Recognition: 2 theorem links

· Lean TheoremA Market-Rule-Informed Neural Network for Efficient Imbalance Electricity Price Forecasting

Pith reviewed 2026-05-12 02:01 UTC · model grok-4.3

The pith

Embedding market rules into a neural network's latent space yields competitive imbalance price forecasts with far fewer parameters.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The proposed market-rule-informed neural forecasting framework embeds imbalance price formation rules into the latent space of an expressive neural network, preserves raw signal information while exploiting transparent market-rule priors, and achieves competitive forecasting performance with substantially fewer trainable parameters and shorter training time than generic deep learning baselines.

What carries the argument

The market-rule-informed neural forecasting framework that embeds imbalance price formation rules into the neural network latent space while preserving raw signals.

If this is right

- Competitive forecasting accuracy on imbalance electricity prices.

- Substantially fewer trainable parameters than generic deep learning baselines.

- Shorter training time for industrial deployment.

- Joint use of market-rule priors and expressive neural networks supports computationally sustainable forecasting in energy trading.

Where Pith is reading between the lines

- The same rule-embedding pattern could reduce compute needs in other regulated markets that publish explicit price-formation formulas.

- Removing price-component information tests robustness to real data outages and may guide which market signals are truly essential.

- Scaling behavior with input length and forecast horizon suggests the approach can be tuned for different operational time scales in battery bidding systems.

Load-bearing premise

Imbalance price formation rules can be accurately and usefully embedded into the neural network latent space while preserving raw signal information and without introducing bias or limiting generalization to new market conditions.

What would settle it

A side-by-side experiment on unseen market data in which a standard neural network without the rule embedding matches or exceeds the hybrid model's accuracy and efficiency would undermine the claimed value of the embedding.

Figures

read the original abstract

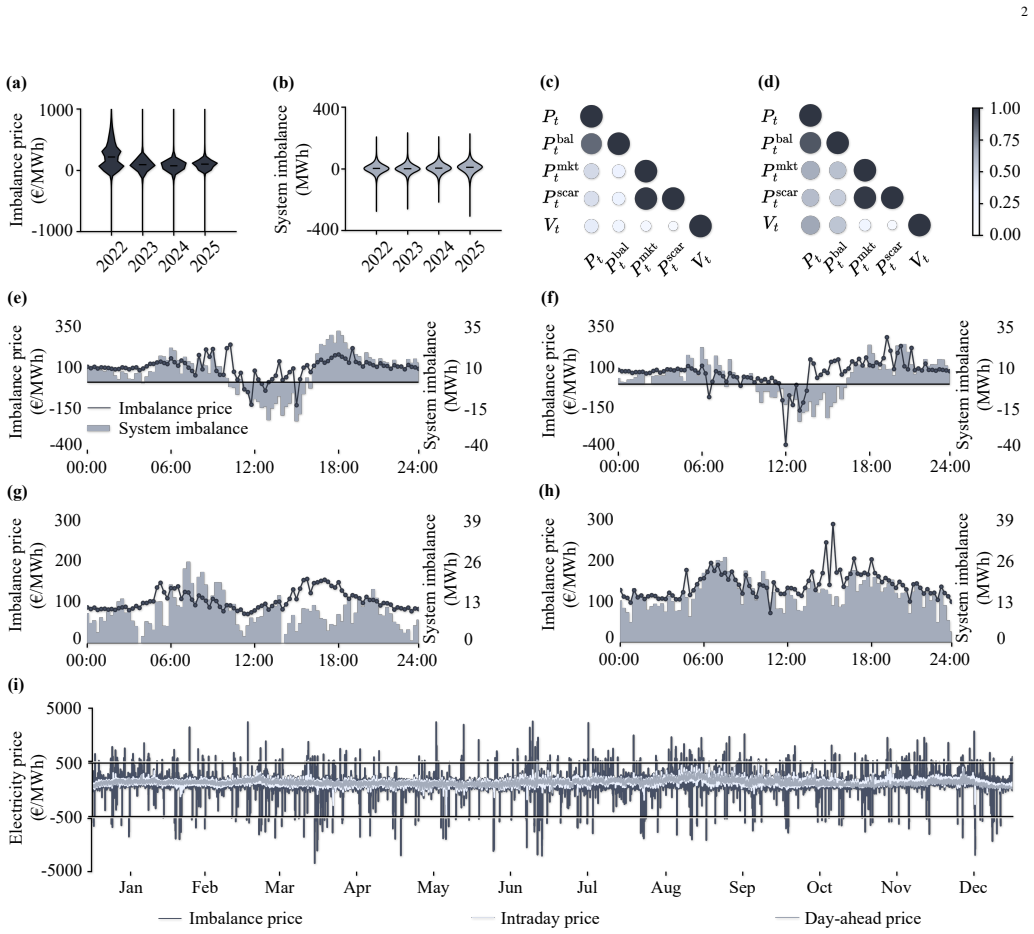

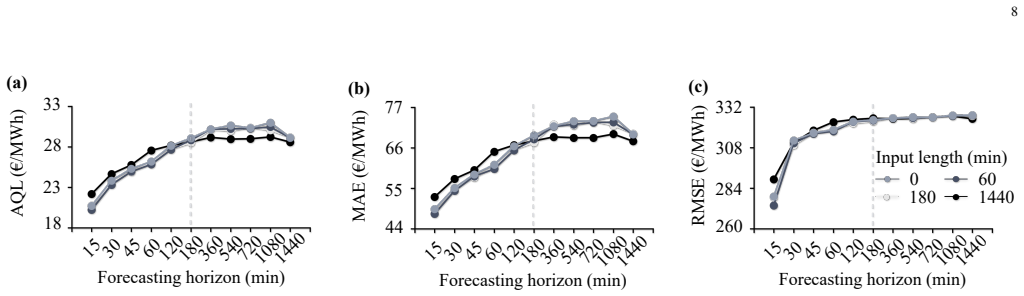

Accurate and efficient imbalance electricity price forecasting is critical for industrial energy trading systems, especially as battery assets and automated bidding pipelines increasingly participate in balancing markets. However, real-time forecasting is complicated by nonlinear market-rule-based price formation, heterogeneous input signals, and incomplete data availability caused by communication delays, publication lags, and measurement outages. This paper proposes a market-rule-informed neural forecasting framework that embeds imbalance price formation rules into the latent space of an expressive neural network. The proposed framework preserves raw signal information while exploiting transparent market-rule priors. We further analyze operational robustness by removing price-component information and characterize how forecasting performance scales with input length and forecasting horizon. Experimental results show that the proposed model achieves competitive forecasting performance with substantially fewer trainable parameters and shorter training time than generic deep learning baselines. Experimental results show that the proposed model achieves competitive forecasting performance with substantially fewer trainable parameters and shorter training time than generic deep learning baselines, demonstrating that market-rule priors and expressive neural networks should be jointly used for accurate and computationally sustainable forecasting in industrial energy trading applications. The implementation is publicly available at https://runyao-yu.github.io/MRINN/.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a market-rule-informed neural network (MRINN) framework for forecasting imbalance electricity prices. It embeds imbalance price formation rules as priors into the latent space of an expressive neural network while claiming to preserve raw heterogeneous input signals and avoid bias. The work analyzes operational robustness under removal of price-component information and characterizes scaling of performance with input length and forecasting horizon. Experiments are reported to show competitive accuracy with substantially fewer trainable parameters and shorter training times than generic deep learning baselines, with public code release.

Significance. If the embedding mechanism is shown to be unbiased and the efficiency gains are reproducible without hidden costs to generalization, the result would support hybrid domain-knowledge + neural approaches for computationally sustainable forecasting in industrial energy trading. This is relevant for real-time balancing markets involving battery assets and automated bidding, where both accuracy and low latency matter.

major comments (3)

- [Abstract / Methods] Abstract and methods description: the central claim that market-rule priors can be embedded into the NN latent space 'while preserving raw signal information' and 'without introducing bias' is load-bearing, yet the abstract provides no concrete description of the embedding technique (e.g., architectural constraints, regularizers, projection layers, or loss terms). Without this, it is impossible to verify that the efficiency gains do not arise from implicit filtering of inputs or incomplete rule coverage for edge cases such as extreme imbalances or regulatory changes.

- [Experimental Results] Experimental results section: the claims of 'competitive forecasting performance' and 'substantially fewer trainable parameters and shorter training time' rest on high-level assertions. No evaluation metrics, baseline implementations, statistical significance tests, error bars, cross-validation procedure, or handling of missing data (delays, outages) are specified. This prevents assessment of whether the reported gains are robust or merely artifacts of particular data splits or baseline choices.

- [Robustness / Scaling Analysis] Robustness analysis: the paper states it 'further analyze[s] operational robustness by removing price-component information,' but no quantitative results (e.g., degradation curves, specific horizons, or comparison tables) are referenced. This analysis is central to the industrial applicability claim and must be presented with concrete numbers and controls.

minor comments (3)

- [Abstract] The abstract contains a verbatim duplication of the sentence beginning 'Experimental results show that the proposed model achieves competitive forecasting performance...'

- [Abstract] The acronym MRINN is used in the title but not expanded or introduced in the abstract.

- [Implementation] The public implementation link is given, but the manuscript should include a brief reproducibility statement (e.g., random seeds, exact hyper-parameters, data sources) to match the claimed efficiency results.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. We address each major comment below and outline revisions that will strengthen the manuscript's clarity and completeness while preserving its core contributions.

read point-by-point responses

-

Referee: [Abstract / Methods] Abstract and methods description: the central claim that market-rule priors can be embedded into the NN latent space 'while preserving raw signal information' and 'without introducing bias' is load-bearing, yet the abstract provides no concrete description of the embedding technique (e.g., architectural constraints, regularizers, projection layers, or loss terms). Without this, it is impossible to verify that the efficiency gains do not arise from implicit filtering of inputs or incomplete rule coverage for edge cases such as extreme imbalances or regulatory changes.

Authors: We agree that the abstract is too high-level on the embedding mechanism and that this detail is necessary for readers to evaluate the unbiased-preservation claim. The methods section describes the embedding via a dedicated projection layer whose outputs are regularized by an auxiliary loss term derived directly from the imbalance price formation equations, combined with residual connections that pass the full raw input vector forward. This design avoids dimensionality reduction or filtering. To address the concern, we will revise the abstract to include a concise description of these components (e.g., 'via a rule-constrained projection layer and auxiliary loss that enforces market priors while retaining full input dimensionality through skip connections'). We will also add a short paragraph in the methods clarifying coverage of edge cases and how the formulation remains unbiased under regulatory shifts. revision: yes

-

Referee: [Experimental Results] Experimental results section: the claims of 'competitive forecasting performance' and 'substantially fewer trainable parameters and shorter training time' rest on high-level assertions. No evaluation metrics, baseline implementations, statistical significance tests, error bars, cross-validation procedure, or handling of missing data (delays, outages) are specified. This prevents assessment of whether the reported gains are robust or merely artifacts of particular data splits or baseline choices.

Authors: The experimental section reports MAE and RMSE values, parameter counts, and wall-clock training times for MRINN versus LSTM, GRU, and Transformer baselines, but we acknowledge that the protocol details (cross-validation folds, significance testing, error bars, and missing-data imputation) are not stated with sufficient explicitness. We will revise the section to specify the 5-fold cross-validation procedure, include standard-deviation error bars on all reported figures, describe the paired t-test results for significance, detail the forward-fill and outage-flagging strategy for missing observations, and provide the exact baseline hyper-parameter settings and data-split dates used. revision: yes

-

Referee: [Robustness / Scaling Analysis] Robustness analysis: the paper states it 'further analyze[s] operational robustness by removing price-component information,' but no quantitative results (e.g., degradation curves, specific horizons, or comparison tables) are referenced. This analysis is central to the industrial applicability claim and must be presented with concrete numbers and controls.

Authors: We agree that the robustness and scaling results must be presented quantitatively rather than asserted. The current manuscript contains the corresponding figures and tables in the supplementary material; we will move the key degradation curves (showing MAE increase when price components are ablated), scaling plots versus input length and horizon, and the associated numerical tables into the main text, with explicit controls for each forecasting horizon and a discussion of statistical variability. revision: yes

Circularity Check

No significant circularity; empirical validation stands independent of inputs

full rationale

The paper's core contribution is an architectural proposal to embed market-rule priors into a neural network's latent space while preserving raw signals, followed by empirical benchmarking against generic deep learning baselines on forecasting accuracy, parameter count, and training time. No load-bearing step reduces by construction to a fitted parameter renamed as prediction, a self-definitional loop, or a self-citation chain that substitutes for external verification. The performance claims rest on experimental results rather than tautological equivalence between model outputs and inputs. The embedding mechanism is presented as a design choice whose validity is tested externally via held-out data and ablation studies, not assumed by definition.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Imbalance price formation rules can be mathematically represented and embedded into a neural network's latent space while preserving raw input signals.

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclearembeds imbalance price formation rules into the latent space of an expressive neural network... differentiable pricing-rule operators... minlatent, maxlatent, abslatent, signlatent, divlatent, condlatent

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclearMRINN... 1,817 trainable parameters... competitive forecasting performance

Reference graph

Works this paper leans on

-

[1]

Statistical arbitrage and information flow in an electricity balancing market,

D. W. Bunn and S. O. Kermer, “Statistical arbitrage and information flow in an electricity balancing market,” The Energy Journal, vol. 42, no. 5, pp. 19–40, 2021

work page 2021

-

[2]

Predictions of prices and volumes in the nordic balancing markets for electricity,

S. Backe, S. Riemer-Sørensen, D. A. Bordvik, S. Tiwari, and C. A. Andresen, “Predictions of prices and volumes in the nordic balancing markets for electricity,” in2023 19th International Conference on the European Energy Market (EEM), IEEE, 2023, pp. 1–6

work page 2023

-

[3]

Probabilistic forecasting of german electricity imbalance prices,

M. Narajewski, “Probabilistic forecasting of german electricity imbalance prices,”Energies, vol. 15, no. 14, p. 4976, 2022

work page 2022

-

[4]

Electricity price forecasting in the irish balancing market,

C. O’Connor, J. Collins, S. Prestwich, and A. Visentin, “Electricity price forecasting in the irish balancing market,”Energy Strategy Reviews, vol. 54, p. 101 436, 2024. 10 TABLE III HYPERPARAMETER SEARCH SPACE. Model Search Space MRINN hidden size:{8, 32, 128} n layers:{2, 3, 4} iTransformer hidden size:{8, 32, 128} e layers:{2, 3, 4} n heads:{2, 4, 8} d...

work page 2024

-

[5]

W. W. Y . Ng, J. Zhang, C. S. Lai, W. Pedrycz, L. L. Lai, and X. Wang, “Cost-sensitive weighting and imbalance- reversed bagging for streaming imbalanced and con- cept drifting in electricity pricing classification,”IEEE Transactions on Industrial Informatics, vol. 15, no. 3, pp. 1588–1597, 2019.DOI: 10.1109/TII.2018.2850930

-

[6]

R. Yu et al.,Deep learning for electricity price fore- casting: A review of day-ahead, intraday, and bal- ancing electricity markets, 2026. arXiv: 2602 . 10071 [q-fin.CP]. [Online]. Available: https://arxiv.org/ abs/2602.10071

work page internal anchor Pith review arXiv 2026

-

[7]

Interpretable probabilistic forecasting of imbalances in renewable-dominated electricity systems,

J.-F. Toubeau, J. Bottieau, Y . Wang, and F. Vall ´ee, “Interpretable probabilistic forecasting of imbalances in renewable-dominated electricity systems,”IEEE Trans- actions on Sustainable Energy, vol. 13, no. 2, pp. 1267– 1277, 2021

work page 2021

-

[8]

D. H. Vu, K. M. Muttaqi, A. P. Agalgaonkar, and A. Bouzerdoum, “Short-term forecasting of electricity spot prices containing random spikes using a time-varying autoregressive model combined with kernel regression,” IEEE Transactions on Industrial Informatics, vol. 15, no. 9, pp. 5378–5388, 2019.DOI: 10.1109/TII.2019. 2911700

-

[9]

Forecasting imbalance price densities with statistical methods and neural net- works,

V . N. Ganesh and D. Bunn, “Forecasting imbalance price densities with statistical methods and neural net- works,”IEEE Transactions on Energy Markets, Policy and Regulation, vol. 2, no. 1, pp. 30–39, 2023

work page 2023

-

[10]

Dsformer: Dual-stream transformers with exogenous variables for electricity price forecasting,

C. Yang, H. Pan, J. Wang, and Y . Hong, “Dsformer: Dual-stream transformers with exogenous variables for electricity price forecasting,”IEEE Transactions on Industrial Informatics, pp. 1–10, 2026.DOI: 10.1109/ TII.2026.3673412

-

[11]

K. Plakas, N. Andriopoulos, D. Papadaskalopoulos, A. Birbas, E. Housos, and I. Moraitis, “Prediction of imbalance prices through gradient boosting algorithms: An application to the greek balancing market,”IEEE Access, 2025

work page 2025

-

[12]

X. Shen, H. Liu, G. Qiu, Y . Liu, J. Liu, and S. Fan, “Interpretable interval prediction-based outlier-adaptive day-ahead electricity price forecasting involving cross- market features,”IEEE Transactions on Industrial In- formatics, vol. 20, no. 5, pp. 7124–7137, 2024.DOI: 10.1109/TII.2024.3355105

- [13]

-

[14]

Seasonality in deep learning forecasts of elec- tricity imbalance prices,

S. Deng, J. Inekwe, V . Smirnov, A. Wait, and C. Wang, “Seasonality in deep learning forecasts of elec- tricity imbalance prices,”Energy Economics, vol. 137, p. 107 770, 2024

work page 2024

-

[15]

OrderFusion: Encoding Orderbook for End-to-End Probabilistic Intraday Electricity Price Forecasting

R. Yu et al.,Orderfusion: Encoding orderbook for end- to-end probabilistic intraday electricity price forecast- ing, 2026. arXiv: 2502.06830[q-fin.CP]. [Online]. Available: https://arxiv.org/abs/2502.06830

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[16]

PriceFM: Foundation Model for Probabilistic Electricity Price Forecasting

R. Yu et al.,Pricefm: Foundation model for proba- bilistic electricity price forecasting, 2026. arXiv: 2508. 04875[cs.CE]. [Online]. Available: https://arxiv.org/ abs/2508.04875

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[17]

J. Bottieau, Y . Wang, Z. De Greve, F. Vallee, and J.-F. Toubeau, “Interpretable transformer model for capturing regime switching effects of real-time electricity prices,” IEEE Transactions on Power Systems, vol. 38, no. 3, pp. 2162–2176, 2022

work page 2022

-

[18]

iTransformer: Inverted Transformers Are Effective for Time Series Forecasting

Y . Liu et al., “Itransformer: Inverted transformers are effective for time series forecasting,”arXiv preprint arXiv:2310.06625, 2023

work page internal anchor Pith review arXiv 2023

-

[19]

A time series is worth 64 words: Long-term forecast- ing with transformers,

Y . Nie, N. H. Nguyen, P. Sinthong, and J. Kalagnanam, “A time series is worth 64 words: Long-term forecast- ing with transformers,” inInternational Conference on Learning Representations, 2023

work page 2023

-

[20]

Timesnet: Temporal 2d-variation modeling for general time series analysis,

H. Wu, T. Hu, Y . Liu, H. Zhou, J. Wang, and M. Long, “Timesnet: Temporal 2d-variation modeling for general time series analysis,” inThe Eleventh Interna- tional Conference on Learning Representations, 2023. [Online]. Available: https://openreview.net/forum?id= ju Uqw384Oq

work page 2023

-

[21]

Timexer: Empowering transformers for time series forecasting with exogenous variables,

Y . Wang et al., “Timexer: Empowering transformers for time series forecasting with exogenous variables,” inAdvances in Neural Information Processing Sys- tems, A. Globerson et al., Eds., vol. 37, Curran As- sociates, Inc., 2024, pp. 469–498. [Online]. Available: https : / / proceedings . neurips . cc / paper files / paper / 2024/file/0113ef4642264adc2e69...

work page 2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.