Recognition: unknown

Fiscal Aggregation and the Limits of IS--LM--BP: Derivations, Aggregation Bias and Reproducible Adversarial Simulations

Pith reviewed 2026-05-07 12:30 UTC · model grok-4.3

The pith

The aggregate fiscal variable G suffices for output analysis only if every instrument has the identical marginal effect on output.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

When fiscal policy consists of heterogeneous instruments, the scalar aggregate G is sufficient for output analysis only under the restrictive gradient condition that all instruments exert identical marginal effects on output; otherwise, composition-weighted multipliers must replace the single variable, and the IS-LM-BP model must incorporate fiscal composition, public capital, debt dynamics, and risk-premium effects. The paper proves the condition, identifies the resulting aggregation bias, and verifies the extended framework through reproducible symbolic checks, derivative tests, accounting identities, adversarial counterexamples, sensitivity sweeps, Monte Carlo simulations, and stress test

What carries the argument

the gradient condition requiring identical marginal output effects across all fiscal instruments, which determines when scalar aggregation is valid and when vector-valued, state-contingent multipliers are required instead

If this is right

- Fiscal policy analysis must treat instruments as a vector rather than a scalar sum.

- Multipliers become state-contingent and depend on the specific mix of purchases, investment, and transfers.

- Standard IS-LM-BP forecasts that ignore composition will contain systematic bias.

- Policy rules and empirical estimates require explicit tracking of fiscal composition and debt feedback.

- The extended model preserves the compact equilibrium representation while adding the necessary detail.

Where Pith is reading between the lines

- Empirical studies that rely on aggregate spending data may systematically mis-estimate multipliers whenever the instrument mix changes across episodes.

- Optimal stimulus design should target the composition of spending rather than its total size to achieve a given output goal at lower cost.

- The same aggregation logic could be applied to other macro models that currently collapse government spending into a single variable.

- Reproducible adversarial testing of this kind could be used to audit other compact representations in open-economy macroeconomics.

Load-bearing premise

That the marginal effects of heterogeneous fiscal instruments can be separately identified within an extended IS-LM-BP equilibrium that still remains useful once composition, public capital, debt, and risk-premium terms are added.

What would settle it

A simulation or empirical case in which fiscal instruments with measurably different marginal effects on output nevertheless produce the same aggregate output response as predicted by scalar G alone, with no detectable composition bias.

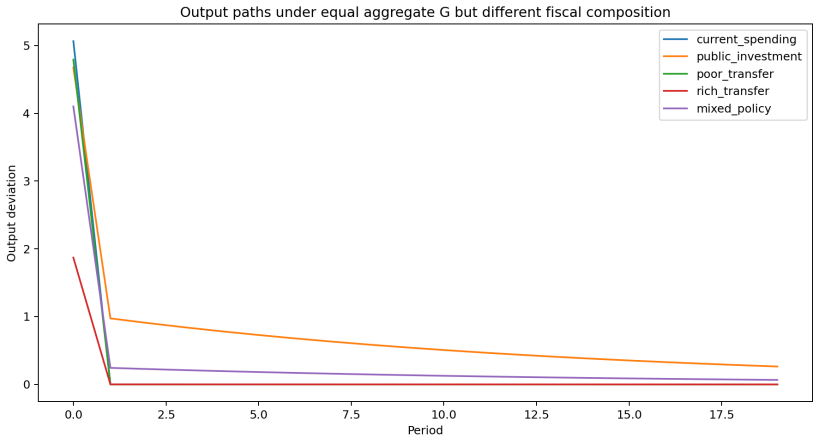

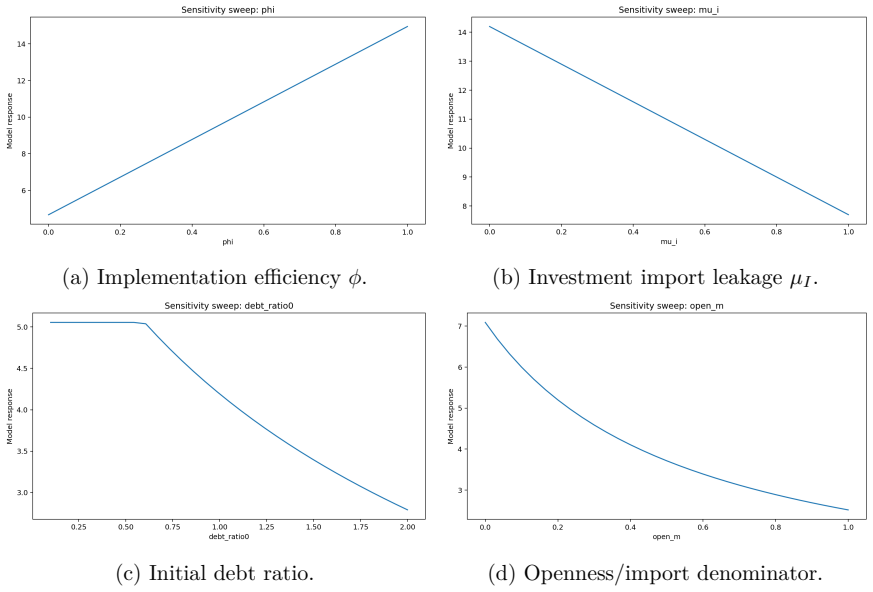

Figures

read the original abstract

This paper develops a formal critique of scalar fiscal aggregation in the IS LM BP/Mundell Fleming framework. It shows that when fiscal policy is composed of heterogeneous instruments current purchases, public investment and transfers to different households the aggregate variable G is sufficient for output analysis only under a restrictive gradient condition: all instruments must have identical marginal effects on output. The paper proves this condition, derives composition weighted multipliers, identifies aggregation bias and extends the open economy IS LM BP model to incorporate fiscal composition, public capital, debt dynamics and risk-premium effects. A reproducible computational exercise with symbolic checks, derivative tests, accounting identities, adversarial counterexamples, sensitivity sweeps, Monte Carlo simulations and stress tests confirms the internal consistency of the argument. The contribution is methodological: IS LM BP remains useful as a compact equilibrium framework, but fiscal policy analysis requires vector-valued instruments and state-contingent multipliers rather than a single homogeneous spending variable.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that scalar fiscal aggregation into a single G variable in the IS-LM-BP (Mundell-Fleming) framework is valid for output determination only under a restrictive gradient condition requiring identical marginal effects across heterogeneous instruments (current purchases, public investment, transfers). It proves this condition, derives composition-weighted multipliers, identifies resulting aggregation bias, extends the model to incorporate public capital accumulation, debt dynamics, and endogenous risk premia while preserving equilibrium solution methods, and verifies internal consistency via symbolic checks, derivative tests, accounting identities, adversarial counterexamples, sensitivity sweeps, Monte Carlo simulations, and stress tests.

Significance. If the derivations and simulations hold, the work offers a clear methodological contribution by showing that IS-LM-BP remains a compact equilibrium framework but requires vector-valued fiscal instruments and state-contingent multipliers rather than homogeneous G. The reproducible adversarial simulations and Monte Carlo exercises, including explicit tests of gradient-condition violations, provide falsifiable verification that strengthens the central claim about aggregation bias.

minor comments (3)

- [Abstract and computational exercise] The abstract and simulation sections reference 'symbolic checks' and 'reproducible computational exercise' but do not name the specific software, libraries, or code repository used, which would aid full reproducibility.

- [Simulation and stress-test sections] Monte Carlo and adversarial simulation descriptions would benefit from explicit reporting of random seeds, exact parameter draws, and the precise functional forms used for heterogeneous marginal effects to allow direct replication of the bias results.

- [Model extension] Notation for the total derivative dY/dG and the gradient condition could be stated more explicitly when the model is extended with public capital and risk premia to avoid ambiguity in how composition weights enter the equilibrium.

Simulated Author's Rebuttal

We thank the referee for the positive and accurate summary of our manuscript, as well as for the recommendation of minor revision. The referee's assessment correctly captures our central methodological contribution on the restrictive conditions for scalar fiscal aggregation in the IS-LM-BP framework and the value of the reproducible verification exercises.

Circularity Check

Derivation self-contained; no circular steps

full rationale

The core claim—that scalar G suffices for output only when all fiscal instruments share identical marginal effects—is derived directly from the total derivative dY/dG being independent of composition in the extended IS-LM-BP equations. This follows from the model's accounting identities and equilibrium conditions without redefinition or fitting. Extensions for public capital, debt dynamics, and risk premia are added while preserving the solution method; adversarial Monte Carlo tests and symbolic checks confirm internal consistency but do not serve as load-bearing inputs. No self-citations are invoked for uniqueness theorems or ansatzes, and no parameter is fitted then relabeled as a prediction. The chain is mathematically independent of its own outputs.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Abiad, A., Furceri, D., and Topalova, P. (2016). The macroeconomic effects of public investment: Evidence from advanced economies.Journal of Macroeconomics, 50, 224– 240.https://doi.org/10.1016/j.jmacro.2016.07.005

-

[2]

Auclert, A., Bardóczy, B., Rognlie, M., and Straub, L. (2021). Using the sequence- space Jacobian to solve and estimate heterogeneous-agent models.Econometrica, 89(5), 2375–2408.https://doi.org/10.3982/ECTA17434

-

[3]

Auerbach, A. J. and Gorodnichenko, Y. (2012). Measuring the output responses to fiscal policy.American Economic Journal: Economic Policy, 4(2), 1–27.https://doi.org/ 10.1257/pol.4.2.1

-

[4]

Blanchard, O. J. and Leigh, D. (2013). Growth forecast errors and fiscal multipliers. American Economic Review, 103(3), 117–120.https://doi.org/10.1257/aer.103.3. 117

-

[5]

Blanchard, O. and Perotti, R. (2002). An empirical characterization of the dynamic effects of changes in government spending and taxes on output.The Quarterly Journal of Economics, 117(4), 1329–1368.https://doi.org/10.1162/003355302320935043 30

-

[6]

Bohn, H. (1998). The behavior of U.S. public debt and deficits.The Quarterly Journal of Economics, 113(3), 949–963.https://doi.org/10.1162/003355398555793

-

[7]

Bom, P. R. D. and Ligthart, J. E. (2014). What have we learned from three decades of research on the productivity of public capital?Journal of Economic Surveys, 28(5), 889–916.https://doi.org/10.1111/joes.12037

- [8]

-

[9]

Clarida, R., Galí, J., and Gertler, M. (1999). The science of monetary policy: A New Keynesian perspective.Journal of Economic Literature, 37(4), 1661–1707.https: //doi.org/10.1257/jel.37.4.1661

-

[10]

Dornbusch, R. (1976). Expectations and exchange rate dynamics.Journal of Political Economy, 84(6), 1161–1176.https://doi.org/10.1086/260506

-

[11]

Fleming, J. M. (1962). Domestic financial policies under fixed and under floating exchange rates.IMF Staff Papers, 9(3), 369–380.https://doi.org/10.2307/3866091

-

[12]

Gechert, S. (2015). What fiscal policy is most effective? A meta-regression analysis.Oxford Economic Papers, 67(3), 553–580.https://doi.org/10.1093/oep/gpv027

-

[13]

Gechert, S. and Rannenberg, A. (2018). Which fiscal multipliers are regime-dependent? A meta-regression analysis.Journal of Economic Surveys, 32(4), 1160–1182.https: //doi.org/10.1111/joes.12241

-

[14]

Mr. Keynes and the "Classics"; A Suggested Interpretation

Hicks, J. R. (1937). Mr. Keynes and the “Classics”: A suggested interpretation.Econo- metrica, 5(2), 147–159.https://doi.org/10.2307/1907242

-

[15]

Huidrom, R., Kose, M. A., Lim, J. J., and Ohnsorge, F. L. (2020). Why do fiscal multipliers depend on fiscal positions?Journal of Monetary Economics, 114, 109–125. https://doi.org/10.1016/j.jmoneco.2019.03.004

-

[16]

G., and Végh, C

Ilzetzki, E., Mendoza, E. G., and Végh, C. A. (2013). How big (small?) are fiscal multipliers?Journal of Monetary Economics, 60(2), 239–254.https://doi.org/10.1 016/j.jmoneco.2012.10.011

2013

-

[17]

Ilzetzki, E., Reinhart, C. M., and Rogoff, K. S. (2019). Exchange arrangements entering the twenty-first century: Which anchor will hold?The Quarterly Journal of Economics, 134(2), 599–646.https://doi.org/10.1093/qje/qjy033 31 International Monetary Fund. (2014). Is it time for an infrastructure push? The macroeco- nomic effects of public investment. InWo...

-

[18]

Clouds, Uncertainties, Chapter 3.https://www.imf.org/-/media/Websites/IMF/i mported-flagship-issues/external/pubs/ft/weo/2014/02/pdf/_c3pdf.pdf

2014

-

[19]

Kaplan, G. and Violante, G. L. (2014). A model of the consumption response to fiscal stimulus payments.Econometrica, 82(4), 1199–1239.https://doi.org/10.3982/ECTA 10528

-

[20]

Kaplan, G., Moll, B., and Violante, G. L. (2018). Monetary policy according to HANK. American Economic Review, 108(3), 697–743.https://doi.org/10.1257/aer.2016 0042

-

[21]

Kraay, A. (2012). How large is the government spending multiplier? Evidence from World Bank lending.The Quarterly Journal of Economics, 127(2), 829–887.https: //doi.org/10.1093/qje/qjs008

-

[22]

Kraay, A. (2014). Government spending multipliers in developing countries.American Economic Journal: Macroeconomics, 6(4), 170–208.https://doi.org/10.1257/mac. 6.4.170

work page doi:10.1257/mac 2014

-

[23]

Leeper, E. M., Walker, T. B., and Yang, S.-C. S. (2010). Government investment and fiscal stimulus.Journal of Monetary Economics, 57(8), 1000–1012.https://doi.org/ 10.1016/j.jmoneco.2010.09.002

-

[24]

Mountford, A. and Uhlig, H. (2009). What are the effects of fiscal policy shocks?Journal of Applied Econometrics, 24(6), 960–992.https://doi.org/10.1002/jae.1079

-

[25]

Mundell, R. A. (1963). Capital mobility and stabilization policy under fixed and flexible exchange rates.Canadian Journal of Economics and Political Science, 29(4), 475–485. https://doi.org/10.2307/139336

-

[26]

and Steinsson, J

Nakamura, E. and Steinsson, J. (2014). Fiscal stimulus in a monetary union: Evidence from US regions.American Economic Review, 104(3), 753–792.https://doi.org/10 .1257/aer.104.3.753

2014

-

[27]

Parker, J. A., Souleles, N. S., Johnson, D. S., and McClelland, R. (2013). Consumer spending and the economic stimulus payments of 2008.American Economic Review, 103(6), 2530–2553.https://doi.org/10.1257/aer.103.6.2530

-

[28]

Perotti, R. (2005). Estimating the effects of fiscal policy in OECD countries. CEPR Discussion Paper No. 4842.https://cepr.org/publications/dp4842 32

2005

-

[29]

Ramey, V. A. (2019). Ten years after the financial crisis: What have we learned from the renaissance in fiscal research?Journal of Economic Perspectives, 33(2), 89–114. https://doi.org/10.1257/jep.33.2.89

-

[30]

Ramey, V. A. and Zubairy, S. (2018). Government spending multipliers in good times and in bad: Evidence from U.S. historical data.Journal of Political Economy, 126(2), 850–901.https://doi.org/10.1086/696277

-

[31]

Reinhart, C. M. and Rogoff, K. S. (2004). The modern history of exchange rate ar- rangements: A reinterpretation.The Quarterly Journal of Economics, 119(1), 1–48. https://doi.org/10.1162/003355304772839515

-

[32]

Romer, D. H. (2000). Keynesian macroeconomics without the LM curve.Journal of Economic Perspectives, 14(2), 149–169.https://doi.org/10.1257/jep.14.2.149 33

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.