Recognition: 2 theorem links

· Lean TheoremScenario generation of intraday electricity price paths for optimal trading in continuous markets

Pith reviewed 2026-05-14 18:31 UTC · model grok-4.3

The pith

A kernel-based regression model plus scenario generation from forecast errors and a new Support Vector Sorting step produces ensemble price trajectories that improve both statistical accuracy and trading profits over benchmarks on German intraday continuous market data.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Combining kernel-based learning with scenario driven uncertainty and adaptive updating provides a flexible and effective approach for forecasting and trading in continuous electricity markets.

Load-bearing premise

That forecast errors of fundamental variables can be used directly to generate scenarios whose statistical properties remain representative of future price uncertainty without additional calibration or regime detection.

Figures

read the original abstract

Continuous intraday electricity markets play an increasingly important role in short-term trading and balancing, yet decision-making under rapidly evolving price dynamics remains challenging. This paper proposes a comprehensive framework for ensemble forecasting of intraday electricity price trajectories and their translation into adaptive trading decisions. Building on a corrected Support Vector Regression model, the approach extends point predictions to probabilistic trajectory forecasts by introducing scenario generation based on forecast errors of fundamental variables and proposing a novel Support Vector Sorting procedure for the efficient selection of representative scenarios. The framework is evaluated using transaction level data from the German intraday continuous market. Empirical results show improvements over benchmark methods in both statistical and economic terms. Fundamental scenarios enhance median trajectory accuracy but produce more concentrated predictive distributions, while historical simulation with scenario selection better captures tail risk. From an economic perspective, ensemble-based forecasts outperform naive benchmarks across most of the trading strategies. Dynamic updating through scenario reweighting further improves profitability with limited impact on downside risk. Overall, the results demonstrate that combining kernel-based learning with scenario driven uncertainty and adaptive updating provides a flexible and effective approach for forecasting and trading in continuous electricity markets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a framework for ensemble forecasting of intraday electricity price trajectories in continuous markets. It starts from a corrected Support Vector Regression point forecast, extends it to probabilistic paths via scenario generation driven by forecast errors of fundamental variables, and introduces a Support Vector Sorting procedure to select a compact set of representative scenarios. The approach is tested on transaction-level data from the German intraday continuous market, with claims of statistical gains in median accuracy and economic gains in trading profitability relative to benchmarks; dynamic reweighting of scenarios is reported to further improve results with limited downside impact.

Significance. If the empirical claims hold after addressing the validation gaps, the work supplies a practical, kernel-based route to scenario-driven trading decisions in fast-moving electricity markets. The combination of SVR point forecasts with fundamental-error scenarios and an explicit selection step offers a reproducible template that could be adopted by market participants; the real-data evaluation and the reported economic outperformance are the primary sources of value.

major comments (3)

- [Abstract and §3] Abstract and §3 (scenario generation): the central premise that raw forecast errors of the chosen fundamentals remain distributionally representative of future price uncertainty is load-bearing yet untested for regime shifts; electricity prices exhibit spikes and mean-reversion changes only weakly linked to the fundamentals, so the generated ensembles may systematically understate tail risk without regime detection or recalibration.

- [§4] §4 (empirical evaluation): no quantitative error bars, bootstrap intervals, or out-of-sample calibration diagnostics are supplied for the reported improvements in median trajectory accuracy or trading profitability; without these, it is impossible to judge whether the gains over benchmarks are statistically distinguishable from sampling variation.

- [§3.2] §3.2 (Support Vector Sorting): the procedure re-uses the same training-period forecast-error distribution for scenario construction on held-out data, creating a modest circularity that is not quantified; the paper must demonstrate that the selected scenarios preserve tail properties out-of-sample rather than merely asserting economic value preservation.

minor comments (2)

- [§3.2] Notation for the Support Vector Sorting algorithm (Algorithm 1) should be aligned with standard SVR notation to avoid confusion between the sorting kernel and the original regression kernel.

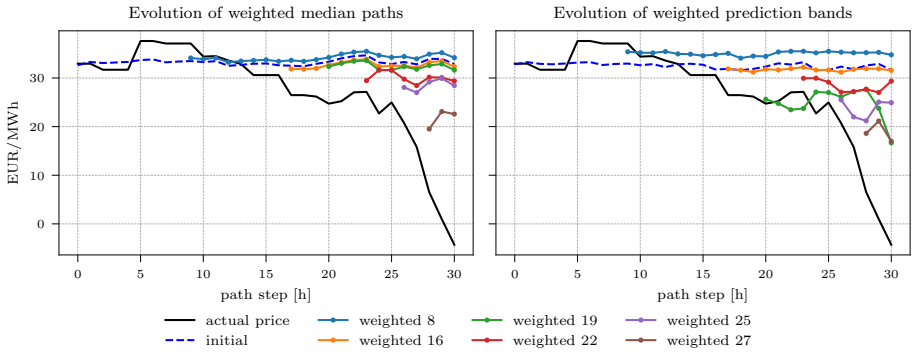

- [Figures] Figure 4 (or equivalent) comparing scenario distributions would benefit from explicit overlay of empirical quantiles to make the concentration of fundamental scenarios versus historical simulation visually clearer.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments. We address each major point below with clarifications and indicate revisions where the concerns can be directly addressed through additional analysis or discussion.

read point-by-point responses

-

Referee: [Abstract and §3] Abstract and §3 (scenario generation): the central premise that raw forecast errors of the chosen fundamentals remain distributionally representative of future price uncertainty is load-bearing yet untested for regime shifts; electricity prices exhibit spikes and mean-reversion changes only weakly linked to the fundamentals, so the generated ensembles may systematically understate tail risk without regime detection or recalibration.

Authors: We acknowledge that the distributional representativeness assumption is central to the scenario generation step. Our evaluation uses a multi-year German intraday dataset that includes multiple volatility regimes and price spikes, providing some empirical coverage of varying conditions. To directly address the concern, we will add a new subsection in the revised manuscript that splits the out-of-sample period by volatility quartiles and reports quantile coverage (including tails) separately for each sub-period. This will quantify any degradation in tail representation across regimes. revision: yes

-

Referee: [§4] §4 (empirical evaluation): no quantitative error bars, bootstrap intervals, or out-of-sample calibration diagnostics are supplied for the reported improvements in median trajectory accuracy or trading profitability; without these, it is impossible to judge whether the gains over benchmarks are statistically distinguishable from sampling variation.

Authors: We agree that statistical uncertainty measures are needed to substantiate the reported gains. In the revision we will add bootstrap confidence intervals (e.g., 1000 resamples) for all median accuracy and profitability metrics, together with out-of-sample calibration diagnostics such as reliability diagrams and PIT histograms for the ensemble forecasts. These additions will allow readers to assess whether improvements exceed sampling variation. revision: yes

-

Referee: [§3.2] §3.2 (Support Vector Sorting): the procedure re-uses the same training-period forecast-error distribution for scenario construction on held-out data, creating a modest circularity that is not quantified; the paper must demonstrate that the selected scenarios preserve tail properties out-of-sample rather than merely asserting economic value preservation.

Authors: The training-period error distribution is deliberately reused to avoid look-ahead bias when constructing scenarios for the test set; this is standard in scenario-generation literature. We will strengthen the presentation by adding explicit out-of-sample diagnostics: comparison of 95 % and 99 % quantile coverage and extreme-value statistics between the selected scenarios and realized prices on the held-out data. These results will be reported alongside the existing economic metrics. revision: yes

Axiom & Free-Parameter Ledger

free parameters (2)

- SVR hyperparameters (C, epsilon, kernel parameters)

- Number of scenarios retained after Support Vector Sorting

axioms (2)

- domain assumption Forecast errors of fundamental variables are stationary and can be sampled to represent price-path uncertainty

- ad hoc to paper The selected representative scenarios preserve the economic value of the full ensemble for trading decisions

invented entities (1)

-

Support Vector Sorting procedure

no independent evidence

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclearcorrected kernel K(xi,xj)=exp(−l∥xi−xj∥)exp(−g∥ŷi−ŷj∥²) … scenario generation based on forecast errors of fundamental variables … Support Vector Sorting … Wasserstein distance

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclearensemble path forecasting … fundamental scenarios … historical simulation

Reference graph

Works this paper leans on

-

[1]

doi: https://doi.org/10.1016/j.ijforecast.2014.08.013

ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2014.08.013. URLhttps: //www.sciencedirect.com/science/article/pii/S0169207014001423. Monica Borunda, Luis Conde-López, Gerardo Ruiz-Chavarría, Guadalupe Lopez Lopez, Victor M. Alvarado, and Edgardo de Jesús Carrera Avendaño. Advances in similar day methods for short-term load forecasting for power...

-

[2]

ISSN 2571-9394. doi: 10.3390/forecast8020032. URLhttps: //www.mdpi.com/2571-9394/8/2/32. Chih-Chung Chang and Chih-Jen Lin. Libsvm: A library for support vector machines.ACM Transactions on Intelligent Systems and Technology (TIST), 2(3),

-

[3]

ISSN 2157-6904. doi: 10.1145/1961189.1961199. URLhttps://doi.org/10.1145/1961189.1961199. Jieyu Chen, Sebastian Lerch, Melanie Schienle, Tomasz Serafin, and Rafał Weron. Probabilistic intraday electricity price forecasting using generative machine learning,

-

[4]

URLhttps://arxiv.org/abs/ 2506.00044. Harris Drucker, Christopher J. C. Burges, Linda Kaufman, Alex Smola, and Vladimir Vapnik. Support vector regression machines. In M.C. Mozer, M. Jordan, and T. Petsche, editors,Advances in Neural Information Processing Systems, volume

-

[5]

URLhttps://proceedings.neurips.cc/ paper_files/paper/1996/file/d38901788c533e8286cb6400b40b386d-Paper.pdf. ENTSO-E. Transparency platform knowledge base, 2026a. URLhttps://transparencyplatform. zendesk.com/hc/en-us/categories/12818231533716-Knowledge-base. Accessed: 2026-04-06. ENTSO-E. Transparency platform, 2026b. URLhttps://transparency.entsoe.eu/. Acc...

-

[6]

European Energy Exchange.https://www.epexspot.com

EPEX SPOT. European Energy Exchange.https://www.epexspot.com. Accessed: 2021-10-25. EPEX SPOT SE. Trading at EPEX SPOT – trading brochure.https://www.epexspot.com/sites/ default/files/download_center_files/20-01-24_TradingBrochure.pdf,

2021

-

[7]

doi: 10.1198/016214506000001437. URL https://doi.org/10.1198/016214506000001437. Holger Heitsch and Werner Römisch. Scenario reduction algorithms in stochastic programming.Com- putational Optimization and Applications, 24(2):187–206,

-

[8]

Random forests.Machine Learning, 45(1):5–32, 2001

ISSN 1573-2894. doi: 10.1023/A: 1021805924152. URLhttps://doi.org/10.1023/A:1021805924152. Simon Hirsch and Florian Ziel. Multivariate simulation-based forecasting for intraday power markets: Mod- eling cross-product price effects.Applied Stochastic Models in Business and Industry, 40(6):1571–1595, 2024a. doi: https://doi.org/10.1002/asmb.2837. URLhttps:/...

-

[9]

Tim Janke and Florian Steinke

Accessed: 2025-12-27. Tim Janke and Florian Steinke. Forecasting the price distribution of continuous intraday electricity trad- ing.Energies, 12(22),

2025

-

[10]

ISSN 1996-1073. doi: 10.3390/en12224262. URLhttps://www.mdpi.com/ 1996-1073/12/22/4262. Christopher Kath and Florian Ziel. The value of forecasts: Quantifying the economic gains of accurate quarter-hourly electricity price forecasts.Energy Economics, 76:411–423,

-

[11]

doi: 10.1016/j.eneco.2018.10.005

ISSN 0140-9883. doi: 10.1016/j.eneco.2018.10.005. URLhttp://dx.doi.org/10.1016/j.eneco.2018.10.005. Grzegorz Marcjasz, Tomasz Serafin, and Rafał Weron. Selection of calibration windows for day-ahead electricity price forecasting.Energies, 11(9),

-

[12]

ISSN 1996-1073. doi: 10.3390/en11092364. URL https://www.mdpi.com/1996-1073/11/9/2364. Grzegorz Marcjasz, Bartosz Uniejewski, and Rafał Weron. Beating the naïve—combining LASSO with naïve intraday electricity price forecasts.Energies, 13(7),

-

[13]

ISSN 1996-1073. doi: 10.3390/en13071667. URL https://www.mdpi.com/1996-1073/13/7/1667. Vivek Mohan, Jai Govind Singh, and Weerakorn Ongsakul. Sortino ratio based portfolio optimization considering EVs and renewable energy in microgrid power market.IEEE Transactions on Sustainable Energy, 8(1):219–229,

-

[14]

Rudy Morel, Stéphane Mallat, and Jean-Philippe Bouchaud

doi: 10.1109/TSTE.2016.2593713. Rudy Morel, Stéphane Mallat, and Jean-Philippe Bouchaud. Path shadowing Monte Carlo.Quantitative Finance, 24(9):1199–1225,

-

[15]

URLhttps://doi.org/10.1080/ 14697688.2024.2399285

doi: 10.1080/14697688.2024.2399285. URLhttps://doi.org/10.1080/ 14697688.2024.2399285. Michał Narajewski and Florian Ziel. Econometric modelling and forecasting of intraday electricity prices. Journal of Commodity Markets, 19:100107, 2020a. ISSN 2405-8513. doi: https://doi.org/10.1016/j.jcomm. 2019.100107. URLhttps://www.sciencedirect.com/science/article/...

-

[16]

doi: https://doi.org/10.1016/j.apenergy.2024.124975. JakubNowotarskiandRafałWeron. Recentadvancesinelectricitypriceforecasting: Areviewofprobabilistic forecasting.Renewable and Sustainable Energy Reviews, 81:1548–1568,

-

[17]

doi: https://doi.org/10.1016/j.rser.2017.05.234

ISSN 1364-0321. doi: https://doi.org/10.1016/j.rser.2017.05.234. URLhttps://www.sciencedirect.com/science/article/ pii/S1364032117308808. F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duch- esnay. Scikit-le...

-

[18]

doi: https://doi.org/10.1016/j.ijforecast.2025.11.007

ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2025.11.007. URLhttps://www.sciencedirect.com/science/ article/pii/S0169207025001098. 25 Jesse Read, Bernhard Pfahringer, Geoff Holmes, and Eibe Frank. Classifier chains for multi-label classifi- cation. In Wray Buntine, Marko Grobelnik, Dunja Mladenić, and John Shawe-Taylor, editors,Machine Learni...

-

[19]

URLhttps://arxiv.org/ abs/2510.15011. arXiv preprint. Tomasz Serafin, Grzegorz Marcjasz, and Rafał Weron. Trading on short-term path forecasts of intraday elec- tricity prices.Energy Economics, 112:106125,

-

[20]

doi: https://doi.org/10.1016/j.eneco

ISSN 0140-9883. doi: https://doi.org/10.1016/j.eneco. 2022.106125. URLhttps://www.sciencedirect.com/science/article/pii/S014098832200281X. Anna Staszewska. Representing uncertainty about response paths: The use of heuristic optimisation methods.Computational Statistics&Data Analysis, 52(1):121–132,

-

[21]

doi: https://doi.org/10.1016/j.csda.2006.12.023

ISSN 0167-9473. doi: https://doi.org/10.1016/j.csda.2006.12.023. URLhttps://www.sciencedirect.com/science/article/ pii/S0167947306005007. Mucun Sun, Cong Feng, and Jie Zhang. Probabilistic solar power forecasting based on weather scenario generation.Applied Energy, 266:114823,

-

[22]

doi: https://doi.org/10.1016/j.apenergy

ISSN 0306-2619. doi: https://doi.org/10.1016/j.apenergy. 2020.114823. URLhttps://www.sciencedirect.com/science/article/pii/S0306261920303354. Léonard Tschora, Erwan Pierre, Marc Plantevit, and Céline Robardet. Electricity price forecasting on the day-ahead market using machine learning.Applied Energy, 313:118752,

-

[23]

doi: https: //doi.org/10.1016/j.apenergy.2022.118752

ISSN 0306-2619. doi: https: //doi.org/10.1016/j.apenergy.2022.118752. URLhttps://www.sciencedirect.com/science/article/ pii/S0306261922002057. Bartosz Uniejewski and Florian Ziel. Probabilistic forecasts of load, solar and wind for electricity price forecasting. arXiv preprint,

-

[24]

Bartosz Uniejewski, Grzegorz Marcjasz, and Rafał Weron

URLhttps://arxiv.org/abs/2501.06180. Bartosz Uniejewski, Grzegorz Marcjasz, and Rafał Weron. Understanding intraday electricity markets: Variable selection and very short-term price forecasting using LASSO.International Journal of Forecast- ing, 35(4):1533–1547,

-

[25]

doi: https://doi.org/10.1016/j.ijforecast.2019.02.001

ISSN 0169-2070. doi: https://doi.org/10.1016/j.ijforecast.2019.02.001. URL https://www.sciencedirect.com/science/article/pii/S0169207019300123. Cédric Villani.Optimal Transport: Old and New, volume 338 ofGrundlehren der Mathematischen Wissenschaften. Springer-Verlag, Berlin, Heidelberg,

-

[26]

OrderFusion: Encoding Orderbook for End-to-End Probabilistic Intraday Electricity Price Forecasting

URLhttps://arxiv.org/abs/2502.06830. Appendix A. Additional figures 26 −10 −5 0 5 10 load [GW] −5.0 −2.5 0.0 2.5 5.0 solar [GW] 1 2 3 4 5 6 7 8 9 10 11 h −10 −5 0 5 10 wind [GW] 100 101 102 103 104 # (log scale) Figure A.5: Colormap representing the histograms of fundamental scenarios∆(i) fs for each quarter-hourly step in a path. Note that, due to differ...

work page internal anchor Pith review Pith/arXiv arXiv 2000

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.