Synthetic American Option Pricing via Jump-HMM-Driven Heston Implied Volatility

Pith reviewed 2026-05-15 02:25 UTC · model grok-4.3

The pith

A structural equity model generates implied volatility surfaces to price synthetic American options without market calibration.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Implied volatility emerges as an output of a structural model of equity returns rather than as an input derived from observed option prices. A Jump Hidden Markov Model produces multi-asset price paths; a modified Heston variance process whose mean-reversion target depends on regime state, days to expiration, moneyness, and a market-mood indicator converts those paths into implied-volatility surfaces; and a recombining binomial lattice prices American options from the resulting surface. Initializing variance at its mean-reversion target for each strike-expiration pair lets the volatility smile and term structure form without external calibration.

What carries the argument

The modified Heston variance process whose mean-reversion target depends on regime, expiration, moneyness, and market-mood indicator, initialized at that target and driven by Jump Hidden Markov Model equity paths, then priced on a recombining binomial lattice.

If this is right

- Synthetic American option prices, finite-difference Greeks, and terminal short-premium P&L can be recovered from one coherent simulation of equity paths.

- Calibration via a hierarchy of parametric baseline, globally shared neural surrogate, and sector-specific neural surrogate allows adaptation while preserving cross-ticker robustness.

- Calendar-derived earnings-distance and same-sector peer-coupling features recover the anticipatory component of scheduled-event effects on generalization error.

- The same pipeline can be re-run on underlyings from different sectors and volatility regimes to confirm consistency of generated surfaces and Greeks.

- An open-source Julia implementation makes the full pipeline available for generating large volumes of consistent synthetic option data.

Where Pith is reading between the lines

- Large-scale machine-learning models for option pricing or risk management could be trained on internally consistent synthetic datasets without circularity artifacts.

- Extending the regime and mood indicators to include macroeconomic variables might improve performance during crisis periods not represented in the original calibration.

- Because the lattice prices American options directly, the framework could be used to study early-exercise boundaries under realistic stochastic volatility without separate numerical solvers.

Load-bearing premise

The modified Heston variance process with regime-, expiration-, moneyness-, and mood-dependent mean-reversion target, when initialized at that target, produces realistic implied volatility surfaces that generalize beyond the calibration data.

What would settle it

Generate implied-volatility surfaces from the model on a hold-out period containing unscheduled events and check whether the surfaces deviate systematically from observed market surfaces in skew, term structure, or level.

Figures

read the original abstract

Generating realistic synthetic option prices requires implied volatility as an input, yet implied volatility is itself derived from observed option prices, creating a circular dependency that limits synthetic data for machine-learning and risk-analysis applications. We break this circularity with a pipeline in which implied volatility emerges as an output of a structural model of equity returns. A Jump Hidden Markov Model produces multi-asset price paths with realistic stylized facts and cross-asset tail dependence; a modified Heston variance process, whose mean-reversion target depends on regime state, days to expiration, moneyness, and a market-mood indicator, converts those paths into implied-volatility paths; and a recombining binomial lattice prices American options from the resulting surface. Initializing variance at its mean-reversion target for each strike-expiration pair lets smile, skew, and term structure emerge without external calibration. We calibrate the shape function through a hierarchy spanning a parametric baseline, a globally shared neural surrogate, and a sector-specific neural surrogate fit to a multi-ticker, multi-sector option ladder. A temporal holdout on a multi-day capture isolated scheduled corporate events as the dominant source of test-time generalization error, and calendar-derived earnings-distance and same-sector peer-coupling features recovered the anticipatory portion of that signal. We then apply the framework as a synthetic-data generator on real near-the-money put and call contracts, forward-simulating price paths, and recovering path-conditional implied volatility, finite-difference American Greeks, and terminal short-premium profit and loss from one coherent simulation, and confirm cross-ticker robustness by re-running on a second underlying from a different sector and volatility regime. The framework is released as an open-source Julia package.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a pipeline for generating synthetic American option prices that aims to break the circularity between observed option prices and implied volatility. It uses a Jump Hidden Markov Model to generate multi-asset price paths, a modified Heston variance process with mean-reversion targets depending on regime, expiration, moneyness, and mood (initialized at the target), and a recombining binomial lattice for pricing. The shape function for the mean-reversion target is calibrated using neural network surrogates fit to real option data from multiple tickers, with a temporal holdout validation. The framework is implemented as an open-source Julia package.

Significance. If the model consistency can be established, this work could provide a valuable tool for generating synthetic data for machine learning applications in quantitative finance, particularly for American options. The open-source release and cross-ticker robustness testing are positive aspects. The approach attempts to derive implied volatility structurally from equity return models rather than directly from market data.

major comments (3)

- [Modified Heston variance process] The mean-reversion target theta in the modified Heston variance process is specified as a function of moneyness. This implies that each strike has a different long-run variance level. No single Itô process for the variance can produce this, so the resulting implied volatility surface is not the marginal distribution implied by any arbitrage-free model of the underlying asset. This is load-bearing for the claim that the surfaces emerge structurally from the equity-return paths.

- [Calibration hierarchy] The abstract states that smile, skew, and term structure emerge 'without external calibration', yet the shape function is calibrated via neural surrogates to real multi-ticker option data. This appears contradictory and requires clarification on what aspects are calibrated versus emergent.

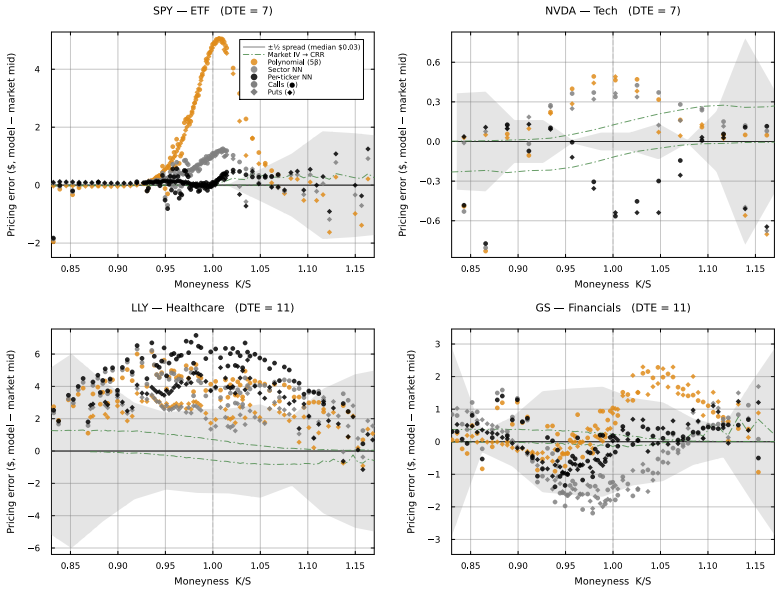

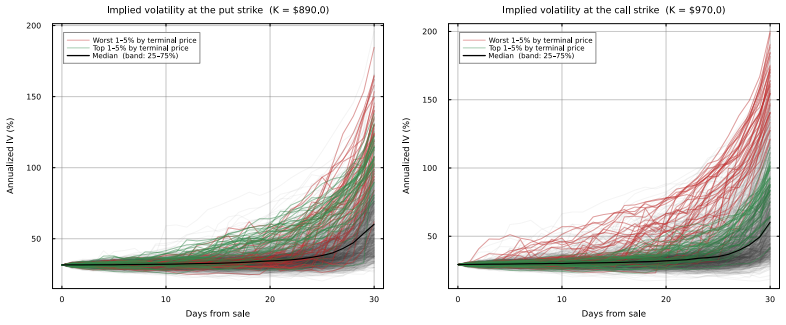

- [Validation experiments] The temporal holdout experiment is described, but no quantitative error metrics (such as RMSE on implied vols or option prices) or checks for no-arbitrage violations (e.g., butterfly positivity, calendar monotonicity) are provided. This makes it difficult to assess whether the generated surfaces are usable for pricing.

minor comments (2)

- [Abstract] The abstract is dense with technical details; consider breaking it into clearer sentences or adding a short overview paragraph.

- [Software release] The manuscript should include a direct link or repository identifier for the open-source Julia package to facilitate reproducibility.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments, which help clarify key aspects of our framework. We address each major comment below with clarifications and proposed revisions where appropriate.

read point-by-point responses

-

Referee: [Modified Heston variance process] The mean-reversion target theta in the modified Heston variance process is specified as a function of moneyness. This implies that each strike has a different long-run variance level. No single Itô process for the variance can produce this, so the resulting implied volatility surface is not the marginal distribution implied by any arbitrage-free model of the underlying asset. This is load-bearing for the claim that the surfaces emerge structurally from the equity-return paths.

Authors: We acknowledge this modeling choice creates strike-dependent variance dynamics rather than a single Itô process. The modification to theta (depending on regime, expiration, moneyness, and mood) is deliberate to let the IV surface emerge from the Jump-HMM equity paths while capturing observed stylized facts. The structural claim rests on generating paths first and then mapping to IV via this process, not on claiming a unified arbitrage-free SDE for the underlying across all strikes. We will add explicit discussion of this approximation and its limitations in a new subsection on model consistency, without altering the core pipeline. revision: partial

-

Referee: [Calibration hierarchy] The abstract states that smile, skew, and term structure emerge 'without external calibration', yet the shape function is calibrated via neural surrogates to real multi-ticker option data. This appears contradictory and requires clarification on what aspects are calibrated versus emergent.

Authors: The phrase 'without external calibration' refers specifically to the per-simulation generation step: once the shape function has been fit once via the hierarchy (parametric baseline to sector-specific neural surrogate) on historical data, new IV surfaces emerge directly from fresh equity paths without refitting to option prices. The calibration is a fixed preprocessing step, not repeated for each synthetic surface. We agree the abstract wording is imprecise and will revise it, the introduction, and the methods section to distinguish pre-calibration of the shape function from the emergent path-driven IV generation. revision: yes

-

Referee: [Validation experiments] The temporal holdout experiment is described, but no quantitative error metrics (such as RMSE on implied vols or option prices) or checks for no-arbitrage violations (e.g., butterfly positivity, calendar monotonicity) are provided. This makes it difficult to assess whether the generated surfaces are usable for pricing.

Authors: We agree that quantitative metrics and arbitrage checks are necessary for evaluating usability. In the revised manuscript we will add RMSE values for both implied volatilities and American option prices on the temporal holdout set. We will also report diagnostics for no-arbitrage conditions, including butterfly spread positivity and calendar-spread monotonicity, computed on the generated surfaces. These results will be included in the validation experiments section. revision: yes

Circularity Check

Moneyness-dependent mean-reversion target calibrated to real option ladders, so IV surface is fitted construction rather than structural emergence

specific steps

-

fitted input called prediction

[Abstract]

"Initializing variance at its mean-reversion target for each strike-expiration pair lets smile, skew, and term structure emerge without external calibration. We calibrate the shape function through a hierarchy spanning a parametric baseline, a globally shared neural surrogate, and a sector-specific neural surrogate fit to a multi-ticker, multi-sector option ladder."

The mean-reversion target is defined via the shape function that is fitted directly to real option data; initializing variance at this target therefore constructs the IV surface by the calibration rather than deriving it from the Jump-HMM paths or a single consistent variance process. The claim of emergence 'without external calibration' is immediately followed by the calibration step that supplies the target, making the output statistically forced by the fitted inputs.

full rationale

The paper claims to break the IV circularity by letting implied volatility emerge from Jump-HMM equity paths through a modified Heston process. However, the mean-reversion target theta is explicitly a calibrated shape function of regime, expiration, moneyness and mood; variance is initialized at this target for each strike-expiration pair. The shape function itself is obtained by fitting parametric and neural surrogates to multi-ticker observed option ladders. Consequently the generated surfaces and the American prices derived from them are produced by construction from the calibration step rather than from unmodified dynamics of the underlying. The temporal-holdout experiment only tests generalization of the fitted shape, not independent structural derivation. This matches the fitted-input-called-prediction pattern and yields partial circularity on the central claim.

Axiom & Free-Parameter Ledger

free parameters (2)

- neural surrogate weights

- regime-dependent mean-reversion targets

axioms (2)

- domain assumption Equity returns follow a Jump Hidden Markov Model that reproduces stylized facts and cross-asset tail dependence.

- domain assumption Modified Heston process with state-dependent mean-reversion target produces realistic implied volatility when initialized at that target.

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

modified Heston variance process whose mean-reversion target depended on regime state, days to expiration, moneyness, and an aggregate market mood indicator

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

ψ(τ,m)=exp(β1 lnτ+β2 lnm+...); neural surrogate ψNN

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

The Review of Financial Studies , volume=

A closed-form solution for options with stochastic volatility with applications to bond and currency options , author=. The Review of Financial Studies , volume=. 1993 , publisher=

work page 1993

-

[2]

Journal of Financial Economics , volume=

Option pricing: A simplified approach , author=. Journal of Financial Economics , volume=. 1979 , publisher=

work page 1979

-

[3]

arXiv preprint arXiv:2603.10202 , year=

Hybrid Hidden Markov Model for Modeling Equity Excess Growth Rate Dynamics: A Discrete-State Approach with Jump-Diffusion , author=. arXiv preprint arXiv:2603.10202 , year=

-

[4]

Simple and efficient simulation of the

Andersen, Leif , journal=. Simple and efficient simulation of the. 2008 , doi=

work page 2008

-

[5]

A parsimonious arbitrage-free implied volatility parameterization with application to the valuation of volatility derivatives , author=

-

[6]

Journal of Political Economy , volume=

The pricing of options and corporate liabilities , author=. Journal of Political Economy , volume=. 1973 , publisher=

work page 1973

-

[7]

Quantitative Finance , volume=

Empirical properties of asset returns: stylized facts and statistical issues , author=. Quantitative Finance , volume=. 2001 , publisher=

work page 2001

- [8]

- [9]

- [10]

-

[11]

International Statistical Review , volume=

The t copula and related copulas , author=. International Statistical Review , volume=. 2005 , publisher=

work page 2005

-

[12]

Quantitative Finance , volume=

Deep hedging , author=. Quantitative Finance , volume=. 2019 , publisher=

work page 2019

-

[13]

Quantitative Finance , volume=

Dynamics of implied volatility surfaces , author=. Quantitative Finance , volume=. 2002 , publisher=

work page 2002

-

[14]

Quantitative Finance , volume=

Deep learning volatility: a deep neural network perspective on pricing and calibration in (rough) volatility models , author=. Quantitative Finance , volume=. 2021 , publisher=

work page 2021

-

[15]

Deep calibration of rough stochastic volatility models

Deep calibration of rough stochastic volatility models , author=. arXiv preprint arXiv:1810.03399 , year=

work page internal anchor Pith review Pith/arXiv arXiv

-

[16]

Journal of Financial Economics , volume=

Approximate option valuation for arbitrary stochastic processes , author=. Journal of Financial Economics , volume=. 1982 , publisher=

work page 1982

-

[17]

Journal of Futures Markets , volume=

A modified lattice approach to option pricing , author=. Journal of Futures Markets , volume=. 1993 , publisher=

work page 1993

-

[18]

Applied Mathematical Finance , volume=

Binomial models for option valuation--examining and improving convergence , author=. Applied Mathematical Finance , volume=. 1996 , publisher=

work page 1996

-

[19]

Wiese, Magnus and Knobloch, Robert and Korn, Ralf and Kretschmer, Peter , journal=. Quant. 2020 , publisher=

work page 2020

-

[20]

Monte Carlo Methods in Financial Engineering , author=. 2004 , publisher=

work page 2004

-

[21]

Review of Financial Studies , volume=

American option valuation: New bounds, approximations, and a comparison of existing methods , author=. Review of Financial Studies , volume=. 1996 , publisher=

work page 1996

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.