Recognition: unknown

Deepening the Secondary Market: Integrating Trade Credit into Market Clearing with the Cycles Protocol

Pith reviewed 2026-05-08 01:33 UTC · model grok-4.3

The pith

The Cycles Protocol clears obligations multilaterally on existing networks by atomic cycle execution without novation or counterparty risk redistribution.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

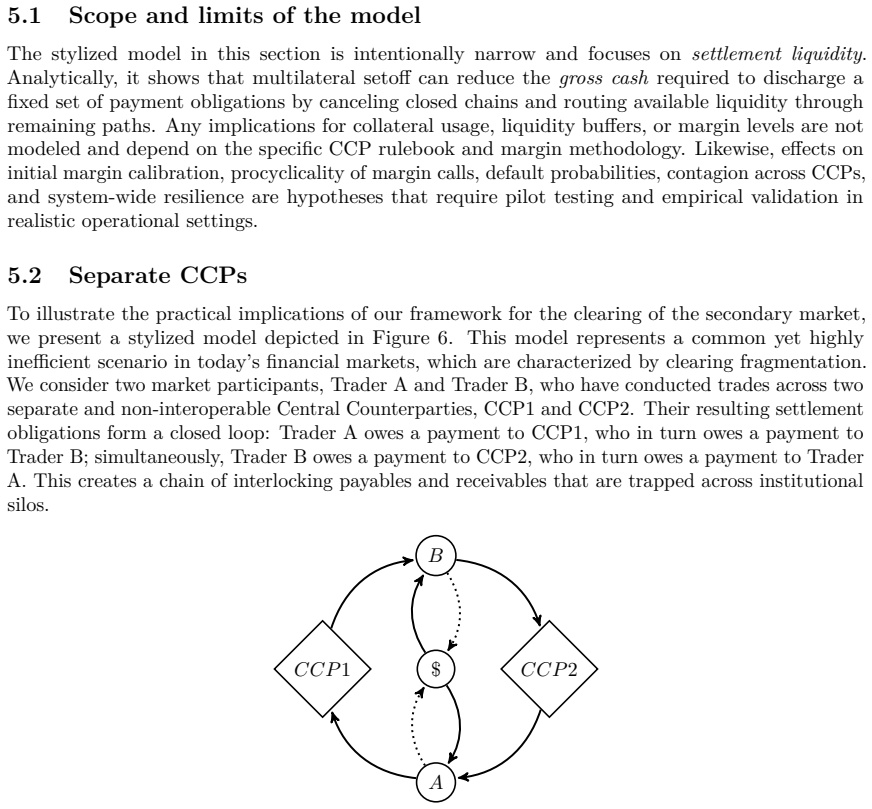

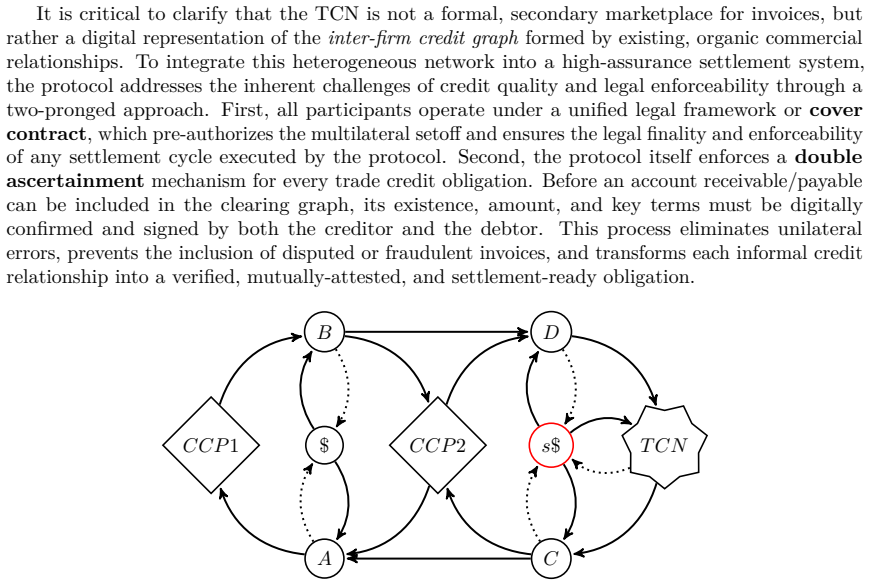

The Cycles Protocol is a distributed, multilateral clearing mechanism based on double-entry accounting and atomic cycle execution that maximizes balance sheet compression. Unlike novation-based clearing, Cycles does not redistribute counterparty risk; it can thus be applied generally to existing financial networks, without any change in counterparty relations, allowing it to complement existing clearing systems and Central Counterparties (CCPs). By representing commitments as edges on a unified directed graph, Cycles surfaces liquidity hiding within existing network structure and focuses on applications as a compression layer for CCPs and as a way to incorporate trade credit into formal结算.

What carries the argument

The Cycles Protocol, a distributed multilateral clearing system that models obligations as edges on a unified directed graph and clears them via atomic cycle execution while preserving original counterparty relations.

If this is right

- It can function as a compression layer between existing clearing participants and CCPs.

- Trade credit liquidity from real-economy networks can enter formal settlement without changes to counterparty structures.

- Existing financial networks can adopt the protocol generally to surface hidden liquidity.

- Market clearing extends beyond financial obligations into real-economy financing.

Where Pith is reading between the lines

- If distributed execution proves feasible, dependence on cash collateral could decrease through greater netting of non-cash obligations.

- Real-economy firms might gain indirect access to deeper secondary markets via integrated trade credit clearing.

- Testing on historical trade credit graphs could reveal whether cycle compression scales without legal friction.

Load-bearing premise

Atomic cycle execution on a unified directed graph can be performed in a distributed manner at scale while preserving the exact existing counterparty relations and without introducing new settlement or legal risks.

What would settle it

A demonstration on a real financial network graph showing that large-scale distributed cycle detection and execution either redistributes counterparty risk, creates new settlement risks, or fails to preserve all original relations.

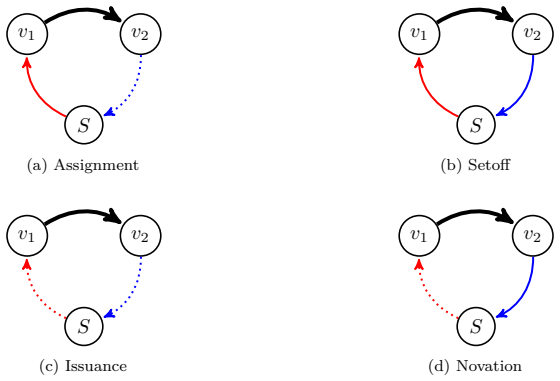

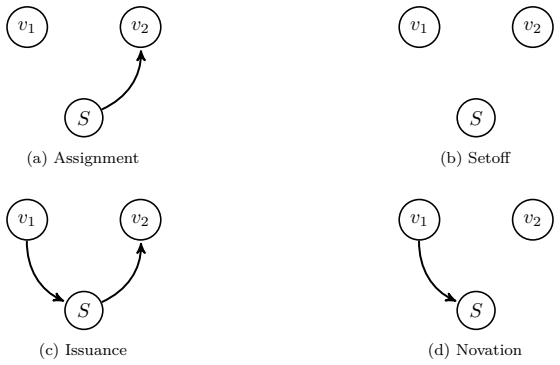

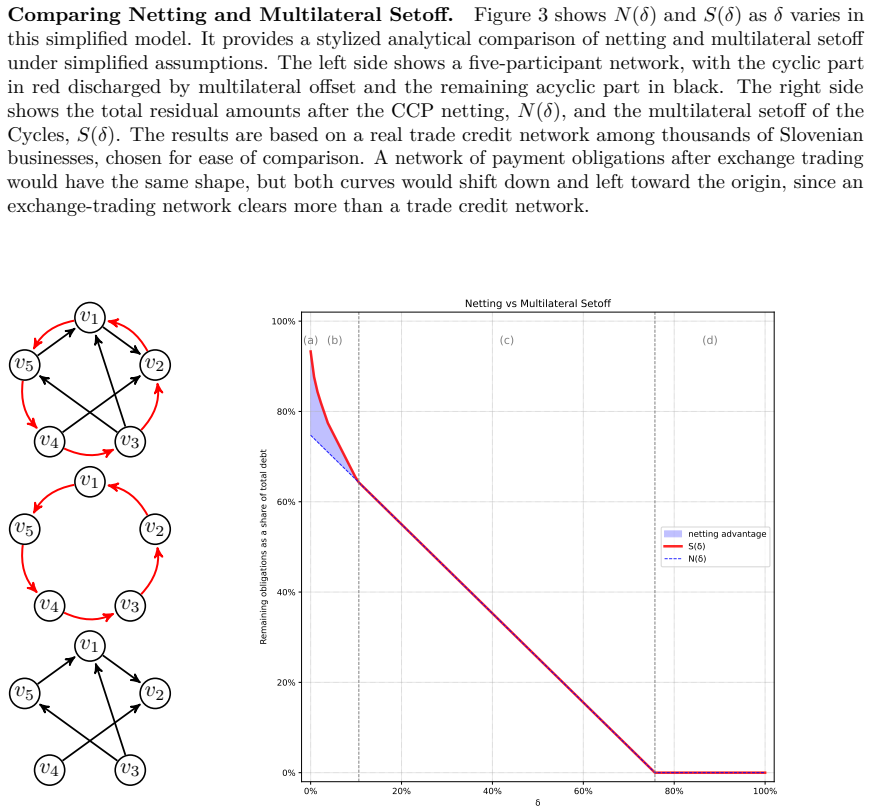

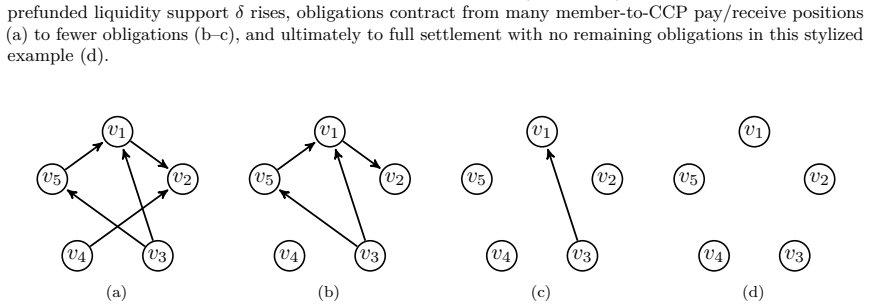

Figures

read the original abstract

Current post-trade clearing systems rely almost exclusively on cash or cash-like collateral, leaving vast reserves of short-term liquidity embedded in trade credit outside formal settlement infrastructures. A key barrier to integrating this liquidity is the near-universal dependence of clearing services on novation, which imposes institutional overhead that restricts accessibility and limits the range of obligations that can be brought into settlement. This paper introduces the Cycles Protocol: a distributed, multilateral clearing mechanism based on double-entry accounting and atomic cycle execution that maximizes balance sheet compression. Unlike novation-based clearing, Cycles does not redistribute counterparty risk; it can thus be applied generally to existing financial networks, without any change in counterparty relations, allowing it to complement existing clearing systems and Central Counterparties (CCPs). By representing commitments as edges on a unified directed graph, Cycles surfaces liquidity hiding within existing network structure. We focus here on two applications of Cycles to deepening secondary market liquidity: first, as a compression layer between existing clearing participants and CCPs; and second, as a means to incorporate the liquidity of the trade credit network into formal settlement, extending market clearing beyond financial obligations and into real-economy financing.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes the Cycles Protocol, a distributed multilateral clearing mechanism based on double-entry accounting and atomic cycle execution on a unified directed graph of commitments. It claims this approach achieves balance-sheet compression and integrates trade credit liquidity into formal settlement without the institutional overhead of novation, thereby avoiding redistribution of counterparty risk and preserving exact existing bilateral relations so that the protocol can complement rather than replace CCPs and existing clearing systems.

Significance. If the central claims regarding risk preservation and distributed atomic execution can be formally established and validated, the protocol could meaningfully deepen secondary-market liquidity by mobilizing embedded trade-credit reserves without requiring new collateral or counterparty changes, offering a practical complement to current post-trade infrastructure.

major comments (3)

- [Abstract] Abstract: the claim that 'Cycles does not redistribute counterparty risk' and 'can be applied generally to existing financial networks, without any change in counterparty relations' is asserted descriptively but receives no mathematical derivation, formal model, or risk-analysis section demonstrating that atomic cycle execution on the directed graph preserves exact bilateral exposures under distributed execution.

- [Protocol description] Protocol description (assumed §3–4): no specification is given of the consensus mechanism, failure model, or atomic-commit protocol that would guarantee (a) no new edges or counterparties are created, (b) no participant incurs additional settlement risk during multi-party execution, and (c) the process scales beyond toy graphs without central coordination.

- [Applications] Applications section: the two use-cases (compression layer to CCPs; incorporation of trade-credit network) rest on the unverified assumption that cycle execution can be performed in a fully distributed manner while satisfying the above constraints; no simulation results, complexity analysis, or empirical validation are supplied to support scalability or legal-risk claims.

minor comments (2)

- [Abstract] The abstract and introduction would benefit from a short paragraph contrasting the Cycles approach with existing multilateral netting protocols (e.g., those based on graph-theoretic cycle decomposition) to clarify novelty.

- [Protocol description] Notation for the directed graph (vertices as participants, directed edges as obligations) is introduced informally; an explicit definition of the edge-weight update rule under cycle execution would improve clarity.

Simulated Author's Rebuttal

We are grateful to the referee for the thoughtful and detailed comments, which have helped us identify areas where the manuscript can be strengthened. We provide point-by-point responses to the major comments below and indicate the revisions we plan to make.

read point-by-point responses

-

Referee: [Abstract] Abstract: the claim that 'Cycles does not redistribute counterparty risk' and 'can be applied generally to existing financial networks, without any change in counterparty relations' is asserted descriptively but receives no mathematical derivation, formal model, or risk-analysis section demonstrating that atomic cycle execution on the directed graph preserves exact bilateral exposures under distributed execution.

Authors: The core property of risk preservation stems from the fact that the protocol operates exclusively on existing directed edges in the commitment graph, executing atomic cycles that mutually offset obligations without introducing new counterparties or altering bilateral net positions. This invariance is a direct consequence of the double-entry accounting and cycle-based cancellation described in the protocol. To make this rigorous, we will add a formal model subsection in the revised manuscript, including a mathematical demonstration that for any participant, the exposure to each specific counterparty remains unchanged post-execution, along with a brief risk-analysis discussion. revision: yes

-

Referee: [Protocol description] Protocol description (assumed §3–4): no specification is given of the consensus mechanism, failure model, or atomic-commit protocol that would guarantee (a) no new edges or counterparties are created, (b) no participant incurs additional settlement risk during multi-party execution, and (c) the process scales beyond toy graphs without central coordination.

Authors: We clarify that the Cycles Protocol defines the clearing logic at the application level and relies on an underlying atomic transaction mechanism to ensure the listed guarantees. Property (a) is ensured by construction since only existing edges are modified. For (b) and (c), we assume a reliable atomic commit protocol (such as those used in distributed databases or permissioned ledgers) that prevents partial executions. We will revise the protocol description section to explicitly outline these assumptions, discuss relevant failure models (e.g., crash failures vs. Byzantine), and provide a high-level complexity analysis showing that cycle finding is efficient for sparse financial graphs, scaling to networks with thousands of nodes using standard algorithms. revision: yes

-

Referee: [Applications] Applications section: the two use-cases (compression layer to CCPs; incorporation of trade-credit network) rest on the unverified assumption that cycle execution can be performed in a fully distributed manner while satisfying the above constraints; no simulation results, complexity analysis, or empirical validation are supplied to support scalability or legal-risk claims.

Authors: The applications are presented as conceptual extensions of the protocol rather than fully validated implementations. We will incorporate a complexity analysis for the cycle detection and execution steps to address scalability. Regarding empirical validation and legal-risk claims, these would indeed benefit from simulations and case studies; however, as the current work focuses on introducing the protocol and its theoretical integration with existing systems, we will note the need for such validation in future work and add a brief discussion of potential legal considerations based on the preservation of existing relations. revision: partial

- Comprehensive simulation results, empirical validation for scalability, and detailed legal-risk assessments, which are not available in the current manuscript and would require substantial additional research.

Circularity Check

No circularity: new protocol construction with independent design claims

full rationale

The paper introduces the Cycles Protocol as a graph-based multilateral clearing mechanism using double-entry accounting and atomic cycle execution. The central claim (no redistribution of counterparty risk, applicability to existing networks without altering relations) follows directly from the stated design choice of avoiding novation, rather than from any fitted parameters, self-referential equations, or load-bearing self-citations. No derivations reduce outputs to inputs by construction; the proposal is presented as a new construction whose properties are asserted from its mechanics. This is the expected non-circular outcome for a protocol paper.

Axiom & Free-Parameter Ledger

axioms (2)

- standard math Double-entry accounting rules hold for all represented obligations

- domain assumption Atomic execution of cycles is feasible in a distributed network

invented entities (1)

-

Cycles Protocol

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Anderson and Karin J˜ oeveer

Ronald W. Anderson and Karin J˜ oeveer. The economics of collateral. Technical report, Systemic Risk Centre, The London School of Economics and Political Science, London, UK,

-

[2]

Discussion Paper Series

-

[3]

The welfare effects of a liquidity-saving mechanism

Enghin Atalay, Antoine Martin, and James McAndrews. The welfare effects of a liquidity-saving mechanism. Staff Report 354, Federal Reserve Bank of New York, 2008

2008

-

[4]

Emergence of scaling in random networks.Science, 286(5439):509–512, 1999

Albert-L´ aszl´ o Barab´ asi and R´ eka Albert. Emergence of scaling in random networks.Science, 286(5439):509–512, 1999

1999

-

[5]

Trade credit and industry dynamics: Evidence from trucking firms.The Journal of Finance, 71(5):1975–2016, 2016

Jean-Noel Barrot. Trade credit and industry dynamics: Evidence from trucking firms.The Journal of Finance, 71(5):1975–2016, 2016

1975

-

[6]

The economics of distributed ledger technology for securities settlement.Ledger, 4, 2019

Evangelos Benos, Rodney Garratt, and Pedro Gurrola-Perez. The economics of distributed ledger technology for securities settlement.Ledger, 4, 2019

2019

-

[7]

The cost of clearing fragmentation.Management Science, 70(6):3581–3596, 2024

Evangelos Benos, Wenqian Huang, Albert Menkveld, and Michalis Vasios. The cost of clearing fragmentation.Management Science, 70(6):3581–3596, 2024

2024

-

[8]

The macroeconomics of trade credit

Luigi Bocola and Gideon Bornstein. The macroeconomics of trade credit. Technical report, National Bureau of Economic Research, 2023. 27

2023

-

[9]

Trade credit, trade finance, and the covid-19 crisis.Trade Finance, and the COVID-19 Crisis (June 19, 2020), 2020

Fr´ ed´ eric Boissay, Nikhil Patel, and Hyun Song Shin. Trade credit, trade finance, and the covid-19 crisis.Trade Finance, and the COVID-19 Crisis (June 19, 2020), 2020

2020

-

[10]

Fostering markets for sme finance.OECD SME and Entrepreneurship Papers, 2017

Kris Boschmans and Lora Pissareva. Fostering markets for sme finance.OECD SME and Entrepreneurship Papers, 2017

2017

-

[11]

Cycles protocol: A peer-to-peer electronic clearing system.arXiv preprint arXiv:2507.22309, 2025

Ethan Buchman, Paolo Dini, Shoaib Ahmed, Andrew Miller, and Tomaˇ z Fleischman. Cycles protocol: A peer-to-peer electronic clearing system.arXiv preprint arXiv:2507.22309, 2025

-

[12]

Mercado de facturas en la bolsa de productos de chile

Juan Manuel Carmona Torres, Diego Galleguillos Sandoval, and Diego Mart´ ınez Aracena. Mercado de facturas en la bolsa de productos de chile. Technical report, Universidad de Chile, 2010

2010

-

[13]

Money and hierarchy: Four ways to discharge a payment obligation.Available at SSRN 4032398, 2022

Borja Clavero. Money and hierarchy: Four ways to discharge a payment obligation.Available at SSRN 4032398, 2022

2022

-

[14]

Cmf issues regulations that simplify the registration of invoices for trading on commodity exchanges

Comisi´ on para el Mercado Financiero (CMF Chile). Cmf issues regulations that simplify the registration of invoices for trading on commodity exchanges. Press release / website, January

-

[15]

429 (January 7, 2019; accessed September 29, 2025)

General Regulation No. 429 (January 7, 2019; accessed September 29, 2025). Available at:https://www.cmfchile.cl/portal/principal/613/w3-article-26959.html

2019

-

[16]

Compressing over-the-counter markets.Operations Research, 69(6):1660–1679, 2021

Marco D’Errico and Tarik Roukny. Compressing over-the-counter markets.Operations Research, 69(6):1660–1679, 2021

2021

-

[17]

Neutral settlement layer for interoperability between different forms of local monetary and financial expression.International Journal of Community Currency Research, 29, 2025

Paolo Dini and Tomaˇ z Fleischman. Neutral settlement layer for interoperability between different forms of local monetary and financial expression.International Journal of Community Currency Research, 29, 2025

2025

-

[18]

Does a central clearing counterparty reduce counterparty risk?The Review of Asset Pricing Studies, 1(1):74–95, 2011

Darrell Duffie and Haoxiang Zhu. Does a central clearing counterparty reduce counterparty risk?The Review of Asset Pricing Studies, 1(1):74–95, 2011

2011

-

[19]

Peter G Fennell, David O’Sullivan, Antoine Godin, and Stephen Kinsella. Visualising stock flow consistent models as directed acyclic graphs.arXiv preprint arXiv:1409.4541, 2014

-

[20]

Mathematical foundations for balancing the payment system in the trade credit market.Journal of Risk and Financial Management, 14(9):452, 2021

Tomaˇ z Fleischman and Paolo Dini. Mathematical foundations for balancing the payment system in the trade credit market.Journal of Risk and Financial Management, 14(9):452, 2021

2021

-

[21]

Liquidity-saving through obligation- clearing and mutual credit: An effective monetary innovation for SMEs in times of crisis

Tomaˇ z Fleischman, Paolo Dini, and Giuseppe Littera. Liquidity-saving through obligation- clearing and mutual credit: An effective monetary innovation for SMEs in times of crisis. Journal of Risk and Financial Management, 13(12):295, 2020

2020

-

[22]

The economics of netting in financial networks.Journal of Economic Interaction and Coordination, 14(3):595–622, 2019

Edoardo Gaffeo, Lucio Gobbi, and Massimo Molinari. The economics of netting in financial networks.Journal of Economic Interaction and Coordination, 14(3):595–622, 2019

2019

-

[23]

Liquidity-saving mechanisms and bank behaviour

Marco Galbiati and Kimmo Soram¨ aki. Liquidity-saving mechanisms and bank behaviour. Technical Report Working Paper No. 400, Bank of England Working Papers, 2010

2010

-

[24]

Central counterparty interoperability.RBA Bulletin, June, pages 59–68, 2012

Nicholas Garvin. Central counterparty interoperability.RBA Bulletin, June, pages 59–68, 2012

2012

-

[25]

Variation margin settlement whitepaper

International Swaps and Derivatives Association (ISDA). Variation margin settlement whitepaper. Whitepaper / website, January 2017. Accessed March 12, 2026. Available at: https://www.isda.org/a/sgiDE/isda-vm-settlement-whitepaper-final.pdf. 28

2017

-

[26]

Trade creditors’ information advantage

Victoria Ivashina and Benjamin Iverson. Trade creditors’ information advantage. Technical report, National Bureau of Economic Research, 2018

2018

-

[27]

Liquidity-saving mechanisms in collateral-based rtgs payment systems

Marius Jurgilas and Antoine Martin. Liquidity-saving mechanisms in collateral-based rtgs payment systems. Technical Report Working Paper No. 389, Bank of England / Federal Reserve Bank of New York, 2010

2010

-

[28]

King, Travis D

Thomas B. King, Travis D. Nesmith, Anna Paulson, and Todd Prono. Central clearing and systemic liquidity risk.International Journal of Central Banking, 19(4):85–142, 2023

2023

-

[29]

The evolution of trade credit: New evidence from developed versus developing countries.Review of Quantitative Finance and Accounting, 59(3):857–912, 2022

Michael Machokoto, Daniel Gyimah, and Boulis Maher Ibrahim. The evolution of trade credit: New evidence from developed versus developing countries.Review of Quantitative Finance and Accounting, 59(3):857–912, 2022

2022

-

[30]

Central counterparty anti-procyclicality tools: a closer assessment.Journal of Financial Market Infrastructures, 7(4):1–25, 2019

Atsushi Maruyama and Fernando Cerezetti. Central counterparty anti-procyclicality tools: a closer assessment.Journal of Financial Market Infrastructures, 7(4):1–25, 2019

2019

-

[31]

Federal Reserve Bank of Chicago, 1994

Dorothy M Nichols.Modern money mechanics. Federal Reserve Bank of Chicago, 1994. Originally published 1961

1994

-

[32]

Decentralised clearing? an assessment of the impact of dlts on ccps.Journal of Securities Operations & Custody, 16(3):227–246, 2024

Rafael Plata, Max Chan, and Fernando Cerezetti. Decentralised clearing? an assessment of the impact of dlts on ccps.Journal of Securities Operations & Custody, 16(3):227–246, 2024

2024

-

[33]

Central clearing: Risks and customer protections.Economic Perspectives, 39(4):1–11, 2015

Ivana Ruffini et al. Central clearing: Risks and customer protections.Economic Perspectives, 39(4):1–11, 2015

2015

-

[34]

Deleveraging of indebtedness in an economy through non-monetary intervention, 2018

Tomaˇ z Schara and Rudi Bric. Deleveraging of indebtedness in an economy through non-monetary intervention, 2018. Working paper / report

2018

-

[35]

Trade credit and stock liquidity.Journal of Corporate Finance, 62:101586, 2020

Chenguang Shang. Trade credit and stock liquidity.Journal of Corporate Finance, 62:101586, 2020

2020

-

[36]

Systemic risk in markets with multiple central counterparties.Mathematical Finance, 35(1):214–262, 2025

Luitgard Anna Maria Veraart and I˜ naki Aldasoro. Systemic risk in markets with multiple central counterparties.Mathematical Finance, 35(1):214–262, 2025

2025

-

[37]

Central counterparties: Addressing their too important to fail nature

Froukelien Wendt. Central counterparties: Addressing their too important to fail nature. IMF Working Paper WP/15/21, International Monetary Fund, 2015

2015

-

[38]

race to the bottom

Siyi Zhu et al. Is there a “race to the bottom” in central counterparties competition? Technical report, Netherlands Central Bank, Research Department, 2011. 29

2011

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.