Recognition: unknown

Causal State-Dependent Local Projections

Pith reviewed 2026-05-08 15:38 UTC · model grok-4.3

The pith

State-dependent local projections recover causal impulse responses under a linearity condition that holds in many models.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

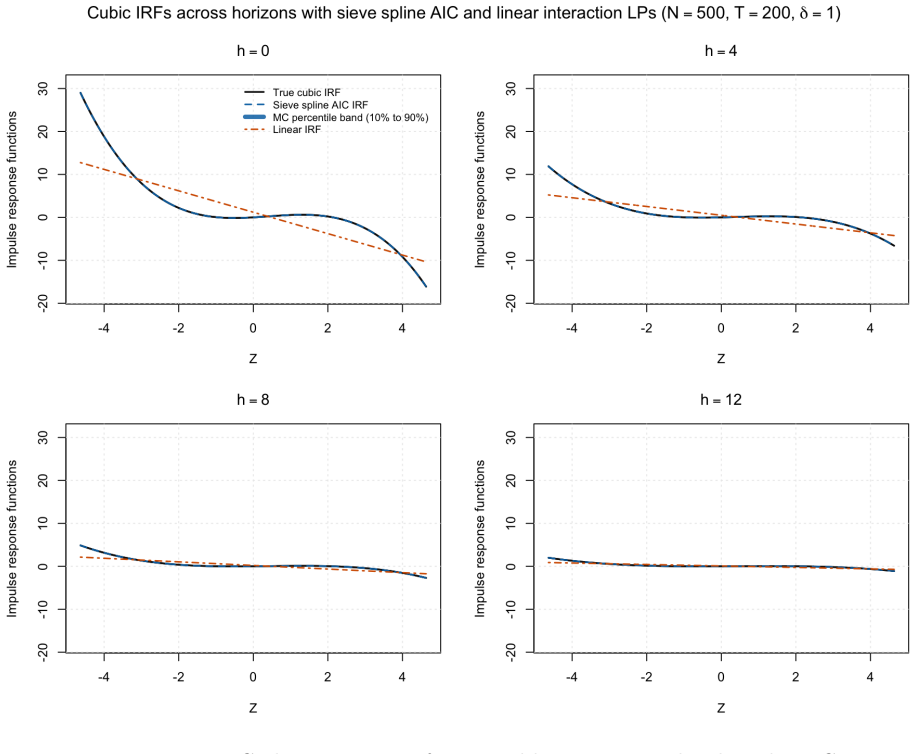

We show that this interpretation obtains under the sufficient condition that the conditional mean is linear in the aggregate shock at each horizon, and that this condition holds in a broad class of canonical micro-macro environments, including first-order perturbation solutions of heterogeneous-agent models and macro-finance models. Under this condition, LPs recover causal impulse responses without requiring specification of the full data-generating process. We further show that the causal interpretation of state-dependent LPs is robust to the choice of state variable. By contrast, commonly used linear interaction LPs generally fail to recover causal objects. We therefore develop a sieve-b

What carries the argument

The sufficient condition of linearity of the conditional mean in the aggregate shock at each horizon, allowing state-dependent local projections to identify causal impulse responses.

If this is right

- Causal impulse responses can be recovered from local projections without specifying the entire data-generating process.

- The linearity condition is satisfied in first-order perturbation solutions of heterogeneous-agent and macro-finance models.

- The causal interpretation holds regardless of the observable state variable used.

- A sieve-based nonparametric estimator provides valid pointwise and uniform inference for state-dependent effects in panel data.

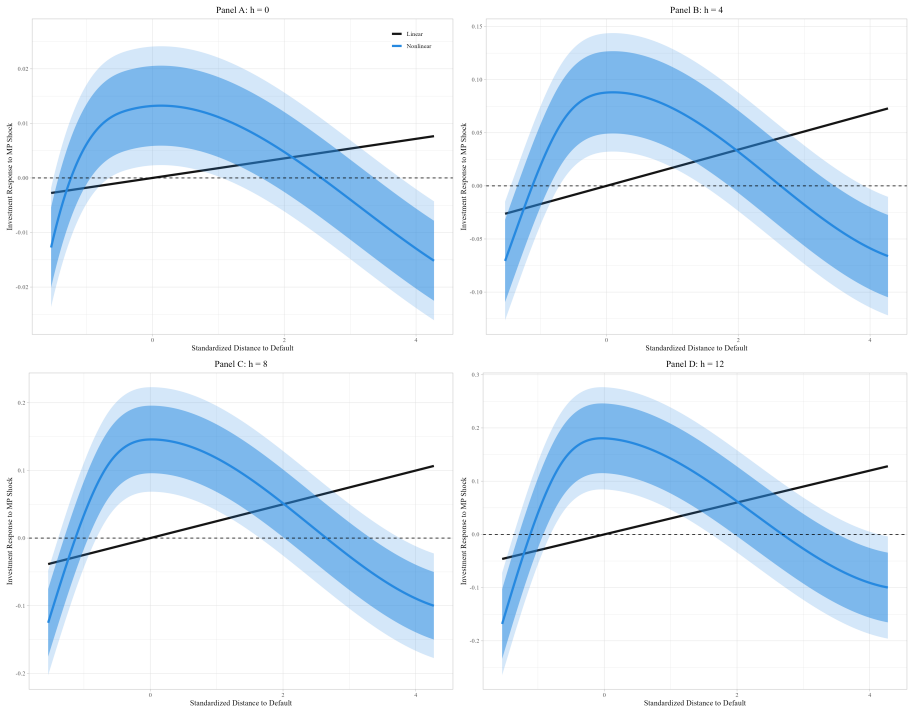

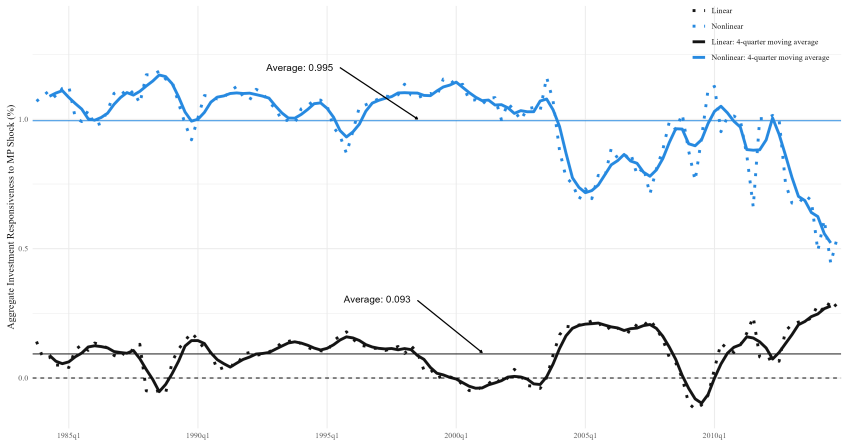

- Nonparametric state dependence alters the estimated pattern of firm investment responses and the aggregate transmission of monetary policy.

Where Pith is reading between the lines

- Empirical findings from studies using linear interaction terms may need to be revisited for causal validity.

- The approach could be tested or extended in other economic contexts involving state-dependent responses to shocks.

- Nonparametric methods might uncover additional heterogeneity in responses beyond what parametric assumptions allow.

- This could influence how macro models incorporate micro-level state dependence for better policy analysis.

Load-bearing premise

The conditional mean is linear in the aggregate shock at each horizon.

What would settle it

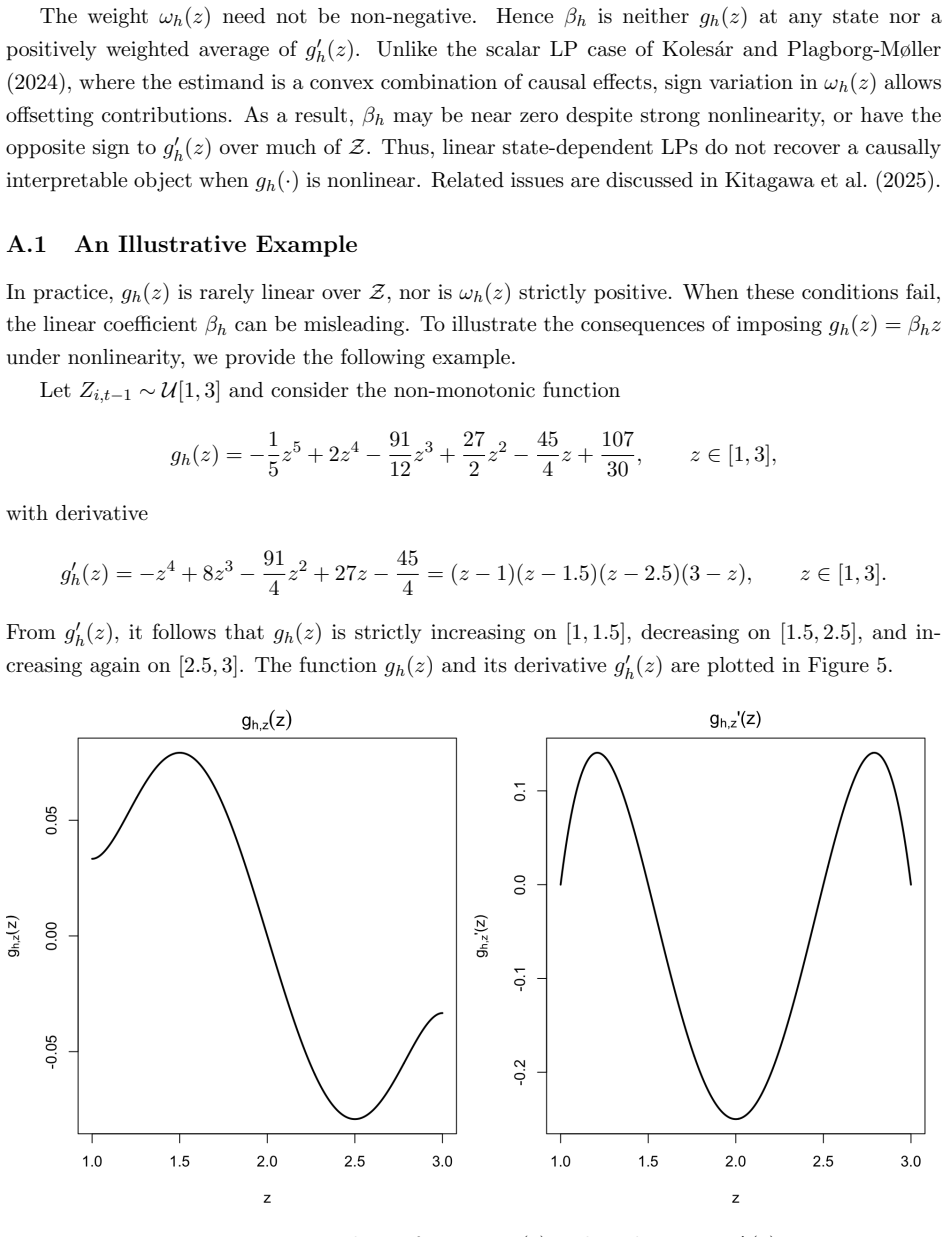

A demonstration that the conditional mean of the outcome is nonlinear in the aggregate shock at some horizon, either in data or in a model simulation, would show that the causal interpretation does not hold.

Figures

read the original abstract

State-dependent local projections (LPs) are widely used to estimate how responses to exogenous aggregate shocks vary as a function of observable state variables, yet their causal interpretation remains unclear. We show that this interpretation obtains under the sufficient condition that the conditional mean is linear in the aggregate shock at each horizon, and that this condition holds in a broad class of canonical micro-macro environments, including first-order perturbation solutions of heterogeneous-agent models and macro-finance models. Under this condition, LPs recover causal impulse responses without requiring specification of the full data-generating process. We further show that the causal interpretation of state-dependent LPs is robust to the choice of state variable. By contrast, commonly used linear interaction LPs generally fail to recover causal objects. We therefore develop a sieve-based nonparametric LP estimator that restores causal interpretation and delivers valid pointwise and uniform inference in micro-macro panels. Empirically, allowing for nonparametric state dependence materially changes both the pattern of heterogeneous firm investment responses and their aggregate implications for the transmission of monetary policy shocks.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that state-dependent local projections recover causal impulse responses under the sufficient condition that the conditional mean is linear in the aggregate shock at each horizon. This linearity is shown to hold in first-order perturbation solutions of heterogeneous-agent and macro-finance models. The authors argue that this allows causal interpretation without specifying the full DGP, that the result is robust to the choice of state variable, and that linear interaction LPs generally fail to recover causal objects. They develop a sieve-based nonparametric LP estimator that restores causal interpretation with valid pointwise and uniform inference in micro-macro panels. An empirical application to firm investment responses to monetary policy shocks shows that nonparametric state dependence materially alters both heterogeneous responses and aggregate implications.

Significance. If the linearity condition and its verification in perturbation solutions hold, the paper supplies a clear sufficient condition for causal interpretation of state-dependent LPs in a broad and policy-relevant class of models, without requiring full structural specification. The nonparametric sieve estimator with valid inference addresses a practical limitation of existing methods. The empirical results indicate that standard linear specifications can miss important heterogeneity in firm responses, with consequences for aggregate monetary transmission. The emphasis on sufficient (rather than necessary) conditions and the robustness to state-variable choice are constructive features.

minor comments (4)

- The abstract and introduction assert that the linearity condition holds in first-order perturbation solutions, but a brief summary of the key steps in that verification (e.g., how the state-dependent conditional expectation reduces under the perturbation) would improve accessibility without lengthening the paper.

- In the empirical application, the paper reports changes in heterogeneous responses and aggregate implications but does not include a direct check or discussion of whether the linearity condition appears to hold in the firm-level data; adding a short diagnostic (e.g., a plot of residuals versus shock size by state) would strengthen the link between theory and application.

- Notation for the sieve basis functions and the dimension choice in the nonparametric estimator could be made more explicit, particularly when stating the rate conditions for uniform inference.

- A small number of references to related work on nonparametric local projections or sieve methods in panels appear to be missing from the literature review.

Simulated Author's Rebuttal

We thank the referee for their positive and constructive assessment of our paper. The referee correctly summarizes our main contributions: the sufficient linearity condition for causal interpretation of state-dependent local projections, its verification in perturbation solutions of heterogeneous-agent and macro-finance models, robustness to state-variable choice, the contrast with linear interaction specifications, the sieve nonparametric estimator with valid inference, and the empirical findings on heterogeneous firm investment responses to monetary policy. We appreciate the recommendation for minor revision. No specific major comments were raised in the report, so we have no substantive revisions to propose at this stage.

Circularity Check

No significant circularity

full rationale

The derivation establishes that state-dependent LPs recover causal objects under the external sufficient condition of linearity of the conditional mean in the aggregate shock at each horizon. This condition is asserted to hold in first-order perturbation solutions of heterogeneous-agent and macro-finance models without being defined in terms of the LP estimator itself or reducing any reported impulse response to a fitted parameter by construction. No self-definitional steps, fitted-input predictions, load-bearing self-citations, or ansatz smuggling appear in the provided chain; the linearity assumption functions as an independent modeling restriction rather than a tautology.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The conditional mean is linear in the aggregate shock at each horizon

Reference graph

Works this paper leans on

-

[1]

Econometrica , volume=

Identification and Estimation of Local Average Treatment Effects , author=. Econometrica , volume=. 1994 , publisher=

1994

-

[2]

Jord. Local Projections , journal =. 2025 , pages =. doi:10.1257/jel.20241521 , url =

-

[3]

and Arellano, Manuel and Blundell, Richard and Bonhomme, Stéphane , title =

Almuzara, Martin. and Arellano, Manuel and Blundell, Richard and Bonhomme, Stéphane , title =

-

[4]

The Annals of Probability , volume =

Chernozhukov, Victor and Chetverikov, Denis and Kato, Kengo , title =. The Annals of Probability , volume =. 2017 , doi =

2017

-

[5]

Probability Theory and Related Fields , volume =

Chernozhukov, Victor and Chetverikov, Denis and Kato, Kengo , title =. Probability Theory and Related Fields , volume =. 2015 , doi =

2015

-

[6]

and Wellner, Jon A

van der Vaart, Aad W. and Wellner, Jon A. , title =. 1996 , series =

1996

-

[7]

Probability Theory and Related Fields , year =

Chernozhukov, Victor and Chetverikov, Denis and Kato, Kengo , title =. Probability Theory and Related Fields , year =

-

[8]

, title =

Chen, Xiaohong and Christensen, Timothy M. , title =. Journal of Econometrics , volume =. 2015 , publisher =

2015

-

[9]

The Annals of Statistics , year =

Zhang, Danna and Wu, Wei Biao , title =. The Annals of Statistics , year =

-

[10]

Donald W. K. Andrews , title =. Econometrica , year =

-

[11]

Foundations of Computational Mathematics , volume =

User-friendly tail bounds for sums of random matrices , author =. Foundations of Computational Mathematics , volume =. 2012 , publisher =

2012

-

[12]

Newey and Kenneth D

Whitney K. Newey and Kenneth D. West , title =. Econometrica , year =

-

[13]

and Linnik, Yurii V

Ibragimov, Ildar A. and Linnik, Yurii V. , title =. 1971 , address =

1971

-

[14]

, title =

Schumaker, Larry L. , title =. 1981 , address =

1981

-

[15]

and Lorentz, George G

DeVore, Ronald A. and Lorentz, George G. , title =. 1993 , address =

1993

-

[16]

, title =

Burkholder, Donald L. , title =. Colloque. 1988 , publisher =

1988

-

[17]

Journal of Theoretical Probability , year =

Rio, Emmanuel , title =. Journal of Theoretical Probability , year =

-

[18]

American Economic Review , volume=

The reversal interest rate , author=. American Economic Review , volume=. 2023 , publisher=

2023

-

[19]

Quantitative Economics , year =

Bayer, Christian and Luetticke, Ralph , title =. Quantitative Economics , year =

-

[20]

and Crosignani, Matteo and Eisert, Tim and Eufinger, Christian , title =

Acharya, Viral V. and Crosignani, Matteo and Eisert, Tim and Eufinger, Christian , title =. 2020 , doi =

2020

-

[21]

Econometrica , volume=

Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimation , author=. Econometrica , volume=. 1991 , publisher=

1991

-

[22]

2018 , institution =

The Intertemporal Keynesian Cross , author =. 2018 , institution =

2018

-

[23]

2020 , institution =

Micro Jumps, Macro Humps: Monetary Policy and Business Cycles in an Estimated HANK Model , author =. 2020 , institution =

2020

-

[24]

and Gorton, Gary and Krishnamurthy, Arvind , title =

Brunnermeier, Markus K. and Gorton, Gary and Krishnamurthy, Arvind , title =. Risk Topography: Systemic Risk and Macro Modeling , editor =

-

[25]

2024 , note =

Cui, Wei and Xie, Richard Cong and Zhang, Renbin , title =. 2024 , note =

2024

-

[26]

Journal of Business & Economic Statistics , volume=

Nonlinearity in Dynamic Causal Effects: Making the Bad into the Good, and the Good into the Great? , author=. Journal of Business & Economic Statistics , volume=. 2025 , publisher=

2025

-

[27]

2025 , month =

Paul Bousquet , title =. 2025 , month =

2025

-

[28]

2024 , eprint =

Identification and Estimation of Causal Effects in High-Frequency Event Studies , author =. 2024 , eprint =

2024

-

[29]

Stochastic Processes and their Applications , volume=

Empirical and multiplier bootstraps for suprema of empirical processes of increasing complexity, and related Gaussian couplings , author=. Stochastic Processes and their Applications , volume=. 2016 , publisher=

2016

-

[30]

arXiv preprint arXiv:2305.19089 , year=

Impulse Response Analysis of Structural Nonlinear Time Series Models , author=. arXiv preprint arXiv:2305.19089 , year=

-

[31]

NBER Macroeconomics Annual , volume=

A reassessment of monetary policy surprises and high-frequency identification , author=. NBER Macroeconomics Annual , volume=. 2023 , publisher=

2023

-

[32]

and Hoshi, Takeo and Kashyap, Anil K

Caballero, Ricardo J. and Hoshi, Takeo and Kashyap, Anil K. , title =. American Economic Review , year =

-

[33]

Journal of Econometrics , pages=

Inference on time series nonparametric conditional moment restrictions using nonlinear sieves , author=. Journal of Econometrics , pages=. 2024 , publisher=

2024

-

[34]

The Annals of Statistics , number =

Victor Chernozhukov and Denis Chetverikov and Kengo Kato , title =. The Annals of Statistics , number =. 2014 , doi =

2014

-

[35]

Journal of the European Economic Association , volume=

Monetary policy, corporate finance, and investment , author=. Journal of the European Economic Association , volume=. 2023 , publisher=

2023

-

[36]

American economic review , volume=

Credit spreads and business cycle fluctuations , author=. American economic review , volume=. 2012 , publisher=

2012

-

[37]

Journal of Financial Economics , volume=

Structural models of credit risk are useful: Evidence from hedge ratios on corporate bonds , author=. Journal of Financial Economics , volume=. 2008 , publisher=

2008

-

[38]

Journal of Banking & Finance , volume=

Robustness of distance-to-default , author=. Journal of Banking & Finance , volume=. 2015 , publisher=

2015

-

[39]

2011 , publisher=

Measuring corporate default risk , author=. 2011 , publisher=

2011

-

[40]

Research in Economics , volume=

Measuring the financial soundness of US firms, 1926--2012 , author=. Research in Economics , volume=. 2017 , publisher=

1926

-

[41]

Journal of financial economics , volume=

Multi-period corporate default prediction with stochastic covariates , author=. Journal of financial economics , volume=. 2007 , publisher=

2007

-

[42]

Chicago Fed Letter , volume=

The rise of intangible investment and the transmission of monetary policy , author=. Chicago Fed Letter , volume=. 2023 , publisher=

2023

-

[43]

The Review of Economic Studies , volume=

Split-panel jackknife estimation of fixed-effect models , author=. The Review of Economic Studies , volume=. 2015 , publisher=

2015

-

[44]

European Economic Review , year =

Durante, Elena and Ferrando, Annalisa and Vermeulen, Philip , title =. European Economic Review , year =

-

[45]

Journal of Econometrics , volume=

State-dependent local projections , author=. Journal of Econometrics , volume=. 2024 , publisher=

2024

-

[46]

2024 , month = nov, institution =

Nonparametric Local Projections , author =. 2024 , month = nov, institution =. doi:10.24149/wp2414 , note =

-

[47]

arXiv preprint arXiv:2506.13531 , year=

Identification of Impulse Response Functions for Nonlinear Dynamic Models , author=. arXiv preprint arXiv:2506.13531 , year=

-

[48]

American Economic Review , year =

He, Zhiguo and Krishnamurthy, Arvind , title =. American Economic Review , year =

-

[49]

Working Paper , year=

Firm balance sheet liquidity, monetary policy shocks, and investment dynamics , author=. Working Paper , year=

-

[50]

American economic review , volume=

Estimation and inference of impulse responses by local projections , author=. American economic review , volume=. 2005 , publisher=

2005

-

[51]

arXiv preprint arXiv:2411.10415 , year=

Dynamic Causal Effects in a Nonlinear World: the Good, the Bad, and the Ugly , author=. arXiv preprint arXiv:2411.10415 , year=

-

[52]

Journal of the American Statistical Association , volume=

Kernel meets sieve: Post-regularization confidence bands for sparse additive model , author=. Journal of the American Statistical Association , volume=. 2020 , publisher=

2020

-

[53]

Journal of International Economics , year =

Nickell bias in panel local projection: Financial crises are worse than you think , author =. Journal of International Economics , year =. doi:10.1016/j.jinteco.2025.104210 , note =

-

[54]

Econometrica , volume=

Local projection inference is simpler and more robust than you think , author=. Econometrica , volume=. 2021 , publisher=

2021

-

[55]

Econometrica , volume=

Financial heterogeneity and the investment channel of monetary policy , author=. Econometrica , volume=. 2020 , publisher=

2020

-

[56]

Journal of Econometrics , volume=

How do firms’ financial conditions influence the transmission of monetary policy? A non-parametric local projection approach , author=. Journal of Econometrics , volume=. 2025 , publisher=

2025

-

[57]

The Annals of Statistics , number =

Danna Zhang and Wei Biao Wu , title =. The Annals of Statistics , number =. 2017 , doi =

2017

-

[58]

The Annals of Statistics , number =

Ibrahim Ahmad and Sittisak Leelahanon and Qi Li , title =. The Annals of Statistics , number =. 2005 , doi =

2005

-

[59]

Lithuanian Mathematical Journal , volume=

Rate of convergence in the central limit theorem for random variables with strong mixing , author=. Lithuanian Mathematical Journal , volume=. 1984 , publisher=

1984

-

[60]

Econometrica , pages=

Inconsistency of the bootstrap when a parameter is on the boundary of the parameter space , author=. Econometrica , pages=. 2000 , publisher=

2000

-

[61]

Andrews, D. W. K. , title =. Econometrica , year =

-

[62]

Journal of

Democracy does cause growth , author=. Journal of. 2019 , publisher=

2019

-

[63]

Journal of Business & Economic Statistics , volume=

Dynamic semiparametric factor model with structural breaks , author=. Journal of Business & Economic Statistics , volume=. 2021 , publisher=

2021

-

[64]

Econometrica , volume=

Eigenvalue ratio test for the number of factors , author=. Econometrica , volume=. 2013 , publisher=

2013

-

[65]

2001 , publisher=

Ahn, Seung Chan and Lee, Young Hoon and Schmidt, Peter , journal=. 2001 , publisher=

2001

-

[66]

Journal of

Panel data models with multiple time-varying individual effects , author=. Journal of. 2013 , publisher=

2013

-

[67]

Journal of

Efficient estimation of models for dynamic panel data , author=. Journal of. 1995 , publisher=

1995

-

[68]

Journal of the

Clustering huge number of financial times series: a panel data approach with high-dimensional predictors and factor structures , author=. Journal of the

-

[69]

Arellano, Manuel , year=. Panel

-

[70]

and Ng, S

Bai, J. and Ng, S. D etermining the number of factors in approximate factor models. E conometrica. 2002

2002

-

[71]

Econometrica , volume=

Inferential theory for factor models of large dimensions , author=. Econometrica , volume=

-

[72]

Econometrica , volume=

Panel data models with interactive fixed effects , author=. Econometrica , volume=

-

[73]

Confidence intervals for diffusion index forecast and inference for factor-augmented regressions , author=

-

[74]

Theory and methods of panel data models with interactive effects , author=

-

[75]

Principal components estimation and identification of static factors , journal =

Jushan Bai and Serena Ng , keywords =. Principal components estimation and identification of static factors , journal =. 2013 , issn =. doi:https://doi.org/10.1016/j.jeconom.2013.03.007 , url =

-

[76]

2015 , publisher=

The Oxford Handbook of Panel Data , author=. 2015 , publisher=

2015

-

[77]

Economic growth in a cross section of countries , author=. The. 1991 , publisher=

1991

-

[78]

Biometrika , volume=

Uniform post-selection inference for least absolute deviation regression and other Z-estimation problems , author=. Biometrika , volume=. 2015 , publisher=

2015

-

[79]

Journal of Business & Economic Statistics , volume=

Inference in high-dimensional panel models with an application to gun control , author=. Journal of Business & Economic Statistics , volume=. 2016 , publisher=

2016

-

[80]

Measuring the effects of montary policy: a factor-augmented vector autoregressive (favar) approach , author=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.