Recognition: unknown

Bootstrap Inference under General Two-way Clustering with Serially and Spatially Dependent Common Effects

Pith reviewed 2026-05-09 18:31 UTC · model grok-4.3

The pith

A data-driven regime classifier paired with a projection-based wild bootstrap delivers uniformly valid inference for linear regression under two-way clustering in all four feasible asymptotic regimes while permitting serial dependence in a

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

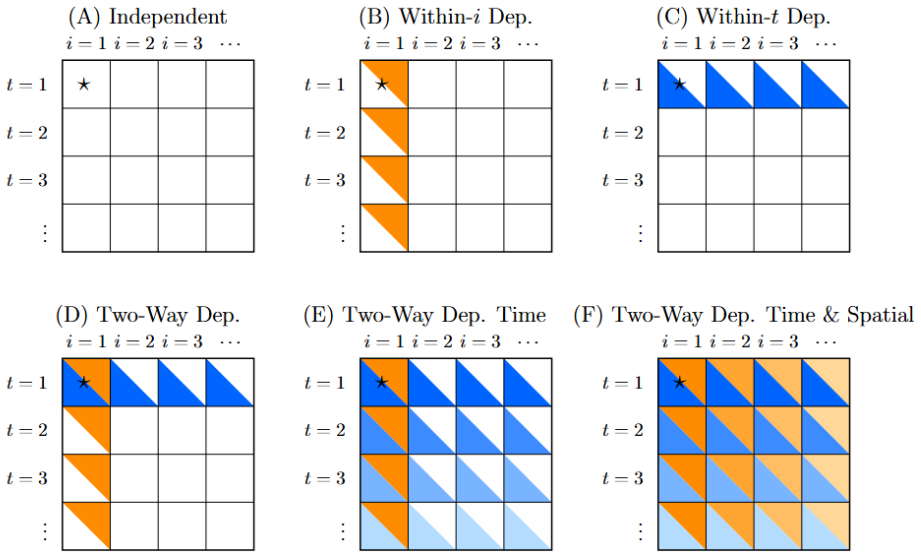

In linear regression with two-way clustering, the score process is asymptotically Gaussian in three regimes and non-Gaussian in two others; uniform consistency fails when score components are heterogeneous or in the infeasible non-Gaussian regime, and the infeasible regime cannot be distinguished uniformly from a feasible one. The proposed procedure therefore uses a data-driven selector to identify the true feasible regime with high probability and applies a projection-based wild bootstrap that remains valid under serial dependence along the second clustering dimension and spatial dependence along the first, yielding uniformly correct asymptotic coverage for confidence intervals and tests in

What carries the argument

The data-driven regime classifier that partitions the sample into one of four feasible regimes based on estimated moments of the score process, together with the projection-based wild bootstrap that generates replicates after subtracting the estimated common effects to preserve the allowed serial and spatial dependence.

If this is right

- Confidence intervals and hypothesis tests for regression coefficients achieve correct asymptotic coverage uniformly over the four feasible regimes.

- The procedure accommodates serial correlation along the second clustering dimension and spatial correlation along the first without requiring the user to specify the regime in advance.

- Uniform validity holds even when the relative strengths of the two clustering dimensions and the dependence parameters vary across the sample.

- Monte Carlo evidence indicates that the finite-sample size and power of the procedure remain accurate under complex clustering structures that mix the permitted forms of dependence.

Where Pith is reading between the lines

- The same regime-classification idea could be applied to multi-way clustering or network dependence settings where the number of limiting regimes is also larger than one.

- Researchers analyzing spatial panel data with both time-series and geographic clustering may obtain more reliable standard errors by first running the classifier rather than defaulting to a single bootstrap method.

- If the projection step can be extended beyond linear models, the approach might yield regime-adaptive inference for nonlinear or instrumental-variables estimators under analogous two-way structures.

Load-bearing premise

The data-driven classifier selects the correct regime with probability approaching one and the projection-based wild bootstrap remains valid under the serial dependence permitted in one dimension and spatial dependence in the other.

What would settle it

A Monte Carlo experiment in which the empirical coverage of the resulting confidence intervals falls materially below the nominal level in any of the four feasible regimes under strong serial dependence along the second clustering dimension would refute the uniform validity claim.

Figures

read the original abstract

This paper develops bootstrap procedures for inference in linear regression models with two-way clustered data. We characterize the estimator's asymptotic behavior in five mutually exclusive and exhaustive regimes: three Gaussian and two non-Gaussian. We establish four impossibility results: heterogeneous score components preclude uniform consistency; uniform consistency also fails in one non-Gaussian (infeasible) regime; the infeasible regime is not uniformly distinguishable from a feasible one; and uniform validity over all feasible regimes rules out uniform conservativeness over the infeasible regime. To address the feasible regimes, we propose a data-driven regime classifier and a projection-based wild bootstrap procedure. The procedure delivers uniformly valid inference across the four feasible regimes while allowing serial dependence along the second clustering dimension and spatial dependence along the first. This combination of regime adaptivity and flexible dependence is new to the two-way clustering literature. Monte Carlo simulations confirm the accuracy and flexibility of the proposed methods in settings with complex clustering structures.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. This paper claims to characterize the asymptotic behavior of the OLS estimator in linear regression under general two-way clustering in five mutually exclusive regimes (three Gaussian and two non-Gaussian), establish four impossibility results on uniform consistency, distinguishability, and validity, and propose a data-driven regime classifier together with a projection-based wild bootstrap that delivers uniformly valid inference across the four feasible regimes while permitting serial dependence along one clustering dimension and spatial dependence along the other. Monte Carlo simulations are used to illustrate finite-sample accuracy under complex clustering.

Significance. If the uniform-validity claim holds, the work would meaningfully advance the two-way clustering literature by supplying the first regime-adaptive bootstrap that simultaneously accommodates serial and spatial dependence structures. The explicit regime taxonomy and the four impossibility results provide a useful organizing framework, while the Monte Carlo evidence offers practical support for the proposed methods in settings with non-standard dependence.

major comments (2)

- [Abstract and impossibility-results section] Abstract and the section on impossibility results: the established result that the infeasible regime is not uniformly distinguishable from a feasible one implies that, near the boundaries between regimes, the data-driven classifier cannot be guaranteed to select the correct regime with probability approaching one. In such cases the projection-based wild bootstrap would be applied under an incorrect regime, directly threatening the claimed uniform validity over all feasible regimes. Boundary-case Monte Carlo experiments or additional high-probability bounds on the classifier are needed to close this gap.

- [Bootstrap-procedure section] Section describing the projection-based wild bootstrap: the manuscript states that the procedure remains valid under serial dependence in the second dimension and spatial dependence in the first, yet supplies no explicit derivation showing how the projection step preserves the required moment conditions or asymptotic normality uniformly across the four feasible regimes. A sketch of the key steps or the precise set of assumptions used for each regime would be required to substantiate the central uniform-validity claim.

minor comments (2)

- [Abstract] The abstract would be clearer if it briefly indicated the main assumptions that delineate the five regimes (e.g., moment conditions or dependence restrictions).

- [Monte Carlo simulations section] In the Monte Carlo section, additional detail on the precise data-generating processes (including the strength of serial and spatial correlation parameters) would improve reproducibility and allow readers to assess how close the designs come to the regime boundaries.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which help clarify and strengthen the presentation of our results on regime-adaptive bootstrap inference under two-way clustering. We address each major comment below.

read point-by-point responses

-

Referee: [Abstract and impossibility-results section] Abstract and the section on impossibility results: the established result that the infeasible regime is not uniformly distinguishable from a feasible one implies that, near the boundaries between regimes, the data-driven classifier cannot be guaranteed to select the correct regime with probability approaching one. In such cases the projection-based wild bootstrap would be applied under an incorrect regime, directly threatening the claimed uniform validity over all feasible regimes. Boundary-case Monte Carlo experiments or additional high-probability bounds on the classifier are needed to close this gap.

Authors: We appreciate the referee's observation on the implications of the impossibility result for uniform distinguishability. This result indicates that the classifier cannot achieve correct selection with probability approaching one uniformly, including near regime boundaries. To address this, we will add high-probability bounds on the classifier's accuracy away from the boundaries and include additional Monte Carlo experiments focused on boundary cases. These revisions will illustrate the finite-sample behavior and support the uniform validity of the overall procedure across the feasible regimes. revision: yes

-

Referee: [Bootstrap-procedure section] Section describing the projection-based wild bootstrap: the manuscript states that the procedure remains valid under serial dependence in the second dimension and spatial dependence in the first, yet supplies no explicit derivation showing how the projection step preserves the required moment conditions or asymptotic normality uniformly across the four feasible regimes. A sketch of the key steps or the precise set of assumptions used for each regime would be required to substantiate the central uniform-validity claim.

Authors: We agree that an explicit derivation would improve the exposition of the central uniform-validity result. In the revised manuscript, we will include a detailed sketch of the key proof steps, specifying the assumptions for each of the four feasible regimes and showing how the projection preserves the requisite moment conditions and asymptotic normality. This will also clarify the accommodation of serial dependence along one dimension and spatial dependence along the other. revision: yes

Circularity Check

No circularity: regimes and bootstrap derived independently from impossibility results

full rationale

The paper first derives five mutually exclusive asymptotic regimes and four impossibility results (heterogeneous scores, non-Gaussian infeasible regime, non-distinguishability, and uniform validity vs. conservativeness trade-off) as standalone characterizations. It then introduces a separate data-driven classifier and projection-based wild bootstrap to achieve uniform validity only on the four feasible regimes. No equation or procedure reduces a claimed prediction or validity result to a fitted parameter or self-referential definition by construction. The classifier and bootstrap are constructed to adapt to the pre-derived regimes without assuming the target uniform validity in their definition. This is self-contained against external benchmarks and does not rely on load-bearing self-citations for the central claims.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Journal of Finance , volume=

Can mutual fund “stars” really pick stocks? New evidence from a bootstrap analysis , author=. Journal of Finance , volume=. 2006 , publisher=

2006

-

[2]

Journal of Finance , volume=

Luck versus skill in the cross-section of mutual fund returns , author=. Journal of Finance , volume=. 2010 , publisher=

2010

-

[3]

Journal of Finance , volume=

The performance of mutual funds in the period 1945-1964 , author=. Journal of Finance , volume=. 1968 , publisher=

1945

-

[4]

Journal of Finance , volume=

Efficient capital markets: A review of theory and empirical work , author=. Journal of Finance , volume=. 1970 , publisher=

1970

-

[5]

Journal of Finance , volume=

Luck versus Skill in the Cross Section of Mutual Fund Returns: Reexamining the Evidence , author=. Journal of Finance , volume=. 2022 , publisher=

2022

-

[6]

Econometrica , volume=

The model confidence set , author=. Econometrica , volume=. 2011 , publisher=

2011

-

[7]

Journal of Financial Economics , volume=

Picking funds with confidence , author=. Journal of Financial Economics , volume=. 2021 , publisher=

2021

-

[8]

Journal of Financial Economics , volume=

Cross-sectional alpha dispersion and performance evaluation , author=. Journal of Financial Economics , volume=. 2019 , publisher=

2019

-

[9]

Econometrica , volume=

A simple, positive semi-definite, heteroskedasticity and autocorrelationconsistent covariance matrix , author=. Econometrica , volume=. 1986 , publisher=

1986

-

[10]

Journal of Finance , volume=

False (and missed) discoveries in Financial economics , author=. Journal of Finance , volume=. 2020 , publisher=

2020

-

[11]

Journal of Econometrics , volume=

Bootstrap analysis of mutual fund performance , author=. Journal of Econometrics , volume=. 2023 , publisher=

2023

-

[12]

Journal of Finance , volume=

A first look at the accuracy of the CRSP mutual fund database and a comparison of the CRSP and Morningstar mutual fund databases , author=. Journal of Finance , volume=. 2001 , publisher=

2001

-

[13]

Econometrica , volume=

A reality check for data snooping , author=. Econometrica , volume=. 2000 , publisher=

2000

-

[14]

Journal of Finance , volume=

On persistence in mutual fund performance , author=. Journal of Finance , volume=. 1997 , publisher=

1997

-

[15]

Journal of Financial Economics , volume=

Can hedge funds time market liquidity? , author=. Journal of Financial Economics , volume=. 2013 , publisher=

2013

-

[16]

Journal of Finance , volume=

Performance and persistence in institutional investment management , author=. Journal of Finance , volume=. 2010 , publisher=

2010

-

[17]

Review of Financial Studies , volume=

Fundamental analysis and the cross-section of stock returns: A data-mining approach , author=. Review of Financial Studies , volume=. 2017 , publisher=

2017

-

[18]

Journal of Financial Economics , volume=

Do mutual funds time the market? Evidence from portfolio holdings , author=. Journal of Financial Economics , volume=. 2007 , publisher=

2007

-

[19]

Econometrica , volume=

Panel data models with interactive fixed effects , author=. Econometrica , volume=. 2009 , publisher=

2009

-

[20]

Economics letters , volume=

Evaluating the size of the bootstrap method for fund performance evaluation , author=. Economics letters , volume=. 2017 , publisher=

2017

-

[21]

1977 , publisher=

Exploratory data analysis , author=. 1977 , publisher=

1977

-

[22]

Journal of Financial Economics , volume=

Asset pricing with liquidity risk , author=. Journal of Financial Economics , volume=. 2005 , publisher=

2005

-

[23]

Review of Financial Studies , volume=

Volatility timing in mutual funds: Evidence from daily returns , author=. Review of Financial Studies , volume=. 1999 , publisher=

1999

-

[24]

Review of Economics and Statistics , volume=

Bootstrap-based improvements for inference with clustered errors , author=. Review of Economics and Statistics , volume=. 2008 , publisher=

2008

-

[25]

1992 , publisher=

Bootstrap methods: another look at the jackknife , author=. 1992 , publisher=

1992

-

[26]

Journal of Financial Economics , volume=

Common risk factors in the returns on stocks and bonds , author=. Journal of Financial Economics , volume=. 1993 , publisher=

1993

-

[27]

Journal of Econometrics , volume=

Bootstrapping integrated covariance matrix estimators in noisy jump--diffusion models with non-synchronous trading , author=. Journal of Econometrics , volume=. 2017 , publisher=

2017

-

[28]

Econometric Theory , volume=

A local Gaussian bootstrap method for realized volatility and realized beta , author=. Econometric Theory , volume=. 2019 , publisher=

2019

-

[29]

Econometric Theory , volume=

Bootstrapping pre-averaged realized volatility under market microstructure noise , author=. Econometric Theory , volume=. 2017 , publisher=

2017

-

[30]

Journal of Money, Credit and Banking, Forthcoming , year=

Are Some Forecasters Really Better than Others? A Note , author=. Journal of Money, Credit and Banking, Forthcoming , year=

-

[31]

Available at SSRN 3523293 , year=

Bootstrapping Laplace transforms of volatility , author=. Available at SSRN 3523293 , year=

-

[32]

Annals of Statistics , volume=

Bootstrap procedures under some non-iid models , author=. Annals of Statistics , volume=. 1988 , publisher=

1988

-

[33]

Annals of Statistics , volume=

Jackknife, bootstrap and other resampling methods in regression analysis , author=. Annals of Statistics , volume=. 1986 , publisher=

1986

-

[34]

Annals of Statistics , volume=

Bootstrap Methods: Another Look at the Jackknife , author=. Annals of Statistics , volume=. 1979 , publisher=

1979

-

[35]

Annals of Statistics , volume=

Bootstrap and wild bootstrap for high dimensional linear models , author=. Annals of Statistics , volume=. 1993 , publisher=

1993

-

[36]

Journal of Econometrics , volume=

The wild bootstrap, tamed at last , author=. Journal of Econometrics , volume=. 2008 , publisher=

2008

-

[37]

Journal of Finance , volume=

Reassessing false discoveries in mutual fund performance: Skill, luck, or lack of power? , author=. Journal of Finance , volume=. 2019 , publisher=

2019

-

[38]

Journal of Finance , volume=

False discoveries in mutual fund performance: Measuring luck in estimated alphas , author=. Journal of Finance , volume=. 2010 , publisher=

2010

-

[39]

Journal of Finance, Forthcoming , year=

Reassessing false discoveries in mutual fund performance: Skill, luck, or lack of power? A reply , author=. Journal of Finance, Forthcoming , year=

-

[40]

Review of Financial Studies , volume=

Thousands of alpha tests , author=. Review of Financial Studies , volume=. 2021 , publisher=

2021

-

[41]

Annals of Statistics , volume=

Phase transition and regularized bootstrap in large-scale -tests with false discovery rate control , author=. Annals of Statistics , volume=. 2014 , publisher=

2014

-

[42]

Econometrica , volume=

Power enhancement in high-dimensional cross-sectional tests , author=. Econometrica , volume=. 2015 , publisher=

2015

-

[43]

Econometric Theory , volume=

The size distortion of bootstrap tests , author=. Econometric Theory , volume=. 1999 , publisher=

1999

-

[44]

Journal of Finance , volume=

Alpha and performance measurement: The effects of investor disagreement and heterogeneity , author=. Journal of Finance , volume=. 2014 , publisher=

2014

-

[45]

Review of Asset Pricing Studies , volume=

Mutual fund industry selection and persistence , author=. Review of Asset Pricing Studies , volume=. 2012 , publisher=

2012

-

[46]

Journal of Finance , volume=

Mutual fund performance: An empirical decomposition into stock-picking talent, style, transactions costs, and expenses , author=. Journal of Finance , volume=. 2000 , publisher=

2000

-

[47]

Journal of Financial and Quantitative Analysis , volume=

The value of active mutual fund management: An examination of the stockholdings and trades of fund managers , author=. Journal of Financial and Quantitative Analysis , volume=. 2000 , publisher=

2000

-

[48]

Econometrica , volume=

Heteroskedasticity and autocorrelation consistent covariance matrix estimation , author=. Econometrica , volume=. 1991 , publisher=

1991

-

[49]

Journal of Financial Economics , volume=

Technical trading revisited: False discoveries, persistence tests, and transaction costs , author=. Journal of Financial Economics , volume=. 2012 , publisher=

2012

-

[50]

The New Palgrave Dictionary of Economics

Multiple testing , author=. The New Palgrave Dictionary of Economics. Forthcoming , year=

-

[51]

Test , volume=

Control of the false discovery rate under dependence using the bootstrap and subsampling , author=. Test , volume=. 2008 , publisher=

2008

-

[52]

Econometric Theory , volume=

Formalized data snooping based on generalized error rates , author=. Econometric Theory , volume=. 2008 , publisher=

2008

-

[53]

Scandinavian Journal of Statistics , pages=

A simple sequentially rejective multiple test procedure , author=. Scandinavian Journal of Statistics , pages=. 1979 , publisher=

1979

-

[54]

Journal of the Royal statistical society: series B (Methodological) , volume=

Controlling the false discovery rate: a practical and powerful approach to multiple testing , author=. Journal of the Royal statistical society: series B (Methodological) , volume=. 1995 , publisher=

1995

-

[55]

Review of Financial Studies , volume=

… and the cross-section of expected returns , author=. Review of Financial Studies , volume=. 2016 , publisher=

2016

-

[56]

Multiple testing in economics , author=

-

[57]

Handbook of Financial Econometrics, Mathematics, Statistics, and Machine Learning , pages=

How many good and bad funds are there, really? , author=. Handbook of Financial Econometrics, Mathematics, Statistics, and Machine Learning , pages=. 2021 , publisher=

2021

-

[58]

Review of Financial Studies , volume=

Detecting repeatable performance , author=. Review of Financial Studies , volume=. 2018 , publisher=

2018

-

[59]

Annals of Statistics , volume=

Improved central limit theorem and bootstrap approximations in high dimensions , author=. Annals of Statistics , volume=. 2022 , publisher=

2022

-

[60]

Review of Finance , volume=

Investing in a global world , author=. Review of Finance , volume=. 2014 , publisher=

2014

-

[61]

Journal of Finance , volume=

Decentralized investment management: Evidence from the pension fund industry , author=. Journal of Finance , volume=. 2013 , publisher=

2013

-

[62]

Review of Financial Studies , volume=

Anomalies and false rejections , author=. Review of Financial Studies , volume=. 2020 , publisher=

2020

-

[63]

Journal of Money, Credit and Banking , volume=

Are some forecasters really better than others? , author=. Journal of Money, Credit and Banking , volume=. 2012 , publisher=

2012

-

[64]

Journal of Financial Economics , volume=

Do hedge funds deliver alpha? A Bayesian and bootstrap analysis , author=. Journal of Financial Economics , volume=. 2007 , publisher=

2007

-

[65]

Journal of Financial and Quantitative Analysis , volume=

New evidence on mutual fund performance: A comparison of alternative bootstrap methods , author=. Journal of Financial and Quantitative Analysis , volume=. 2017 , publisher=

2017

-

[66]

Journal of Econometrics , volume=

Improved inference in the evaluation of mutual fund performance using panel bootstrap methods , author=. Journal of Econometrics , volume=. 2014 , publisher=

2014

-

[67]

The Fama Portfolio: Selected Papers of Eugene F

Luck versus Skill and Factor Selection , author=. The Fama Portfolio: Selected Papers of Eugene F. Fama , year=

-

[68]

Journal of Financial and Quantitative Analysis , volume=

Using stocks or portfolios in tests of factor models , author=. Journal of Financial and Quantitative Analysis , volume=. 2020 , publisher=

2020

-

[69]

Review of Financial Studies , volume=

Fund flows and market states , author=. Review of Financial Studies , volume=. 2017 , publisher=

2017

-

[70]

2009 , institution=

Is investor rationality time varying? Evidence from the mutual fund industry , author=. 2009 , institution=

2009

-

[71]

Journal of Finance, Forthcoming , pages=

Time-Varying Fund Manager Skill , author=. Journal of Finance, Forthcoming , pages=

-

[72]

Econometrica , volume=

A rational theory of mutual funds' attention allocation , author=. Econometrica , volume=. 2016 , publisher=

2016

-

[73]

Review of Finance , volume=

Improved forecasting of mutual fund alphas and betas , author=. Review of Finance , volume=. 2007 , publisher=

2007

-

[74]

Review of Financial Studies , volume=

Estimating the dynamics of mutual fund alphas and betas , author=. Review of Financial Studies , volume=. 2008 , publisher=

2008

-

[75]

Journal of Finance , volume=

The persistence of mutual fund performance , author=. Journal of Finance , volume=. 1992 , publisher=

1992

-

[76]

Review of Financial Studies , volume=

Mutual fund competition, managerial skill, and alpha persistence , author=. Review of Financial Studies , volume=. 2018 , publisher=

2018

-

[77]

Journal of Finance , volume=

Evaluating mutual fund performance , author=. Journal of Finance , volume=. 2001 , publisher=

2001

-

[78]

Mutual fund performance: evidence from the

Blake, David and Timmermann, Allan , journal=. Mutual fund performance: evidence from the. 1998 , publisher=

1998

-

[79]

Journal of Finance , volume=

Are some mutual fund managers better than others? Cross-sectional patterns in behavior and performance , author=. Journal of Finance , volume=. 1999 , publisher=

1999

-

[80]

Journal of Finance , volume=

Another puzzle: The growth in actively managed mutual funds , author=. Journal of Finance , volume=. 1996 , publisher=

1996

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.