Recognition: unknown

Funding-Aware Optimal Market Making for Perpetual DEXs

Pith reviewed 2026-05-08 03:17 UTC · model grok-4.3

The pith

Incorporating stochastic funding rates into the control problem improves optimal quotes for perpetual DEX market making.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

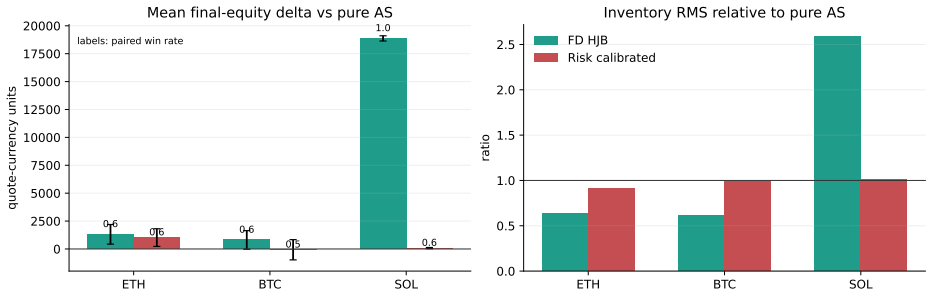

The central claim is that the funding-augmented value function yields quote offsets recovered from discrete inventory differences that, under two official-fill proxy calibrations, produce higher mean returns and lower root-mean-square inventory levels than the classical Avellaneda-Stoikov strategy in 100-seed simulations for ETH and BTC perpetuals on Hyperliquid.

What carries the argument

The reduced inventory-funding control problem whose solution via monotone finite-difference HJB yields state-dependent bid and ask offsets from value-function differences.

If this is right

- Higher mean performance for ETH and BTC liquidity provision once funding cash flows are included in the objective.

- Reduced root-mean-square inventory exposure relative to the classical model without funding dynamics.

- Positive performance gains for SOL versus the unscaled classical benchmark, though not a strict Pareto improvement against a risk-scaled version.

- A practical numerical route to recover optimal offsets directly from the solved value function on a discrete inventory grid.

Where Pith is reading between the lines

- Platforms could embed the funding state into real-time quoting engines so that market makers automatically tighten or widen spreads when funding rates move sharply.

- The same reduced-control approach may extend to other stochastic cash-flow terms such as borrowing fees or liquidation penalties that scale with position size.

- Out-of-sample tests on live order-book data would show whether the simulated fill proxies translate into actual execution advantages.

Load-bearing premise

That a Gaussian Ornstein-Uhlenbeck diffusion for the funding rate remains sufficient to derive and test the optimal quotes even though real funding innovations exhibit heavy tails.

What would settle it

A side-by-side simulation or live-trading comparison in which the funding-aware quotes lose their mean-performance or inventory-RMS advantage once the funding process is replaced by an OU-plus-jump model calibrated to the same data.

Figures

read the original abstract

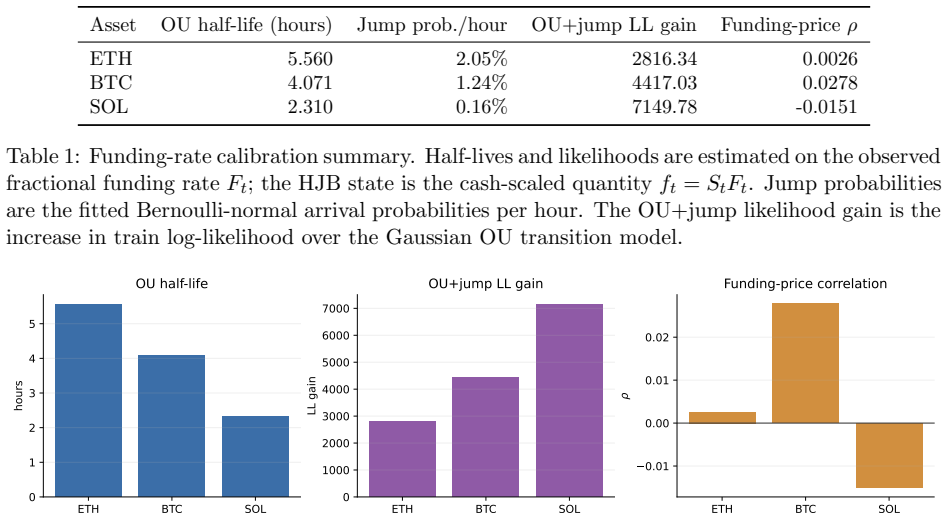

This paper studies optimal liquidity provision for perpetual contracts when the funding rate is a stochastic state variable. The core extension to classical market making is the coupling between inventory and funding payments: inventory creates both mark-to-market exposure and a state-dependent funding cash flow. A reduced inventory-funding control problem is formulated, solved with a monotone finite-difference Hamilton-Jacobi-Bellman scheme, and bid and ask quote offsets are recovered from discrete inventory value differences. Funding is calibrated on Hyperliquid ETH, BTC, and SOL perpetual data. Gaussian OU funding is retained as a tractable diffusion baseline, while OU-plus-jump diagnostics document the heavy-tailed funding innovations that should enter a future extension. In 100-seed holdout simulations under two official-fill proxy calibrations, the funding-aware HJB improves mean ETH/BTC performance while lowering inventory RMS relative to classical Avellaneda-Stoikov. SOL gains are positive versus unscaled AS but are not a Pareto improvement once a risk-scaled AS diagnostic is included.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper extends classical Avellaneda-Stoikov market making to perpetual DEXs by coupling inventory with a stochastic funding rate state variable. It formulates a reduced inventory-funding control problem, solves it via a monotone finite-difference HJB scheme, calibrates a Gaussian OU funding process on Hyperliquid ETH/BTC/SOL data, and reports that in 100-seed holdout simulations the funding-aware quotes improve mean performance for ETH/BTC while reducing inventory RMS relative to classical AS (with SOL results positive versus unscaled AS but not versus risk-scaled AS).

Significance. If the simulation results are robust, the work supplies a tractable numerical method for liquidity provision that internalizes funding cash flows, a distinctive feature of perpetual contracts. The calibration on real exchange data, explicit holdout protocol, and retention of the Gaussian OU as a documented baseline for future jump extensions are constructive elements that support applicability in DeFi perpetual markets.

major comments (2)

- [Abstract / Model formulation] Abstract and funding-model section: The manuscript documents heavy-tailed funding innovations via OU-plus-jump diagnostics yet derives the HJB value function and recovers bid/ask offsets exclusively under the Gaussian OU diffusion. Because the optimal quotes are obtained from discrete inventory-value differences under this process, any systematic mismatch with empirical funding dynamics directly affects the computed policy and the claimed outperformance versus Avellaneda-Stoikov in the holdout simulations.

- [Simulation results] Simulation-results paragraph: The reported improvements in mean ETH/BTC performance and inventory RMS are stated without accompanying magnitudes, standard errors across the 100 seeds, or formal statistical tests. This omission prevents assessment of whether the gains are economically material or sensitive to the two official-fill proxy calibrations.

minor comments (1)

- [Abstract] Clarify the precise definition of 'mean performance' (e.g., cumulative P&L, Sharpe, or other metric) and 'inventory RMS' when comparing the funding-aware HJB to both unscaled and risk-scaled Avellaneda-Stoikov baselines.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on our manuscript. We address each major point below and will make revisions to clarify modeling assumptions and strengthen the reporting of simulation results.

read point-by-point responses

-

Referee: [Abstract / Model formulation] Abstract and funding-model section: The manuscript documents heavy-tailed funding innovations via OU-plus-jump diagnostics yet derives the HJB value function and recovers bid/ask offsets exclusively under the Gaussian OU diffusion. Because the optimal quotes are obtained from discrete inventory-value differences under this process, any systematic mismatch with empirical funding dynamics directly affects the computed policy and the claimed outperformance versus Avellaneda-Stoikov in the holdout simulations.

Authors: We agree that the HJB value function and resulting bid/ask offsets are derived exclusively under the Gaussian OU funding process, as stated in the model section. The OU-plus-jump diagnostics are provided to document empirical heavy tails and to motivate future extensions, but the current policy and simulation comparisons are conditional on the OU specification. To address the concern, we will revise the abstract to explicitly state that the funding-aware quotes are obtained under the Gaussian OU diffusion and that the reported improvements versus classical Avellaneda-Stoikov hold under this modeling choice. revision: yes

-

Referee: [Simulation results] Simulation-results paragraph: The reported improvements in mean ETH/BTC performance and inventory RMS are stated without accompanying magnitudes, standard errors across the 100 seeds, or formal statistical tests. This omission prevents assessment of whether the gains are economically material or sensitive to the two official-fill proxy calibrations.

Authors: The referee is correct that the simulation paragraph reports only directional improvements without magnitudes, standard errors, or statistical tests. In the revised manuscript we will add the mean performance differences, standard errors computed across the 100 seeds, and p-values from paired statistical tests for the ETH/BTC and SOL comparisons under both official-fill proxy calibrations. This will allow readers to evaluate economic significance and sensitivity to the calibration choices. revision: yes

Circularity Check

No significant circularity; HJB derivation and simulation testing are independent

full rationale

The paper's core chain is: (1) formulate reduced inventory-funding stochastic control problem coupling inventory to stochastic funding cash flows; (2) solve numerically via monotone finite-difference HJB scheme; (3) recover bid/ask offsets from discrete value-function differences; (4) calibrate Gaussian OU parameters on Hyperliquid data solely for Monte-Carlo simulation testing; (5) compare funding-aware quotes against classical Avellaneda-Stoikov in 100-seed holdout simulations. None of these steps reduce to a self-definition, a fitted parameter renamed as prediction, or a load-bearing self-citation. The improvement claim is a model-consistent validation that the funding state variable adds value relative to the funding-ignorant benchmark; it is not forced by construction of the inputs. Calibration enters only post-derivation for testing, satisfying the independence criterion.

Axiom & Free-Parameter Ledger

free parameters (1)

- OU drift and volatility parameters for funding rate

axioms (2)

- domain assumption Funding rate dynamics can be approximated by a Gaussian Ornstein-Uhlenbeck process for the purpose of optimal control

- standard math The reduced inventory-funding control problem admits a unique viscosity solution recoverable via monotone finite differences

Reference graph

Works this paper leans on

-

[1]

Perpetual futures pricing.arXiv preprint arXiv:2310.11771, 2023

Damien Ackerer, Julien Hugonnier, and Urban Jermann. Perpetual futures pricing.arXiv preprint arXiv:2310.11771, 2023

-

[2]

Uniswap v2 core, 2020

Hayden Adams, Noah Zinsmeister, and Dan Robinson. Uniswap v2 core, 2020. White paper

2020

-

[3]

Uniswap v3 core, 2021

Hayden Adams, Noah Zinsmeister, Moody Salem, River Keefer, and Dan Robinson. Uniswap v3 core, 2021. White paper

2021

-

[4]

Bitmex bitcoin derivatives: Price discovery, informational efficiency, and hedging effectiveness.Journal of Futures Markets, 40(1):23–43, 2020

Carol Alexander, Jaehyuk Choi, Heungju Park, and Sungbin Sohn. Bitmex bitcoin derivatives: Price discovery, informational efficiency, and hedging effectiveness.Journal of Futures Markets, 40(1):23–43, 2020

2020

-

[5]

Optimal execution of portfolio transactions.Journal of Risk, 3(2):5–39, 2001

Robert Almgren and Neil Chriss. Optimal execution of portfolio transactions.Journal of Risk, 3(2):5–39, 2001

2001

-

[6]

Improved price oracles: Constant function market mak- ers.Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, pages 80–91, 2020

Guillermo Angeris and Tarun Chitra. Improved price oracles: Constant function market mak- ers.Proceedings of the 2nd ACM Conference on Advances in Financial Technologies, pages 80–91, 2020

2020

-

[7]

Optimal routing for constant function market makers.arXiv preprint arXiv:2204.05238, 2022

Guillermo Angeris, Tarun Chitra, Alex Evans, and Stephen Boyd. Optimal routing for constant function market makers.arXiv preprint arXiv:2204.05238, 2022

-

[8]

Replicating market makers.arXiv preprint arXiv:2103.14769, 2021

Guillermo Angeris, Alex Evans, and Tarun Chitra. Replicating market makers.arXiv preprint arXiv:2103.14769, 2021

-

[9]

Liquidity provision by automated market makers.SSRN Working Paper, 2020

Jun Aoyagi. Liquidity provision by automated market makers.SSRN Working Paper, 2020

2020

-

[10]

High-frequency trading in a limit order book.Quanti- tative Finance, 2008

Marco Avellaneda and Sasha Stoikov. High-frequency trading in a limit order book.Quanti- tative Finance, 2008

2008

-

[11]

Souganidis

Guy Barles and Panagiotis E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations.Asymptotic Analysis, 4(3):271–283, 1991

1991

-

[12]

Dimitris Bertsimas and Andrew W. Lo. Optimal control of execution costs.Journal of Finan- cial Markets, 1(1):1–50, 1998. 19

1998

-

[13]

Alvaro Cartea, Faycal Drissi, and Marcello Monga. Decentralised finance and automated mar- ket making: Predictable loss and optimal liquidity provision.arXiv preprint arXiv:2309.08431, 2023

-

[14]

Decentralised finance and automated market making: Execution and speculation.Journal of Economic Dynamics and Control, 177:105134, 2025

Alvaro Cartea, Faycal Drissi, and Marcello Monga. Decentralised finance and automated market making: Execution and speculation.Journal of Economic Dynamics and Control, 177:105134, 2025

2025

-

[15]

Cambridge University Press, 2015

Alvaro Cartea, Sebastian Jaimungal, and Jose Penalva.Algorithmic and High-Frequency Trad- ing. Cambridge University Press, 2015

2015

-

[16]

A stochastic model for order book dynamics

Rama Cont, Sasha Stoikov, and Rishi Talreja. A stochastic model for order book dynamics. Operations Research, 58(3):549–563, 2010

2010

-

[17]

Crandall, Hitoshi Ishii, and Pierre-Louis Lions

Michael G. Crandall, Hitoshi Ishii, and Pierre-Louis Lions. User’s guide to viscosity solutions of second order partial differential equations.Bulletin of the American Mathematical Society, 27(1):1–67, 1992

1992

-

[18]

Crandall and Pierre-Louis Lions

Michael G. Crandall and Pierre-Louis Lions. Viscosity solutions of hamilton-jacobi equations. Transactions of the American Mathematical Society, 277(1):1–42, 1983

1983

-

[19]

Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability

Philip Daian, Steven Goldfeder, Tyler Kell, Yunqi Li, Xueyuan Zhao, Iddo Bentov, Lorenz Breidenbach, and Ari Juels. Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. In2020 IEEE Symposium on Security and Privacy, pages 910–927, 2020

2020

-

[20]

The cost of transacting.The Quarterly Journal of Economics, 82(1):33–53, 1968

Harold Demsetz. The cost of transacting.The Quarterly Journal of Economics, 82(1):33–53, 1968

1968

-

[21]

Optimal liquidation of perpetual contracts

Ryan Donnelly, Junhan Lin, and Matthew Lorig. Optimal liquidation of perpetual contracts. arXiv preprint arXiv:2601.10812, 2026

-

[22]

Fleming and H

Wendell H. Fleming and H. Mete Soner.Controlled Markov Processes and Viscosity Solutions. Springer, 2 edition, 2006

2006

-

[23]

Pietro Fodra and Mauricio Labadie. High-frequency market-making with inventory constraints and directional bets.arXiv preprint arXiv:1206.4810, 2012

-

[24]

Glosten and Paul R

Lawrence R. Glosten and Paul R. Milgrom. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders.Journal of Financial Economics, 14(1):71– 100, 1985

1985

-

[25]

Gould, Mason A

Martin D. Gould, Mason A. Porter, Stacy Williams, Mark McDonald, Daniel J. Fenn, and Sam D. Howison. Limit order books.Quantitative Finance, 13(11):1709–1742, 2013

2013

-

[26]

Dealing with the inven- tory risk: a solution to the market making problem.Mathematics and Financial Economics, 2013

Olivier Gueant, Charles-Albert Lehalle, and Joaquin Fernandez-Tapia. Dealing with the inven- tory risk: a solution to the market making problem.Mathematics and Financial Economics, 2013

2013

-

[27]

Optimal high-frequency trading with limit and market orders.Quantitative Finance, 13(1):79–94, 2013

Fabien Guilbaud and Huyen Pham. Optimal high-frequency trading with limit and market orders.Quantitative Finance, 13(1):79–94, 2013

2013

-

[28]

Logarithmic market scoring rules for modular combinatorial information ag- gregation.Journal of Prediction Markets, 1(1):3–15, 2007

Robin Hanson. Logarithmic market scoring rules for modular combinatorial information ag- gregation.Journal of Prediction Markets, 1(1):3–15, 2007. 20

2007

-

[29]

Oxford Uni- versity Press, 2003

Larry Harris.Trading and Exchanges: Market Microstructure for Practitioners. Oxford Uni- versity Press, 2003

2003

-

[30]

Oxford University Press, 2007

Joel Hasbrouck.Empirical Market Microstructure: The Institutions, Economics, and Econo- metrics of Securities Trading. Oxford University Press, 2007

2007

-

[31]

Fundamentals of perpetual futures.arXiv preprint arXiv:2212.06888, 2022

Songrun He, Asaf Manela, Omri Ross, and Victor von Wachter. Fundamentals of perpetual futures.arXiv preprint arXiv:2212.06888, 2022

-

[32]

Thomas Ho and Hans R. Stoll. Optimal dealer pricing under transactions and return uncer- tainty.Journal of Financial Economics, 9(1):47–73, 1981

1981

-

[33]

Stochastic modeling of funding rate dynamics with jumps.SSRN Working Paper 5290137, 2025

Shreyash Kharat. Stochastic modeling of funding rate dynamics with jumps.SSRN Working Paper 5290137, 2025

2025

-

[34]

Jaehyun Kim and Hyungbin Park. Designing funding rates for perpetual futures in cryptocur- rency markets.arXiv preprint arXiv:2506.08573, 2025

-

[35]

Kushner and Paul G

Harold J. Kushner and Paul G. Dupuis.Numerical Methods for Stochastic Control Problems in Continuous Time. Springer, 2 edition, 2001

2001

-

[36]

Albert S. Kyle. Continuous auctions and insider trading.Econometrica, 53(6):1315–1335, 1985

1985

-

[37]

Moallemi, Tim Roughgarden, and Anthony Lee Zhang

Jason Milionis, Ciamac C. Moallemi, Tim Roughgarden, and Anthony Lee Zhang. Automated market making and loss-versus-rebalancing.arXiv preprint arXiv:2208.06046, 2022

-

[38]

Automated market makers and decentralized exchanges: A defi primer.Finan- cial Innovation, 8(1):20, 2022

Vijay Mohan. Automated market makers and decentralized exchanges: A defi primer.Finan- cial Innovation, 8(1):20, 2022

2022

-

[39]

Blackwell, 1995

Maureen O’Hara.Market Microstructure Theory. Blackwell, 1995

1995

-

[40]

Springer, 2009

Huyen Pham.Continuous-Time Stochastic Control and Optimization with Financial Applica- tions. Springer, 2009

2009

-

[41]

Decentralized finance: On blockchain- and smart contract-based financial mar- kets.Federal Reserve Bank of St

Fabian Schar. Decentralized finance: On blockchain- and smart contract-based financial mar- kets.Federal Reserve Bank of St. Louis Review, 103(2):153–174, 2021

2021

-

[42]

Springer, 2013

Nizar Touzi.Optimal Stochastic Control, Stochastic Target Problems, and Backward SDE. Springer, 2013

2013

-

[43]

Werner, Daniel Perez, Lewis Gudgeon, Ariah Klages-Mundt, Dominik Harz, and William J

Sam M. Werner, Daniel Perez, Lewis Gudgeon, Ariah Klages-Mundt, Dominik Harz, and William J. Knottenbelt. Sok: Decentralized finance (defi).arXiv preprint arXiv:2101.08778, 2022. 21

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.