Recognition: no theorem link

Partial Identification of the Valuation Distribution in Sequential English Auctions

Pith reviewed 2026-05-15 01:53 UTC · model grok-4.3

The pith

Sequential English auctions allow partial identification of bidder valuations through dynamic opportunity-cost restrictions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

In sequential English auctions, the distribution of private valuations is partially identified by imposing a dynamic opportunity-cost restriction: bidders do not permit rivals to win at prices below the value of participating in subsequent auctions. This restriction generates nonparametric bounds on valuations that are sharp, and these bounds can be estimated by inverting moment conditions that pool information across auctions with different numbers of participants.

What carries the argument

Dynamic opportunity-cost restriction on bidder behavior, which replaces the static no-regret condition and generates valuation bounds by incorporating the value of future auction participation.

If this is right

- The option to wait for future auctions reduces revenue in the first period by 8 to 11 percent in the Korean wholesale used-car market.

- Increasing the number of serious bidders from 8 to 20 in online auctions like Cars and Bids can raise seller revenue by 40 to 65 percent.

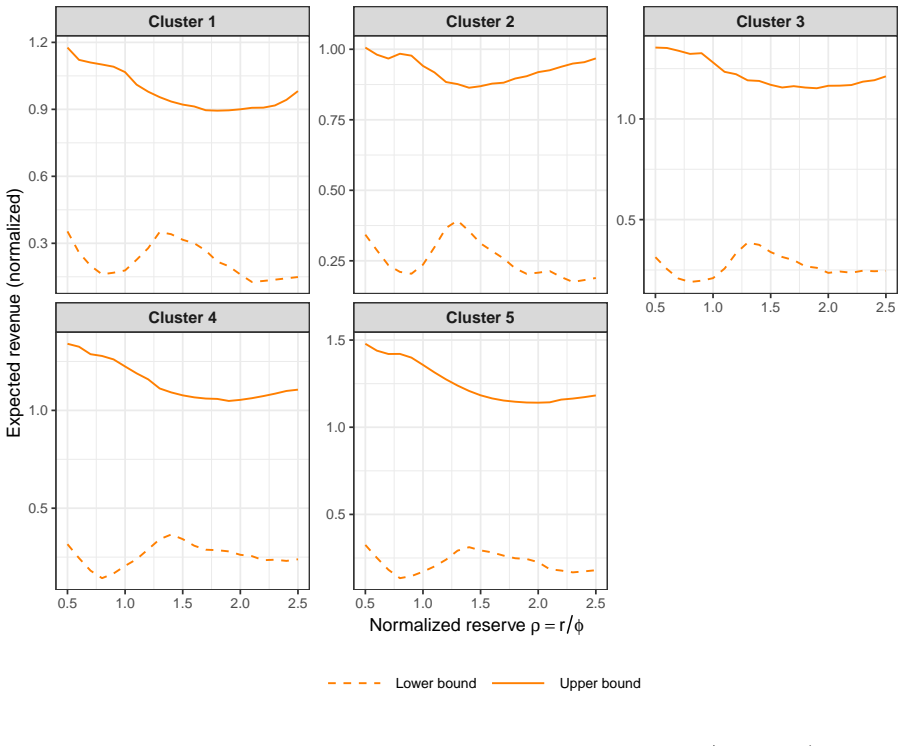

- Optimal reserve prices that maximize the minimum possible revenue differ substantially across different vehicle types.

- Sharp bounds on the valuation distribution are attainable without solving for equilibrium bidding strategies in the dynamic game.

Where Pith is reading between the lines

- These identification results could inform the design of multi-period auction mechanisms to reduce the revenue loss from bidder waiting.

- The pooling estimator might be adapted for other settings with heterogeneous group sizes, such as in labor market or procurement data.

- Future work could test whether relaxing the opportunity-cost assumption further changes the bounds in markets with high uncertainty about future supply.

Load-bearing premise

Bidders satisfy the dynamic opportunity-cost restriction by not allowing rivals to win at prices below their opportunity cost of waiting for future auctions.

What would settle it

Observing a bidder allowing a rival to win at a price that exceeds the bidder's calculated opportunity cost from future auction outcomes would contradict the restriction and falsify the bounds.

Figures

read the original abstract

This paper extends the incomplete model of Haile and Tamer (2003) from static English auctions to sequential English auctions. Because bidders may wait for future opportunities, the static condition that bidders do not let rivals win at beatable prices need not hold. We replace it with a dynamic opportunity-cost restriction, yielding nonparametric valuation bounds without solving a dynamic equilibrium. Sharp bounds are also characterized. We propose a novel moment-condition inversion estimator that pools auctions with heterogeneous bidder counts, mitigating finite-sample instability of order statistics approaches and admitting analytical standard errors and smooth confidence intervals. Applications to Korean wholesale used-car auctions and Cars and Bids online auctions deliver informative bounds. Counterfactual analyses show that the option to wait lowers first-period revenue by 8--11% in the Korean market, that increasing effective competition from 8 to 20 serious bidders in Cars and Bids raises seller revenue by 40--65%, and that maximin reserve prices vary substantially across vehicle clusters.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper extends the incomplete-model framework of Haile and Tamer (2003) from static to sequential English auctions. It replaces the static “no letting rivals win at beatable prices” condition with a dynamic opportunity-cost restriction under which bidders do not allow rivals to win below the value of waiting for future auctions. This restriction is claimed to deliver nonparametric bounds on the valuation distribution F without solving a dynamic equilibrium; sharp bounds are characterized. A moment-condition inversion estimator is proposed that pools auctions with heterogeneous bidder counts, yields analytical standard errors, and is applied to Korean wholesale used-car data and Cars and Bids online auctions. Counterfactuals quantify revenue losses from the option to wait (8–11 percent) and gains from increased competition.

Significance. If the dynamic restriction can be shown to produce closed-form bounds independent of the unknown F, the paper would constitute a useful methodological advance for sequential auction settings that are common in practice. The estimator’s ability to pool across varying n and deliver smooth confidence intervals addresses a practical limitation of order-statistic approaches. The empirical applications deliver economically interpretable bounds and counterfactuals on reserve prices and competition effects. The manuscript receives credit for avoiding explicit equilibrium computation while still characterizing sharpness.

major comments (2)

- [§3.2] §3.2 (Dynamic opportunity-cost restriction): The central claim that the restriction yields nonparametric bounds “without solving a dynamic equilibrium” requires an explicit representation showing that the opportunity cost of waiting can be bounded using only observables (order statistics or exogenous variation in n) rather than continuation values that themselves depend on F. If opportunity cost equals the expected payoff from future auctions, the inequalities become a joint system in F; the manuscript must demonstrate that this fixed-point problem is avoided.

- [§5] §5 (Moment-condition inversion estimator): The estimator pools auctions with heterogeneous bidder counts via moment conditions derived from the dynamic restriction. The paper should verify that these moments remain valid and identifying when n varies across auctions and should report Monte Carlo evidence on finite-sample coverage of the analytical standard errors, especially for the lower and upper bounds on F.

minor comments (2)

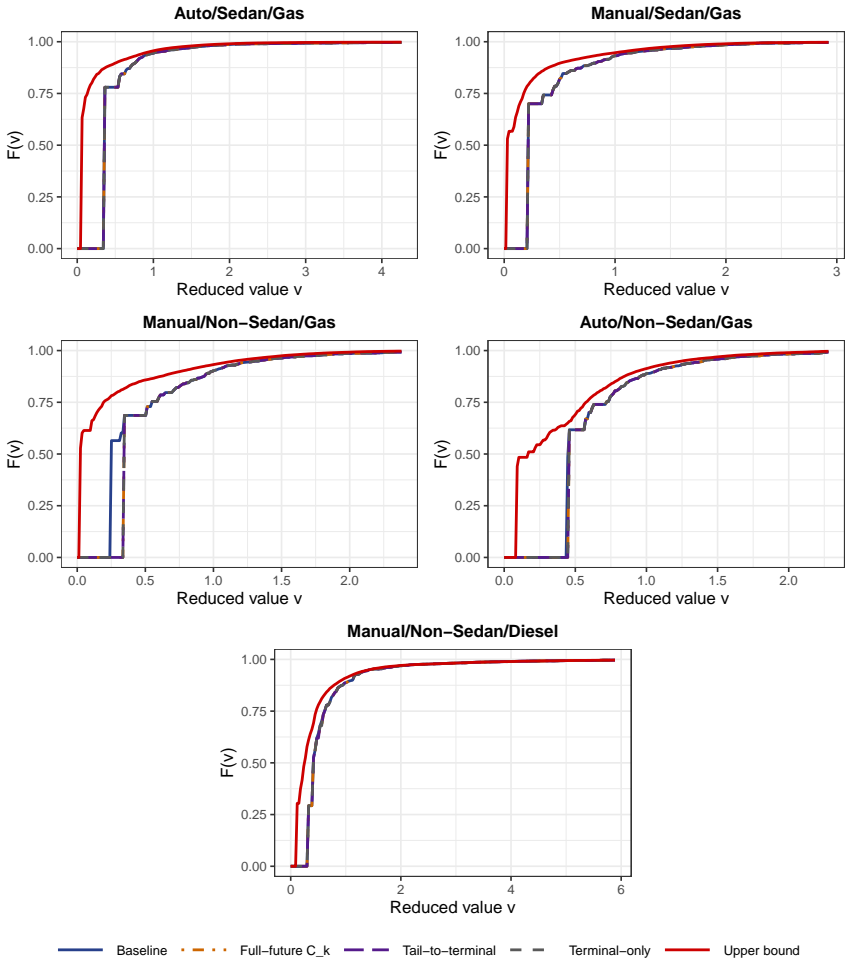

- [Table 1, Figure 2] Table 1 and Figure 2: axis labels and legends should explicitly state whether the plotted objects are bounds on the cdf or on quantiles, and whether they incorporate the dynamic restriction.

- [§6.2] §6.2 (Counterfactuals): the 8–11 percent revenue reduction attributed to the waiting option should be accompanied by a sensitivity check that varies the assumed discount factor or continuation-value functional form.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. The comments highlight important points for clarification and additional verification. We address each major comment below and indicate the planned revisions to the manuscript.

read point-by-point responses

-

Referee: [§3.2] §3.2 (Dynamic opportunity-cost restriction): The central claim that the restriction yields nonparametric bounds “without solving a dynamic equilibrium” requires an explicit representation showing that the opportunity cost of waiting can be bounded using only observables (order statistics or exogenous variation in n) rather than continuation values that themselves depend on F. If opportunity cost equals the expected payoff from future auctions, the inequalities become a joint system in F; the manuscript must demonstrate that this fixed-point problem is avoided.

Authors: We agree that an explicit representation is needed to clarify how the fixed-point problem is avoided. In the model, the dynamic opportunity-cost restriction is an inequality: a bidder does not let a rival win at a price below the value of waiting, where the opportunity cost is bounded above by the expected maximum surplus obtainable from future auctions. This upper bound is expressed solely in terms of observable order statistics (e.g., the expected second-highest bid in subsequent periods) and exogenous variation in the number of bidders n, without requiring the continuation value to be computed as a function of the unknown F. Because the restriction enters as an inequality rather than an equality, the resulting bounds on F are obtained directly from the observed bid distributions via a system of inequalities that does not involve iteration or fixed-point computation. We will add a new subsection in the revised §3.2 that derives this representation step by step, showing the bounding argument and confirming that no equilibrium continuation values depending on F are required. revision: yes

-

Referee: [§5] §5 (Moment-condition inversion estimator): The estimator pools auctions with heterogeneous bidder counts via moment conditions derived from the dynamic restriction. The paper should verify that these moments remain valid and identifying when n varies across auctions and should report Monte Carlo evidence on finite-sample coverage of the analytical standard errors, especially for the lower and upper bounds on F.

Authors: We agree that explicit verification of validity under heterogeneous n and finite-sample properties of the standard errors would strengthen the paper. The moment conditions are derived from the dynamic restriction under the maintained assumption that the valuation distribution F is common across auctions; pooling is justified because the moments are linear in the empirical distribution of bids and remain valid for any fixed n as long as the support and monotonicity conditions hold uniformly. Identification is preserved because the variation in n across auctions provides additional identifying power for the bounds without introducing bias. To address the finite-sample coverage, we will add a Monte Carlo section in the revised §5 that reports coverage probabilities of the analytical standard errors for both the lower and upper bounds on F under designs with varying n, different sample sizes, and heterogeneous bidder counts. revision: yes

Circularity Check

No significant circularity: bounds follow from independent behavioral restriction without fixed-point reduction

full rationale

The paper replaces the static Haile-Tamer condition with a new dynamic opportunity-cost restriction on bidder behavior. This restriction is introduced as a primitive assumption that directly yields nonparametric valuation bounds without requiring solution of a dynamic equilibrium or joint fixed point in the unknown distribution F. No equations in the provided text reduce the bounds to fitted parameters, self-referential definitions, or a self-citation chain that itself depends on the target result. The moment-condition inversion estimator pools data under the maintained restriction but does not rename or invert fitted inputs as predictions. The derivation chain is therefore self-contained against the stated behavioral assumption and external benchmarks such as the original Haile-Tamer model.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Bidders obey the dynamic opportunity-cost restriction in sequential English auctions

Reference graph

Works this paper leans on

-

[1]

Nonparametric Estimation of Sponsored Search Auctions and Impact of Ad Quality on Search Revenue , author=. Management Science , volume=. 2025 , doi=

work page 2025

-

[2]

Annales d'Economie et de Statistique , pages=

First-price sealed-bid auctions with secret reservation prices , author=. Annales d'Economie et de Statistique , pages=. 1994 , publisher=

work page 1994

-

[3]

Generalized instrumental variable models , author=. Econometrica , volume=. 2017 , publisher=

work page 2017

-

[4]

The American Economic Review , volume=

Optimal auctions , author=. The American Economic Review , volume=. 1981 , publisher=

work page 1981

-

[5]

Theoretical Economics , volume=

Loss aversion in sequential auctions , author=. Theoretical Economics , volume=. 2023 , publisher=

work page 2023

-

[6]

Equilibrium price paths in sequential auctions with stochastic supply , author=. Economics Letters , volume=. 1999 , publisher=

work page 1999

-

[7]

New evidence on price anomalies in sequential auctions: Used cars in

Raviv, Yaron , journal=. New evidence on price anomalies in sequential auctions: Used cars in. 2006 , publisher=

work page 2006

-

[8]

Journal of Economic Theory , volume=

Sequential auctions with ambiguity , author=. Journal of Economic Theory , volume=. 2021 , publisher=

work page 2021

-

[9]

The RAND Journal of Economics , pages=

Declining values and the afternoon effect: Evidence from art auctions , author=. The RAND Journal of Economics , pages=. 1997 , publisher=

work page 1997

-

[10]

Models for competitive bidding under uncertainty , author=. 1968 , publisher=

work page 1968

-

[11]

Journal of Economic Literature , volume=

Auctions and the price of art , author=. Journal of Economic Literature , volume=. 2003 , publisher=

work page 2003

-

[12]

Identification and estimation in sequential, asymmetric,

Brendstrup, Bjarne and Paarsch, Harry J , journal=. Identification and estimation in sequential, asymmetric,. 2006 , publisher=

work page 2006

-

[13]

Non-parametric estimation of sequential

Brendstrup, Bjarne , journal=. Non-parametric estimation of sequential. 2007 , publisher=

work page 2007

-

[14]

Journal of Economic Theory , volume=

Equilibrium reserve prices in sequential ascending auctions , author=. Journal of Economic Theory , volume=. 2004 , publisher=

work page 2004

-

[15]

Estimation of a dynamic auction game , author=. Econometrica , volume=. 2003 , publisher=

work page 2003

-

[16]

The BE Journal of Theoretical Economics , volume=

Sequential auctions with decreasing reserve prices , author=. The BE Journal of Theoretical Economics , volume=. 2018 , publisher=

work page 2018

-

[17]

The Review of Economic Studies , volume=

Multiple-object auctions with budget constrained bidders , author=. The Review of Economic Studies , volume=. 2001 , publisher=

work page 2001

-

[18]

Sequential auctions of heterogeneous objects , author=. Economics Letters , volume=. 2016 , publisher=

work page 2016

-

[19]

Journal of Applied Econometrics , volume=

An empirical model of the multi-unit, sequential, clock auction , author=. Journal of Applied Econometrics , volume=. 2006 , publisher=

work page 2006

-

[20]

Identification and estimation of sequential

Lamy, Laurent , year=. Identification and estimation of sequential

-

[21]

RAND Journal of Economics , volume=

Implementing optimal outcomes through sequential auctions , author=. RAND Journal of Economics , volume=. 2022 , publisher=

work page 2022

-

[22]

Journal of Political Economy , volume=

Sequential auctions with synergy and affiliation across auctions , author=. Journal of Political Economy , volume=. 2021 , publisher=

work page 2021

-

[23]

Optimal nonparametric estimation of first-price auctions , author=. Econometrica , volume=. 2000 , publisher=

work page 2000

-

[24]

The importance of ordering in sequential auctions , author=. Management Science , volume=. 2003 , publisher=

work page 2003

-

[25]

International Journal of Game Theory , volume=

Declining valuations in sequential auctions , author=. International Journal of Game Theory , volume=. 2004 , publisher=

work page 2004

-

[26]

Inference with an incomplete model of

Haile, Philip A and Tamer, Elie , journal=. Inference with an incomplete model of. 2003 , publisher=

work page 2003

-

[27]

Journal of Economic Perspectives , volume=

How auctions work for wine and art , author=. Journal of Economic Perspectives , volume=

-

[28]

Nonparametric estimation and testing of the symmetric

Kim, Kyoo il and Lee, Joonsuk , year=. Nonparametric estimation and testing of the symmetric

-

[29]

Review of Industrial Organization , pages=

Last-minute bidding in sequential auctions with unobserved, stochastic entry , author=. Review of Industrial Organization , pages=. 2012 , publisher=

work page 2012

-

[30]

Identification of standard auction models , author=. Econometrica , volume=. 2002 , publisher=

work page 2002

-

[31]

Journal of Econometrics , volume=

Estimating first-price auctions with an unknown number of bidders: A misclassification approach , author=. Journal of Econometrics , volume=. 2010 , publisher=

work page 2010

-

[32]

A theory of auctions and competitive bidding , author=. Econometrica , volume=. 1982 , publisher=

work page 1982

-

[33]

Auctions, Bidding, and Contracting: Uses and Theory , editor=

Multiple-object auctions , author=. Auctions, Bidding, and Contracting: Uses and Theory , editor=. 1983 , publisher=

work page 1983

-

[34]

Journal of Economic Theory , volume=

The declining price anomaly , author=. Journal of Economic Theory , volume=. 1993 , publisher=

work page 1993

-

[35]

The American Economic Review , volume=

A note on sequential auctions , author=. The American Economic Review , volume=. 1994 , publisher=

work page 1994

-

[36]

Journal of Economics & Management Strategy , volume=

Systematic Price Differences Between Successive Auctions Are No Anomaly , author=. Journal of Economics & Management Strategy , volume=

-

[37]

Games and Economic Behavior , volume=

Sequential auctions with randomly arriving buyers , author=. Games and Economic Behavior , volume=. 2011 , publisher=

work page 2011

-

[38]

Sequential auctions of stochastically equivalent objects , author=. Economics Letters , volume=. 1994 , publisher=

work page 1994

-

[39]

RAND Journal of Economics , volume=

Bounds on revenue distributions in counterfactual auctions with reserve prices , author=. RAND Journal of Economics , volume=. 2011 , publisher=

work page 2011

-

[40]

Handbook of Econometrics , volume=

Nonparametric approaches to auctions , author=. Handbook of Econometrics , volume=. 2007 , publisher=

work page 2007

-

[41]

The Review of Economic Studies , volume=

Identification and estimation of auction models with unobserved heterogeneity , author=. The Review of Economic Studies , volume=. 2011 , publisher=

work page 2011

-

[42]

Last-minute bidding and the rules of the auction: A field experiment on

Roth, Alvin E and Ockenfels, Axel , journal=. Last-minute bidding and the rules of the auction: A field experiment on. 2002 , publisher=

work page 2002

-

[43]

Identification in auctions with selective entry , author=. Econometrica , volume=. 2014 , publisher=

work page 2014

-

[44]

International Economic Review , volume=

A study of participation in dynamic auctions , author=. International Economic Review , volume=. 2014 , publisher=

work page 2014

-

[45]

The declining price anomaly in

van den Berg, Gerard J and van Ours, Jan C and Pradhan, Menno P , journal=. The declining price anomaly in. 2001 , publisher=

work page 2001

-

[46]

Sequential auctions with synergies: An example , author=. Economics Letters , volume=. 1997 , publisher=

work page 1997

-

[47]

RAND Journal of Economics , volume=

Structural estimation of the affiliated private value auction model , author=. RAND Journal of Economics , volume=. 2002 , publisher=

work page 2002

-

[48]

Quantitative Economics , volume=

Large sample properties for estimators based on the order statistics approach in auctions , author=. Quantitative Economics , volume=. 2013 , publisher=

work page 2013

-

[49]

Proceedings of the 23rd ACM Conference on Economics and Computation , pages=

Estimation of standard auction models , author=. Proceedings of the 23rd ACM Conference on Economics and Computation , pages=

-

[50]

Intersection bounds: Estimation and inference , author=. Econometrica , volume=. 2013 , publisher=

work page 2013

-

[51]

Confidence intervals for partially identified parameters , author=. Econometrica , volume=. 2004 , publisher=

work page 2004

-

[52]

On estimating distribution functions using

Leblanc, Alexandre , journal=. On estimating distribution functions using. 2012 , publisher=

work page 2012

- [53]

-

[54]

Estimation and confidence regions for parameter sets in econometric models , author=. Econometrica , volume=. 2007 , publisher=

work page 2007

-

[55]

RAND Journal of Economics , volume=

Unobserved heterogeneity and reserve prices in auctions , author=. RAND Journal of Economics , volume=. 2013 , publisher=

work page 2013

-

[56]

Nielsen, Finn. A new. Proceedings of the ESWC2011 Workshop on ``Making Sense of Microposts'' , pages=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.