Recognition: 2 theorem links

· Lean TheoremAdaptive Liquidity in Prediction Markets via Online Learning

Pith reviewed 2026-05-12 03:57 UTC · model grok-4.3

The pith

A prediction market can dynamically adapt its liquidity by mixing several fixed-liquidity cost functions using online learning weights.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The mechanism mixes a family of cost-function markets via learnable weights, yielding a single adaptive market that preserves no-arbitrage, bounded worst-case loss, expressiveness, and positive upside. Standard online learning algorithms achieve switching-regret guarantees relative to the best sequence of liquidity regimes in hindsight using a hybrid structural risk signal that quantifies the trade-off between price impact and inventory risk.

What carries the argument

Weighted combination of multiple cost-function markets, with weights learned online to minimize a hybrid structural risk signal that trades off price impact and inventory risk.

If this is right

- The combined market always satisfies no-arbitrage.

- The worst-case loss for the market maker stays bounded no matter how the weights adapt.

- Traders retain the ability to express arbitrary beliefs through their trades.

- The market maker retains positive expected profit potential.

- The adaptation achieves low switching regret compared to the optimal sequence of liquidity regimes chosen in hindsight.

Where Pith is reading between the lines

- Similar online learning could be applied to adjust other parameters in market design, such as fees or subsidy levels.

- The approach may generalize to non-stationary environments in auction design or dynamic pricing mechanisms.

- Real-world deployment would require testing whether the risk signal remains stable when traders anticipate the adaptation.

- It opens the possibility of fully automated, regret-optimal liquidity management in live prediction platforms.

Load-bearing premise

A hybrid structural risk signal exists that quantifies the price-impact versus inventory-risk trade-off in a way that allows standard online learning algorithms to achieve the switching-regret guarantees without violating the preserved market properties.

What would settle it

An explicit sequence of trades and market responses where the learned weights produce either an arbitrage opportunity, an unbounded loss, or regret that exceeds the claimed switching-regret bound.

Figures

read the original abstract

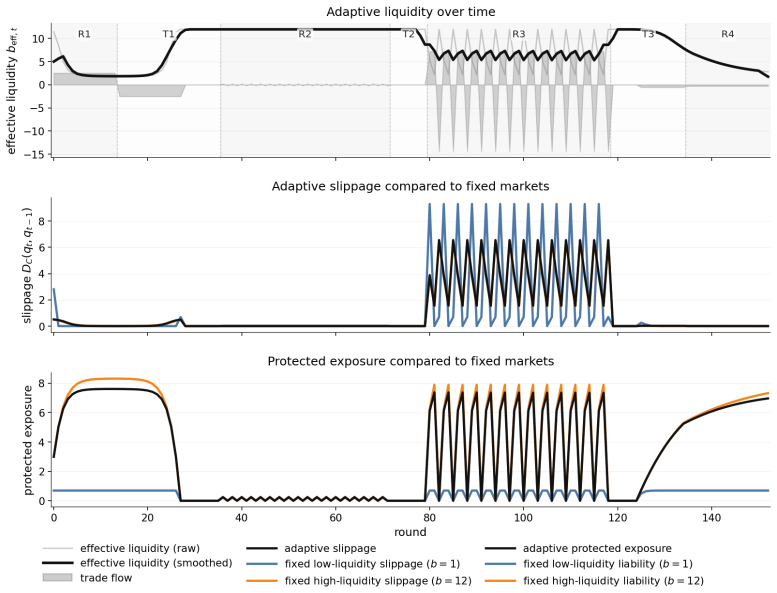

Prediction markets rely on liquidity to convert trades into informative prices, yet existing mechanisms fix liquidity ex ante. This restriction enforces a static trade-off between price responsiveness and worst-case loss despite inherently nonstationary trading conditions. We propose a fundamentally different approach that treats liquidity selection itself as an online learning problem. Our mechanism mixes a family of cost-function markets via learnable weights, yielding a single adaptive market that preserves no-arbitrage, bounded worst-case loss, expressiveness, and positive upside. We introduce a hybrid structural risk signal, a per-round objective that quantifies the trade-off between price impact and inventory risk, and show that standard online learning algorithms achieve switching-regret guarantees relative to the best sequence of liquidity regimes in hindsight. Simulations demonstrate that the mechanism adaptively shifts liquidity across regimes in response to both order flow and inventory dynamics. Our results establish a principled framework for adaptive liquidity, connecting prediction market design with online learning.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes treating liquidity selection in prediction markets as an online learning problem. It mixes a family of cost-function markets using learnable weights updated by standard online learning algorithms driven by a hybrid structural risk signal that trades off price impact against inventory risk. The central claims are that the resulting adaptive market preserves no-arbitrage, bounded worst-case loss, expressiveness, and positive upside while delivering switching-regret guarantees relative to the best sequence of liquidity regimes in hindsight, with simulations illustrating adaptive behavior.

Significance. If the construction and guarantees hold, the work supplies a principled bridge between online learning and prediction-market mechanism design, enabling liquidity to respond to non-stationary order flow and inventory without sacrificing the core economic invariants of cost-function markets. The explicit use of switching regret and the hybrid signal as a per-round objective are potentially valuable contributions if they can be shown to be compatible with market validity.

major comments (3)

- The hybrid structural risk signal is introduced as the per-round objective that enables the online learning step, yet no explicit functional form, proof of convexity or boundedness, or verification that it yields a valid loss for the chosen algorithms appears in the manuscript. Without this, it is impossible to confirm that the claimed switching-regret bounds are independent of the signal definition or that the adaptive weighting preserves the four market invariants at every round.

- The mixing operation over cost-function markets is asserted to preserve no-arbitrage and bounded worst-case loss for any weights, but the manuscript supplies neither the explicit convex-combination construction nor a proof that the effective cost function remains a valid cost function (i.e., convex, strictly increasing, etc.) under time-varying weights produced by the online learner.

- Simulations are invoked to demonstrate adaptive shifts across liquidity regimes, but the manuscript reports neither quantitative performance metrics, baseline comparisons, nor statistical significance; this leaves the empirical support for the theoretical claims unverified.

minor comments (1)

- Notation for the family of base markets and the weight vector is introduced without a dedicated notation table or consistent use across sections, making it difficult to track the dependence of the effective market on the learned weights.

Simulated Author's Rebuttal

We thank the referee for their constructive comments on our paper. We address each of the major comments in detail below, indicating the revisions we will make to strengthen the manuscript.

read point-by-point responses

-

Referee: The hybrid structural risk signal is introduced as the per-round objective that enables the online learning step, yet no explicit functional form, proof of convexity or boundedness, or verification that it yields a valid loss for the chosen algorithms appears in the manuscript. Without this, it is impossible to confirm that the claimed switching-regret bounds are independent of the signal definition or that the adaptive weighting preserves the four market invariants at every round.

Authors: We agree with the referee that the manuscript would benefit from a more explicit presentation of the hybrid structural risk signal. In the revised version, we will include the precise functional form in Section 3, which is a weighted sum of a price impact term (based on the derivative of the cost function) and an inventory risk term (based on the current position). We will prove its convexity as a sum of convex functions and its boundedness (normalized to [0,1]). Additionally, we will verify that it constitutes a valid loss function for the online gradient descent or follow-the-regularized-leader algorithms employed, ensuring the switching-regret bounds hold. We will also add a proposition demonstrating that the adaptive weighting preserves the market invariants at every round, as the mixture remains a valid cost function. revision: yes

-

Referee: The mixing operation over cost-function markets is asserted to preserve no-arbitrage and bounded worst-case loss for any weights, but the manuscript supplies neither the explicit convex-combination construction nor a proof that the effective cost function remains a valid cost function (i.e., convex, strictly increasing, etc.) under time-varying weights produced by the online learner.

Authors: We thank the referee for pointing this out. The mixing is performed by taking the convex combination of the individual cost functions using the weights output by the online learner at each round: the effective cost function is C(q) = sum_{i=1}^k w_i C_i(q), where sum w_i =1 and w_i >=0. Since each C_i is a valid cost function (convex, strictly increasing, C(0)=0), the combination inherits these properties. No-arbitrage is preserved because the market is still defined by a cost function, and the worst-case loss is bounded by the maximum loss bound of the component markets. We will add this explicit construction and the corresponding proof as a new lemma in the revised manuscript. Note that time-varying weights do not compromise validity because the properties hold for any fixed weights at each time step. revision: yes

-

Referee: Simulations are invoked to demonstrate adaptive shifts across liquidity regimes, but the manuscript reports neither quantitative performance metrics, baseline comparisons, nor statistical significance; this leaves the empirical support for the theoretical claims unverified.

Authors: We acknowledge that the current simulations primarily illustrate the qualitative adaptive behavior. In the revision, we will augment the experimental section with quantitative results, including average switching regret compared to the best fixed and best switching baselines, regret plots over time, and statistical significance via multiple independent runs with error bars. This will provide stronger empirical validation of the theoretical guarantees. revision: yes

Circularity Check

No significant circularity; derivation relies on external online learning theory

full rationale

The abstract introduces a hybrid structural risk signal as a new per-round objective quantifying price-impact versus inventory-risk trade-off, then states that standard online learning algorithms achieve switching-regret guarantees relative to the best sequence of liquidity regimes. No equations, definitions, or self-citations are supplied that reduce the claimed preservation of no-arbitrage, bounded loss, expressiveness, or positive upside to the signal definition itself or to any fitted input renamed as a prediction. The mechanism mixes cost-function markets via learnable weights, but the invariants and regret bounds are asserted to follow from the construction plus external OL results rather than any self-definitional loop or load-bearing self-citation. The derivation chain therefore remains self-contained against independent benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Standard online learning algorithms achieve switching-regret guarantees when applied to the hybrid structural risk signal

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.lean; IndisputableMonolith/Foundation/BranchSelection.leanwashburn_uniqueness_aczel; RCLCombiner_isCoupling_iff; costAlphaLog_high_calibrated_iff echoesCmix(q;w) = 1/β log ∑ w(k) e^{β C_k(q)}; slippage S_k,t = D_{C_k}(q_t, q_{t-1}); hybrid Γ_hyb,k,t = a(S_k,t - mean) + b L_k(q_t)

-

IndisputableMonolith/Foundation/AbsoluteFloorClosure.lean; IndisputableMonolith/Foundation/AlphaCoordinateFixation.leanabsolute_floor_iff_bare_distinguishability; J_uniquely_calibrated_via_higher_derivative refinesPay_mix preserves no-arbitrage, bounded worst-case loss, expressiveness under weight updates + fee = [Δ*_t]+

Reference graph

Works this paper leans on

-

[1]

Journal of Dynamics and Games , volume=

A continuous-time approach to online optimization , author=. Journal of Dynamics and Games , volume=. 2017 , publisher=

work page 2017

- [2]

-

[3]

ACM Transactions on Economics and Computation (TEAC) , volume=

Efficient market making via convex optimization, and a connection to online learning , author=. ACM Transactions on Economics and Computation (TEAC) , volume=. 2013 , publisher=

work page 2013

-

[4]

Proceedings of the twenty-ninth annual ACM-SIAM symposium on discrete algorithms , pages=

Cycles in adversarial regularized learning , author=. Proceedings of the twenty-ninth annual ACM-SIAM symposium on discrete algorithms , pages=. 2018 , organization=

work page 2018

-

[5]

Online optimization in games via control theory: Connecting regret, passivity and poincar

Cheung, Yun Kuen and Piliouras, Georgios , booktitle=. Online optimization in games via control theory: Connecting regret, passivity and poincar. 2021 , organization=

work page 2021

-

[6]

Unpublished Manuscript, http://ttic

On the duality of strong convexity and strong smoothness: Learning applications and matrix regularization , author=. Unpublished Manuscript, http://ttic. uchicago. edu/shai/papers/KakadeShalevTewari09. pdf , volume=

- [7]

-

[8]

Convergence rate of gradient descent algorithm on β-smooth ... , url=. Convergence rate of gradient descent algorithm on L-smooth function , author=. 2025 , month=

work page 2025

-

[9]

Advances in neural information processing systems , volume=

A regularized framework for sparse and structured neural attention , author=. Advances in neural information processing systems , volume=

-

[10]

Convex Analysis and Monotone Operator Theory in Hilbert Spaces , author=. 2017 , publisher=

work page 2017

-

[11]

Advances in Neural Information Processing Systems , volume=

Bounded-loss private prediction markets , author=. Advances in Neural Information Processing Systems , volume=

-

[12]

Budget Constraints in Prediction Markets , author=

-

[13]

Proceedings of the fifteenth ACM conference on economics and computation , pages=

A general volume-parameterized market making framework , author=. Proceedings of the fifteenth ACM conference on economics and computation , pages=

-

[14]

SIAM Journal on Optimization , volume=

A unified convergence analysis of block successive minimization methods for nonsmooth optimization , author=. SIAM Journal on Optimization , volume=. 2013 , publisher=

work page 2013

- [15]

-

[16]

Proceedings of the twenty-fifth annual ACM-SIAM symposium on Discrete algorithms , pages=

An almost-linear-time algorithm for approximate max flow in undirected graphs, and its multicommodity generalizations , author=. Proceedings of the twenty-fifth annual ACM-SIAM symposium on Discrete algorithms , pages=. 2014 , organization=

work page 2014

-

[17]

The Journal of Machine Learning Research , volume=

Regularization techniques for learning with matrices , author=. The Journal of Machine Learning Research , volume=. 2012 , publisher=

work page 2012

-

[18]

15th Innovations in Theoretical Computer Science Conference (ITCS 2024) , pages=

An Axiomatic Characterization of CFMMs and Equivalence to Prediction Markets , author=. 15th Innovations in Theoretical Computer Science Conference (ITCS 2024) , pages=. 2024 , organization=

work page 2024

-

[19]

Journal of convex analysis , volume=

The role of perspective functions in convexity, polyconvexity, rank-one convexity and separate convexity , author=. Journal of convex analysis , volume=

-

[20]

Journal of Optimization Theory and Applications , volume=

On a functional operation generating convex functions, part 1: duality , author=. Journal of Optimization Theory and Applications , volume=. 2005 , publisher=

work page 2005

-

[21]

Information Systems Frontiers , volume=

Combinatorial information market design , author=. Information Systems Frontiers , volume=. 2003 , publisher=

work page 2003

-

[22]

Wright, Stephen J. and Recht, Benjamin , year=. Optimization for Data Analysis , publisher=

-

[23]

The review of economic studies , volume=

The role of securities in the optimal allocation of risk-bearing , author=. The review of economic studies , volume=. 1964 , publisher=

work page 1964

-

[24]

Overview - Topics in Signal Processing , author=

Topics in signal processing , url=. Overview - Topics in Signal Processing , author=

-

[25]

Conference on Uncertainty in Artificial Intelligence , year=

Market making with decreasing utility for information , author=. Conference on Uncertainty in Artificial Intelligence , year=

- [26]

-

[27]

International conference on machine learning , pages=

From softmax to sparsemax: A sparse model of attention and multi-label classification , author=. International conference on machine learning , pages=. 2016 , organization=

work page 2016

-

[28]

Multi-outcome and Multidimensional Market Scoring Rules (Manuscript) , author=

-

[29]

Proceedings of the fourteenth ACM Conference on Electronic Commerce , pages=

An axiomatic characterization of adaptive-liquidity market makers , author=. Proceedings of the fourteenth ACM Conference on Electronic Commerce , pages=

-

[30]

Introduction to online convex optimization , author=. Foundations and Trends. 2016 , publisher=

work page 2016

-

[31]

Journal of Machine Learning Research , volume=

Metagrad: Adaptation using multiple learning rates in online learning , author=. Journal of Machine Learning Research , volume=

-

[32]

Presentation and Publication: Loss and Slippage in Networks of Automated Market Makers , author=. 3rd International Conference on Blockchain Economics, Security and Protocols (Tokenomics 2021) , pages=. 2022 , organization=

work page 2021

-

[33]

Journal of mathematical analysis and applications , volume=

Conjugate convex functions in optimal control and the calculus of variations , author=. Journal of mathematical analysis and applications , volume=. 1970 , publisher=

work page 1970

-

[34]

Conference on Learning Theory , pages=

Second-order quantile methods for experts and combinatorial games , author=. Conference on Learning Theory , pages=. 2015 , organization=

work page 2015

-

[35]

Conference on Learning Theory , pages=

A second-order bound with excess losses , author=. Conference on Learning Theory , pages=. 2014 , organization=

work page 2014

- [36]

-

[37]

Graphical models, exponential families, and variational inference , author=. Foundations and Trends. 2008 , publisher=

work page 2008

- [38]

-

[39]

International Workshop on Internet and Network Economics , pages=

Liquidity-sensitive automated market makers via homogeneous risk measures , author=. International Workshop on Internet and Network Economics , pages=. 2011 , organization=

work page 2011

-

[40]

Proceedings of the 13th ACM Conference on Electronic Commerce , pages=

Profit-charging market makers with bounded loss, vanishing bid/ask spreads, and unlimited market depth , author=. Proceedings of the 13th ACM Conference on Electronic Commerce , pages=

-

[41]

ACM Transactions on Economics and Computation (TEAC) , volume=

A practical liquidity-sensitive automated market maker , author=. ACM Transactions on Economics and Computation (TEAC) , volume=. 2013 , publisher=

work page 2013

-

[42]

arXiv preprint arXiv:2307.13624 , year=

Dynamic function market maker , author=. arXiv preprint arXiv:2307.13624 , year=

-

[43]

Journal of computer and system sciences , volume=

A decision-theoretic generalization of on-line learning and an application to boosting , author=. Journal of computer and system sciences , volume=. 1997 , publisher=

work page 1997

-

[44]

Machine learning: a probabilistic perspective , author=. 2012 , publisher=

work page 2012

-

[45]

Optimization and engineering , volume=

A tutorial on geometric programming , author=. Optimization and engineering , volume=. 2007 , publisher=

work page 2007

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.