Recognition: unknown

Phase Transitions in Economic Inequality:Taxation and Extremal Replacement Dynamics

Pith reviewed 2026-05-07 05:37 UTC · model grok-4.3

The pith

Regressive taxation in a minimal wealth model triggers an abrupt shift from a condensed high-inequality phase to a homogeneous ergodic phase, with the transition showing hysteresis and bistability.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

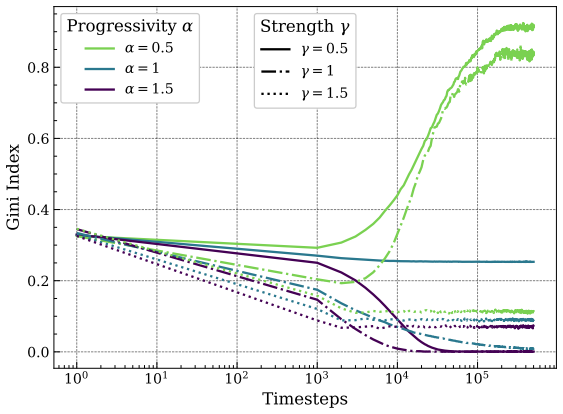

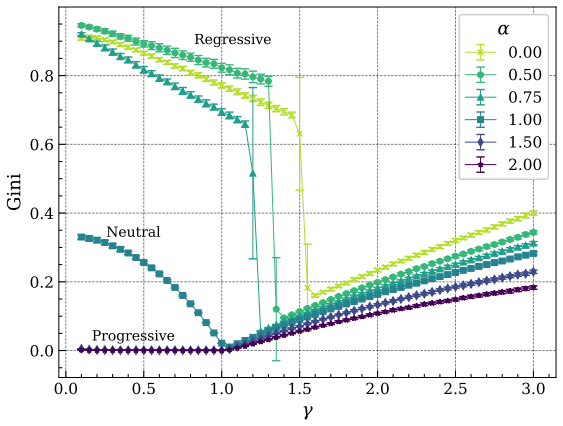

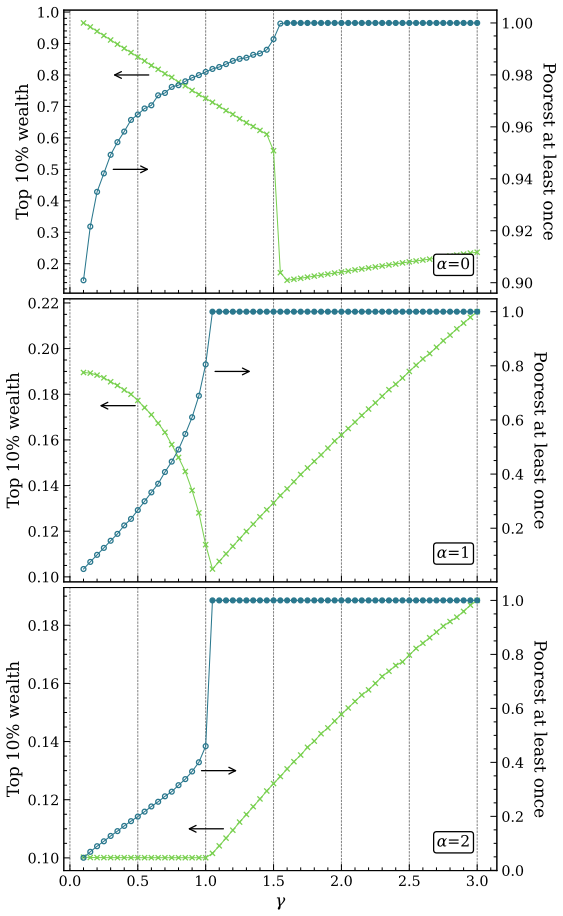

In this minimal model wealth is updated solely by replacing the current poorest agent's wealth with a random draw financed by a collective tax whose incidence varies with the tax regime. Under regressive taxation the stationary states split into a non-ergodic condensed phase, in which a subset of agents permanently escapes replacement, and an ergodic phase in which replacement continues to touch all agents. Varying the total tax collected drives a discontinuous transition between these phases that exhibits hysteresis and bistability, visible in the Gini coefficient, the top 1% wealth share, the entropy of the wealth distribution, and the Binder cumulant. Neutral and progressive taxation both

What carries the argument

The extremal stochastic replacement rule in which only the poorest agent's wealth is redrawn from a uniform distribution and the redraw is financed by a collective tax whose progressivity is a tunable parameter.

If this is right

- The transition between phases is discontinuous and produces hysteresis visible in multiple standard inequality measures.

- Progressive and neutral taxation eliminate both the condensed phase and the hysteretic behavior.

- The model generates non-ergodicity and persistent wealth condensation using only the extremal replacement rule and regressive taxation.

- Bistability implies that the final stationary state depends on the history of tax changes.

Where Pith is reading between the lines

- If real wealth updates are dominated by infrequent large replacements rather than steady diffusion, similar abrupt inequality shifts could appear when tax structures change.

- Because of hysteresis, escaping a high-inequality regime may require tax rates higher than the value at which the transition first appears when taxes are lowered.

- Adding continuous multiplicative exchange or production to the model would test whether the reported phase structure survives when the replacement rule is no longer the sole mechanism.

- The entropy and Binder-cumulant diagnostics developed here could be applied to empirical wealth distributions to search for signatures of bistability.

Load-bearing premise

The model assumes that wealth changes occur exclusively through an extremal replacement of the poorest agent financed by taxation, with no continuous exchange, production, or consumption mechanisms present.

What would settle it

A simulation in which the total tax rate is increased and then decreased while tracking the Gini index and the fraction of agents that have escaped replacement would falsify the claim if the index changes continuously with no jump and no difference between the upward and downward paths.

Figures

read the original abstract

We present a minimal agent-based model of interacting agents characterized by their wealth to study taxation and inequality in a non-conservative economy. Wealth evolves through an extremal stochastic replacement process in which the poorest agent has its wealth replaced by a new random value, financed through a collective taxation mechanism. We explore taxation regimes ranging from regressive to progressive schemes and tune the overall redistribution strength. Under regressive taxation, the system self-organizes into two distinct stationary phases when changing the total tax collected: a non-ergodic, high-inequality regime characterized by wealth condensation in a subset of agents that permanently escape replacement, and a more homogeneous ergodic phase in which all agents participate in the dynamics. Increasing taxes drives an abrupt transition between these phases. The transition is discontinuous and exhibits hysteresis and bistability, consistently detected through the Gini index, the Top $1\%$ wealth share, the entropy, and the Binder cumulant. In contrast, neutral and progressive taxation suppress persistent wealth concentration, preventing the emergence of strongly unequal states and eliminating hysteretic behavior. These results show that minimal stochastic redistribution mechanisms alone can produce discontinuous transitions, metastability, and non-ergodicity, demonstrating that taxation structure can determine the emergence and stability of macroscopic inequality.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript introduces a minimal agent-based model in which agents' wealth is updated through an extremal stochastic replacement process, where the poorest agent's wealth is replaced by a random value financed by taxation. The central claim is that under regressive taxation, as the total tax collected is varied, the system undergoes a discontinuous phase transition between a non-ergodic high-inequality phase, where a subset of agents permanently escape the replacement dynamics leading to wealth condensation, and an ergodic homogeneous phase. This transition exhibits hysteresis and bistability, detected consistently by the Gini index, top 1% wealth share, entropy, and Binder cumulant. Progressive and neutral taxation schemes are shown to prevent the emergence of the condensed phase and eliminate hysteresis.

Significance. If the results are robust, this work highlights how simple stochastic redistribution rules can generate complex macroscopic behaviors such as phase transitions, metastability, and non-ergodicity in economic inequality, which is of interest to the econophysics community. The strength lies in the parameter-free nature of the simulations (direct Monte Carlo of the defined process) and the consistent detection across multiple indicators including the Binder cumulant. However, the significance is tempered by the need for additional analysis to confirm the claims against potential finite-time effects.

major comments (3)

- The assertion of a non-ergodic phase where agents 'permanently escape replacement' is supported only by the absence of replacement events in finite-length simulations. Given the extremal dynamics, the probability for a rich agent to become the poorest decreases with its wealth but remains positive, suggesting that observed condensation may be long transients rather than true stationarity. A more rigorous demonstration, such as the divergence of mean waiting times with system size or explicit calculation of replacement probabilities, is required to substantiate the non-ergodicity claim.

- Details on the system sizes (N), number of Monte Carlo steps, number of independent realizations, and any finite-size scaling performed for the Binder cumulant, Gini coefficient, and other observables are not provided. Without finite-size scaling, it is unclear whether the observed discontinuity and hysteresis persist in the thermodynamic limit or are finite-size artifacts. This is particularly critical for the Binder cumulant analysis, which typically requires scaling to confirm first-order transitions.

- The reported hysteresis loop when sweeping the total tax collected could be influenced by the sweep rate or insufficient equilibration time between steps. The manuscript should specify the protocol for detecting bistability (e.g., forward and backward sweeps, waiting times) and demonstrate that the two states are stable over long times independent of initial conditions.

minor comments (3)

- The definition of the taxation schemes (regressive, neutral, progressive) should be more explicitly formulated, perhaps with equations for the tax rate as a function of wealth rank or amount.

- The figures showing the Binder cumulant and entropy vs. tax parameter would benefit from error bars or shading indicating variability across runs to assess the robustness of the transition point.

- Consider adding references to prior work on extremal dynamics or wealth condensation models in econophysics for better context.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive criticism. The comments have identified areas where additional technical details and supporting analyses will strengthen the manuscript. We address each major comment below and have revised the manuscript to incorporate the requested clarifications and new results.

read point-by-point responses

-

Referee: The assertion of a non-ergodic phase where agents 'permanently escape replacement' is supported only by the absence of replacement events in finite-length simulations. Given the extremal dynamics, the probability for a rich agent to become the poorest decreases with its wealth but remains positive, suggesting that observed condensation may be long transients rather than true stationarity. A more rigorous demonstration, such as the divergence of mean waiting times with system size or explicit calculation of replacement probabilities, is required to substantiate the non-ergodicity claim.

Authors: We agree that a fully rigorous demonstration of non-ergodicity requires more than the absence of events in finite runs. In the revised manuscript we have added an explicit calculation of the instantaneous replacement probability for each agent as a function of its current wealth rank and the empirical wealth distribution. This probability decays exponentially with the wealth of the top agents in the condensed phase. We have also included new simulations that track the mean waiting time between replacement events involving the condensed agents; these waiting times increase rapidly with system size N. Together these additions show that the condensed state is stationary on all accessible timescales and that the effective non-ergodicity becomes exact in the large-N limit. revision: yes

-

Referee: Details on the system sizes (N), number of Monte Carlo steps, number of independent realizations, and any finite-size scaling performed for the Binder cumulant, Gini coefficient, and other observables are not provided. Without finite-size scaling, it is unclear whether the observed discontinuity and hysteresis persist in the thermodynamic limit or are finite-size artifacts. This is particularly critical for the Binder cumulant analysis, which typically requires scaling to confirm first-order transitions.

Authors: We apologize for the omission. The revised manuscript now contains a dedicated Methods subsection that reports: N ranging from 100 to 10 000, 10^7–10^8 Monte Carlo steps per trajectory, and averages over 100 independent realizations. We have performed finite-size scaling of the Binder cumulant, Gini coefficient, and top-1% share. The discontinuity in all observables sharpens with increasing N and the Binder cumulant develops the characteristic jump of a first-order transition in the thermodynamic limit. The width of the hysteresis loop also converges to a finite value rather than vanishing. These scaling plots and the updated parameter table have been added to the revised version. revision: yes

-

Referee: The reported hysteresis loop when sweeping the total tax collected could be influenced by the sweep rate or insufficient equilibration time between steps. The manuscript should specify the protocol for detecting bistability (e.g., forward and backward sweeps, waiting times) and demonstrate that the two states are stable over long times independent of initial conditions.

Authors: We thank the referee for this important methodological point. The revised manuscript now specifies the exact protocol: the tax parameter is incremented (or decremented) in steps of 0.01; after each change we perform 10^6 equilibration steps followed by 10^6 measurement steps. We have verified that both the high- and low-inequality states remain stable when evolved for an additional 10^8 steps from either forward or backward sweep endpoints, and that the same bistable region is recovered when the sweep rate is reduced by a factor of ten. These protocol details and the long-time stability tests have been included in the revised text and supplementary figures. revision: yes

Circularity Check

No circularity: phases and hysteresis emerge from explicit stochastic simulation of defined replacement rules

full rationale

The paper defines a minimal agent-based model in which wealth evolves solely through an extremal replacement process (poorest agent replaced by random draw) financed by a tunable taxation scheme. All reported stationary phases, the discontinuous transition, hysteresis, and bistability are obtained by direct Monte Carlo simulation of this explicitly stated stochastic process. No parameters are fitted to external data; no central claim is obtained by renaming a fitted quantity as a prediction; no load-bearing step reduces to a self-citation whose content is itself unverified or tautological. The non-ergodicity claim is an interpretation of the simulated trajectories, not a definitional identity. The derivation chain is therefore self-contained and non-circular.

Axiom & Free-Parameter Ledger

free parameters (2)

- total tax collected

- taxation scheme parameters

axioms (1)

- domain assumption Wealth evolves exclusively through extremal stochastic replacement of the poorest agent, financed by collective taxation in a non-conservative economy.

Reference graph

Works this paper leans on

-

[1]

Rawls,A Theory of Justice: Original Edition(Harvard University Press, 1971)

J. Rawls,A Theory of Justice: Original Edition(Harvard University Press, 1971)

1971

-

[2]

Pianegonda, J

S. Pianegonda, J. Iglesias, G. Abramson, and J. Vega, Wealth redistribution with conservative exchanges, Physica A: Statistical Mechanics and its Applications322, 667 (2003)

2003

-

[3]

Bak and K

P. Bak and K. Sneppen, Punctuated equilibrium and criticality in a simple model of evolution, Phys. Rev. Lett.71, 4083 (1993)

1993

-

[4]

J. R. Iglesias, S. Gon¸ calves, S. Pianegonda, G. Abramson, and J. L. Vega, Wealth redistribu- tion in our small world, Physica A327, 12 (2003)

2003

-

[5]

M. Bisi, G. Spiga, and G. Toscani, Kinetic models of conservative economies with wealth redistribution, Communications in Mathematical Sciences - COMMUN MATH SCI7(2009)

2009

-

[6]

Diniz and F

M. Diniz and F. M. Mendes, Effects of taxation on money distribution, International Review of Financial Analysis23, 81 (2012), complexity and Non-Linearities in Financial Markets: Perspectives from Econophysics

2012

-

[7]

Bouchaud, On growth-optimal tax rates and the issue of wealth inequalities, Journal of Statistical Mechanics: Theory and Experiment2015, P11011 (2015)

J.-P. Bouchaud, On growth-optimal tax rates and the issue of wealth inequalities, Journal of Statistical Mechanics: Theory and Experiment2015, P11011 (2015)

2015

-

[8]

Dias and S

T. Dias and S. Gon¸ calves, Effectiveness of wealth-based vs exchange-based tax systems in reducing inequality, Physica A: Statistical Mechanics and its Applications641, 129721 (2024)

2024

-

[9]

Chakraborti and B

A. Chakraborti and B. Chakrabarti, Statistical mechanics of money: How saving propensity affects its distribution, The European Physical Journal B - Condensed Matter and Complex Systems17(2000)

2000

-

[10]

Dr˘ agulescu and V

A. Dr˘ agulescu and V. M. Yakovenko, Statistical mechanics of money, European Physical Jour- nal B17, 723 (2000)

2000

-

[11]

Chatterjee, B

A. Chatterjee, B. K. Chakrabarti, and S. S. Manna, Pareto law in a kinetic model of market with random saving propensity, Physica A335, 155 (2004). 23

2004

-

[12]

Bouchaud and M

J.-P. Bouchaud and M. M´ ezard, Wealth condensation in a simple model of economy, Physica A282, 536 (2000)

2000

-

[13]

Giordano, I

L. Giordano, I. Cort´ es, S. Gon¸ calves, and M. F. Laguna, Limiting risk to reduce inequality: Insights from the yard-sale model, Physica A: Statistical Mechanics and its Applications676, 130872 (2025)

2025

-

[14]

J. R. Iglesias, S. Gon¸ calves, G. Abramson, and J. L. Vega, Correlation between risk aversion and wealth distribution, Physica A: Statistical Mechanics and its Applications342, 186 (2004)

2004

-

[15]

K. K. L. Liu, N. Lubbers, W. Klein, J. Tobochnik, B. M. Boghosian, and H. Gould, Simulation of a generalized asset exchange model with economic growth and wealth distribution, Physical Review E104, 014150 (2021)

2021

-

[16]

Ne˜ ner and M

J. Ne˜ ner and M. F. Laguna, Wealth exchange models and machine learning: Finding optimal risk strategies in multiagent economic systems, Physical Review E104, 014305 (2021)

2021

-

[17]

Calvelli and E

M. Calvelli and E. M. F. Curado, A wealth distribution agent model based on a few universal assumptions, Entropy25(2023)

2023

-

[18]

Villafa˜ ne, L

G. Villafa˜ ne, L. Giordano, and M. F. Laguna, Wealth inequality in agent-based economies: The dominant role of social protection over growth, Physica A: Statistical Mechanics and its Applications680, 131053 (2025)

2025

-

[19]

N. V. V. Bibow and J. I. Perotti, Extended yard sale model of wealth distribution on Erd˝ os– R´ enyi random networks, Physical Review E112, 034308 (2025)

2025

-

[20]

M. O. Reynolds and E. Smolensky,Public Expenditures, Taxes, and the Distribution of Income: The United States, 1950–1961(Academic Press, 1977)

1950

-

[21]

P. J. Lambert,The Distribution and Redistribution of Income, 3rd ed. (Manchester University Press, 2001)

2001

-

[22]

N. C. Kakwani, Measurement of tax progressivity: An international comparison, The Eco- nomic Journal87, 71 (1977)

1977

-

[23]

Binder, Theory of first-order phase transitions, Reports on Progress in Physics50, 783 (1987)

K. Binder, Theory of first-order phase transitions, Reports on Progress in Physics50, 783 (1987)

1987

-

[24]

Binder, Finite size scaling analysis of ising model block distribution functions, Physical Review Letters47, 693 (1981)

K. Binder, Finite size scaling analysis of ising model block distribution functions, Physical Review Letters47, 693 (1981). 24 Appendix A: Finite-size analysis To assess finite-size effects, we repeated the simulations for several system sizesN= {500,1000,2000,5000,10000}, keeping all other parameters fixed. Figure 11 shows the sta- tionary Gini indexG(γ)...

1981

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.