Recognition: unknown

Pareto frontier of portfolio investment under volatility uncertainty and short-sale constraints market

Pith reviewed 2026-05-08 01:34 UTC · model grok-4.3

The pith

A single risk factor w produces an analytical polynomial expression for the Pareto frontier in the SLE-MUV portfolio model under volatility uncertainty.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

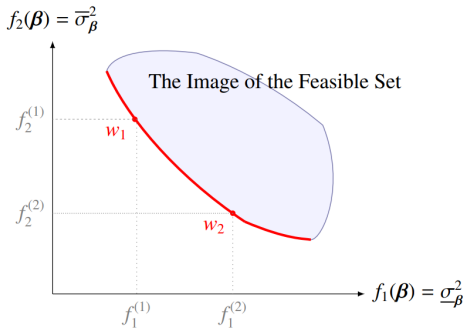

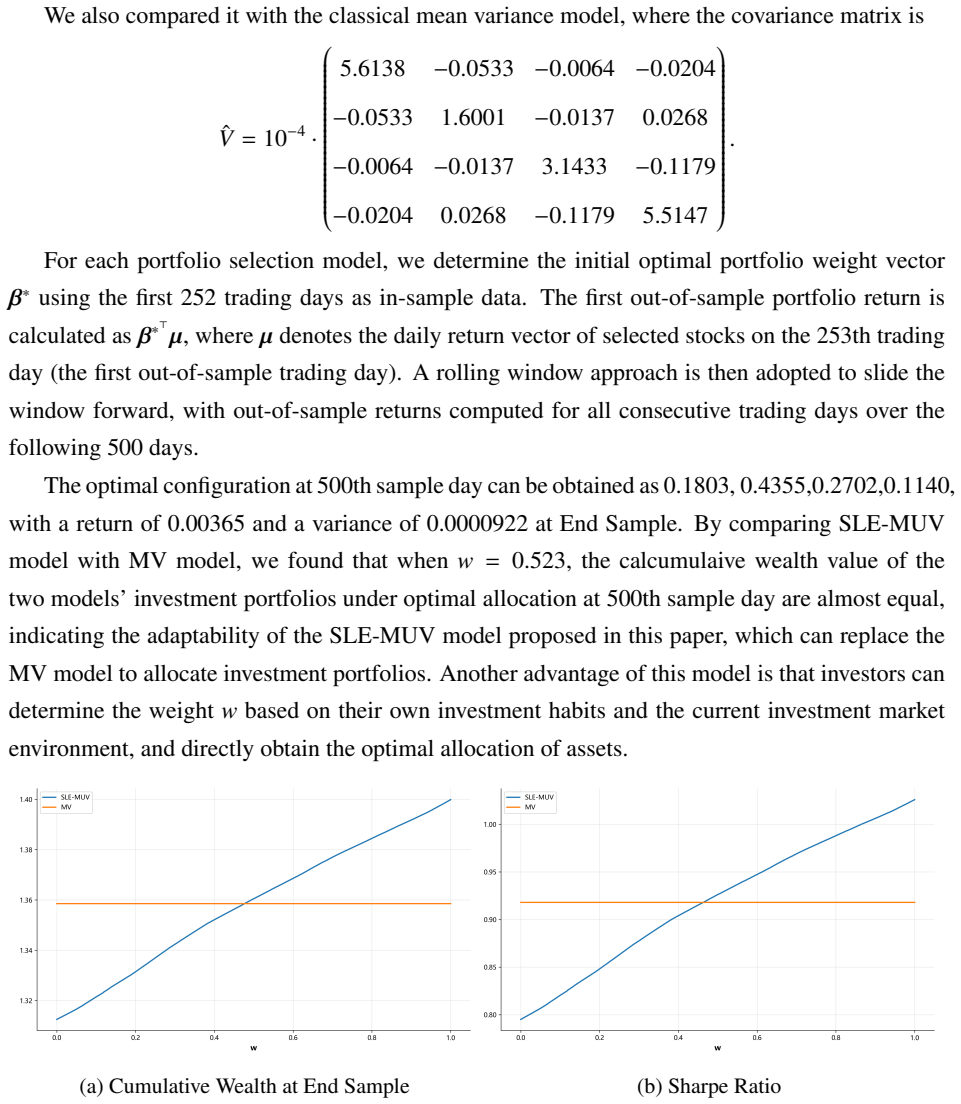

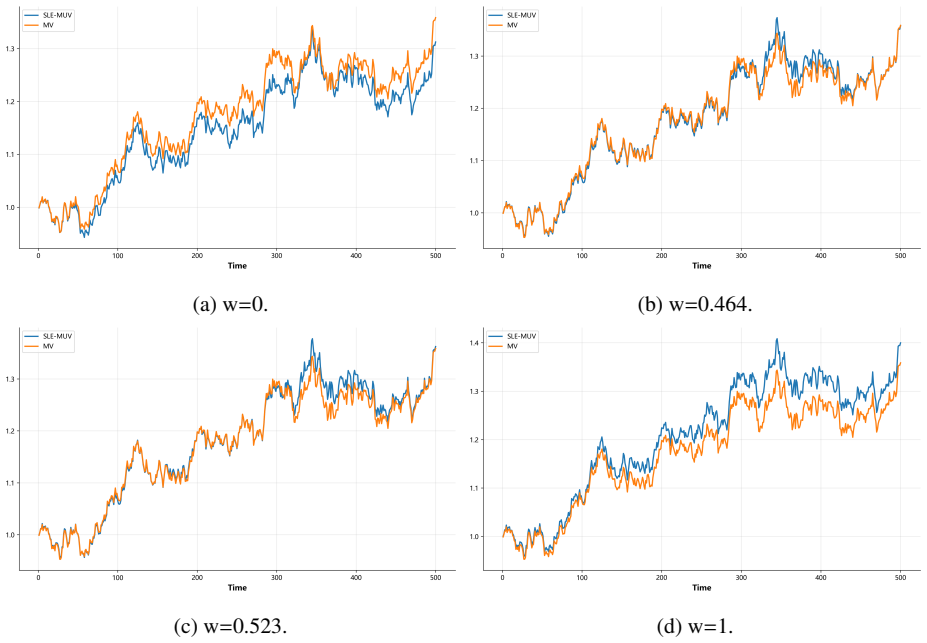

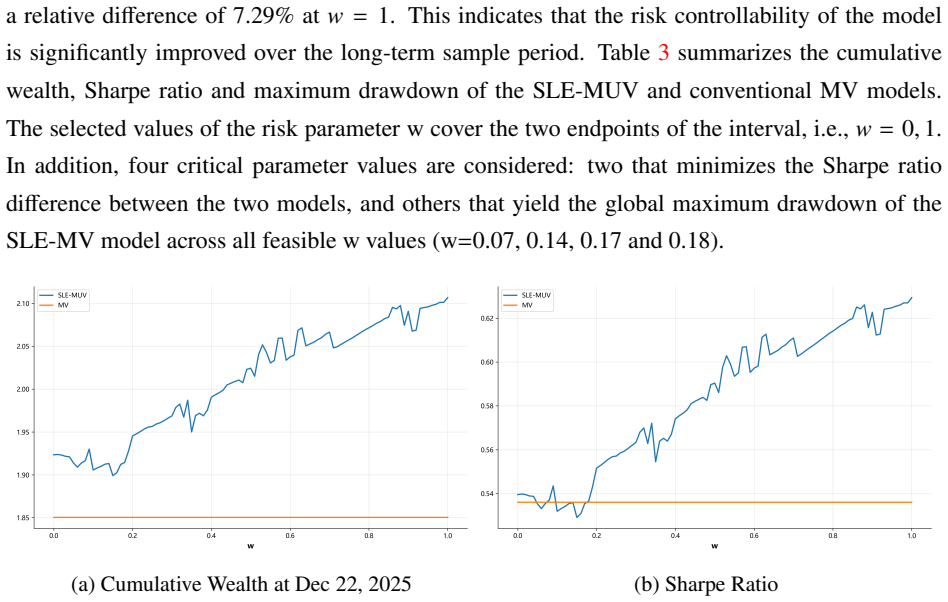

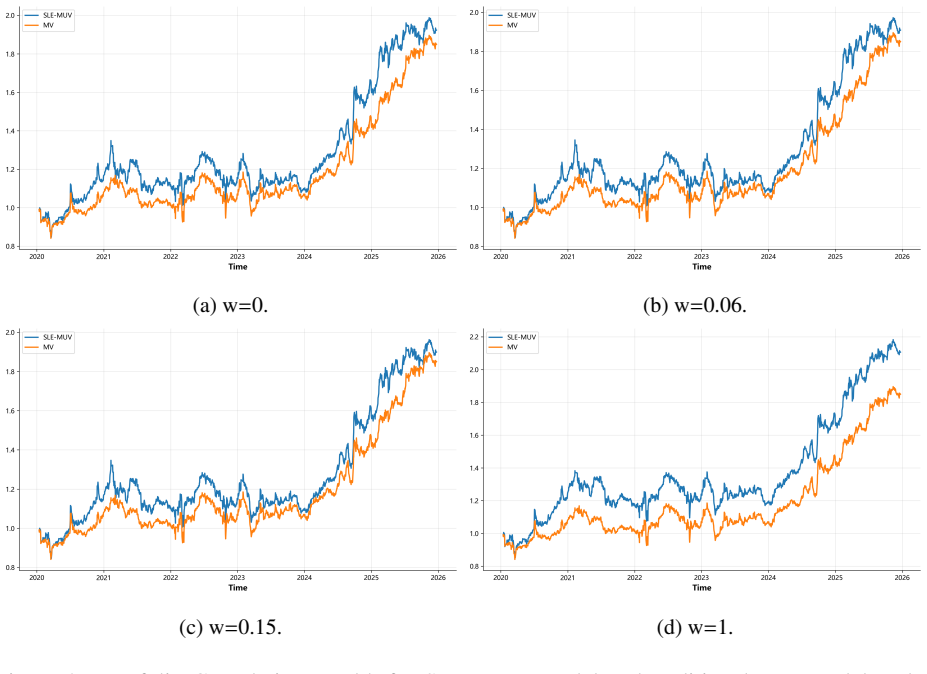

The Pareto frontier of the SLE-MUV model is a continuous convex curve, and its optimal solution can be expressed as a polynomial analytical expression with respect to the risk factor w. The model is tested empirically on simulated data, US stock market data, and A-share market data, where it significantly improves the risk-adjusted return of the investment portfolio compared to the traditional Mean-Variance model.

What carries the argument

The SLE-MUV model, which uses a risk factor w to couple the maximum and minimum variances arising from volatility uncertainty under sublinear expectations.

Load-bearing premise

That sublinear expectations accurately represent volatility uncertainty and that a single risk factor w suffices to couple maximum and minimum risks without creating inconsistencies in the optimal portfolios.

What would settle it

Finding a value of w where the polynomial-derived weights do not solve the underlying optimization problem, or showing that out-of-sample portfolios from the model have risk-adjusted performance no better than or worse than mean-variance portfolios.

Figures

read the original abstract

In this paper, we investigate a portfolio investment problem under volatility uncertainty and short-sale constraints market via sublinear expectation which is used to model volatility uncertainty. We assume the stocks admit volatility uncertainty. Thus the related portfolio has upper variance (maximum risk) and lower variance (minimum risk). By introducing a risk factor $w$ to conduct coupled modeling of the maximum and minimum risks, a simplified Sublinear Expectation Mean-Uncertainty Variance (SLE-MUV) model is constructed. Theoretically, we show that the Pareto frontier of the SLE-MUV model is a continuous convex curve, and its optimal solution can be expressed as a polynomial analytical expression with respect to the risk factor $w$. Empirically, we systematically test the practical performance of the SLE-MUV model and conduct comparative analysis with the traditional Mean-Variance (MV) model as the benchmark based on three sets of samples -- simulated generated data, data of the US stock market and the A-share market. The empirical results show that the SLE-MUV model can significantly improving the risk-adjusted return of the investment portfolio.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes the SLE-MUV model for portfolio optimization under volatility uncertainty using sublinear expectations, incorporating short-sale constraints. A risk factor w is introduced to couple the maximum and minimum variances, leading to the claim that the Pareto frontier is a continuous convex curve and that the optimal weights are given by a polynomial expression in w. The paper also presents empirical comparisons with the mean-variance model on simulated and real stock data, asserting improved risk-adjusted returns.

Significance. If the central theoretical claim is rigorously established, the work offers an analytical solution to a mean-uncertainty-variance optimization problem, which could be significant for robust portfolio management in uncertain volatility environments. The convexity of the frontier and closed-form solution would be valuable contributions to mathematical finance. The empirical tests, if they include proper statistical validation, could support practical applicability. However, the introduction of the free parameter w requires careful justification for the results to be fully convincing.

major comments (3)

- [Abstract] Abstract: The claim that 'its optimal solution can be expressed as a polynomial analytical expression with respect to the risk factor w' is difficult to reconcile with the short-sale constraints, which impose non-negativity inequalities on the weights. Standard optimization theory (KKT conditions with complementary slackness) suggests that the solution would be piecewise, depending on which constraints are binding for different ranges of w, rather than a single polynomial for all w. This needs to be addressed with explicit case analysis or a proof that the expression remains polynomial across the domain.

- [Theoretical section] Theoretical development: The abstract states that the Pareto frontier is a continuous convex curve and the solution is polynomial in w, yet provides no derivation steps, proof outline, or verification that the polynomial satisfies the original constrained problem. The role of w in coupling max and min variances must be shown to preserve convexity without introducing kinks at active-set boundaries.

- [Empirical section] Empirical analysis: Superiority over the MV benchmark is asserted without reported metrics (e.g., Sharpe ratios, specific risk-adjusted returns), confidence intervals, or details on how w is selected or fitted in the tests on simulated, US, and A-share data. This prevents evaluation of whether the claimed improvements are statistically significant or robust.

minor comments (1)

- [Model setup] The notation for upper and lower variances under sublinear expectation could be introduced more explicitly before the model formulation to aid readability.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on our manuscript. We address each major comment below and indicate the revisions we will make to strengthen the presentation of the SLE-MUV model.

read point-by-point responses

-

Referee: [Abstract] Abstract: The claim that 'its optimal solution can be expressed as a polynomial analytical expression with respect to the risk factor w' is difficult to reconcile with the short-sale constraints, which impose non-negativity inequalities on the weights. Standard optimization theory (KKT conditions with complementary slackness) suggests that the solution would be piecewise, depending on which constraints are binding for different ranges of w, rather than a single polynomial for all w. This needs to be addressed with explicit case analysis or a proof that the expression remains polynomial across the domain.

Authors: We acknowledge that short-sale constraints generally produce piecewise solutions via KKT conditions. In our derivation, the coupled modeling via the risk factor w yields an explicit polynomial form for the optimal weights that satisfies the non-negativity constraints over the relevant domain of w. To make this fully rigorous, we will add an explicit case analysis in the revised theoretical section, verifying that the polynomial expression remains valid without requiring separate cases for active constraints, and confirm it meets the KKT conditions for the constrained problem. revision: yes

-

Referee: [Theoretical section] Theoretical development: The abstract states that the Pareto frontier is a continuous convex curve and the solution is polynomial in w, yet provides no derivation steps, proof outline, or verification that the polynomial satisfies the original constrained problem. The role of w in coupling max and min variances must be shown to preserve convexity without introducing kinks at active-set boundaries.

Authors: We agree that additional derivation details are needed. In the revised manuscript we will insert a step-by-step proof outline: first showing how w couples the maximum and minimum variances under sublinear expectation, then proving that the resulting objective produces a continuous convex Pareto frontier, and finally verifying that the polynomial solution satisfies the original constrained optimization problem without introducing kinks at constraint boundaries. revision: yes

-

Referee: [Empirical section] Empirical analysis: Superiority over the MV benchmark is asserted without reported metrics (e.g., Sharpe ratios, specific risk-adjusted returns), confidence intervals, or details on how w is selected or fitted in the tests on simulated, US, and A-share data. This prevents evaluation of whether the claimed improvements are statistically significant or robust.

Authors: We recognize that quantitative metrics and selection details are essential for evaluating the empirical claims. In the revision we will report specific risk-adjusted performance measures (including Sharpe ratios), confidence intervals for the improvements, and a clear description of how the risk factor w is chosen or fitted for each dataset. These additions will allow readers to assess statistical significance and robustness of the SLE-MUV results relative to the MV benchmark. revision: yes

Circularity Check

No significant circularity; derivation proceeds from model definition to closed-form solution

full rationale

The SLE-MUV model is explicitly constructed by introducing the tunable risk factor w to couple maximum and minimum variances under sublinear expectations. The subsequent theoretical result—that the Pareto frontier is a continuous convex curve and that optimal weights admit a polynomial expression in w—is obtained by analytically solving the resulting constrained quadratic program for varying w. This is a direct derivation from the stated objective and constraints rather than a re-labeling or self-referential fit. Short-sale constraints are acknowledged in the model but do not alter the non-circular character of the algebraic solution step. No self-citation chains, ansatz smuggling, or renaming of known results are required for the central claim. The empirical section compares the model against MV benchmarks on external data and is independent of the theoretical derivation.

Axiom & Free-Parameter Ledger

free parameters (1)

- risk factor w

axioms (1)

- domain assumption Sublinear expectation properties suffice to represent volatility uncertainty for all stocks

Reference graph

Works this paper leans on

-

[1]

Probability, Uncertainty & Quantitative Risk , volume=

Linear regression under model uncertainty , author=. Probability, Uncertainty & Quantitative Risk , volume=

-

[2]

Available at SSRN 5225465 , year=

Conditional Value-at-Risk Under Reward-Penalty Mechanism with Applications to Robust Portfolio Management , author=. Available at SSRN 5225465 , year=

-

[3]

A Worst-Case Risk Measure by

Pei, Ziting and Wang, Xishun and Yue, Xingye , year =. A Worst-Case Risk Measure by. Acta Mathematicae Applicatae Sinica, English Series , doi =

-

[4]

The Journal of Finance , volume=

Portfolio selection , author=. The Journal of Finance , volume=

-

[5]

Peng , journal=

S. Peng , journal=. Nonlinear expectations and stochastic calculus under uncertainty with robust

-

[6]

2015 , note =

Li He and Qinghuai Liu , title =. 2015 , note =

2015

-

[7]

Journal of Financial Econometrics , year=

Improving Value-at-Risk prediction under model uncertainty , author=. Journal of Financial Econometrics , year=

-

[8]

Pei, Z. T. and Yue, X. Y. and Zheng, X. T. , journal=. Numerical methods for two-dimensional

-

[9]

White , keywords =

D.J. White , keywords =. Epsilon-dominating solutions in mean-variance portfolio analysis , journal =. 1998 , issn =

1998

-

[10]

Fuzzy Optimization and Decision Making , volume=

Portfolio selection problems with Markowitz’s mean--variance framework: a review of literature , author=. Fuzzy Optimization and Decision Making , volume=. 2018 , publisher=

2018

-

[11]

Journal of business , volume=

The variation of certain speculative prices , author=. Journal of business , volume=. 1963 , publisher=

1963

-

[12]

2007 , organization=

Peng, Shige , booktitle=. 2007 , organization=

2007

-

[13]

Distributional uncertainty of the financial time series measured by

Peng, Shige and Yang, Shuzhen , journal=. Distributional uncertainty of the financial time series measured by. 2022 , publisher=

2022

-

[14]

Journal of Machine Learning Research , year =

Steven Diamond and Stephen Boyd , title =. Journal of Machine Learning Research , year =

-

[15]

Nature Methods , year =

Virtanen, Pauli and Gommers, et.al , title =. Nature Methods , year =

-

[16]

Worst-case values of target semi-variances with applications to robust portfolio selection , journal =

Jun Cai and Zhanyi Jiao and Tiantian Mao , keywords =. Worst-case values of target semi-variances with applications to robust portfolio selection , journal =. 2025 , issn =

2025

-

[17]

Worst-case risk measures of stop-loss and limited loss random variables under distribution uncertainty with applications to robust reinsurance , journal =

Jun Cai and Fangda Liu and Mingren Yin , keywords =. Worst-case risk measures of stop-loss and limited loss random variables under distribution uncertainty with applications to robust reinsurance , journal =. 2024 , issn =

2024

-

[18]

Distributionally robust optimal allocation of financial assets under the uncertainty and irrationality , journal =

Jianping Li and Jiaxin Yuan and Jun Hao , keywords =. Distributionally robust optimal allocation of financial assets under the uncertainty and irrationality , journal =. 2026 , issn =

2026

-

[19]

Jones and Helenice O

Dylan F. Jones and Helenice O. Florentino , title=. The Palgrave Handbook of Operations Research , chapter=. 2022 , month=

2022

-

[20]

Decision sciences , pages=

Multi-objective optimization , author=. Decision sciences , pages=. 2016 , publisher=

2016

-

[21]

Fifty years of portfolio optimization , journal =

Ahti Salo and Michalis Doumpos and Juuso Liesiö and Constantin Zopounidis , keywords =. Fifty years of portfolio optimization , journal =. 2024 , issn =

2024

-

[22]

The Review of Economic Studies , volume=

Mean-variance analysis in the theory of liquidity preference and portfolio selection , author=. The Review of Economic Studies , volume=. 1969 , publisher=

1969

-

[23]

The Review of Economic Studies , volume=

A note on uncertainty and indifference curves , author=. The Review of Economic Studies , volume=. 1969 , publisher=

1969

-

[24]

The Review of Economic Studies , volume=

The fundamental approximation theorem of portfolio analysis in terms of means, variances and higher moments , author=. The Review of Economic Studies , volume=. 1970 , publisher=

1970

-

[25]

Journal of Financial and Quantitative Analysis , volume=

General proof that diversification pays , author=. Journal of Financial and Quantitative Analysis , volume=. 1967 , publisher=

1967

-

[26]

International Journal of Systems Science , volume=

Mean-variance-skewness model for portfolio selection with transaction costs , author=. International Journal of Systems Science , volume=. 2003 , publisher=

2003

-

[27]

Computers & Operations Research , volume=

Neural network-based mean--variance--skewness model for portfolio selection , author=. Computers & Operations Research , volume=. 2008 , publisher=

2008

-

[28]

European Journal of Operational Research , volume=

Mean-variance-skewness model for portfolio selection with fuzzy returns , author=. European Journal of Operational Research , volume=. 2010 , publisher=

2010

-

[29]

Optimization , volume=

Uncertain random mean--variance--skewness models for the portfolio optimization problem , author=. Optimization , volume=. 2022 , publisher=

2022

-

[30]

Soft computing , volume=

Uncertain random variables: A mixture of uncertainty and randomness , author=. Soft computing , volume=. 2013 , publisher=

2013

-

[31]

European Journal of Operational Research , volume=

Mean-variance model for portfolio optimization problem in the simultaneous presence of random and uncertain returns , author=. European Journal of Operational Research , volume=. 2015 , publisher=

2015

-

[32]

Statistics, Optimization & Information Computing , volume=

Uncertain Portfolio Optimization Problems: Systematic Review , author=. Statistics, Optimization & Information Computing , volume=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.