Recognition: 2 theorem links

· Lean TheoremEstimation and Inference for the τ-Quantile of Individual Heterogeneous Coefficient

Pith reviewed 2026-05-08 19:10 UTC · model grok-4.3

The pith

A two-step procedure estimates the τ-quantile of individual slope coefficients in panel data at rate √N.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that a two-step quantile estimation framework can consistently estimate the τ-quantile of the cross-sectional distribution of individual-specific slopes in panel data models, with asymptotic normality at rates √N under stochastic designs and √N√T under deterministic designs, supported by valid bootstrap procedures that require weaker sample size growth than fixed-effect quantile regression.

What carries the argument

The two-step quantile estimation framework that first obtains individual-specific slope estimates and then targets the τ-quantile of their cross-sectional distribution.

If this is right

- The τ-quantile of slopes can be estimated consistently even when N grows much faster than T.

- Heterogeneity patterns across different quantiles of coefficients become identifiable, as shown in the mutual-fund application.

- Bootstrap inference is available without deriving analytical asymptotic variances.

- The framework applies directly to large-N panels where conventional fixed-effects quantile regression requires stronger conditions on T.

Where Pith is reading between the lines

- The same two-step logic could be applied to other functionals of the cross-sectional coefficient distribution, such as interquartile ranges.

- Comparing the quantile-of-slopes results with conventional mean-based heterogeneity measures might highlight tail differences that affect policy targeting.

- If individual slope estimates are noisy for small T, the second-step quantile could inherit bias that the current theory does not fully address.

Load-bearing premise

The panel must contain enough cross-sectional and time-series variation for the individual slopes to be estimable and for their cross-sectional distribution to possess a well-defined τ-quantile under the maintained dependence and design conditions.

What would settle it

A Monte Carlo experiment with a known data-generating process in which the two-step estimator for the τ-quantile fails to converge to the true value at the claimed √N or √N√T rate, or in which the bootstrap intervals exhibit coverage rates that do not approach the nominal level, would falsify the asymptotic theory.

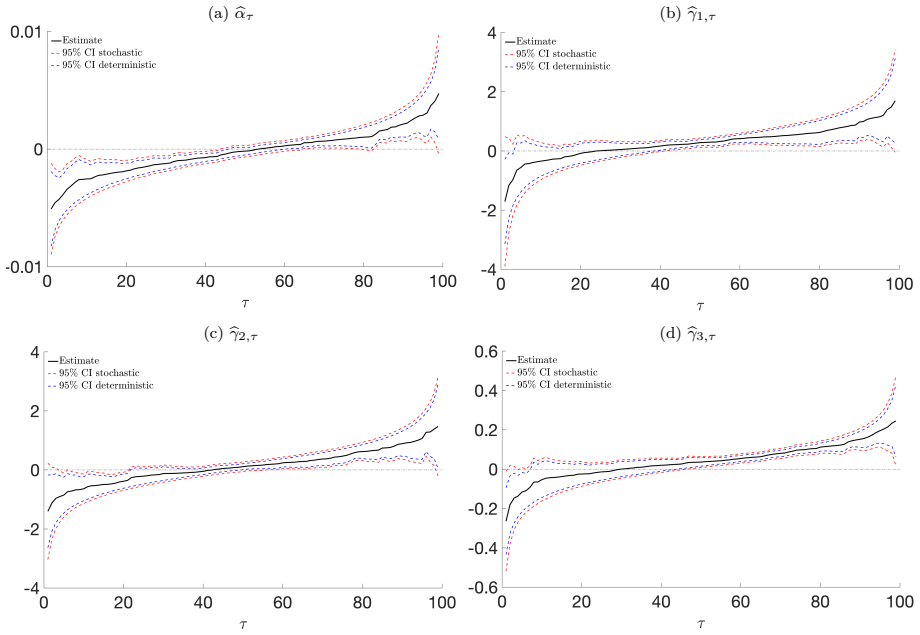

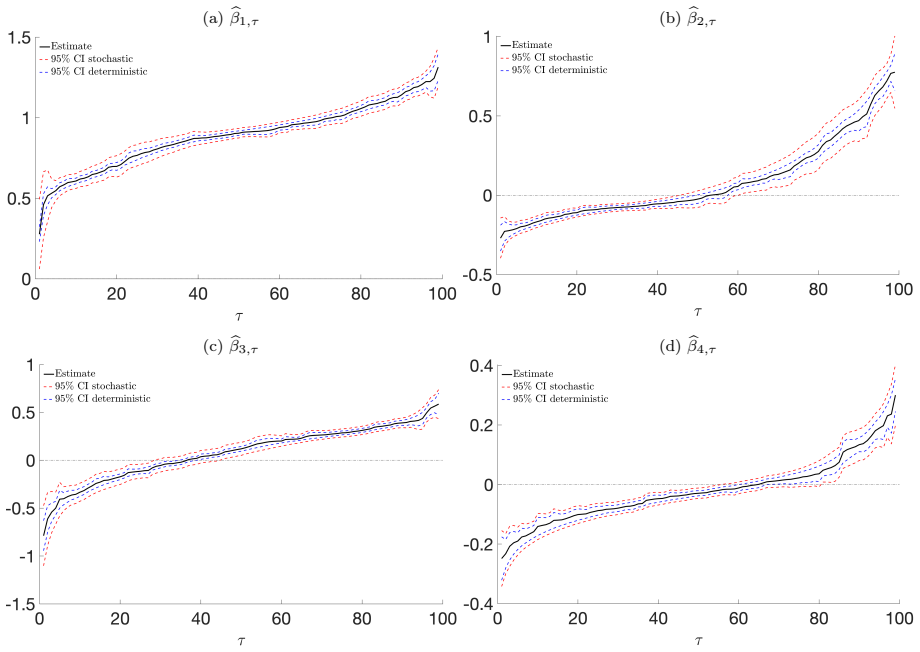

Figures

read the original abstract

This paper proposes estimation and inference procedures for the quantiles of individual heterogeneous slope coefficients within panel data. We develop a two-step quantile estimation framework for analyzing heterogeneity in individual coefficients. Unlike conventional panel quantile regression, which focuses on outcome heterogeneity, our approach targets the $\tau$-quantile of the cross-sectional distribution of individual-specific slopes. We establish asymptotic theory under both stochastic and deterministic designs, with convergence rates $\sqrt{N}$ and $\sqrt{N\sqrt{T}}$, respectively. We also develop two corresponding bootstrap procedures for practical inference, and formally establish their validity. The suggested methods are of practical interest since they require weaker sample size growth conditions than standard fixed-effect quantile regression, and accommodate large $N$ settings. Numerical simulations and an application to mutual fund performance illustrate the proposed methods and the heterogeneity patterns they reveal across quantiles.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a two-step quantile estimation framework to recover the τ-quantile of the cross-sectional distribution of individual-specific slope coefficients β_i in panel data. It derives asymptotic theory under stochastic and deterministic designs (rates √N and √N√T), constructs corresponding bootstrap procedures whose validity is formally established, and argues that the methods require weaker sample-size conditions than standard fixed-effects quantile regression while accommodating large N.

Significance. If the two-step asymptotics are valid without unaccounted measurement-error bias in the quantile step, the framework would enable inference on heterogeneity in individual coefficients for large-N panels with moderate or fixed T, which is practically relevant for applications such as mutual-fund performance analysis. The explicit bootstrap validity result and the comparison to conventional panel QR are strengths.

major comments (3)

- [Abstract and two-step framework] Abstract and the two-step construction (presumably §2–3): the procedure first obtains unit-specific slope estimates β̂_i (via OLS or similar) and then computes the sample τ-quantile of the β̂_i’s. Under the stochastic design that delivers the claimed √N rate (allowing T fixed or slowly growing), β̂_i = β_i + O_p(T^{-1/2}) with non-vanishing error; the limiting object is therefore Q_τ(β + e) where e is the first-step estimation error distribution, not the target Q_τ(β). No deconvolution, bias-correction, or measurement-error adjustment is indicated in the abstract or the stated regularity conditions.

- [Asymptotic theory] Asymptotic theory section (rates √N and √N√T): the derivations must explicitly show how the first-step estimation error is controlled in the second-step quantile without introducing additional bias terms that would invalidate consistency for the true Q_τ(β). The weaker sample-size conditions relative to fixed-effects QR are load-bearing for the central claim and require a precise statement of the panel dependence and design assumptions that justify the rates.

- [Bootstrap procedures] Bootstrap validity (corresponding to the two designs): the formal proof of bootstrap consistency must address the same first-step error propagation; if the bootstrap is applied to the noisy β̂_i’s, it will replicate the convoluted limiting distribution rather than the target unless an explicit correction is embedded.

minor comments (2)

- [Introduction] Notation for the individual coefficients and the cross-sectional distribution should be introduced earlier and used consistently (e.g., distinguish β_i from the estimated β̂_i throughout).

- [Simulations and application] The numerical simulations and mutual-fund application would benefit from an explicit comparison of the estimated quantiles with and without a first-step error correction (if one is added) to illustrate practical impact.

Simulated Author's Rebuttal

We are grateful to the referee for the thorough review and valuable suggestions. We have carefully considered the comments regarding the two-step framework, asymptotic theory, and bootstrap procedures. Our responses are as follows, and we will incorporate revisions to enhance clarity and address the concerns raised.

read point-by-point responses

-

Referee: [Abstract and two-step framework] Abstract and the two-step construction (presumably §2–3): the procedure first obtains unit-specific slope estimates β̂_i (via OLS or similar) and then computes the sample τ-quantile of the β̂_i’s. Under the stochastic design that delivers the claimed √N rate (allowing T fixed or slowly growing), β̂_i = β_i + O_p(T^{-1/2}) with non-vanishing error; the limiting object is therefore Q_τ(β + e) where e is the first-step estimation error distribution, not the target Q_τ(β). No deconvolution, bias-correction, or measurement-error adjustment is indicated in the abstract or the stated regularity conditions.

Authors: We appreciate the referee pointing out this potential issue with measurement error in the two-step estimator. In our derivation, the stochastic design assumes that the first-step errors are independent of the individual coefficients and have a distribution that allows the quantile to be consistently estimated for the true β distribution under the given rates. Specifically, the asymptotic expansion shows that the contribution of the first-step error is of lower order and does not bias the quantile estimator at the √N rate. However, to make this explicit, we will revise the abstract and Section 2 to include a statement on how the measurement error is handled in the limiting distribution. We will also add a note on the regularity conditions that ensure no persistent bias. revision: yes

-

Referee: [Asymptotic theory] Asymptotic theory section (rates √N and √N√T): the derivations must explicitly show how the first-step estimation error is controlled in the second-step quantile without introducing additional bias terms that would invalidate consistency for the true Q_τ(β). The weaker sample-size conditions relative to fixed-effects QR are load-bearing for the central claim and require a precise statement of the panel dependence and design assumptions that justify the rates.

Authors: We agree that the asymptotic theory section would benefit from more explicit details on error control. In the current manuscript, the proofs in the appendix demonstrate that under the stochastic design, the first-step error is averaged out in the quantile estimation due to the cross-sectional independence, leading to the √N rate without additional bias. For the deterministic design, the √N√T rate arises when T grows. We will revise the main text to include a clearer statement of the assumptions on panel dependence and design, and add a remark comparing the sample size conditions to those of fixed-effects quantile regression. revision: yes

-

Referee: [Bootstrap procedures] Bootstrap validity (corresponding to the two designs): the formal proof of bootstrap consistency must address the same first-step error propagation; if the bootstrap is applied to the noisy β̂_i’s, it will replicate the convoluted limiting distribution rather than the target unless an explicit correction is embedded.

Authors: The bootstrap procedures are designed to resample the original panel data, thereby capturing the joint distribution of the first-step estimates and the second-step quantile. The validity proof establishes that the bootstrap mimics the asymptotic distribution of the estimator for Q_τ(β), accounting for the first-step error propagation. We will add a brief explanation in the main text (Section 4) to clarify this aspect and ensure readers understand that no separate correction is needed due to the resampling scheme. revision: yes

Circularity Check

No significant circularity detected in the two-step quantile estimation derivation

full rationale

The paper presents a two-step procedure that first obtains unit-specific slope estimates and then computes their cross-sectional τ-quantile, followed by separate asymptotic derivations under stochastic and deterministic designs plus bootstrap validity proofs. These steps rely on standard panel data regularity conditions and do not reduce by construction to a fitted parameter or self-referential quantity; the target quantile is defined externally as the τ-quantile of the heterogeneous coefficient distribution, and the asymptotics are derived from first principles rather than by renaming or importing unverified self-citations as load-bearing uniqueness theorems. No equations equate the estimator to its own input, and the bootstrap procedures are validated independently of the main claim.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith.Cost.FunctionalEquationwashburn_uniqueness_aczel unclearWe develop a two-step quantile estimation framework for analyzing heterogeneity in individual coefficients... convergence rates √N and √(N√T)

Reference graph

Works this paper leans on

-

[1]

Journal of Finance , volume=

Can mutual fund “stars” really pick stocks? New evidence from a bootstrap analysis , author=. Journal of Finance , volume=. 2006 , publisher=

2006

-

[2]

Journal of Finance , volume=

Luck versus skill in the cross-section of mutual fund returns , author=. Journal of Finance , volume=. 2010 , publisher=

2010

-

[3]

Journal of Finance , volume=

The performance of mutual funds in the period 1945-1964 , author=. Journal of Finance , volume=. 1968 , publisher=

1945

-

[4]

Journal of Finance , volume=

Efficient capital markets: A review of theory and empirical work , author=. Journal of Finance , volume=. 1970 , publisher=

1970

-

[5]

Journal of Finance , volume=

Luck versus Skill in the Cross Section of Mutual Fund Returns: Reexamining the Evidence , author=. Journal of Finance , volume=. 2022 , publisher=

2022

-

[6]

Econometrica , volume=

The model confidence set , author=. Econometrica , volume=. 2011 , publisher=

2011

-

[7]

Journal of Financial Economics , volume=

Picking funds with confidence , author=. Journal of Financial Economics , volume=. 2021 , publisher=

2021

-

[8]

Journal of Financial Economics , volume=

Cross-sectional alpha dispersion and performance evaluation , author=. Journal of Financial Economics , volume=. 2019 , publisher=

2019

-

[9]

Econometrica , volume=

A simple, positive semi-definite, heteroskedasticity and autocorrelationconsistent covariance matrix , author=. Econometrica , volume=. 1986 , publisher=

1986

-

[10]

Journal of Finance , volume=

False (and missed) discoveries in Financial economics , author=. Journal of Finance , volume=. 2020 , publisher=

2020

-

[11]

Journal of Econometrics , volume=

Bootstrap analysis of mutual fund performance , author=. Journal of Econometrics , volume=. 2023 , publisher=

2023

-

[12]

Journal of Finance , volume=

A first look at the accuracy of the CRSP mutual fund database and a comparison of the CRSP and Morningstar mutual fund databases , author=. Journal of Finance , volume=. 2001 , publisher=

2001

-

[13]

Econometrica , volume=

A reality check for data snooping , author=. Econometrica , volume=. 2000 , publisher=

2000

-

[14]

Journal of Finance , volume=

On persistence in mutual fund performance , author=. Journal of Finance , volume=. 1997 , publisher=

1997

-

[15]

Journal of Financial Economics , volume=

Can hedge funds time market liquidity? , author=. Journal of Financial Economics , volume=. 2013 , publisher=

2013

-

[16]

Journal of Finance , volume=

Performance and persistence in institutional investment management , author=. Journal of Finance , volume=. 2010 , publisher=

2010

-

[17]

Review of Financial Studies , volume=

Fundamental analysis and the cross-section of stock returns: A data-mining approach , author=. Review of Financial Studies , volume=. 2017 , publisher=

2017

-

[18]

Journal of Financial Economics , volume=

Do mutual funds time the market? Evidence from portfolio holdings , author=. Journal of Financial Economics , volume=. 2007 , publisher=

2007

-

[19]

Econometrica , volume=

Panel data models with interactive fixed effects , author=. Econometrica , volume=. 2009 , publisher=

2009

-

[20]

Economics letters , volume=

Evaluating the size of the bootstrap method for fund performance evaluation , author=. Economics letters , volume=. 2017 , publisher=

2017

-

[21]

1977 , publisher=

Exploratory data analysis , author=. 1977 , publisher=

1977

-

[22]

Journal of Financial Economics , volume=

Asset pricing with liquidity risk , author=. Journal of Financial Economics , volume=. 2005 , publisher=

2005

-

[23]

Review of Financial Studies , volume=

Volatility timing in mutual funds: Evidence from daily returns , author=. Review of Financial Studies , volume=. 1999 , publisher=

1999

-

[24]

Review of Economics and Statistics , volume=

Bootstrap-based improvements for inference with clustered errors , author=. Review of Economics and Statistics , volume=. 2008 , publisher=

2008

-

[25]

1992 , publisher=

Bootstrap methods: another look at the jackknife , author=. 1992 , publisher=

1992

-

[26]

Journal of Financial Economics , volume=

Common risk factors in the returns on stocks and bonds , author=. Journal of Financial Economics , volume=. 1993 , publisher=

1993

-

[27]

Journal of Econometrics , volume=

Bootstrapping integrated covariance matrix estimators in noisy jump--diffusion models with non-synchronous trading , author=. Journal of Econometrics , volume=. 2017 , publisher=

2017

-

[28]

Econometric Theory , volume=

A local Gaussian bootstrap method for realized volatility and realized beta , author=. Econometric Theory , volume=. 2019 , publisher=

2019

-

[29]

Econometric Theory , volume=

Bootstrapping pre-averaged realized volatility under market microstructure noise , author=. Econometric Theory , volume=. 2017 , publisher=

2017

-

[30]

Journal of Money, Credit and Banking, Forthcoming , year=

Are Some Forecasters Really Better than Others? A Note , author=. Journal of Money, Credit and Banking, Forthcoming , year=

-

[31]

Available at SSRN 3523293 , year=

Bootstrapping Laplace transforms of volatility , author=. Available at SSRN 3523293 , year=

-

[32]

Annals of Statistics , volume=

Bootstrap procedures under some non-iid models , author=. Annals of Statistics , volume=. 1988 , publisher=

1988

-

[33]

Annals of Statistics , volume=

Jackknife, bootstrap and other resampling methods in regression analysis , author=. Annals of Statistics , volume=. 1986 , publisher=

1986

-

[34]

Annals of Statistics , volume=

Bootstrap Methods: Another Look at the Jackknife , author=. Annals of Statistics , volume=. 1979 , publisher=

1979

-

[35]

Annals of Statistics , volume=

Bootstrap and wild bootstrap for high dimensional linear models , author=. Annals of Statistics , volume=. 1993 , publisher=

1993

-

[36]

Journal of Econometrics , volume=

The wild bootstrap, tamed at last , author=. Journal of Econometrics , volume=. 2008 , publisher=

2008

-

[37]

Journal of Finance , volume=

Reassessing false discoveries in mutual fund performance: Skill, luck, or lack of power? , author=. Journal of Finance , volume=. 2019 , publisher=

2019

-

[38]

Journal of Finance , volume=

False discoveries in mutual fund performance: Measuring luck in estimated alphas , author=. Journal of Finance , volume=. 2010 , publisher=

2010

-

[39]

Journal of Finance, Forthcoming , year=

Reassessing false discoveries in mutual fund performance: Skill, luck, or lack of power? A reply , author=. Journal of Finance, Forthcoming , year=

-

[40]

Review of Financial Studies , volume=

Thousands of alpha tests , author=. Review of Financial Studies , volume=. 2021 , publisher=

2021

-

[41]

Annals of Statistics , volume=

Phase transition and regularized bootstrap in large-scale -tests with false discovery rate control , author=. Annals of Statistics , volume=. 2014 , publisher=

2014

-

[42]

Econometrica , volume=

Power enhancement in high-dimensional cross-sectional tests , author=. Econometrica , volume=. 2015 , publisher=

2015

-

[43]

Econometric Theory , volume=

The size distortion of bootstrap tests , author=. Econometric Theory , volume=. 1999 , publisher=

1999

-

[44]

Journal of Finance , volume=

Alpha and performance measurement: The effects of investor disagreement and heterogeneity , author=. Journal of Finance , volume=. 2014 , publisher=

2014

-

[45]

Review of Asset Pricing Studies , volume=

Mutual fund industry selection and persistence , author=. Review of Asset Pricing Studies , volume=. 2012 , publisher=

2012

-

[46]

Journal of Finance , volume=

Mutual fund performance: An empirical decomposition into stock-picking talent, style, transactions costs, and expenses , author=. Journal of Finance , volume=. 2000 , publisher=

2000

-

[47]

Journal of Financial and Quantitative Analysis , volume=

The value of active mutual fund management: An examination of the stockholdings and trades of fund managers , author=. Journal of Financial and Quantitative Analysis , volume=. 2000 , publisher=

2000

-

[48]

Econometrica , volume=

Heteroskedasticity and autocorrelation consistent covariance matrix estimation , author=. Econometrica , volume=. 1991 , publisher=

1991

-

[49]

Journal of Financial Economics , volume=

Technical trading revisited: False discoveries, persistence tests, and transaction costs , author=. Journal of Financial Economics , volume=. 2012 , publisher=

2012

-

[50]

The New Palgrave Dictionary of Economics

Multiple testing , author=. The New Palgrave Dictionary of Economics. Forthcoming , year=

-

[51]

Test , volume=

Control of the false discovery rate under dependence using the bootstrap and subsampling , author=. Test , volume=. 2008 , publisher=

2008

-

[52]

Econometric Theory , volume=

Formalized data snooping based on generalized error rates , author=. Econometric Theory , volume=. 2008 , publisher=

2008

-

[53]

Scandinavian Journal of Statistics , pages=

A simple sequentially rejective multiple test procedure , author=. Scandinavian Journal of Statistics , pages=. 1979 , publisher=

1979

-

[54]

Journal of the Royal statistical society: series B (Methodological) , volume=

Controlling the false discovery rate: a practical and powerful approach to multiple testing , author=. Journal of the Royal statistical society: series B (Methodological) , volume=. 1995 , publisher=

1995

-

[55]

Review of Financial Studies , volume=

… and the cross-section of expected returns , author=. Review of Financial Studies , volume=. 2016 , publisher=

2016

-

[56]

Multiple testing in economics , author=

-

[57]

Handbook of Financial Econometrics, Mathematics, Statistics, and Machine Learning , pages=

How many good and bad funds are there, really? , author=. Handbook of Financial Econometrics, Mathematics, Statistics, and Machine Learning , pages=. 2021 , publisher=

2021

-

[58]

Review of Financial Studies , volume=

Detecting repeatable performance , author=. Review of Financial Studies , volume=. 2018 , publisher=

2018

-

[59]

Annals of Statistics , volume=

Improved central limit theorem and bootstrap approximations in high dimensions , author=. Annals of Statistics , volume=. 2022 , publisher=

2022

-

[60]

Review of Finance , volume=

Investing in a global world , author=. Review of Finance , volume=. 2014 , publisher=

2014

-

[61]

Journal of Finance , volume=

Decentralized investment management: Evidence from the pension fund industry , author=. Journal of Finance , volume=. 2013 , publisher=

2013

-

[62]

Review of Financial Studies , volume=

Anomalies and false rejections , author=. Review of Financial Studies , volume=. 2020 , publisher=

2020

-

[63]

Journal of Money, Credit and Banking , volume=

Are some forecasters really better than others? , author=. Journal of Money, Credit and Banking , volume=. 2012 , publisher=

2012

-

[64]

Journal of Financial Economics , volume=

Do hedge funds deliver alpha? A Bayesian and bootstrap analysis , author=. Journal of Financial Economics , volume=. 2007 , publisher=

2007

-

[65]

Journal of Financial and Quantitative Analysis , volume=

New evidence on mutual fund performance: A comparison of alternative bootstrap methods , author=. Journal of Financial and Quantitative Analysis , volume=. 2017 , publisher=

2017

-

[66]

Journal of Econometrics , volume=

Improved inference in the evaluation of mutual fund performance using panel bootstrap methods , author=. Journal of Econometrics , volume=. 2014 , publisher=

2014

-

[67]

The Fama Portfolio: Selected Papers of Eugene F

Luck versus Skill and Factor Selection , author=. The Fama Portfolio: Selected Papers of Eugene F. Fama , year=

-

[68]

Journal of Financial and Quantitative Analysis , volume=

Using stocks or portfolios in tests of factor models , author=. Journal of Financial and Quantitative Analysis , volume=. 2020 , publisher=

2020

-

[69]

Review of Financial Studies , volume=

Fund flows and market states , author=. Review of Financial Studies , volume=. 2017 , publisher=

2017

-

[70]

2009 , institution=

Is investor rationality time varying? Evidence from the mutual fund industry , author=. 2009 , institution=

2009

-

[71]

Journal of Finance, Forthcoming , pages=

Time-Varying Fund Manager Skill , author=. Journal of Finance, Forthcoming , pages=

-

[72]

Econometrica , volume=

A rational theory of mutual funds' attention allocation , author=. Econometrica , volume=. 2016 , publisher=

2016

-

[73]

Review of Finance , volume=

Improved forecasting of mutual fund alphas and betas , author=. Review of Finance , volume=. 2007 , publisher=

2007

-

[74]

Review of Financial Studies , volume=

Estimating the dynamics of mutual fund alphas and betas , author=. Review of Financial Studies , volume=. 2008 , publisher=

2008

-

[75]

Journal of Finance , volume=

The persistence of mutual fund performance , author=. Journal of Finance , volume=. 1992 , publisher=

1992

-

[76]

Review of Financial Studies , volume=

Mutual fund competition, managerial skill, and alpha persistence , author=. Review of Financial Studies , volume=. 2018 , publisher=

2018

-

[77]

Journal of Finance , volume=

Evaluating mutual fund performance , author=. Journal of Finance , volume=. 2001 , publisher=

2001

-

[78]

Mutual fund performance: evidence from the

Blake, David and Timmermann, Allan , journal=. Mutual fund performance: evidence from the. 1998 , publisher=

1998

-

[79]

Journal of Finance , volume=

Are some mutual fund managers better than others? Cross-sectional patterns in behavior and performance , author=. Journal of Finance , volume=. 1999 , publisher=

1999

-

[80]

Journal of Finance , volume=

Another puzzle: The growth in actively managed mutual funds , author=. Journal of Finance , volume=. 1996 , publisher=

1996

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.