Recognition: unknown

Numerical methods for lambda quantiles: robust evaluation and portfolio optimisation

Pith reviewed 2026-05-08 03:11 UTC · model grok-4.3

The pith

A hybrid Newton-bisection algorithm computes lambda quantiles reliably even with discontinuities and supports portfolio optimization.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper establishes that the Lambda-Newton-Bis algorithm combines Newton's method with a bisection strategy to ensure global convergence for lambda quantile computation, handles potential discontinuities, and attains local quadratic convergence under standard regularity assumptions. It further shows that embedding this procedure in two alternative portfolio optimization schemes produces computationally efficient solutions for risk-management problems that rely on lambda quantiles.

What carries the argument

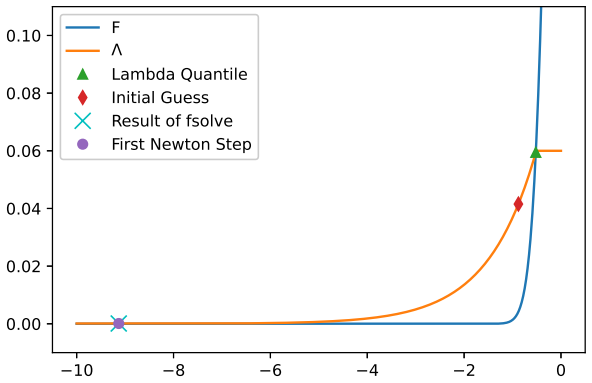

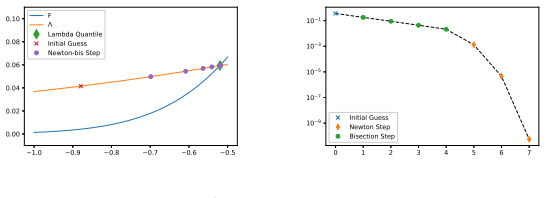

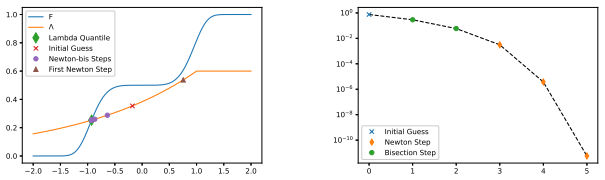

The Lambda-Newton-Bis algorithm, a hybrid of Newton's method and bisection that solves the defining equation of the lambda quantile while guaranteeing convergence despite jumps in the function.

If this is right

- Lambda quantiles become practical to evaluate for large data sets in risk management.

- Portfolio optimization problems that minimize or constrain lambda quantiles can be solved with the two proposed methods at reduced computational cost.

- The algorithm supplies both global reliability and quadratic local speed when the solution is approached.

- Interval analysis resolves cases where the defining equation admits more than one solution.

Where Pith is reading between the lines

- The same hybrid strategy could be tested on related risk measures that also produce discontinuous or non-monotone defining functions.

- Real-time trading systems might incorporate variable-confidence risk limits without sacrificing speed.

- Parameter choices for the lambda level could be optimized jointly with portfolio weights using the same root-finding routine.

Load-bearing premise

Lambda quantiles are well-defined as unique or identifiable roots of an equation, and the underlying function satisfies standard regularity conditions so that the hybrid Newton-bisection procedure converges globally and quadratically.

What would settle it

Apply the Lambda-Newton-Bis algorithm to a constructed lambda-quantile equation that contains a discontinuity exactly at the root or multiple roots within the search interval, then check whether the procedure returns a value outside a small tolerance of the true root or fails to terminate.

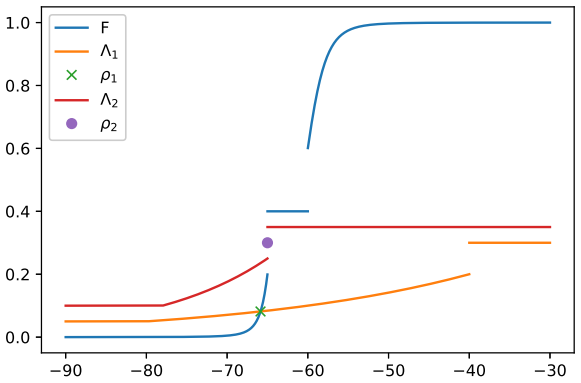

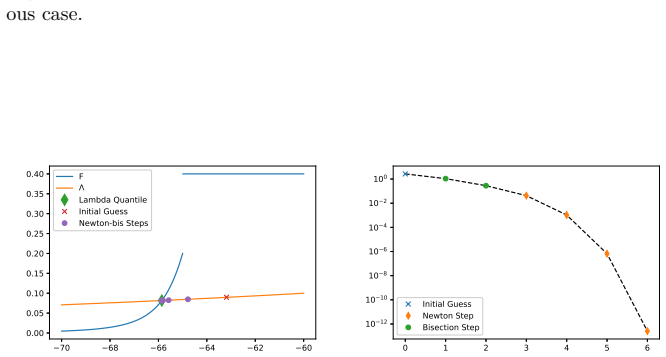

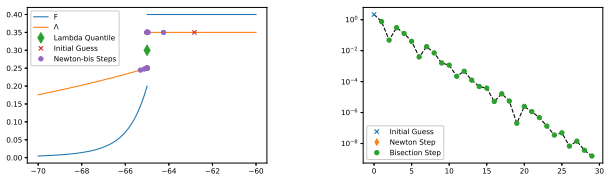

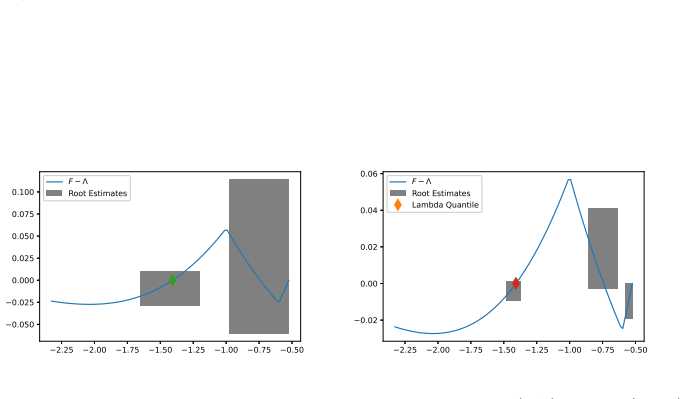

Figures

read the original abstract

Lambda quantiles, originally introduced as lambda value at risk, generalise the classical value at risk by allowing for a variable confidence level. This work presents efficient algorithms for computing lambda quantiles and demonstrates their application in portfolio optimisation. We first develop a robust algorithm, {\Lambda}-Newton-Bis, that combines Newton's method with a bisection strategy to ensure global convergence. The algorithm handles potential discontinuities and achieves local quadratic convergence under standard regularity assumptions. To address cases with multiple roots, we also propose an interval analysis approach. We then demonstrate the algorithm's computational efficiency and practical relevance within a portfolio optimization framework. To this end, we develop two alternative solution methods that incorporate the {\Lambda}-Newton-Bis procedure. Numerical experiments confirm the algorithm's convergence properties and highlight its computational advantages in optimization tasks based on lambda quantiles.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces lambda quantiles as a generalization of value-at-risk with a variable confidence level λ(x). It develops the Λ-Newton-Bis algorithm, which hybridizes Newton's method with bisection to guarantee global convergence while handling discontinuities in the underlying distribution function, and claims local quadratic convergence under standard regularity assumptions. The algorithm is then embedded in two alternative methods for portfolio optimization problems based on lambda quantiles, with numerical experiments used to demonstrate convergence behavior and computational gains.

Significance. If the convergence properties can be rigorously established for the empirical step-function distributions that arise in portfolio applications, the work supplies practical, robust numerical tools for lambda-quantile risk measures and optimization, which could improve computational efficiency in quantitative finance.

major comments (2)

- [Λ-Newton-Bis algorithm] Λ-Newton-Bis algorithm (section describing the hybrid method): local quadratic convergence of Newton's iteration requires that the derivative of the residual function be nonzero at the root. For the empirical distribution functions employed in the portfolio-optimization examples the sample CDF is a step function whose derivative vanishes almost everywhere (and is undefined at atoms). The bisection safeguard ensures a root is located but does not restore quadratic rate once the Newton phase begins; the manuscript must therefore state the observed convergence rate (or prove a weaker rate) for this data regime.

- [Numerical experiments] Numerical experiments section: the reported experiments confirm convergence and computational advantages, yet supply neither tabulated error-reduction factors nor raw iteration data that would allow verification of quadratic (versus linear) behavior on the discontinuous empirical CDFs central to the portfolio claims. Without such evidence the quadratic-convergence assertion remains unsupported for the very setting in which the method is applied.

minor comments (1)

- [Abstract and introduction] The abstract and introduction refer to 'standard regularity assumptions' without enumerating them; the paper should list the precise conditions (e.g., local Lipschitz continuity of the derivative, isolation of the root) under which quadratic convergence is asserted.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments, which help clarify the scope of our convergence results. We address each major point below and will revise the manuscript accordingly to strengthen the presentation of the algorithm's behavior on empirical distributions.

read point-by-point responses

-

Referee: [Λ-Newton-Bis algorithm] Λ-Newton-Bis algorithm (section describing the hybrid method): local quadratic convergence of Newton's iteration requires that the derivative of the residual function be nonzero at the root. For the empirical distribution functions employed in the portfolio-optimization examples the sample CDF is a step function whose derivative vanishes almost everywhere (and is undefined at atoms). The bisection safeguard ensures a root is located but does not restore quadratic rate once the Newton phase begins; the manuscript must therefore state the observed convergence rate (or prove a weaker rate) for this data regime.

Authors: We appreciate the referee pointing out the distinction between the theoretical setting and the empirical step-function case. The manuscript claims local quadratic convergence only under standard regularity assumptions that include a nonzero derivative at the root. For the discontinuous empirical CDFs arising in finite-sample portfolio optimization, we acknowledge that the local rate may reduce to linear once the Newton phase is active. In the revised manuscript we will explicitly state this limitation, add a discussion of the hybrid method's behavior on step functions, and report the observed convergence rates (including error-reduction factors) from the numerical experiments on the portfolio problems. revision: yes

-

Referee: [Numerical experiments] Numerical experiments section: the reported experiments confirm convergence and computational advantages, yet supply neither tabulated error-reduction factors nor raw iteration data that would allow verification of quadratic (versus linear) behavior on the discontinuous empirical CDFs central to the portfolio claims. Without such evidence the quadratic-convergence assertion remains unsupported for the very setting in which the method is applied.

Authors: We agree that the current numerical section would benefit from more granular data to allow independent verification of convergence rates on the empirical distributions. We will revise the experiments section to include tabulated error-reduction factors, raw iteration counts, and a direct comparison of observed rates against the theoretical quadratic prediction for the portfolio-optimization examples. This will substantiate the practical performance while clarifying the rate achieved in the discontinuous regime. revision: yes

Circularity Check

No circularity: algorithmic root-finding procedure with standard convergence analysis

full rationale

The paper develops the Λ-Newton-Bis hybrid algorithm for root-finding on the generalized inverse defining lambda quantiles, combining Newton steps with bisection for global convergence and claiming local quadratic convergence only under standard regularity assumptions (f'(root) ≠ 0). These properties follow directly from classical numerical analysis of hybrid methods and are not derived from or equivalent to the paper's own outputs, fitted parameters, or self-referential definitions. No equations reduce a claimed result to an input by construction, no load-bearing uniqueness theorems are imported via self-citation, and no ansatz or known empirical pattern is renamed as a new derivation. Numerical experiments serve as external validation of the implemented procedure rather than tautological confirmation. The work is self-contained algorithmic development.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Standard regularity assumptions hold so that Newton's method achieves local quadratic convergence and the hybrid strategy guarantees global convergence.

Reference graph

Works this paper leans on

-

[1]

Minimization of functions having Lipschitz continuous first partial derivatives

Larry Armijo. Minimization of functions having Lipschitz continuous first partial derivatives. Pacific Journal of Mathematics , 16(1):1–3, 1966

1966

-

[2]

Balakrishnan and S

N. Balakrishnan and S. Kocherlakota. On the double Weibull distribution: Order statistics and estimation. Sankhyā: The Indian Journal of Statistics, Series B , 47(2):161–178, 1985

1985

-

[3]

Lambda-quantiles as fixed points

Alejandro Balbás, Beatriz Balbás, and Raquel Balbás. Lambda-quantiles as fixed points. Available at SSRN 4583950 , 2023. 28

2023

-

[4]

On elicitable risk measures

Fabio Bellini and Valeria Bignozzi. On elicitable risk measures. Quantitative Finance, 15(5):725–733, 2015

2015

-

[5]

An axiomatization of Λ-quantiles

Fabio Bellini and Ilaria Peri. An axiomatization of Λ-quantiles. SIAM Journal on Financial Mathematics , 13(1), 2022

2022

-

[6]

Risk measures based on benchmark loss distributions

Valeria Bignozzi, Matteo Burzoni, and Cosimo Munari. Risk measures based on benchmark loss distributions. Journal of Risk and Insurance , 87(2):437–475, 2020

2020

-

[7]

Optimal insur- ance design with lambda-value-at-risk

Tim J Boonen, Yuyu Chen, Xia Han, and Qiuqi Wang. Optimal insur- ance design with lambda-value-at-risk. European Journal of Operational Research, 327(1):232–246, 2025

2025

-

[8]

Richard P. Brent. An algorithm with guaranteed convergence for finding a zero of a function. The Computer Journal , 14(4):422–425, 1971

1971

-

[9]

On the properties of the lambda value at risk: robustness, elicitability and consistency

Matteo Burzoni, Ilaria Peri, and Chiara M Ruffo. On the properties of the lambda value at risk: robustness, elicitability and consistency. Quantitative Finance, 17(11):1735–1743, 2017

2017

-

[10]

On the theory of elliptically contoured distributions

Stamatis Cambanis, Steel Huang, and Gordon Simons. On the theory of elliptically contoured distributions. Journal of Multivariate Analysis , 11(3):368–385, 1981

1981

-

[11]

Max- and min-stability under first-order stochastic dominance

Christopher Chambers, Alan Miller, Ruodu Wang, and Qinyu Wu. Max- and min-stability under first-order stochastic dominance. Mathematics and Financial Economics , 19:641–659, 2025

2025

-

[12]

Backtesting lambda value at risk

Jacopo Corbetta and Ilaria Peri. Backtesting lambda value at risk. The European Journal of Finance , 24(13):1075–1087, 2018

2018

-

[13]

Optimization Methods in Finance

Gérard Cornuéjols, Javier Peña, and Reha Tütüncü. Optimization Methods in Finance . Cambridge University Press, 2018

2018

-

[14]

Haskell B. Curry. The method of steepest descent for non-linear minimiza- tion problems. Quarterly of Applied Mathematics , 2:258–261, 1944

1944

-

[15]

Newton Methods for Nonlinear Problems

Peter Deuflhard. Newton Methods for Nonlinear Problems . Springer, 2011

2011

-

[16]

Risk measures on P(R) and value at risk with probability/loss function

Marco Frittelli, Marco Maggis, and Ilaria Peri. Risk measures on P(R) and value at risk with probability/loss function. Mathematical Finance , 24(3):442–463, 2014

2014

-

[17]

Making and evaluating point forecasts

Tilmann Gneiting. Making and evaluating point forecasts. Journal of the American Statistical Association, 106(494):746–762, 2011

2011

-

[18]

A. W. Tucker H. W. Kuhn. Nonlinear programming. Berkeley Symp. on Math. Statist. and Prob. , pages 481–492, 1951. 29

1951

-

[19]

Robust Λ-quantiles and extremal distributions

Xia Han and Peng Liu. Robust Λ-quantiles and extremal distributions. Mathematical Finance, 2025

2025

-

[20]

Cash-subadditive risk measures without quasi-convexity

Xia Han, Qiuqi Wang, Ruodu Wang, and Jianming Xia. Cash-subadditive risk measures without quasi-convexity. Mathematics of Operations Re- search, published online, 2025

2025

-

[21]

Lambda value at risk and regulatory capital: a dynamic approach to tail risk

Asmerilda Hitaj, Cesario Mateus, and Ilaria Peri. Lambda value at risk and regulatory capital: a dynamic approach to tail risk. Risks, 6(1):17, 2018

2018

-

[22]

Risk contributions of lambda quantiles

Akif Ince, Ilaria Peri, and Silvana Pesenti. Risk contributions of lambda quantiles. Quantitative Finance , 22(10):1871–1891, 2022

2022

-

[23]

60 years of portfolio optimization: Practical challenges and current trends

Petter N Kolm, Reha Tütüncü, and Frank J Fabozzi. 60 years of portfolio optimization: Practical challenges and current trends. European Journal of Operational Research, 234(2):356–371, 2014

2014

-

[24]

Risk sharing with lambda value at risk

Peng Liu. Risk sharing with lambda value at risk. Mathematics of Opera- tions Research, 50(1), 2024

2024

-

[25]

Risk sharing with lambda value at risk under heterogeneous beliefs

Peng Liu, Andreas Tsanakas, and Yunran Wei. Risk sharing with lambda value at risk under heterogeneous beliefs. arXiv preprint arXiv:2408.03147 , 2024

-

[26]

Moore, R

Ramon E. Moore, R. Baker Kearfott, and Michael J. Cloud. Introduction to Interval Analysis . SIAM, 2009

2009

-

[27]

Lectures on Convex Optimization

Yurii Nesterov. Lectures on Convex Optimization . Springer Optimization and Its Applications. Springer, 2nd edition, 2018

2018

-

[28]

Jorge Nocedal and Stephen J. Wright. Numerical Optimization . Springer, 2nd edition, 2006

2006

-

[29]

On the class of elliptical distributions and their applications to the theory of portfolio choice

Joel Owen and Ramon Rabinovitch. On the class of elliptical distributions and their applications to the theory of portfolio choice. The Journal of Finance, 38(3):745–752, 1983

1983

-

[30]

Numerical Mathemat- ics

Alfio Quarteroni, Riccardo Sacco, and Fausto Saleri. Numerical Mathemat- ics. Texts in Applied Mathematics. Springer, 2007

2007

-

[31]

Fifty years of portfolio optimization - A European perspective

Ahti Salo, Michalis Doumpos, Juuso Liesiö, and Constantin Zopounidis. Fifty years of portfolio optimization - A European perspective. European Journal of Operational Research , 2023

2023

-

[32]

D. C. Sorensen. Newton’s method with a model trust region modification. SIAM Journal on Numerical Analysis , 19(2):409–426, 1982

1982

-

[33]

Optimal risk sharing for lambda value-at-risk

Zichao Xia and Taizhong Hu. Optimal risk sharing for lambda value-at-risk. Advances in Applied Probability , pages 1–33, 2024. 30 A Deferred Proofs A.1 Proof of Theorem 1 As for ¯x = xl or ¯x = xr the algorithm immediately terminates successfully, we can consider ¯x ∈ (xmin, xmax) in the following. We formally consider the infinite sequence of iterates cr...

2024

-

[34]

By construction, ¯x ∈ [xi l, xi r] ⊂ [xmin, xmax] holds for all i > 0

We note that the algorithm either continues using a standard Newton step (line 21) or a bisection step (line 23). By construction, ¯x ∈ [xi l, xi r] ⊂ [xmin, xmax] holds for all i > 0. Thus if the length of the interval converges to zero, xi r − xi l → 0, we have convergence xi → ¯x. If the length of the interval does not converge to zero, there must be a...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.