Recognition: unknown

Principal-agent problems with adverse selection: A stochastic target problem formulation

Pith reviewed 2026-05-09 14:20 UTC · model grok-4.3

The pith

The agent's optimization in unique-contract adverse selection problems reformulates as a stochastic target problem, turning the principal's design into a stochastic control problem with partial information and state constraints.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

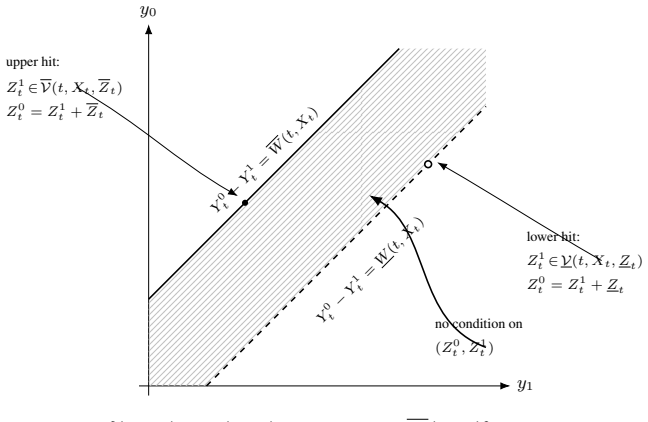

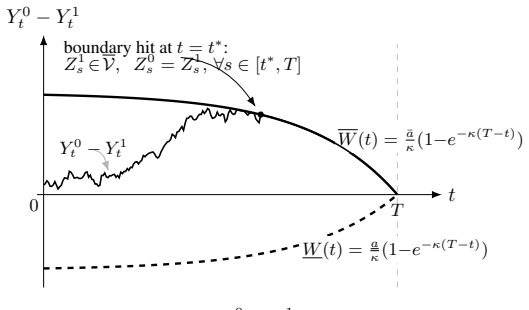

The agent's optimization problem can be reformulated as a stochastic target problem. After characterizing the credible domain of this target problem, the principal's objective can be solved as a stochastic optimal control problem with partial information and state constraints. The description of the credible domain also allows us to obtain the value of screening contracts.

What carries the argument

Stochastic target problem reformulation of the agent's choice, with its credible domain serving as the state constraint set for the principal's control problem.

Load-bearing premise

The agent's problem with a fixed contract is exactly equivalent to a stochastic target problem whose credible domain admits a complete characterization.

What would settle it

A case where the agent's optimal action under the derived contract reaches a target outside the paper's credible domain or leads to non-participation.

Figures

read the original abstract

We study a principal-agent problem with adverse selection, where the principal does not know the agent's true cost but must design a contract to optimize a specific criterion. Unlike standard screening frameworks that allow for self-selection, we assume the principal can only offer a unique contract. We show that the agent's optimization problem can be reformulated as a stochastic target problem. After characterizing the credible domain of this target problem, we show that the principal's objective can be solved as a stochastic optimal control problem with partial information and state constraints. The description of the credible domain also allows us to obtain the value of screening contracts.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies principal-agent problems with adverse selection in which the principal is restricted to offering a unique contract (rather than a menu). It claims that the agent's optimization problem (maximizing expected utility given a privately known cost type) admits an exact reformulation as a stochastic target problem. After characterizing the credible domain of this target problem, the principal's objective is recast as a stochastic optimal control problem with partial information and state constraints; the credible-domain description is also used to obtain the value of screening contracts.

Significance. If the claimed exact equivalence holds and the credible domain is fully and rigorously characterized for general (including continuous) type distributions, the paper would supply a novel stochastic-control route to unique-contract screening problems. This could be useful for dynamic settings with partial information, as it converts the screening problem into one with explicit state constraints whose value can be computed via control techniques. The approach is technically interesting at the intersection of contract theory and stochastic target problems, but its significance is conditional on the completeness of the domain characterization.

major comments (2)

- [Abstract and agent's reformulation section] The central claim (abstract and the section introducing the agent's problem) is that the agent's optimization admits an exact reformulation as a stochastic target problem whose credible domain can be characterized in closed form and then used as a state constraint. For continuously distributed types under the unique-contract restriction, this equivalence may fail to be exact at boundary points where the agent's continuation value equals the reservation utility for a positive-measure set of types; any such gap would make the subsequent partial-information control formulation incomplete and the derived screening value incorrect. Explicit regularity conditions on the cost function and filtration are needed to guarantee the equivalence.

- [Principal's control problem section] The principal's problem is solved as a stochastic optimal control problem with partial information and state constraints supplied by the credible domain. Because the type remains private information throughout (unique contract), the partial-information filter must be shown to be consistent with the domain characterization; otherwise the value function and optimal contract may not be correctly identified.

minor comments (2)

- [Abstract] The abstract would be clearer if it briefly stated the key regularity conditions (e.g., on the cost function or the filtration) under which the stochastic-target reformulation and credible-domain characterization hold.

- [Notation and definitions] Notation for the credible domain and the partial-information filter should be introduced with explicit definitions before being used in the principal's control problem.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments. We address each major comment below, clarifying the equivalence and consistency results while committing to strengthen the manuscript with additional regularity conditions and proofs.

read point-by-point responses

-

Referee: [Abstract and agent's reformulation section] The central claim (abstract and the section introducing the agent's problem) is that the agent's optimization admits an exact reformulation as a stochastic target problem whose credible domain can be characterized in closed form and then used as a state constraint. For continuously distributed types under the unique-contract restriction, this equivalence may fail to be exact at boundary points where the agent's continuation value equals the reservation utility for a positive-measure set of types; any such gap would make the subsequent partial-information control formulation incomplete and the derived screening value incorrect. Explicit regularity conditions on the cost function and filtration are needed to guarantee the equivalence.

Authors: We appreciate the referee pointing out the boundary behavior for continuous types. The manuscript's reformulation sets the credible domain to include the reservation utility as its lower boundary, with the agent's optimal strategy constructed to reach the target with probability one. Under the paper's maintained assumptions (Lipschitz continuous cost function and right-continuous filtration), the equivalence holds exactly, including boundaries, because the value function is continuous and the hitting time is controlled. To fully address the concern, we will add a new proposition in the revised version stating the explicit regularity conditions and providing a rigorous proof of exact equivalence for general (including continuous) type distributions, covering boundary cases. This will ensure the subsequent control formulation is complete. revision: yes

-

Referee: [Principal's control problem section] The principal's problem is solved as a stochastic optimal control problem with partial information and state constraints supplied by the credible domain. Because the type remains private information throughout (unique contract), the partial-information filter must be shown to be consistent with the domain characterization; otherwise the value function and optimal contract may not be correctly identified.

Authors: We agree that consistency between the partial-information filter and the credible domain is necessary. The manuscript constructs the filter via Bayesian updating on observed actions under the unique contract, with the credible domain defined from the stochastic target problem independently of realized types. We will add a lemma in the revision proving that the filtered belief process remains inside the credible domain almost surely, leveraging the martingale property of the posterior and the closedness of the domain. This confirms the value function and optimal contract are correctly identified without changing the main results. revision: yes

Circularity Check

No circularity in derivation; reformulation uses standard stochastic control

full rationale

The paper's central steps—reformulating the agent's problem as a stochastic target problem, characterizing its credible domain, and recasting the principal's problem as a partial-information stochastic control problem with state constraints—are presented as applications of existing stochastic control theory rather than self-referential definitions or fitted inputs. No load-bearing self-citations, uniqueness theorems imported from the authors' prior work, or ansatzes smuggled via citation are invoked. The derivation chain remains self-contained against external benchmarks of stochastic target problems and filtering theory; the unique-contract restriction is an explicit modeling choice, not a hidden tautology.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption The principal offers only a single contract rather than a screening menu.

- ad hoc to paper The agent's optimization problem admits an exact reformulation as a stochastic target problem.

Reference graph

Works this paper leans on

-

[1]

arXiv preprint arXiv:2406.19607 , year=

Hern. arXiv preprint arXiv:2406.19607 , year=

work page internal anchor Pith review arXiv

-

[2]

Econometrica , volume=

Insurance and inequality with persistent private information , author=. Econometrica , volume=. 2025 , publisher=

2025

-

[3]

Contract Theory in Continuous-Time Models , series =

Cvitani. Contract Theory in Continuous-Time Models , series =. 2012 , doi =

2012

-

[4]

Journal of Optimization Theory and Applications , volume=

Bank monitoring incentives under moral hazard and adverse selection , author=. Journal of Optimization Theory and Applications , volume=. 2020 , publisher=

2020

-

[5]

Available at SSRN 4778185 , year=

Persistent private information revisited , author=. Available at SSRN 4778185 , year=

-

[6]

SIAM Journal on Control and Optimization , volume =

Soner, Halil Mete , title =. SIAM Journal on Control and Optimization , volume =. 1986 , doi =

1986

-

[7]

Mathematische Annalen , volume =

Lasry, Jean-Michel and Lions, Pierre-Louis , title =. Mathematische Annalen , volume =. 1989 , doi =

1989

-

[8]

Transactions of the American Mathematical Society , volume =

Capuzzo-Dolcetta, Italo and Lions, Pierre-Louis , title =. Transactions of the American Mathematical Society , volume =. 1990 , doi =

1990

-

[9]

, title =

Katsoulakis, Markos A. , title =. Indiana University Mathematics Journal , volume =. 1994 , doi =

1994

-

[10]

and Soner, H

Fleming, Wendell H. and Soner, H. Mete , title =. 2006 , doi =

2006

-

[11]

Mete and Touzi, Nizar , title =

Soner, H. Mete and Touzi, Nizar , title =. Journal of the European Mathematical Society , volume =. 2002 , doi =

2002

-

[12]

Mete and Touzi, Nizar , title =

Soner, H. Mete and Touzi, Nizar , title =. SIAM Journal on Control and Optimization , volume =. 2002 , doi =

2002

-

[13]

SIAM Journal on Control and Optimization , volume =

Bouchard, Bruno and Elie, Romuald and Imbert, Cyril , title =. SIAM Journal on Control and Optimization , volume =. 2010 , doi =

2010

-

[14]

SIAM Journal on Control and Optimization , volume =

Bouchard, Bruno and Nutz, Marcel , title =. SIAM Journal on Control and Optimization , volume =. 2012 , doi =

2012

-

[15]

Dynamic programming approach to principal--agent problems , journal =

Cvitani. Dynamic programming approach to principal--agent problems , journal =. 2018 , doi =

2018

-

[16]

and Aggoun, Lakhdar and Moore, John B

Elliott, Robert J. and Aggoun, Lakhdar and Moore, John B. , title =. 1995 , doi =

1995

-

[17]

and Ishii, Hitoshi and Lions, Pierre-Louis , title =

Crandall, Michael G. and Ishii, Hitoshi and Lions, Pierre-Louis , title =. Bulletin of the American Mathematical Society , volume =. 1992 , doi =

1992

-

[18]

Journal of Differential Equations , volume=

Singular nonlinear boundary value problems for second-order ordinary differential equations , author=. Journal of Differential Equations , volume=. 1989 , publisher=

1989

-

[19]

SIAM Journal on Control and Optimization , volume=

Stochastic target problems with controlled loss , author=. SIAM Journal on Control and Optimization , volume=. 2010 , publisher=

2010

-

[20]

Mathematical finance , volume=

Backward stochastic differential equations in finance , author=. Mathematical finance , volume=. 1997 , publisher=

1997

-

[21]

Econometrica , volume=

Optimal asset management contracts with hidden savings , author=. Econometrica , volume=. 2021 , publisher=

2021

-

[22]

Econometrica , volume=

Robust contracts in continuous time , author=. Econometrica , volume=. 2016 , publisher=

2016

-

[23]

The Review of Financial Studies , volume=

Optimal long-term contracting with learning , author=. The Review of Financial Studies , volume=. 2017 , publisher=

2017

-

[24]

The Annals of Probability , volume=

Stochastic control for a class of nonlinear kernels and applications , author=. The Annals of Probability , volume=. 2018 , publisher=

2018

-

[25]

arXiv preprint arXiv:1606.04062 , year=

Causal transport in discrete time and applications , author=. arXiv preprint arXiv:1606.04062 , year=

-

[26]

Econometrica: Journal of the Econometric Society , pages=

Aggregation and linearity in the provision of intertemporal incentives , author=. Econometrica: Journal of the Econometric Society , pages=. 1987 , publisher=

1987

-

[27]

2008 , publisher=

Controlled diffusion processes , author=. 2008 , publisher=

2008

-

[28]

Quadratic

Briand, Philippe and Hu, Ying , journal=. Quadratic. 2007 , publisher=

2007

-

[29]

, author=

Time-inconsistent contract theory. , author=. Mathematical Finance , pages=. 2024 , publisher=

2024

-

[30]

The RAND Journal of Economics , pages=

Linearity with project selection and controllable diffusion rate in continuous-time principal-agent problems , author=. The RAND Journal of Economics , pages=. 1995 , publisher=

1995

-

[31]

Journal of Functional Analysis , pages=

BSDEs with terminal conditions that have bounded Malliavin derivative , author=. Journal of Functional Analysis , pages=. 2014 , volume=

2014

-

[32]

Management Science , year=

A Continuous Time Framework for Sequential Goal-Based Wealth Management , author=. Management Science , year=

-

[33]

Journal de math

Convex viscosity solutions and state constraints , author=. Journal de math. 1997 , publisher=

1997

-

[34]

Journal of Economic Theory , volume=

The first-order approach to the continuous-time principal--agent problem with exponential utility , author=. Journal of Economic Theory , volume=. 1993 , publisher=

1993

-

[35]

Journal of Economic Theory , volume=

Corporate insurance and managerial incentives , author=. Journal of Economic Theory , volume=. 1997 , publisher=

1997

-

[36]

Journal of Economic Theory , volume=

Asymptotic efficiency in dynamic principal-agent problems , author=. Journal of Economic Theory , volume=. 2000 , publisher=

2000

-

[37]

, journal=

Hellwig, Martin F. , journal=. The role of boundary solutions in principal--agent problems of the. 2007 , publisher=

2007

-

[38]

and Schmidt, Klaus M

Hellwig, Martin F. and Schmidt, Klaus M. , journal=. Discrete--time approximations of the. 2002 , publisher=

2002

-

[39]

Econometrica: Journal of the Econometric Society , pages=

The first-order approach to principal-agent problems , author=. Econometrica: Journal of the Econometric Society , pages=. 1985 , publisher=

1985

-

[40]

University of Wisconsin, Madison , year=

On dynamic principal-agent problems in continuous time , author=. University of Wisconsin, Madison , year=

-

[41]

Econometrica , volume=

Persistent private information , author=. Econometrica , volume=. 2011 , publisher=

2011

-

[42]

Journal of Economic Theory , volume=

A solvable continuous time dynamic principal--agent model , author=. Journal of Economic Theory , volume=. 2015 , publisher=

2015

-

[43]

International Journal of Stochastic Analysis , volume=

Optimal contracts in continuous-time models , author=. International Journal of Stochastic Analysis , volume=. 2006 , publisher=

2006

-

[44]

The BE Journal of Theoretical Economics , volume=

Principal-agent problems with exit options , author=. The BE Journal of Theoretical Economics , volume=. 2008 , publisher=

2008

-

[45]

Applied Mathematics and Optimization , volume=

Optimal compensation with hidden action and lump-sum payment in a continuous-time model , author=. Applied Mathematics and Optimization , volume=. 2009 , publisher=

2009

-

[46]

Econometrica , pages=

Ironing, sweeping, and multidimensional screening , author=. Econometrica , pages=. 1998 , publisher=

1998

-

[47]

Journal of economic theory , volume=

Short-term contracts and long-term agency relationships , author=. Journal of economic theory , volume=. 1990 , publisher=

1990

-

[48]

Journal of Economic Theory , volume=

Optimal cartel equilibria with imperfect monitoring , author=. Journal of Economic Theory , volume=. 1986 , publisher=

1986

-

[49]

Journal of Economic theory , volume=

Repeated insurance contracts and moral hazard , author=. Journal of Economic theory , volume=. 1983 , publisher=

1983

-

[50]

Econometrica: Journal of the Econometric Society , pages=

Repeated moral hazard , author=. Econometrica: Journal of the Econometric Society , pages=. 1985 , volume=

1985

-

[51]

Accounting, organizations and society , volume=

Agency research in managerial accounting: A second look , author=. Accounting, organizations and society , volume=. 1990 , publisher=

1990

-

[52]

Econometrica: Journal of the Econometric Society , pages=

Moral hazard and renegotiation in agency contracts , author=. Econometrica: Journal of the Econometric Society , pages=. 1990 , publisher=

1990

-

[53]

The Bell Journal of Economics , volume=

Long-term contracts and moral hazard , author=. The Bell Journal of Economics , volume=. 1983 , publisher=

1983

-

[54]

2018 , publisher=

Justin Sirignano and Konstantinos Spiliopoulos , journal=. 2018 , publisher=

2018

-

[55]

The Review of Economic Studies , volume=

On repeated moral hazard with discounting , author=. The Review of Economic Studies , volume=. 1987 , publisher=

1987

-

[56]

The journal of Finance , volume=

Optimal security design and dynamic capital structure in a continuous-time agency model , author=. The journal of Finance , volume=. 2006 , publisher=

2006

-

[57]

2006 , publisher=

Infinite dimensional analysis, a Hitchhiker's Guide , author=. 2006 , publisher=

2006

-

[58]

Zeitschrift f

On the strong comparison theorems for solutions of stochastic differential equations , author=. Zeitschrift f. 1981 , publisher=

1981

-

[59]

SIAM Journal on Control and Optimization , volume=

Weak dynamic programming for generalized state constraints , author=. SIAM Journal on Control and Optimization , volume=. 2012 , publisher=

2012

-

[60]

Econometrica , volume=

Large risks, limited liability, and dynamic moral hazard , author=. Econometrica , volume=. 2010 , publisher=

2010

-

[61]

Journal of Mathematical Economics , volume=

Bayesian Nash equilibrium and variational inequalities , author=. Journal of Mathematical Economics , volume=. 2016 , publisher=

2016

-

[62]

The Review of Economic Studies , volume=

A continuous-time version of the principal-agent problem , author=. The Review of Economic Studies , volume=. 2008 , publisher=

2008

-

[63]

Applied Mathematics , volume=

An Application of the Maximum Theorem in Multi-Criteria Optimization, Properties of Pareto-Retract Mappings, and the Structure of Pareto Sets , author=. Applied Mathematics , volume=

-

[64]

Is there a Golden Parachute in

Possama. Is there a Golden Parachute in. Mathematics of Operations Research , volume=. 2024 , publisher=

2024

-

[65]

Econometrica , volume=

Envelope theorems for arbitrary choice sets , author=. Econometrica , volume=. 2002 , publisher=

2002

-

[66]

The Journal of finance , volume=

The dynamics of dealer markets under competition , author=. The Journal of finance , volume=. 1983 , publisher=

1983

-

[67]

Financial Analysts Journal , volume=

The only game in town , author=. Financial Analysts Journal , volume=. 1995 , publisher=

1995

-

[68]

2013 , publisher=

Ordinary differential equations , author=. 2013 , publisher=

2013

-

[69]

, author=

Existence and regularity for a minimum problem with free boundary. , author=. 1981 , publisher=

1981

-

[70]

1991 , publisher=

Game theory , author=. 1991 , publisher=

1991

-

[71]

Econometrica: Journal of the Econometric Society , pages=

Optimal auctions with risk averse buyers , author=. Econometrica: Journal of the Econometric Society , pages=. 1984 , publisher=

1984

-

[72]

Proceedings of the London Mathematical Society , volume=

Viscosity Solutions for Weakly Coupled Systems of Hamilton-Jacobi Equations , author=. Proceedings of the London Mathematical Society , volume=. 1991 , publisher=

1991

-

[73]

1997 , publisher=

Optimization by vector space methods , author=. 1997 , publisher=

1997

-

[74]

1993 , publisher=

Nonlinear pricing , author=. 1993 , publisher=

1993

-

[75]

2005 , publisher=

Multidimensional screening , author=. 2005 , publisher=

2005

-

[76]

Journal of Economic theory , volume=

Monopoly and product quality , author=. Journal of Economic theory , volume=. 1978 , publisher=

1978

-

[77]

The Journal of Finance , volume=

Why did Nasdaq market makers stop avoiding odd-eighth quotes? , author=. The Journal of Finance , volume=. 1994 , publisher=

1994

-

[78]

Competing mechanisms in a common value environment

Corrigendum to" Competing mechanisms in a common value environment" , author=. Econometrica , volume=. 2013 , publisher=

2013

-

[79]

Aase, Knut K. and Bjuland, Terje and. Strategic. Afrika Matematika , language =. 2012 , month = sep, volume =. doi:10.1007/s13370-011-0026-x , abstract =

-

[80]

Annals of mathematics , pages=

Free boundaries in optimal transport and Monge-Ampere obstacle problems , author=. Annals of mathematics , pages=. 2010 , publisher=

2010

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.