Recognition: 2 theorem links

· Lean TheoremOptimal Control of the Ethena Yield-Bearing Stablecoin

Pith reviewed 2026-05-13 00:46 UTC · model grok-4.3

The pith

The optimal rate for building or unwinding the Ethena position is derived in closed form for both infinite and finite horizons.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The authors formulate two stochastic control problems that capture the Ethena strategy. The state includes the current position size, the prevailing basis, and the stochastic funding rate and staking reward processes. The control is the instantaneous rate at which the protocol buys stETH and shorts the perpetual. Permanent impact shifts both mid-prices so that the basis narrows linearly with position size, while temporary impact adds linear slippage costs. For both the infinite-horizon discounted objective and the finite-horizon objective that includes a terminal liquidation cost, the Hamilton-Jacobi-Bellman equation admits an explicit solution, from which the optimal control is obtained in

What carries the argument

The stochastic control problem with linear permanent price impact that compresses the basis and linear temporary slippage, driven by stochastic funding-rate and staking-reward processes.

If this is right

- The optimal control trades off immediate carry income against the permanent reduction in future funding payments caused by basis compression.

- In the infinite-horizon case the control converges to a constant rate that depends explicitly on the discount rate and the impact coefficients.

- In the finite-horizon case the control includes a time-dependent term that accelerates or decelerates near the terminal date to manage liquidation costs.

- Because the solution is explicit, the value of the entire strategy can be computed directly for any set of current market parameters.

Where Pith is reading between the lines

- If the linear impact assumptions hold in real markets, the model supplies a practical rule for setting position-size caps that preserve the funding basis.

- The same control framework could be reused for other delta-neutral carry trades whose size affects their own yield sources.

- Empirical calibration of the impact parameters against observed basis dynamics would turn the closed-form control into a directly implementable trading signal.

Load-bearing premise

The model assumes particular linear functional forms for permanent and temporary price impacts together with specific stochastic processes for funding rates and staking rewards in order to obtain closed-form solutions.

What would settle it

Simulating the market with the assumed impact functions and processes and checking whether the actual position-adjustment rates observed in the Ethena protocol match the explicit optimal control derived from the model.

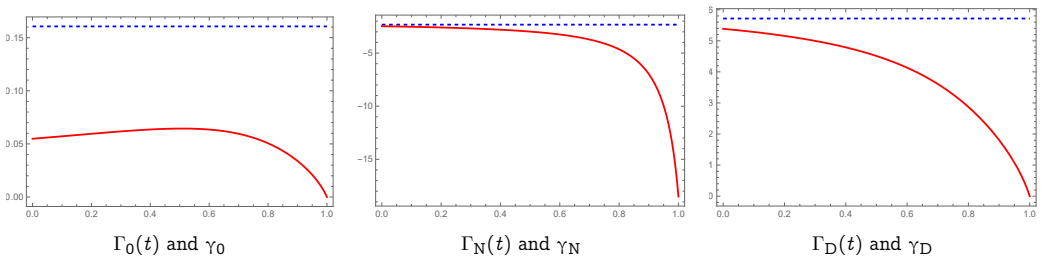

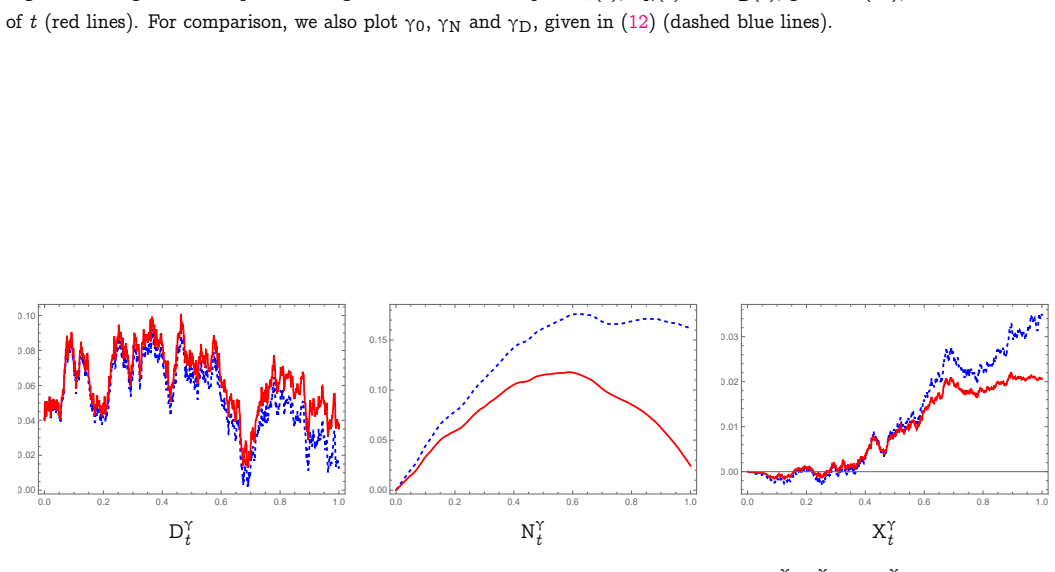

Figures

read the original abstract

We formulate and solve stochastic control problems that model the core yield-generating strategy of the Ethena protocol, a decentralized finance (DeFi) stablecoin that earns yield by combining a long position in staked Ethereum (stETH) with an equal-sized short position in ETH perpetual futures. The combined position is delta-neutral with respect to the ETH spot price, yet earns carry from two sources: staking rewards on the stETH leg, and funding-rate payments received from long perpetual holders when the perpetual trades at a premium to spot. A key feature of our model is that the control -- the rate of simultaneously buying stETH and shorting the perpetual -- exerts two distinct types of price impact. \textit{Permanent} impact shifts the mid-market prices of both legs, compressing the basis and permanently eroding future funding income. \textit{Temporary} impact reflects execution slippage on each leg. We study both an infinite-horizon discounted problem and a finite-horizon problem in which the protocol maximizes total wealth up to a fixed date $T$, subject to a terminal cost for liquidating any remaining position. In both cases the optimal control is obtained explicitly.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper formulates stochastic control problems for the Ethena protocol's core yield strategy: a delta-neutral long stETH/short ETH-perpetual position that earns staking rewards and funding-rate carry. Controls (simultaneous purchases of stETH and shorts of the perpetual) produce linear permanent impact that compresses the basis and erodes future funding income, plus quadratic temporary slippage. Stochastic dynamics are specified for funding rates and staking rewards. Explicit optimal controls are derived for both the infinite-horizon discounted problem and the finite-horizon problem with a terminal liquidation penalty.

Significance. If the derivations hold, the work supplies closed-form optimal controls for a realistic DeFi yield strategy under price impact, which is a useful analytical benchmark for protocol design, risk management, and algorithmic execution in crypto markets. The deliberate choice of functional forms that permit explicit HJB solutions is a methodological strength that enhances reproducibility and practical interpretability.

major comments (1)

- The central claim that optimal controls are obtained explicitly rests on the specific linear-permanent and quadratic-temporary impact functions together with the chosen stochastic processes for funding and staking rewards. The manuscript should verify that these forms are not merely convenient but are at least qualitatively consistent with observed Ethena basis dynamics; otherwise the explicit solutions remain a modeling artifact rather than a robust prediction.

minor comments (2)

- Notation for the permanent impact coefficient and the basis process should be introduced with a clear table or equation block early in the model section to avoid later ambiguity.

- The finite-horizon terminal penalty is described only qualitatively; an explicit functional form and its calibration rationale would improve transparency.

Simulated Author's Rebuttal

We thank the referee for the constructive comment and the positive overall assessment. We address the major point below and will incorporate revisions to strengthen the discussion of modeling assumptions.

read point-by-point responses

-

Referee: The central claim that optimal controls are obtained explicitly rests on the specific linear-permanent and quadratic-temporary impact functions together with the chosen stochastic processes for funding and staking rewards. The manuscript should verify that these forms are not merely convenient but are at least qualitatively consistent with observed Ethena basis dynamics; otherwise the explicit solutions remain a modeling artifact rather than a robust prediction.

Authors: We agree that the explicit solutions rely on the chosen functional forms, which were selected to permit closed-form HJB solutions while remaining consistent with standard market-impact modeling. Linear permanent impact is qualitatively supported by observed basis compression in ETH perpetual markets as large delta-neutral positions are accumulated, eroding funding rates over time; quadratic temporary impact aligns with execution slippage in relatively illiquid crypto venues. The Ornstein-Uhlenbeck dynamics for funding rates and staking rewards capture the mean-reverting behavior documented in DeFi historical data. In the revised manuscript we will add a dedicated paragraph in the model section providing this qualitative justification, supported by references to observed Ethena basis patterns during periods of high utilization. A full empirical calibration lies outside the scope of the present theoretical work. revision: yes

Circularity Check

No significant circularity; derivation self-contained

full rationale

The paper formulates a stochastic control problem with explicit functional forms for permanent and temporary price impact plus stochastic dynamics for funding and rewards, then solves the associated HJB equations to obtain closed-form optimal controls for both infinite- and finite-horizon cases. These functional forms are chosen precisely to permit explicit solutions, but the resulting controls are derived outputs rather than presupposed inputs or fitted parameters renamed as predictions. No self-citations, self-definitional steps, or reductions of the claimed result to the model's own equations by construction appear in the provided text. The derivation chain is therefore independent of its target result.

Axiom & Free-Parameter Ledger

free parameters (1)

- permanent and temporary impact coefficients

axioms (2)

- domain assumption Permanent impact permanently compresses the basis between spot and perpetual prices

- domain assumption Funding rates and staking rewards follow diffusion-type stochastic processes

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclearthe optimal control is obtained explicitly: in the infinite-horizon case via a quadratic ansatz for the Hamilton–Jacobi–Bellman (HJB) equation, and in the finite-horizon case via a time-dependent quadratic ansatz that reduces the HJB partial differential equation to a system of Riccati ordinary differential equations

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclearWe formulate continuous-time stochastic control problems capturing the Ethena trade-offs: permanent two-sided price impact... quadratic inventory risk penalty

Reference graph

Works this paper leans on

- [1]

-

[2]

What explains the stock market's reaction to F ederal R eserve policy?

Bernanke, Ben S and Kuttner, Kenneth N. What explains the stock market's reaction to F ederal R eserve policy?. J. Finance

-

[3]

Risk, uncertainty and monetary policy

Bekaert, Geert and Hoerova, Marie and Lo Duca, Marco. Risk, uncertainty and monetary policy. J. Monet. Econ

-

[4]

Are simple technical trading rules profitable in bitcoin markets?

Deprez, Niek and Fr \"o mmel, Michael. Are simple technical trading rules profitable in bitcoin markets?. Int. Rev. Econ. Finance

-

[5]

Market Volatility, Monetary Policy, and the Term Premium , author =. 2017 , institution =

work page 2017

-

[6]

Bernanke, Ben S. and Kuttner, Kenneth N. , journal =. What Explains the Stock Market's Reaction to. 2005 , doi =

work page 2005

-

[7]

Journal of Monetary Economics , volume =

Risk, Uncertainty and Monetary Policy , author =. Journal of Monetary Economics , volume =. 2013 , doi =

work page 2013

-

[8]

Kearney, Joseph D. and Lombra, Raymond E. , institution =. Monetary Policy and the. 2008 , note =

work page 2008

- [9]

-

[10]

The Effects of Monetary Policy on Asset Prices , journal =

G. The Effects of Monetary Policy on Asset Prices , journal =. 2005 , volume =

work page 2005

-

[11]

Bekaert, Geert and Hoerova, Maria , title =. Management Science , year =

-

[12]

Review of Financial Studies , year =

Liu, Yao and Zhang, Wei and Chen, Ming , title =. Review of Financial Studies , year =

-

[13]

Journal of Financial Markets , year =

Anderson, James and Kearney, Patrick and Lee, Sung , title =. Journal of Financial Markets , year =

-

[14]

John C. Cox AND Jonathan E. Ingersoll AND Jr. AND Stephen A. Ross , title =. Econometrica , volume =

-

[15]

Asia-Pacific Financial Markets , volume=

An interest rate model with upper and lower bounds , author=. Asia-Pacific Financial Markets , volume=. 2002 , publisher=

work page 2002

-

[16]

Mathematical Finance , volume =

Lorig, Matthew and Pagliarani, Stefano and Pascucci, Andrea , title =. Mathematical Finance , volume =. doi:https://doi.org/10.1111/mafi.12105 , url =

-

[17]

Ethena: A Synthetic Dollar Protocol , author =. 2024 , howpublished =

work page 2024

-

[18]

Optimal execution of portfolio transactions , author =. Journal of Risk , volume =

-

[19]

Continuous auctions and insider trading , author =. Econometrica , volume =

-

[20]

Journal of Financial Markets , volume =

Optimal control of execution costs , author =. Journal of Financial Markets , volume =

-

[21]

Algorithmic and High-Frequency Trading , author =

-

[22]

The Financial Mathematics of Market Liquidity , author =

-

[23]

Working Paper, Harvard University , year =

Dynamic portfolio selection in arbitrage , author =. Working Paper, Harvard University , year =

-

[24]

Journal of Financial Economics , volume =

Dynamic derivative strategies , author =. Journal of Financial Economics , volume =

-

[25]

SIAM Journal on Financial Mathematics , volume =

Decentralised Finance and Automated Market Making: Predictable Loss and Optimal Liquidity Provision , author =. SIAM Journal on Financial Mathematics , volume =

- [26]

- [27]

- [28]

-

[29]

and Soner, Halil Mete , publisher =

Fleming, Wendell H. and Soner, Halil Mete , publisher =. Controlled

-

[30]

Bernanke, Ben S. and Kuttner, Kenneth N. , journal =. What explains the stock market's reaction to

-

[31]

Journal of Monetary Economics , volume =

Risk, uncertainty, and monetary policy , author =. Journal of Monetary Economics , volume =

-

[32]

The effects of monetary policy on asset prices: An intraday event-study analysis , author =. Journal of Finance , volume =

-

[33]

Review of Financial Studies , volume =

Monetary policy uncertainty and cryptocurrency markets , author =. Review of Financial Studies , volume =

-

[34]

Quarterly Journal of Economics , volume =

High-frequency identification of monetary non-neutrality: The information effect , author =. Quarterly Journal of Economics , volume =

- [35]

- [36]

- [37]

-

[38]

2025 Annual Crypto Industry Report , author =. 2026 , howpublished =

work page 2025

- [39]

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.