Recognition: unknown

MSE-Optimal Difference-in-Differences Estimator

Pith reviewed 2026-05-08 15:56 UTC · model grok-4.3

The pith

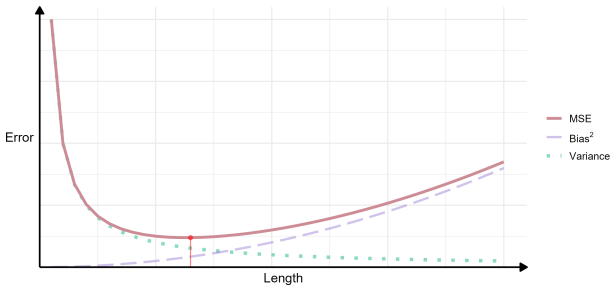

A difference-in-differences estimator chooses the pre-trend length that minimizes mean squared error.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

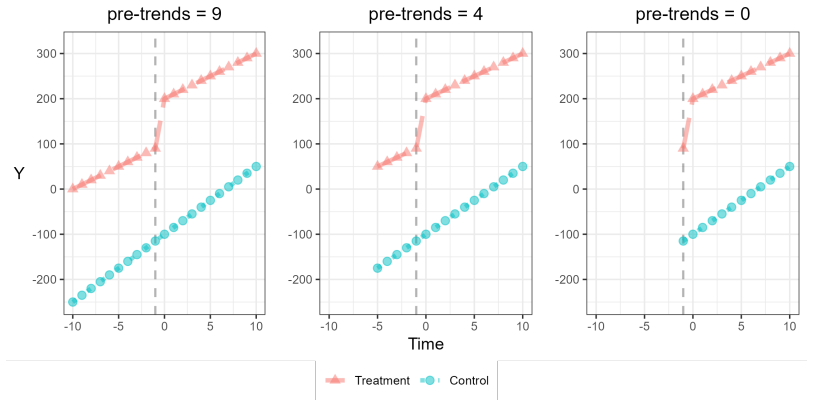

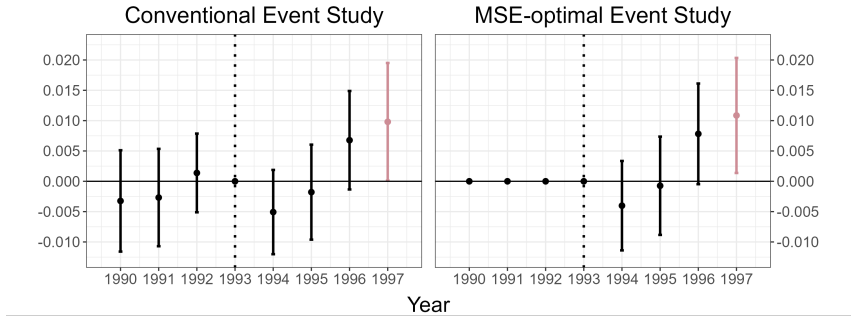

The paper develops a difference-in-differences estimation method that selects the optimal length of pre-trends by minimizing the mean squared error (MSE). By focusing on the bias and variance tradeoff, the proposed method derives the MSE-optimal estimator from the optimal length of pre-trends.

What carries the argument

MSE minimization over the choice of pre-trend length applied to conventional two-way fixed effects or event-study DiD specifications.

If this is right

- The estimator can achieve lower MSE than arbitrary fixed pre-trend choices when sample sizes are small.

- Pre-testing for parallel trends is replaced by direct optimization of estimation error.

- The same selection procedure applies to both two-way fixed effects and event-study models.

- Empirical applications can obtain more accurate treatment-effect estimates by using the data-driven pre-trend length.

Where Pith is reading between the lines

- The method could reduce arbitrary researcher choices in DiD design across many applied settings.

- Extensions might adapt the MSE criterion to other causal estimators that face similar window-length decisions.

- Further checks could test performance when pre-trends follow patterns not well captured by linear or fixed-length assumptions.

- Policy evaluations with limited data might gain more reliable small-sample results from this selection rule.

Load-bearing premise

That the MSE can be reliably minimized from the observed data without introducing new selection bias or requiring extra assumptions about the shape of pre-trends.

What would settle it

Repeated simulations with known true treatment effects in which the proposed estimator produces higher MSE than a fixed pre-trend length choice would falsify the optimality claim.

Figures

read the original abstract

This paper develops a difference-in-differences (DiD) estimation method that selects the optimal length of pre-trends by minimizing the mean squared error (MSE). Conventional DiD regression models, such as the two-way fixed effects model or the event study model, may suffer from accuracy and validity concerns. If the sample size is small, the estimator may have a larger variance. Also, pre-tests often lack power to detect violations of the parallel trends assumption as Roth (2022) highlights. By focusing on the bias and variance tradeoff, the proposed method derives the MSE-optimal estimator from the optimal length of pre-trends. Simulation results and an empirical application demonstrate the practical applicability of the proposed method.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. This paper proposes a difference-in-differences estimator that selects the optimal length of pre-trends by minimizing the mean squared error, explicitly balancing bias from possible parallel-trends violations against variance reduction. It contrasts the approach with conventional two-way fixed-effects and event-study specifications, and supports the proposal with simulation evidence and an empirical application.

Significance. If the derivation is valid, the method supplies a principled, data-driven rule for choosing pre-period length in DiD designs, which could improve finite-sample accuracy relative to arbitrary fixed lengths or low-powered pre-tests. The explicit bias-variance framing is a clear strength when the MSE objective can be minimized without introducing additional selection bias.

major comments (2)

- [Methodology section] The central derivation of the MSE-optimal pre-trend length (presumably in the methodology section) must demonstrate that the data-driven minimization of the MSE does not itself induce post-selection bias or circularity in the bias term; the reader's weakest assumption highlights that this step is load-bearing for the optimality claim.

- [Simulations] Simulation results (Section 4 or equivalent) report MSE improvements, but the design should include explicit comparisons against standard DiD estimators that use fixed pre-trend lengths chosen ex ante, to isolate whether the data-driven selection delivers gains beyond what a correctly specified fixed-length estimator would achieve.

minor comments (2)

- Notation for the pre-trend length parameter should be standardized and distinguished from event-study lag indices to prevent reader confusion.

- [Abstract] The abstract could state more precisely the set of candidate lengths over which the MSE is minimized and whether the minimization is performed in-sample or via cross-validation.

Simulated Author's Rebuttal

We thank the referee for the constructive comments and the opportunity to clarify and strengthen our manuscript. We address each major comment below.

read point-by-point responses

-

Referee: [Methodology section] The central derivation of the MSE-optimal pre-trend length (presumably in the methodology section) must demonstrate that the data-driven minimization of the MSE does not itself induce post-selection bias or circularity in the bias term; the reader's weakest assumption highlights that this step is load-bearing for the optimality claim.

Authors: We thank the referee for this important observation. In our derivation, the MSE is expressed as an explicit function of the pre-trend length k: bias squared (arising from any linear deviation from parallel trends over the pre-period) plus variance (which declines with larger k under standard DiD assumptions). The optimal k minimizes this expression, and the estimator itself is the conventional DiD estimator computed with the selected k. The bias term used for selection is obtained from the observed pre-period trends and does not depend on the post-period outcome or the final estimator, avoiding direct circularity. Nevertheless, because selection is data-driven, we acknowledge that a formal argument ruling out post-selection bias is valuable. We will add a dedicated subsection (or appendix) that derives the asymptotic properties of the selected estimator and shows that the selection step does not introduce additional bias beyond the intended bias-variance tradeoff under the paper's maintained assumptions. revision: yes

-

Referee: [Simulations] Simulation results (Section 4 or equivalent) report MSE improvements, but the design should include explicit comparisons against standard DiD estimators that use fixed pre-trend lengths chosen ex ante, to isolate whether the data-driven selection delivers gains beyond what a correctly specified fixed-length estimator would achieve.

Authors: We agree that direct comparisons to fixed-length estimators chosen ex ante would better isolate the value of the data-driven rule. Our existing simulations compare the MSE-optimal estimator to conventional two-way fixed-effects and event-study specifications (which implicitly use all available pre-periods). We will revise Section 4 to add explicit benchmarks that fix the pre-trend length ex ante at several reasonable values (e.g., half the available pre-periods, or other commonly used fractions). In addition, where the simulation design permits, we will include an oracle benchmark that uses the true MSE-minimizing length known from the DGP. These additions will clarify whether the data-driven selection improves upon well-specified fixed alternatives. revision: yes

Circularity Check

No significant circularity in MSE-optimal pre-trend length selection

full rationale

The paper proposes selecting pre-trend length to minimize estimated MSE as an explicit bias-variance tradeoff. This is a direct optimization step that does not reduce the final estimator to its inputs by construction, nor does it rely on self-definitional equations, fitted parameters renamed as predictions, or load-bearing self-citations. The provided abstract and context describe a standard data-driven procedure consistent with external DiD assumptions, with no quoted steps showing equivalence to inputs. The central claim remains independent content.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Journal of Economic Literature , volume=

Difference-in-Differences Designs: A Practitioner's Guide , author=. Journal of Economic Literature , volume=

-

[2]

Journal of Financial Economics , volume=

How much should we trust staggered difference-in-differences estimates? , author=. Journal of Financial Economics , volume=

-

[3]

2023 , eprint=

Difference-in-Differences Estimation with Spatial Spillovers , author=. 2023 , eprint=

2023

-

[4]

Journal of Econometrics , volume=

Difference-in-differences with multiple time periods , author=. Journal of Econometrics , volume=

-

[5]

Econometrica , volume =

Robust Nonparametric Confidence Intervals for Regression-Discontinuity Designs , author =. Econometrica , volume =

-

[6]

American Economic Review , volume=

Minimum wages and employment: A case study of the fast-food industry in New Jersey and Pennsylvania , author=. American Economic Review , volume=

-

[7]

American Economic Review , volume=

Two-way fixed effects estimators with heterogeneous treatment effects , author=. American Economic Review , volume=

-

[8]

The Econometrics Journal , volume=

Two-way fixed effects and differences-in-differences with heterogeneous treatment effects: A survey , author=. The Econometrics Journal , volume=

-

[9]

Political Analysis , volume=

Using multiple pretreatment periods to improve difference-in-differences and staggered adoption designs , author=. Political Analysis , volume=

-

[10]

A simple approach to staggered difference-in-differences in the presence of spillovers , author=

-

[11]

American Economic Journal: Economic Policy , volume=

Early retirement incentives and student achievement , author=. American Economic Journal: Economic Policy , volume=

-

[12]

Replication data for: Early Retirement Incentives and Student Achievement , author=

-

[13]

Journal of Econometrics , volume=

Difference-in-differences with variation in treatment timing , author=. Journal of Econometrics , volume=

-

[14]

Econometrics , author=

-

[15]

2026 , archivePrefix=

Estimating Treatment Effects in Panel Data Without Parallel Trends , author=. 2026 , archivePrefix=

2026

-

[16]

The Review of Economic Studies , volume=

Optimal bandwidth choice for the regression discontinuity estimator , author=. The Review of Economic Studies , volume=

-

[17]

The Review of Economic Studies , volume=

A more credible approach to parallel trends , author=. The Review of Economic Studies , volume=

-

[18]

American Economic Review: Insights , volume=

Pretest with caution: Event-study estimates after testing for parallel trends , author=. American Economic Review: Insights , volume=

-

[19]

Journal of Econometrics , volume=

What's trending in difference-in-differences? A synthesis of the recent econometrics literature , author=. Journal of Econometrics , volume=

-

[20]

Journal of Econometrics , volume=

Estimating dynamic treatment effects in event studies with heterogeneous treatment effects , author=. Journal of Econometrics , volume=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.