Recognition: no theorem link

Analytic approximation for Bachelier option prices and applications

Pith reviewed 2026-05-12 00:55 UTC · model grok-4.3

The pith

Bachelier option prices for OTM and ITM strikes expand in moneyness with coefficients given by negative powers of future mean volatility.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

In the uncorrelated Bachelier model the price of an out-of-the-money or in-the-money option admits an asymptotic expansion in powers of moneyness whose coefficients are explicit functionals of the negative (non-integer) powers of the future mean volatility; the expansion is obtained by applying Itô's formula to the Bachelier payoff and then performing a Taylor expansion in the strike variable.

What carries the argument

Moneyness Taylor expansion of the Bachelier payoff combined with Itô calculus to express the resulting expectations in terms of negative powers of the integrated future volatility.

If this is right

- The expansion recovers the known identity that implied volatility equals the fair value of the volatility swap when asset and volatility are uncorrelated.

- Truncation of the series yields a fast analytic approximation for near-at-the-money Bachelier prices.

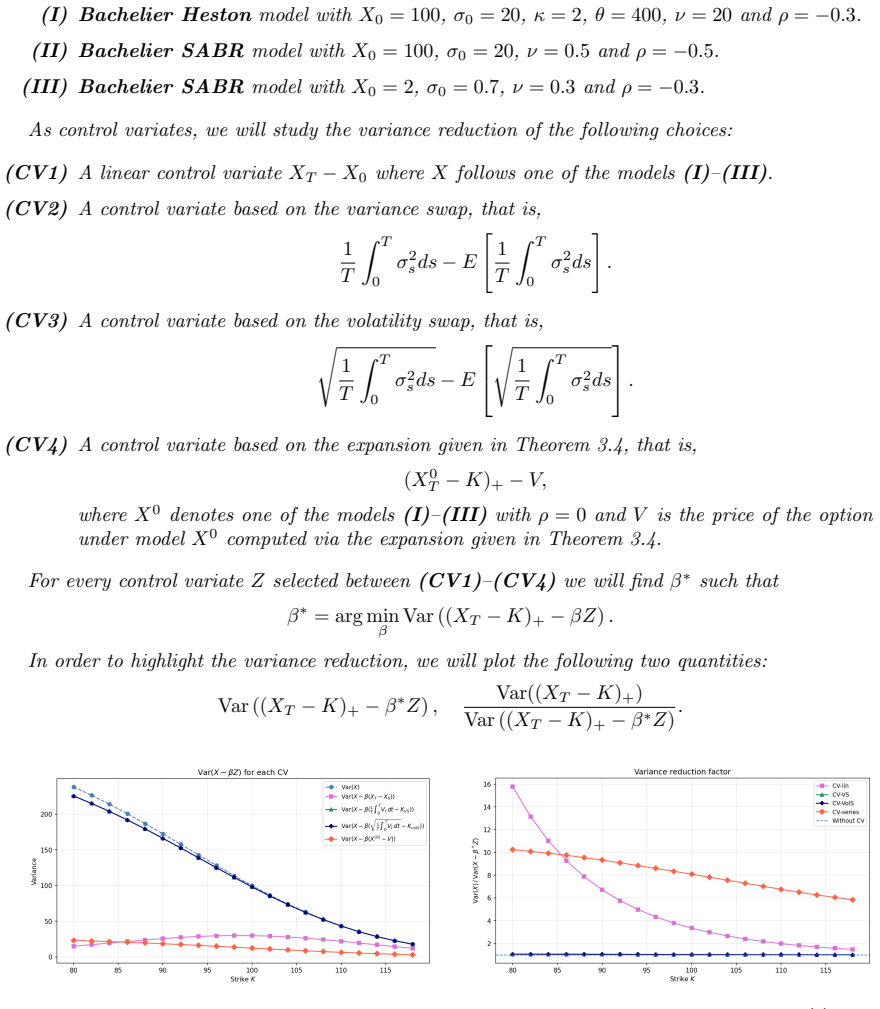

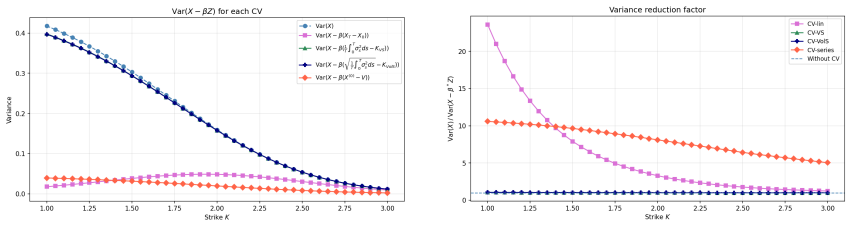

- The same expansion serves as an effective control variate that materially lowers the variance of Monte Carlo estimators in the correlated Bachelier model.

- Higher-order terms can be generated systematically by continuing the Taylor expansion and applying further Itô corrections.

Where Pith is reading between the lines

- The same moneyness-expansion technique may be portable to other diffusion models whose payoff admits a simple Taylor series in strike.

- In practice the control-variate version could accelerate risk calculations for portfolios of Bachelier-style options without requiring full path simulation for every contract.

- The appearance of negative volatility moments suggests possible links to moment-generating functions or cumulant expansions used in other stochastic-volatility pricing routines.

Load-bearing premise

The Taylor expansion in moneyness converges rapidly enough for the strikes of practical interest and the future mean volatility can be treated as a deterministic quantity whose negative powers enter the coefficients directly.

What would settle it

Compute the exact Bachelier price for a fixed strike and volatility path, subtract the truncated expansion, and verify that the remainder shrinks at the expected rate as more terms are added; alternatively, run Monte Carlo pricing in the correlated case both with and without the expansion as control variate and measure the reduction in sample variance.

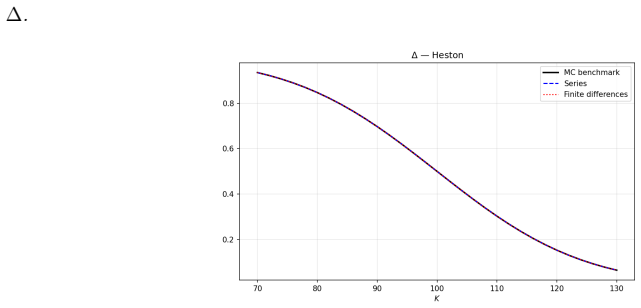

Figures

read the original abstract

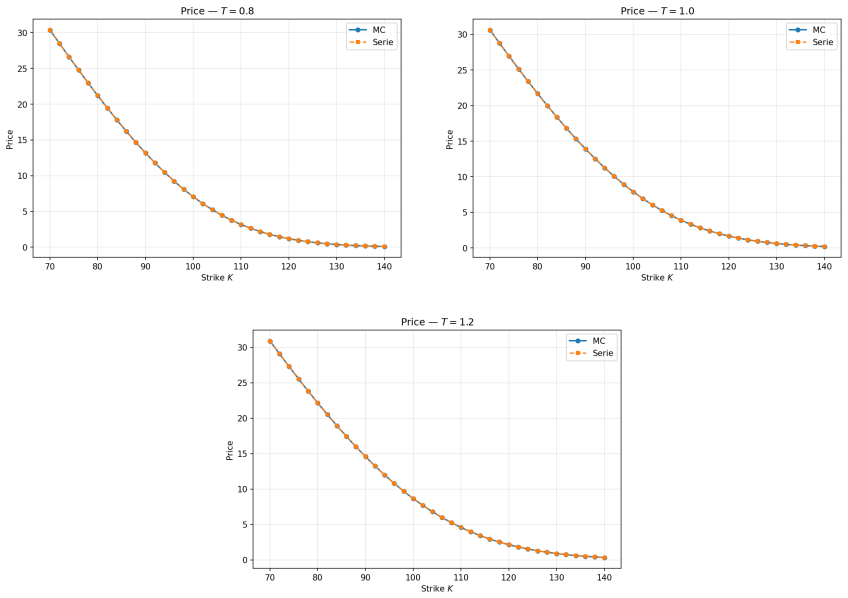

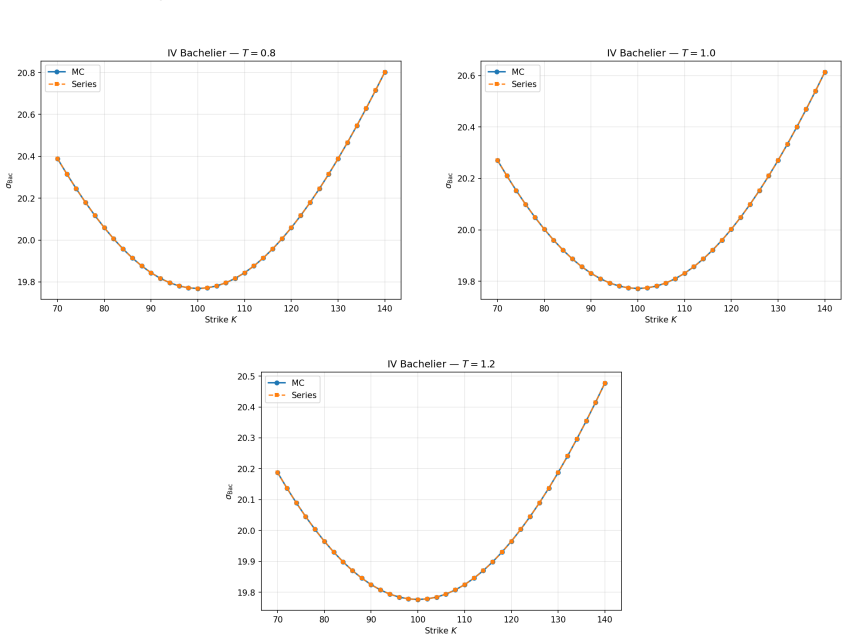

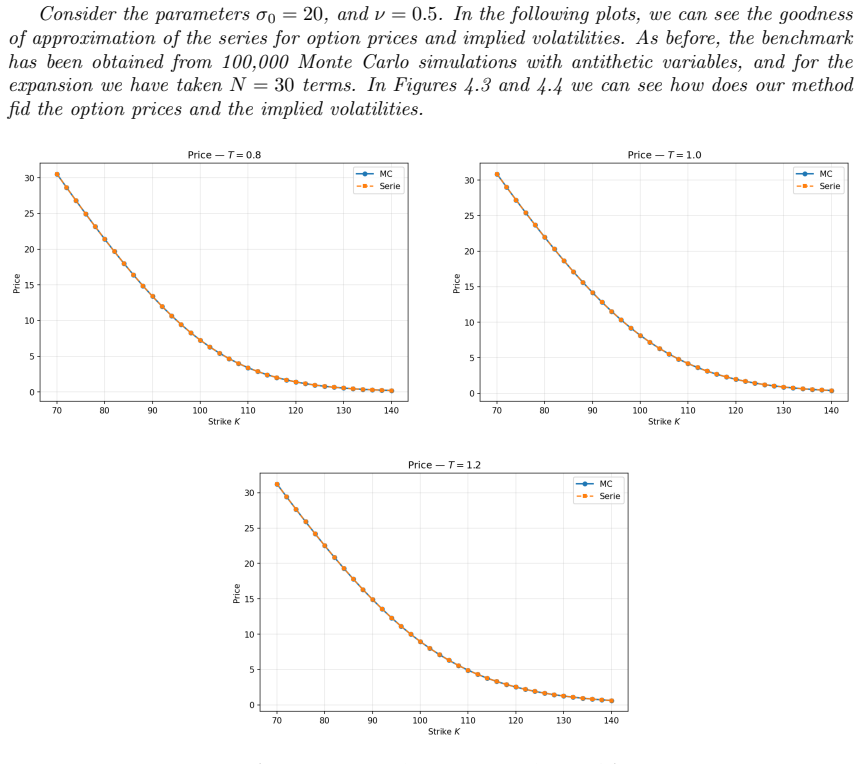

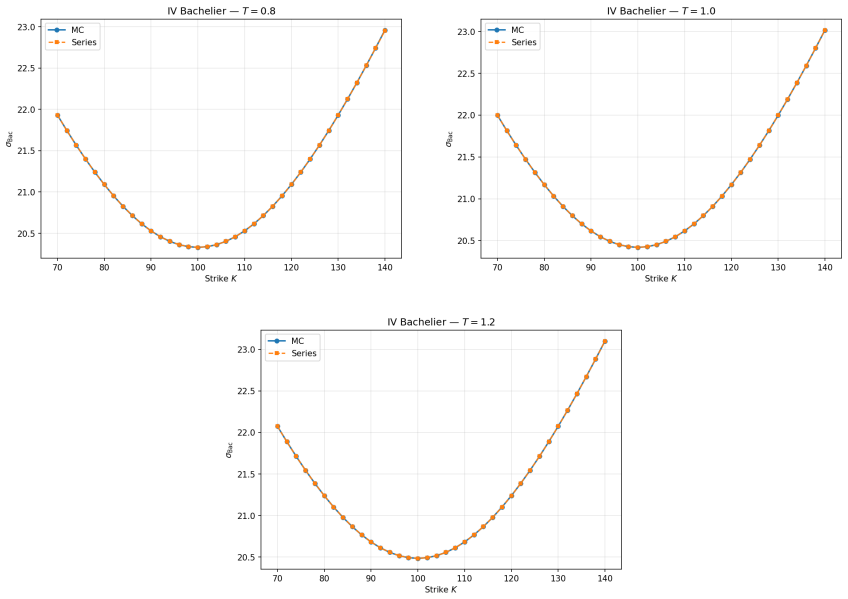

It is well-known that, in the Bachelier model, when asset prices and volatilities are uncorrelated, the implied volatility coincides with the fair value of the volatility swap. In this paper, via classical It\^o calculus and Taylor expansions, we write the price for out-of-the-money (OTM) and in-the-money (ITM) options as an expansion with respect to the moneyness, where the coefficients are related to the negative (non-integer) powers of the future mean volatility. As an a application, we use it as a control variate to reduce the variance of Monte Carlo option prices in the correlated case.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript derives an analytic series approximation for out-of-the-money and in-the-money option prices in the Bachelier (normal) model. Starting from the stochastic differential equation for the forward price and applying Itô calculus followed by a Taylor expansion in the moneyness variable m = F − K, the authors obtain explicit coefficients that involve negative non-integer powers of the future mean volatility. The resulting expansion is then used as a control variate to reduce the variance of Monte Carlo price estimates when the asset price and volatility processes are correlated.

Significance. If the expansion is shown to be accurate over the relevant moneyness range and the control-variate variance reduction is quantified, the work supplies a practical, closed-form tool for Bachelier-model pricing and simulation. The reliance on classical Itô calculus and Taylor series rather than ad-hoc fitting is a methodological strength; the control-variate application directly addresses a common computational bottleneck in stochastic-volatility Monte Carlo.

major comments (2)

- [§3] §3, Eq. (12)–(15): the Taylor expansion in moneyness is written with coefficients containing terms σ̄^{−p} for non-integer p > 0. When volatility is stochastic (even if uncorrelated with the asset), the true price is E[ Bachelier(F, K, σ) ], and interchanging the series with the outer expectation is not automatic for negative powers; the manuscript provides no justification or moment conditions that would validate pulling the powers outside the expectation.

- [§4] §4, Table 1 and Figure 3: no radius-of-convergence estimate or truncation-error bound is supplied for the moneyness expansion. Without such a bound or a systematic numerical comparison of the truncated series against the exact Bachelier formula across |m|/(σ̄√T) ∈ [0, 3], it is impossible to assess whether the approximation remains useful for the OTM strikes that are the primary target of the control-variate application.

minor comments (2)

- The notation for the future mean volatility is introduced as σ̄ in the text but appears as σ_m in some displayed equations; a single consistent symbol would eliminate ambiguity.

- [Abstract] The abstract states that the expansion coefficients are “related to” negative powers of volatility, yet the explicit formulae in §3 contain additional factors involving the normal density and its derivatives; a brief sentence clarifying the precise functional dependence would improve readability.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on our manuscript. The two major points raised concern the justification for interchanging the series with the expectation under stochastic volatility and the need for better error analysis and numerical validation of the expansion. Both can be addressed by targeted revisions, as detailed below.

read point-by-point responses

-

Referee: [§3] §3, Eq. (12)–(15): the Taylor expansion in moneyness is written with coefficients containing terms σ̄^{−p} for non-integer p > 0. When volatility is stochastic (even if uncorrelated with the asset), the true price is E[ Bachelier(F, K, σ) ], and interchanging the series with the outer expectation is not automatic for negative powers; the manuscript provides no justification or moment conditions that would validate pulling the powers outside the expectation.

Authors: The derivation begins from the closed-form Bachelier price for deterministic volatility and expands the normal cdf and pdf terms in powers of moneyness m before any expectation is taken. When volatility is stochastic but uncorrelated, the price is the outer expectation of that expression. The negative powers of the mean volatility appear in the coefficients after the expansion. We agree that a rigorous justification for interchanging the infinite series with the outer expectation is missing. In the revision we will add a short paragraph in Section 3 stating the sufficient conditions (e.g., the volatility process is bounded away from zero almost surely and possesses finite moments of all orders up to the truncation order) under which the interchange is justified by dominated convergence or uniform integrability. This will also clarify that the control-variate application in the correlated case inherits the same local expansion per path. revision: yes

-

Referee: [§4] §4, Table 1 and Figure 3: no radius-of-convergence estimate or truncation-error bound is supplied for the moneyness expansion. Without such a bound or a systematic numerical comparison of the truncated series against the exact Bachelier formula across |m|/(σ̄√T) ∈ [0, 3], it is impossible to assess whether the approximation remains useful for the OTM strikes that are the primary target of the control-variate application.

Authors: A closed-form radius of convergence for the moneyness series is indeed difficult to obtain because the coefficients depend on the random mean volatility. We therefore focus on practical validation. In the revised manuscript we will replace the current Table 1 with an expanded table that reports the absolute and relative errors of the truncated series (orders 2, 3 and 4) against the exact Bachelier formula for a grid of normalized moneyness values |m|/(σ̄√T) from 0 to 3, using several representative volatility levels. An additional panel in Figure 3 will display the error decay as a function of truncation order for the most OTM strikes. These additions will quantify the range where the approximation remains accurate enough for the control-variate purpose. revision: yes

Circularity Check

No circularity: derivation uses independent Itô calculus and Taylor series on standard Bachelier model.

full rationale

The paper derives an expansion for Bachelier OTM/ITM option prices via classical Itô calculus and Taylor expansions in moneyness, with coefficients involving negative powers of the (deterministic) future mean volatility under the uncorrelated assumption. These steps rely on standard stochastic calculus identities and series expansions whose validity does not depend on the final formula or any fitted quantity defined by the result. No self-citations are invoked as load-bearing premises, no parameters are fitted to data and then relabeled as predictions, and no ansatz or uniqueness theorem is smuggled in. The central claim remains a direct mathematical consequence of the model assumptions and does not reduce to its own inputs by construction.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Classical Ito calculus applies to the Bachelier processes

- domain assumption Taylor expansion of the option price function around moneyness is valid to the required order

Reference graph

Works this paper leans on

-

[1]

Alòs, E. (2012). A decomposition formula for option prices in the heston model and applications to option pricing approximation.Finance and Stochastics, 16(3):403–422. Alòs, E., Burés, Ò., and Vives, J. (2025). Short-time behavior of the at-the-money implied volatil- ity for the jump-diffusion stochastic volatility bachelier model.arXiv preprint arXiv:250...

-

[2]

Antonelli, F. and Scarlatti, S. (2009). Pricing options under stochastic volatility: a power series approach.Finance Stoch., 13(2):269–303

work page 2009

-

[3]

Bachelier, L. (1900). Théorie de la spéculation.Annales scientifiques de l’École Normale Supérieure, 3e série, 17:21–86

work page 1900

-

[4]

Baviera, R. and Massaria, M. D. (2025). Smile asymptotic for bachelier implied volatility.arXiv preprint arXiv:2506.08067

-

[5]

Bergomi, L. and Guyon, J. (2012). Stochastic volatility’s orderly smiles.Risk Magazine, pages 60–66

work page 2012

-

[6]

Choi, J., Kwak, M., Tee, C. W., and Wang, Y. (2022). A Black–Scholes user’s guide to the Bachelier model.Journal of Futures Markets, 42(5):959–980. Floc’h, F. L. (2022). On the bachelier implied volatility at extreme strikes.arXiv preprint arXiv:2211.10232

-

[7]

Fouque, J.-P., Papanicolaou, G., and Sircar, K. R. (2000).Derivatives in financial markets with stochastic volatility. Cambridge University Press

work page 2000

-

[8]

P., Papanicolaou, G., Sircar, R., and Solna, K

Fouque, J. P., Papanicolaou, G., Sircar, R., and Solna, K. (2003). Singular perturbations in option pricing.SIAM Journal on Applied Mathematics, 63(5):1648–1665

work page 2003

-

[9]

Fukasawa, M. (2011). Asymptotic analysis for stochastic volatility: martingale expansion.Finance and Stochastics, 15:635–654

work page 2011

-

[10]

Hagan, P. S., Kumar, D., Lesniewski, A. S., and Woodward, D. E. (2002). Managing smile risk. The Best of Wilmott, 1(1):249–296. 14

work page 2002

-

[11]

Lewis, A. L. (2016).Option valuation under stochastic volatility. II. Finance Press, Newport

work page 2016

-

[12]

Lewis, A. L. and Pirjol, D. (2022). Proof of non-convergence of the short-maturity expansion for the sabr model.Quantitative Finance, 22(9):1747–1757. 15

work page 2022

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.