Recognition: 2 theorem links

· Lean TheoremRobust Bayes Acts under Prior Perturbations: Contamination, Stability, and Selection Paths

Pith reviewed 2026-05-12 04:58 UTC · model grok-4.3

The pith

Two complementary stability measures quantify how robust Bayes-optimal acts are to prior perturbations in finite decision problems.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

In finite decision problems, the robustness radius and contamination need provide quantitative assessments of an act's stability under prior perturbations. These are solved via linear programming and bisection. A cost-adjusted version yields parametric selection rules whose paths reveal regime shifts. Application to portfolio strategies under regime uncertainty demonstrates how robustness considerations modify classical Bayes decisions.

What carries the argument

The robustness radius and contamination need, defined as optimization problems over prior perturbations and characterized through linear programming formulations that exploit monotonicity for efficient computation via bisection.

If this is right

- The cost-adjusted stability criterion generates a parametric family of decision rules indexed by a regularization parameter.

- Selection paths reveal structural transitions between stability-driven and cost-driven regimes as the parameter varies.

- Robustness-based selection refines classical expected utility by incorporating considerations of prior misspecification.

- In the portfolio choice example, different strategies exhibit distinct robustness and contamination profiles under heterogeneous belief specifications.

Where Pith is reading between the lines

- These stability notions could be tested in other finite decision settings, such as medical treatment choices under uncertain priors.

- The bisection computation method suggests the approach scales well to moderately sized finite problems.

- Selection paths might be used to analyze sensitivity in dynamic decision environments where priors evolve over time.

Load-bearing premise

Prior perturbations can be quantified such that the resulting optimization problems remain linear programs with the required monotonicity properties.

What would settle it

A counterexample in a small finite decision problem where the linear programming solution for the robustness radius does not correspond to the actual maximum perturbation preserving Bayes-optimality of the act.

Figures

read the original abstract

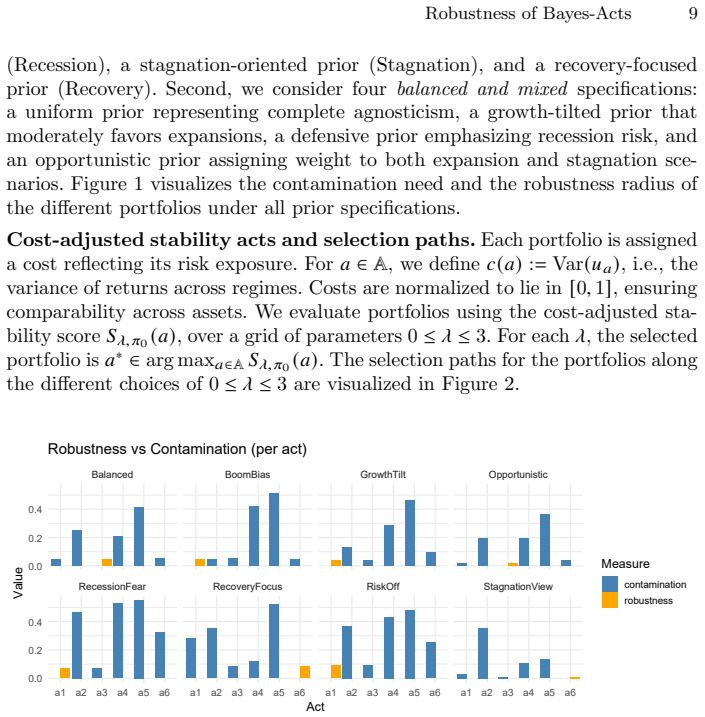

This paper develops a quantitative framework to assess the robustness of Bayes-optimal decisions in finite decision problems under model uncertainty. We introduce two complementary stability notions for acts: the robustness radius, measuring the largest perturbation of a reference prior under which an act remains Bayes-optimal, and the contamination need, quantifying the minimal perturbation required for an act to become Bayes-optimal under some nearby prior. Both concepts are characterized via linear programming formulations and computed efficiently using bisection methods exploiting monotonicity properties. Building on these stability measures, we propose a cost-adjusted stability criterion that integrates robustness considerations with act-specific selection costs, yielding a parametric family of decision rules indexed by a regularization parameter. We analyze how optimal act selection evolves along this parameter and derive selection paths that reveal structural transitions between stability-driven and cost-driven regimes. The framework is applied to a portfolio choice problem under uncertainty between different economic regimes. Concretely, using data on historical ETF returns, we compute robustness and contamination profiles for six portfolio strategies and analyze their behavior under heterogeneous belief specifications. The results illustrate that robustness-based selection refines classical expected utility by accounting for prior misspecification.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a quantitative framework to assess the robustness of Bayes-optimal decisions in finite decision problems under model uncertainty. It introduces the robustness radius and contamination need, characterized via linear programming and computed using bisection methods. It proposes a cost-adjusted stability criterion with a regularization parameter leading to selection paths, and applies it to portfolio choice with ETF data.

Significance. The framework extends robust Bayes methods with efficient computational tools and parametric selection rules. The LP formulations and monotonicity exploitation are standard but well-applied here, providing practical measures for decision stability. The portfolio application illustrates how robustness refines expected utility under prior misspecification. This could be significant for decision theory in statistics and economics if the derivations are tight.

minor comments (3)

- [Introduction] The motivation for the two complementary measures could be expanded with a simple example early on.

- [§4] Clarify how the bisection method exploits the monotonicity property with a proof sketch or reference.

- [Application] Provide more details on the discretization of the ETF returns data and the choice of the six strategies.

Simulated Author's Rebuttal

We thank the referee for the positive and accurate summary of our work, the recognition of its potential significance for decision theory, and the recommendation of minor revision. The referee's description of the robustness radius, contamination need, LP characterizations, bisection methods, cost-adjusted selection paths, and the ETF portfolio application aligns closely with the manuscript.

Circularity Check

No significant circularity detected in derivation chain

full rationale

The paper introduces robustness radius and contamination need as new stability notions explicitly characterized by linear programming formulations that are constructed independently of the target quantities. These are solved via bisection on monotonic value functions, which relies on standard LP duality and monotonicity properties external to the paper's definitions. The cost-adjusted stability criterion, parametric decision rules, and selection paths are then derived directly from these LP-based measures without any reduction to fitted parameters, self-definitional loops, or load-bearing self-citations. The portfolio application simply instantiates the finite-act framework on discretized data. All load-bearing steps rest on verifiable external technical ingredients rather than internal redefinitions or renamings, rendering the chain self-contained.

Axiom & Free-Parameter Ledger

free parameters (1)

- regularization parameter

axioms (2)

- domain assumption Finite decision problems allow characterization via linear programming

- domain assumption Monotonicity properties hold for the stability measures under prior perturbations

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclearrob(a,π0) and con(a,π0) characterized via linear programs with perturbation constraints and bisection exploiting monotonicity of R(ε)

-

IndisputableMonolith/Foundation/BranchSelection.leanbranch_selection unclearcost-adjusted stability score Sλ,π0(a) trading robustness radius against selection costs

Reference graph

Works this paper leans on

-

[1]

T. Augustin, F. Coolen, G. De Cooman, and M. Troffaes, eds.Introduction to Imprecise Probabilities. Wiley, 2014

work page 2014

-

[2]

Imprecise probabilities in engi- neering analyses

M. Beer, S. Ferson, and V. Kreinovich. “Imprecise probabilities in engi- neering analyses”. In:Mechanical Systems and Signal Processing37 (2013), pp. 4–29

work page 2013

-

[3]

Comparing ma- chine learning algorithms by union-free generic depth

H. Blocher, G. Schollmeyer, M. Nalenz, and C. Jansen. “Comparing ma- chine learning algorithms by union-free generic depth”. In:International Journal of Approximate Reasoning169 (2024), p. 109166

work page 2024

-

[4]

S. Boyd and L. Vandenberghe.Convex Optimization. Cambridge Univer- sity Press, 2004

work page 2004

-

[5]

Semi-supervised Learning Guided by the Generalized Bayes Rule Under Soft Revision

S. Dietrich, J. Rodemann, and C. Jansen. “Semi-supervised Learning Guided by the Generalized Bayes Rule Under Soft Revision”. In:Combining, Mod- elling and Analyzing Imprecision, Randomness and Dependence. Springer, 2024, pp. 110–117

work page 2024

-

[6]

D. Donoho and P. Huber. “The notion of breakdown point”. In:A festschrift for Erich L. Lehmann157184 (1983), p. 1004

work page 1983

-

[7]

Kenneth R. French Data Library

K. French. “Kenneth R. French Data Library”. In:Dartmouth College (2024).url: https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/ data library.html

work page 2024

-

[8]

P. Gordienko, C. Jansen, J. Rodemann, and G. Schollmeyer.Beyond Ar- row: From Impossibility to Possibilities in Multi-Criteria Benchmarking

- [9]

-

[10]

A General Qualitative Definition of Robustness

F. Hampel. “A General Qualitative Definition of Robustness”. In:The Annals of Mathematical Statistics42.6 (1971), pp. 1887–1896.doi: 10. 1214/aoms/1177693054.url: https://doi.org/10.1214/aoms/1177693054

-

[11]

Efficiency in normal samples and tolerance of extreme val- ues for some estimates of location

J. Hodges Jr. “Efficiency in normal samples and tolerance of extreme val- ues for some estimates of location”. In:Proceedings of the fifth Berkeley symposium on mathematical statistics and probability. Vol. 1. Univ of Cal- ifornia Press. 1967, pp. 163–186. 12 Christoph Jansen & Georg Schollmeyer

work page 1967

-

[12]

The use of previous experience in reaching statistical decisions

J. Hodges Jr and E. Lehmann. “The use of previous experience in reaching statistical decisions”. In:The Annals of Mathematical Statistics(1952), pp. 396–407

work page 1952

- [13]

-

[14]

C. Jansen.Contributions to the Decision Theoretic Foundations of Ma- chine Learning and Robust Statistics under Weakly Structured Informa- tion. Habilitationsschrift, Ludwig-Maximilians-Universit¨ at M¨ unchen: https: //arxiv.org/abs/2501.10195. 2025

-

[15]

C. Jansen. “Some Contributions to Decision Making in Complex Informa- tion Settings with Imprecise Probabilities and Incomplete Preferences”. PhD thesis. Ludwig-Maximilians-Universit¨ at M¨ unchen: https://edoc.ub. uni-muenchen.de/22653/1/Jansen Christoph.pdf, 2018

work page 2018

-

[16]

Decision Making with State-Dependent Pref- erence Systems

C. Jansen and T. Augustin. “Decision Making with State-Dependent Pref- erence Systems”. In:Information Processing and Management of Uncer- tainty in Knowledge-Based Systems. Springer, 2022, pp. 729–742

work page 2022

-

[17]

Decision Theory Meets Lin- ear Optimization Beyond Computation

C. Jansen, T. Augustin, and G. Schollmeyer. “Decision Theory Meets Lin- ear Optimization Beyond Computation”. In:Symbolic and Quantitative Approaches to Reasoning with Uncertainty. Springer, 2017, pp. 329–339

work page 2017

-

[18]

C. Jansen, H. Blocher, T. Augustin, and G. Schollmeyer. “Information ef- ficient learning of complexly structured preferences: Elicitation procedures and their application to decision making under uncertainty”. In:Interna- tional Journal of Approximate Reasoning144 (2022), pp. 69–91

work page 2022

-

[19]

Statistical Com- parisons of Classifiers by Generalized Stochastic Dominance

C. Jansen, M. Nalenz, G. Schollmeyer, and T. Augustin. “Statistical Com- parisons of Classifiers by Generalized Stochastic Dominance”. In:Journal of Machine Learning Research24.231 (2023), pp. 1–37

work page 2023

-

[20]

A probabilistic evaluation framework for preference aggregation reflecting group homogeneity

C. Jansen, G. Schollmeyer, and T. Augustin. “A probabilistic evaluation framework for preference aggregation reflecting group homogeneity”. In: Mathematical Social Sciences96 (2018), pp. 49–62

work page 2018

-

[21]

C. Jansen, G. Schollmeyer, and T. Augustin. “Concepts for decision mak- ing under severe uncertainty with partial ordinal and partial cardinal pref- erences”. In:International Journal of Approximate Reasoning98 (2018), pp. 112–131

work page 2018

-

[22]

Multi-target decision mak- ing under conditions of severe uncertainty

C. Jansen, G. Schollmeyer, and T. Augustin. “Multi-target decision mak- ing under conditions of severe uncertainty”. In:Modeling Decisions for Artificial Intelligence (MDAI). Springer. 2023

work page 2023

-

[23]

Quantifying degrees of E- admissibility in decision making with imprecise probabilities

C. Jansen, G. Schollmeyer, and T. Augustin. “Quantifying degrees of E- admissibility in decision making with imprecise probabilities”. In:Reflec- tions on the Foundations of Statistics: Essays in Honor of Teddy Seiden- feld. Springer, 2022, pp. 319–346

work page 2022

-

[24]

Robust statistical comparison of random variables with locally varying scale of measurement

C. Jansen, G. Schollmeyer, H. Blocher, J. Rodemann, and T. Augustin. “Robust statistical comparison of random variables with locally varying scale of measurement”. In:Proceedings of the Thirty-Ninth Conference on Uncertainty in Artificial Intelligence. Vol. 216. Proceedings of Machine Learning Research. PMLR, 2023, pp. 941–952. Robustness of Bayes-Acts 13

work page 2023

-

[25]

Statistical Multicriteria Benchmarking via the GSD-Front

C. Jansen, G. Schollmeyer, J. Rodemann, H. Blocher, and T. Augustin. “Statistical Multicriteria Benchmarking via the GSD-Front”. In:Advances in Neural Information Processing Systems 37 (NeurIPS 2024). 2024

work page 2024

-

[26]

E. Kofler and G. Menges.Entscheidungen bei unvollst¨ andiger Information. Springer, 1976

work page 1976

-

[27]

Impre- cise probability assessment of tipping points in the climate system

E. Kriegler, J. Hall, H. Held, R. Dawson, and H. Schellnhuber. “Impre- cise probability assessment of tipping points in the climate system”. In: Proceedings of the National Academy of Sciences106 (2009), pp. 5041– 5046

work page 2009

-

[28]

On indeterminate probabilities

I. Levi. “On indeterminate probabilities”. In:Journal of Philosophy71 (1974), pp. 391–418

work page 1974

-

[29]

In all likeli- hoods: robust selection of pseudo-labeled data

J. Rodemann, C. Jansen, G. Schollmeyer, and T. Augustin. “In all likeli- hoods: robust selection of pseudo-labeled data”. In:Proceedings of the 13th International Symposium on Imprecise Probability: Theories and Applica- tions. Vol. 215. PMLR, 2023, pp. 412–425

work page 2023

-

[30]

J. Ryan and J. Ulrich.quantmod: Quantitative Financial Modelling Frame- work. R package version available on CRAN. 2025.url: https://CRAN.R- project.org/package=quantmod

work page 2025

-

[31]

Savage.The Foundations of Statistics

L. Savage.The Foundations of Statistics. Wiley, 1954

work page 1954

-

[32]

Decision making under uncertainty using imprecise proba- bilities

M. Troffaes. “Decision making under uncertainty using imprecise proba- bilities”. In:International Journal of Approximate Reasoning45 (2007), pp. 17–29

work page 2007

-

[33]

L. Utkin and T. Augustin. “Powerful algorithms for decision making under partial prior information and general ambiguity attitudes”. In:Proceedings of the Fourth International Symposium on Imprecise Probability: Theories and Applications. SIPTA, 2005, pp. 349–358

work page 2005

-

[34]

J. Von Neumann and O. Morgenstern.Theory of Games and Economic Behavior. Princeton University Press, 1944

work page 1944

-

[35]

Walley.Statistical Reasoning with Imprecise Probabilities

P. Walley.Statistical Reasoning with Imprecise Probabilities. Chapman & Hall, 1991. [35]Yahoo Finance Historical Price Data. Accessed via thequantmodR pack- age. ETF price data for SPY, EFA, EEM, TLT, GLD, VNQ. 2024

work page 1991

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.