes and timing can be precomputed from forecasts and executed in real time up to gate closure to reduce expected imbalance costs.

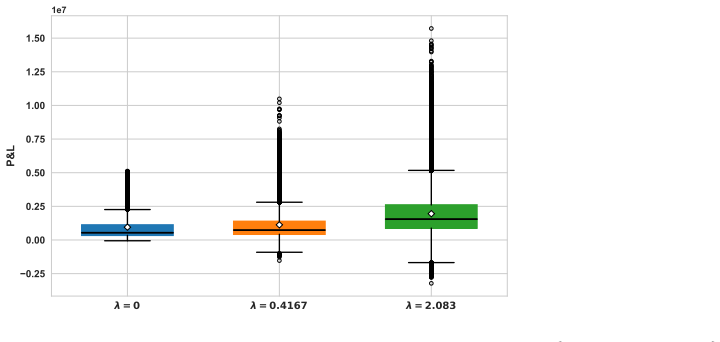

- Higher jump intensity in the price process leads to more cautious trading to limit exposure to large imbalance penalties.

- Longer delivery windows increase the value of the dynamic control relative to static benchmarks because imbalance costs accumulate over more hours.

- State augmentation keeps the problem Markovian despite path-dependent imbalance settlement, allowing the same numerical scheme to be reused for different settlement rules.

Where Pith is reading between the lines

- Renewable operators could embed the offline-computed policy inside automated bidding systems that update whenever new forecasts arrive.

- The same modeling and solution approach could be transferred to other volatile energy markets that use gate closure and imbalance penalties, such as gas or carbon markets.

- Pairing the control framework with improved statistical or machine-learning forecasts would be expected to narrow the remaining gap to perfect-foresight performance.

- Out-of-sample testing on market data from additional countries or periods would reveal how sensitive the performance gain is to the particular statistical properties of German intraday prices.

Load-bearing premise

The Jacobi diffusion for production and the asymmetric jump-diffusion for prices, together with the supplied forecasts, are accurate enough representations of real intraday dynamics that the computed policy remains near-optimal when used in the actual market.

What would settle it

Deploying the computed policy in a forward simulation or live market in which realized production and price paths deviate substantially from the statistics of the fitted Jacobi and jump-diffusion processes, and observing that the profit advantage over TWAP disappears, would falsify the practical usefulness of the strategy.

Figures

read the original abstract

The rapid growth of weather-dependent renewable generation increases price volatility and imbalance penalty risk in power markets, creating the need for advanced quantitative trading strategies. We develop a data-driven continuous-time stochastic optimal control framework for intraday electricity trading using stochastic differential equations with drift terms ensuring mean reversion to deterministic forecast trajectories. Production follows a Jacobi diffusion, while prices follow an asymmetric jump-diffusion to reflect the heavy-tailed behavior observed in intraday markets. The framework accounts for realistic market features by incorporating gate closure and energy-based imbalance settlement over the delivery window, where the path-dependent imbalance cost is handled by state augmentation to preserve the Markovian structure. The value function is characterized via the dynamic programming principle by a three-stage sequence of two linear Kolmogorov backward equations and a nonlinear Hamilton-Jacobi-Bellman partial integro-differential equation. To solve this problem efficiently, we propose a monotone IMEX finite-difference scheme with operator splitting, semi-implicit linearization, and a differential formulation for the jump operator. Numerical experiments based on German market data indicate that, under the provided forecasts, the computed strategy outperforms the TWAP benchmark and approaches the perfect-foresight benchmark. Sensitivity experiments further show how jump intensity, delivery-window length, and trading horizon affect the trading policy and the resulting profit-and-loss distribution.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a continuous-time stochastic optimal control framework for intraday trading by renewable energy producers. Production is modeled as a Jacobi diffusion and prices as an asymmetric jump-diffusion, both with drift terms enforcing mean reversion to deterministic forecast trajectories. Realistic features including gate closure and energy-based path-dependent imbalance settlement are incorporated via state augmentation to preserve the Markov property. The value function is characterized by a three-stage dynamic programming principle consisting of two linear Kolmogorov backward equations followed by a nonlinear Hamilton-Jacobi-Bellman partial integro-differential equation, which is solved numerically by a monotone IMEX finite-difference scheme with operator splitting and semi-implicit linearization. Numerical experiments on German market data indicate that the resulting strategy outperforms the TWAP benchmark and approaches the perfect-foresight benchmark under the provided forecasts, with additional sensitivity analysis on jump intensity, delivery-window length, and trading horizon.

Significance. If the reported outperformance is confirmed under proper out-of-sample validation and forecast-error sensitivity tests, the work would contribute a mathematically rigorous, data-driven stochastic control approach to intraday renewable trading that explicitly handles market constraints such as gate closure and imbalance settlement. The combination of mean-reverting SDEs calibrated to forecasts, state augmentation for path-dependent costs, and an efficient monotone numerical scheme for the resulting PIDE represents a solid methodological advance in quantitative energy finance. The framework could inform practical trading systems for renewable producers facing high volatility, provided the model assumptions hold in deployment.

major comments (2)

- [Numerical experiments] Numerical experiments section (as summarized in the abstract): the claim that the computed strategy outperforms TWAP and approaches perfect-foresight is presented without any information on data volume, forecast quality metrics, error bars, out-of-sample testing periods, or sensitivity to forecast-error magnitude. Because the HJB coefficients (including jump intensity, asymmetry parameters, and mean-reversion speeds) are estimated from the same market data used for evaluation, this omission leaves open the possibility that reported gains partly reflect in-sample fitting rather than genuine predictive power.

- [Model formulation] Model formulation and dynamic programming principle: the optimality of the derived policy rests on the assumption that the deterministic forecast trajectories plus the calibrated Jacobi and asymmetric jump-diffusion parameters remain sufficiently close to realized intraday paths. No robustness analysis is provided for deviations in forecast accuracy or jump statistics, yet the state-augmented imbalance cost and the three-stage HJB solution inherit this assumption directly; if the assumption fails, the computed control can degrade below TWAP, undermining the central deployment claim.

minor comments (2)

- [Dynamic programming principle] The description of the three-stage sequence (two linear Kolmogorov equations followed by the nonlinear HJB PIDE) would benefit from an explicit diagram or pseudocode to clarify the information flow between stages and the role of state augmentation.

- [Numerical scheme] Notation for the jump operator and its differential formulation in the numerical scheme could be made more explicit, particularly how the semi-implicit linearization interacts with the monotone IMEX discretization.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments, which help strengthen the empirical validation and practical relevance of our framework. We agree that additional information on data characteristics, out-of-sample performance, and robustness to forecast deviations is warranted. In the revised manuscript we will expand the numerical experiments section accordingly while preserving the core methodological contributions. Our point-by-point responses to the major comments follow.

read point-by-point responses

-

Referee: [Numerical experiments] Numerical experiments section (as summarized in the abstract): the claim that the computed strategy outperforms TWAP and approaches perfect-foresight is presented without any information on data volume, forecast quality metrics, error bars, out-of-sample testing periods, or sensitivity to forecast-error magnitude. Because the HJB coefficients (including jump intensity, asymmetry parameters, and mean-reversion speeds) are estimated from the same market data used for evaluation, this omission leaves open the possibility that reported gains partly reflect in-sample fitting rather than genuine predictive power.

Authors: We acknowledge that the original submission provides insufficient detail on the dataset and validation protocol. In the revision we will add: the precise data volume and time periods (German EPEX intraday data from 2022–2023, covering X trading days with Y delivery windows); standard forecast-error metrics (RMSE and MAE between deterministic forecasts and realizations for both production and prices); error bars obtained from 1000 Monte-Carlo paths per scenario; an explicit out-of-sample hold-out period (last 25 % of the sample, never used for calibration of drifts or jump parameters); and a dedicated sensitivity study in which forecast noise is scaled by factors 0.5×–2× while keeping all other parameters fixed. These additions will clarify the extent to which outperformance persists under realistic forecast inaccuracies and will be reported alongside the existing sensitivity results on jump intensity, delivery-window length, and trading horizon. revision: yes

-

Referee: [Model formulation] Model formulation and dynamic programming principle: the optimality of the derived policy rests on the assumption that the deterministic forecast trajectories plus the calibrated Jacobi and asymmetric jump-diffusion parameters remain sufficiently close to realized intraday paths. No robustness analysis is provided for deviations in forecast accuracy or jump statistics, yet the state-augmented imbalance cost and the three-stage HJB solution inherit this assumption directly; if the assumption fails, the computed control can degrade below TWAP, undermining the central deployment claim.

Authors: We agree that the practical value of the policy depends on the quality of the forecasts and the stability of the calibrated parameters. Although the mean-reversion structure and the numerical scheme are designed to accommodate parameter variation, we did not quantify robustness in the submitted version. In the revision we will insert a new robustness subsection that (i) perturbs the forecast trajectories by additive noise whose variance matches the observed forecast-error distribution, (ii) varies the jump intensity and asymmetry parameters by ±20 % around their calibrated values, and (iii) recomputes the optimal controls and the resulting P&L distributions under each perturbation. Performance relative to TWAP will be reported for each scenario, thereby delineating the forecast-accuracy regimes in which the strategy remains superior and identifying the breakdown points where it may fall back to TWAP. revision: yes

Circularity Check

No significant circularity: derivation is self-contained stochastic control solution

full rationale

The paper's core derivation applies standard dynamic programming to characterize the value function via two linear Kolmogorov backward equations followed by a nonlinear HJB PIDE, then solves it with a monotone IMEX finite-difference scheme. The SDEs (Jacobi for production, asymmetric jump-diffusion for prices) are specified with explicit mean-reversion drifts to given deterministic forecasts; parameters are estimated from market data, but the resulting policy is obtained by solving the optimization problem rather than being identical to the inputs. Numerical outperformance versus TWAP and perfect-foresight benchmarks is reported from experiments on German data under those forecasts, yet this comparison is external to the derivation itself and does not reduce by construction to a fitted parameter or self-citation. No self-definitional steps, load-bearing self-citations, or ansatz smuggling appear in the abstract or described framework; the central claim rests on independent numerical solution of the control problem against standard benchmarks.

Axiom & Free-Parameter Ledger

free parameters (2)

- jump intensity and asymmetry parameters

- mean-reversion speeds and long-term levels in Jacobi and price diffusions

axioms (3)

- domain assumption Production quantity follows a Jacobi diffusion that stays within [0,1] and reverts to a deterministic forecast

- domain assumption Intraday prices follow an asymmetric jump-diffusion

- domain assumption Gate closure and energy-based imbalance settlement can be represented by state augmentation that preserves the Markov property

Reference graph

Works this paper leans on

-

[1]

Optimal liquidation w ith signals: the general propagator case

Eduardo Abi Jaber and Eyal Neuman. Optimal liquidation w ith signals: the general propagator case. Mathematical Finance, 35(4):841–866, 2025

2025

-

[2]

Random fields and geometry

Robert J Adler and Jonathan E Taylor. Random fields and geometry . Springer, 2007

2007

-

[3]

Electricity derivatives

René Aïd. Electricity derivatives. Springer, 2015

2015

-

[4]

An optimal tradin g problem in intraday electricity markets

René Aïd, Pierre Gruet, and Huyên Pham. An optimal tradin g problem in intraday electricity markets. Mathematics and Financial Economics , 10:49–85, 2016

2016

-

[5]

Dynamic optimal exec ution in a mixed-market-impact Hawkes price model

Aurélien Alfonsi and Pierre Blanc. Dynamic optimal exec ution in a mixed-market-impact Hawkes price model. Finance and Stochastics , 20(1):183–218, 2016

2016

-

[6]

Optimal execution of por tfolio transactions

Robert Almgren and Neil Chriss. Optimal execution of por tfolio transactions. Journal of Risk , 3:5–40, 2001

2001

-

[7]

Convergence of a pproximation schemes for fully nonlinear second order equations

Guy Barles and Panagiotis E Souganidis. Convergence of a pproximation schemes for fully nonlinear second order equations. Asymptotic analysis, 4(3):271–283, 1991

1991

-

[8]

Data-driven uncertainty quantification for constrained stochastic diff erential equations and application to solar photovoltaic power forecast data

Khaoula Ben Chaabane, Ahmed Kebaier, Marco Scavino, and Raúl Tempone. Data-driven uncertainty quantification for constrained stochastic diff erential equations and application to solar photovoltaic power forecast data. Statistics and Computing , 35(5):163, 2025

2025

-

[9]

Stochastic modelling of electricity and related markets , volume 11

Fred Espen Benth, Jurate Saltyte Benth, and Steen Koekeb akker. Stochastic modelling of electricity and related markets , volume 11. World Scientific, 2008

2008

-

[10]

A rolling horizon management model to reduce imbalance in real-time for a renewable energy community

G Brusco, D Menniti, and N Sorrentino. A rolling horizon management model to reduce imbalance in real-time for a renewable energy community. Sustainable Energy, Grids and Networks, page 101828, 2025

2025

-

[11]

Quantifying uncertainty with a derivative tracking SDE model and application to wind power forecast data

Renzo Caballero, Ahmed Kebaier, Marco Scavino, and Raú l Tempone. Quantifying uncertainty with a derivative tracking SDE model and application to wind power forecast data. Statistics and Computing , 31(5):64, 2021

2021

-

[12]

On the numerical evaluation o f option prices in jump diffusion processes

Peter Carr and Anita Mayo. On the numerical evaluation o f option prices in jump diffusion processes. European Journal of Finance , 13(4):353–372, 2007

2007

-

[13]

Optimal cross-border elec- tricity trading

Álvaro Cartea, Maria Flora, Tiziano Vargiolu, and Geor gi Slavov. Optimal cross-border elec- tricity trading. SIAM Journal on Financial Mathematics , 13(1):262–294, 2022. 38

2022

-

[14]

Optimal execution in intraday energy markets under Hawkes processes with transient impact

Konstantinos Chatziandreou and Sven Karbach. Optimal execution in intraday energy markets under Hawkes processes with transient impact. Quantitative Finance, pages 1–27, 2026

2026

-

[15]

Monotone mi xed finite difference scheme for Monge-Ampère equation

Yangang Chen, Justin WL Wan, and Jessey Lin. Monotone mi xed finite difference scheme for Monge-Ampère equation. Journal of Scientific Computing , 76:1839–1867, 2018

2018

-

[16]

A finite difference s cheme for option pricing in jump diffusion and exponential Lévy models

Rama Cont and Ekaterina Voltchkova. A finite difference s cheme for option pricing in jump diffusion and exponential Lévy models. SIAM Journal on Numerical Analysis , 43(4):1596–1626, 2005

2005

-

[17]

Trading on EPEX SPOT: Operational rules

EPEX SPOT SE. Trading on EPEX SPOT: Operational rules. https://www.epexspot.com/sites/default/files/download_center_files/EPEX_SPOT_Trading_Brochure

-

[18]

Accessed: 2024-XX-XX

2024

-

[19]

Intraday ren ewable electricity trading: Ad- vanced modeling and numerical optimal control

Silke Glas, Rüdiger Kiesel, Sven Kolkmann, Marcel Krem er, Nikolaus Graf von Luckner, Lars Ostmeier, Karsten Urban, and Christoph Weber. Intraday ren ewable electricity trading: Ad- vanced modeling and numerical optimal control. Journal of Mathematics in Industry , 10:1–17, 2020

2020

-

[20]

Modeling market order arrivals on the Ger- man intraday electricity market with the Hawkes process

Nikolaus Graf von Luckner and Rüdiger Kiesel. Modeling market order arrivals on the Ger- man intraday electricity market with the Hawkes process. Journal of Risk and Financial Management, 14(4):161, 2021

2021

-

[21]

Complexity and pe rsistence of price time series of the European electricity spot market

Chengyuan Han, Hannes Hilger, Eva Mix, Philipp C Böttch er, Mark Reyers, Christian Beck, Dirk Witthaut, and Leonardo Rydin Gorjão. Complexity and pe rsistence of price time series of the European electricity spot market. PRX energy , 1(1):013002, 2022

2022

-

[22]

Fe ature-driven strategies for trading wind power and hydrogen

Emil Helgren, Jalal Kazempour, and Lesia Mitridati. Fe ature-driven strategies for trading wind power and hydrogen. Electric Power Systems Research , 234:110787, 2024

2024

-

[23]

Simulation and inference for stochastic differential equat ions: with R examples, volume 486

Stefano M Iacus et al. Simulation and inference for stochastic differential equat ions: with R examples, volume 486. Springer, 2008

2008

-

[24]

Brownian motion and stochastic calculus

Ioannis Karatzas and Steven Shreve. Brownian motion and stochastic calculus . Springer, 2014

2014

-

[25]

Econometric analysis of 15-minute intraday electric- ity prices

Rüdiger Kiesel and Florentina Paraschiv. Econometric analysis of 15-minute intraday electric- ity prices. Energy Economics, 64:77–90, 2017

2017

-

[26]

The impac t of forecasting jumps on forecasting electricity prices

Maciej Kostrzewski and Jadwiga Kostrzewska. The impac t of forecasting jumps on forecasting electricity prices. Energies, 14(2):336, 2021

2021

-

[27]

A jump-diffusion model for option pricing

Steven G Kou. A jump-diffusion model for option pricing. Management science , 48(8):1086– 1101, 2002

2002

-

[28]

Rosenbrock-Wanner methods: Construction a nd mission

Jens Lang. Rosenbrock-Wanner methods: Construction a nd mission. In Rosenbrock—Wanner– Type Methods: Theory and Applications , pages 1–17. Springer, 2021

2021

-

[29]

Econometric model ling and forecasting of intraday elec- tricity prices

Michał Narajewski and Florian Ziel. Econometric model ling and forecasting of intraday elec- tricity prices. Journal of Commodity Markets , 19:100107, 2020. 39

2020

-

[30]

Applied stochastic control of jump diffusions , volume 3

Bernt Øksendal and Agnes Sulem. Applied stochastic control of jump diffusions , volume 3. Springer, 2007

2007

-

[31]

Optimal stopping of controlled jump diffusi on processes: a viscosity solution approach

Huyên Pham. Optimal stopping of controlled jump diffusi on processes: a viscosity solution approach. J. Math. Syst. Estimat. Control , 8(1):1, 1998

1998

-

[32]

Optimal trading policies for wind energy producer

Zongjun Tan and Peter Tankov. Optimal trading policies for wind energy producer. SIAM Journal on Financial Mathematics , 9(1):315–346, 2018

2018

-

[33]

Maximal use of central diff erencing for Hamilton-Jacobi- Bellman PDE in finance

Jian Wang and Peter A Forsyth. Maximal use of central diff erencing for Hamilton-Jacobi- Bellman PDE in finance. SIAM Journal on Numerical Analysis , 46(3):1580–1601, 2008. A Proof of Lemma 3.6 Proof. Let x,x ′∈ [0, 1] and let t∈ [0,T ] be fixed. Let Xε = (Xε s )s∈ [t,T ] and X ′,ε = (X ′,ε s )s∈ [t,T ] be the strong solutions of the SDE defined in (2.1) with...

2008

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.