Recognition: 1 theorem link

· Lean TheoremAdaptive Long-Run Variance Thresholding for Sparse Covariance Estimation in High-Dimensional Time Series

Pith reviewed 2026-05-15 01:44 UTC · model grok-4.3

The pith

Incorporating long-run variance into entrywise thresholds produces consistent sparse covariance estimates for high-dimensional time series under weak dependence.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By constructing entry-specific thresholds from consistent long-run variance estimators, the proposed thresholding procedure yields a covariance estimator that is consistent under the spectral norm, attains the optimal convergence rate over a class of sparse matrices, and achieves consistent support recovery for the nonzero entries, all under weak dependence conditions on the time series.

What carries the argument

Adaptive long-run variance thresholding procedure, which builds entrywise thresholds from consistent estimators of long-run variances to correct for temporal dependence in the sample covariance.

If this is right

- The estimator converges in spectral norm at the optimal rate for sparse covariance classes.

- Support recovery is consistent, correctly identifying zero and nonzero entries with high probability.

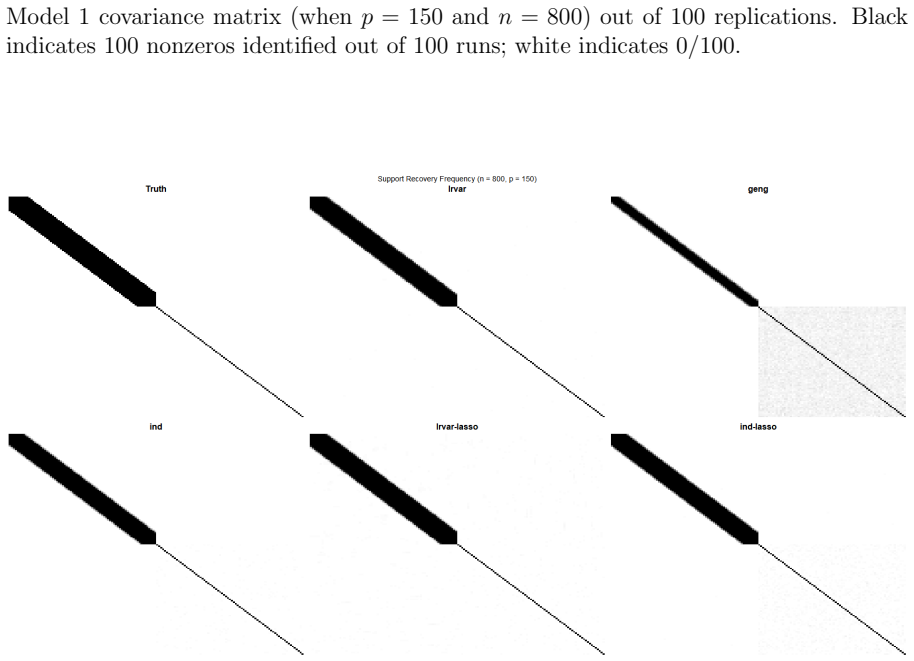

- Universal and adaptive thresholding rules without long-run variance adjustment fail to recover support under autocorrelation.

- The method outperforms existing thresholding estimators in both estimation error and support accuracy on simulated and real data.

Where Pith is reading between the lines

- The same long-run variance adjustment principle may extend to other high-dimensional matrix problems such as precision matrix estimation under dependence.

- Fields that routinely analyze autocorrelated high-dimensional data, such as finance and genomics, could obtain more reliable sparse structures by adopting the adjustment.

- Finite-sample behavior under moderate dependence strengths offers a natural next empirical check of the method's practical range.

Load-bearing premise

The time series satisfy weak dependence conditions that permit consistent estimation of long-run variances and keep the dependence from altering sample-covariance behavior beyond what the variance adjustment corrects.

What would settle it

A dataset or simulation in which strong dependence makes long-run variance estimation inconsistent and causes the spectral-norm error or support-recovery error to exceed the claimed rates would falsify the central claim.

Figures

read the original abstract

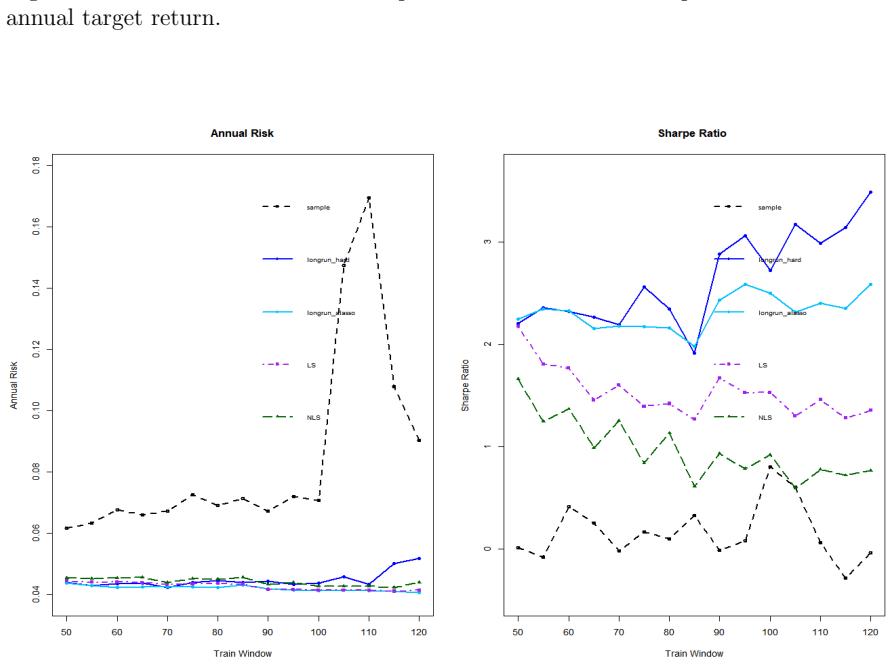

Estimating a sparse covariance matrix is a fundamental problem in high-dimensional statistics. However, thresholding methods developed for independent data are generally not directly applicable to high-dimensional time series, where temporal dependence alters the stochastic behavior of sample covariance estimators. This paper studies sparse covariance matrix estimation for high-dimensional time series under weak dependence. We propose a thresholding procedure that incorporates long-run variance into the construction of entry-specific thresholds, thereby adapting to temporal dependence. Under suitable regularity conditions, we show that the proposed estimator is consistent under the spectral norm and attains the optimal convergence rate over a class of sparse covariance matrices. We further establish support recovery consistency for identifying the nonzero entries of the covariance matrix. In addition, we show that universal and adaptive thresholding methods developed for independent data may fail to recover the support consistently in the presence of autocorrelation. Simulation studies demonstrate that the proposed method compares favorably with existing thresholding estimators in terms of both estimation accuracy and support recovery. Applications to gene expression data and stock return data further illustrate its practical usefulness.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes an adaptive thresholding estimator for sparse covariance matrices in high-dimensional time series under weak dependence. Entrywise thresholds are constructed using consistent estimators of the long-run variance (LRV) to account for temporal autocorrelation. The authors claim that the resulting estimator is consistent in the spectral norm, attains the minimax optimal rate over a class of sparse covariances, and achieves consistent support recovery for the nonzero entries. They also show that standard thresholding methods ignoring dependence can fail to recover the support, supported by simulations and applications to gene expression and stock return data.

Significance. If the claims hold, the work fills an important gap by extending sparse covariance thresholding to dependent data settings common in genomics and finance. The explicit demonstration that independent-data methods fail under autocorrelation, combined with the adaptive LRV adjustment, offers both theoretical and practical value. The simulation comparisons and real-data illustrations add to the contribution, provided the proofs rigorously handle the dependence structure.

major comments (2)

- [§4] §4 (theoretical results on support recovery): The uniform tail bounds used to establish support recovery consistency rely on the LRV-based thresholds controlling deviations of the sample covariance entries. However, because the kernel-based LRV estimator for each (i,j) pair is computed from the identical time series as the sample covariance, the two quantities are dependent; the manuscript must either invoke sample splitting or derive joint concentration inequalities that account for this shared-data correlation at the scale of the threshold (roughly sqrt(LRV log p / n)). Without this step, the claimed support recovery may not hold under the stated weak dependence conditions.

- [§3] §3 (methodology and assumptions): The regularity conditions for consistent LRV estimation are given, but the paper does not explicitly verify that these conditions suffice for the joint stochastic behavior needed in the uniform deviation bounds for support recovery. If the mixing rates required for joint concentration exceed those stated for marginal LRV consistency, the central support-recovery claim would require stronger assumptions than currently listed.

minor comments (2)

- [Abstract] The abstract states that the estimator 'attains the optimal convergence rate over a class of sparse covariance matrices' but does not name the precise sparsity class (e.g., row-sparsity level s or maximum degree) in the main theorem statement; this should be clarified for precision.

- [Simulations] In the simulation section, the dependence parameters (e.g., AR coefficients or mixing coefficients) used to generate the time series should be reported in the figure captions or table notes to allow reproducibility of the reported performance gains.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments, which highlight important technical points regarding dependence and joint concentration. We address each major comment below and will incorporate revisions to strengthen the proofs.

read point-by-point responses

-

Referee: [§4] §4 (theoretical results on support recovery): The uniform tail bounds used to establish support recovery consistency rely on the LRV-based thresholds controlling deviations of the sample covariance entries. However, because the kernel-based LRV estimator for each (i,j) pair is computed from the identical time series as the sample covariance, the two quantities are dependent; the manuscript must either invoke sample splitting or derive joint concentration inequalities that account for this shared-data correlation at the scale of the threshold (roughly sqrt(LRV log p / n)). Without this step, the claimed support recovery may not hold under the stated weak dependence conditions.

Authors: We agree that the dependence between the sample covariance and the kernel-based LRV estimator (computed from the same series) must be explicitly handled to justify the uniform tail bounds for support recovery. In the revised manuscript, we will modify the proof in Section 4 by introducing a sample-splitting scheme: under the weak dependence conditions, we partition the time series into two blocks separated by a gap of sufficient length to ensure near-independence. One block is used to compute the sample covariances, and the other to compute the LRV estimates. This renders the thresholds independent of the covariance entries at the relevant scale, allowing the existing concentration inequalities to apply directly without altering the convergence rates. We will also add a brief discussion of the block-size choice to preserve the asymptotic results. revision: yes

-

Referee: [§3] §3 (methodology and assumptions): The regularity conditions for consistent LRV estimation are given, but the paper does not explicitly verify that these conditions suffice for the joint stochastic behavior needed in the uniform deviation bounds for support recovery. If the mixing rates required for joint concentration exceed those stated for marginal LRV consistency, the central support-recovery claim would require stronger assumptions than currently listed.

Authors: We appreciate this observation. The alpha-mixing rates already stated for marginal LRV consistency (via the kernel estimator) are in fact sufficient for the joint uniform deviation bounds, as the same blocking arguments and Bernstein-type inequalities for dependent processes extend to the joint setting without requiring faster mixing. To make this rigorous and explicit, we will add a supporting lemma in the appendix that derives the joint concentration under the current assumptions, confirming that no stronger mixing conditions are needed. This lemma will be referenced in the proof of support recovery. revision: yes

Circularity Check

No circularity: derivation uses standard LRV construction without self-referential reduction

full rationale

The paper defines an adaptive thresholding estimator that incorporates a kernel-based long-run variance estimator into entrywise thresholds for the sample covariance of weakly dependent time series. Consistency under spectral norm and support recovery are claimed under regularity conditions on mixing rates and sparsity, with no equations or steps that define the target covariance in terms of the estimator itself, rename fitted quantities as predictions, or rely on self-citations whose content reduces to the present claims. The long-run variance is treated as an estimable population quantity independent of the sparsity pattern being recovered, and the abstract and described procedure contain no self-definitional or fitted-input loops.

Axiom & Free-Parameter Ledger

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

We propose a thresholding procedure that incorporates long-run variance into the construction of entry-specific thresholds

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

Andrews, D. W. (1991). Heteroskedasticity and autocorrelation consistent covariance matrix estimation.Econometrica: Journal of the Econometric Society, 817–858

1991

-

[2]

J., and Levina, E

Bickel, P. J., and Levina, E. (2008). Covariance regularization by thresholding.The An- nals of Statistics, 36(6), 2577–2604

2008

-

[3]

Cai, T., and Liu, W. (2011). Adaptive thresholding for sparse covariance matrix estima- tion.Journal of the American Statistical Association, 106(494), 672–684

2011

-

[4]

T., and Zhou, H

Cai, T. T., and Zhou, H. H. (2012). Minimax estimation of large covariance matrices under 1-norm.Statistica Sinica, 22(4), 1319–1378

2012

-

[5]

T., and Zhou, H

Cai, T. T., and Zhou, H. H. (2013). Optimal rates of convergence for sparse covariance matrix estimation.The Annals of Statistics, 40(5), 2389–2420

2013

-

[6]

Y., Lo, A

Campbell, J. Y., Lo, A. W., MacKinlay, A. C., and Whitelaw, R. F. (1998). The econo- metrics of financial markets.Macroeconomic Dynamics, 2(4), 559–562

1998

-

[7]

Campbell, J. Y. (2000). Asset pricing at the millennium.The Journal of Finance, 55(4), 1515–1567

2000

-

[8]

Chang, J., Guo, B., and Yao, Q. (2015). High dimensional stochastic regression with latent factors, endogeneity and nonlinearity.Journal of Econometrics, 189(2), 297–312

2015

-

[9]

Cochrane, J. H. (2009).Asset Pricing: Revised Edition. Princeton University Press. Den Haan, W. J., and Levin, A. T. (1997). A practitioner’s guide to robust covariance matrix estimation.Handbook of Statistics, 15, 299–342

2009

-

[10]

L., and Johnstone, I

Donoho, D. L., and Johnstone, I. M. (1994). Ideal spatial adaptation by wavelet shrinkage. Biometrika, 81(3), 425–455

1994

-

[11]

L., and Johnstone, I

Donoho, D. L., and Johnstone, I. M. (1998). Minimax estimation via wavelet shrinkage. The Annals of Statistics, 26(3), 879–921

1998

-

[12]

F., and French, K

Fama, E. F., and French, K. R. (1993). Common risk factors in the returns on stocks and bonds.Journal of Financial Economics, 33(1), 3–56. 40

1993

-

[13]

F., and French, K

Fama, E. F., and French, K. R. (2014). A five-factor asset pricing model.Journal of Financial Economics, 116(1), 1–22

2014

-

[14]

Fan, J., Fan, Y., and Lv, J. (2008). High dimensional covariance matrix estimation using a factor model.Journal of Econometrics, 147(1), 186–197

2008

-

[15]

Fan, J., Liu, H., and Wang, W. (2018). Large covariance estimation through elliptical factor models.The Annals of Statistics, 46(4), 1383–1414

2018

-

[16]

Gao, Z., and Tsay, R. S. (2019). A structural-factor approach to modeling high- dimensional time series and space-time data.Journal of Time Series Analysis, 40(3), 343–362

2019

-

[17]

Jiang, B. (2013). Covariance selection by thresholding the sample correlation matrix. Statistics & Probability Letters, 83(11), 2492–2498

2013

-

[18]

S., Ringner, M., Saal, L

Khan, J., Wei, J. S., Ringner, M., Saal, L. H., Ladanyi, M., Westermann, F., et al. (2001). Classification and diagnostic prediction of cancers using gene expression profiling and artificial neural networks.Nature Medicine, 7(6), 673–679

2001

-

[19]

M., Vogelsang, T

Kiefer, N. M., Vogelsang, T. J., and Bunzel, H. (2000). Simple robust testing of regression hypotheses.Econometrica, 68(3), 695–714

2000

-

[20]

Lahiri, S. N. (2013).Resampling Methods for Dependent Data. Springer Science & Busi- ness Media

2013

-

[21]

Ledoit, O., and Wolf, M. (2004). A well-conditioned estimator for large-dimensional co- variance matrices.Journal of Multivariate Analysis, 88(2), 365–411

2004

-

[22]

Ledoit, O., and Wolf, M. (2012). Nonlinear shrinkage estimation of large-dimensional covariance matrices.The Annals of Statistics, 40(2), 1024–1060

2012

-

[23]

M., Corum, A

Malioutov, D. M., Corum, A. A., and Cetin, M. (2016). Covariance matrix estimation for interest-rate risk modeling via smooth and monotone regularization.IEEE Journal of Selected Topics in Signal Processing, 10(6), 1006–1014

2016

-

[24]

Markowitz, H. M. (1952). Portfolio selection.The Journal of Finance, 7(1), 71–91

1952

-

[25]

(1959).Portfolio Selection: Efficient Diversification of Investments

Markowitz, H. (1959).Portfolio Selection: Efficient Diversification of Investments. John Wiley and Sons. Merlev` ede, F., Peligrad, M., and Rio, E. (2011). A Bernstein type inequality and moder- ate deviations for weakly dependent sequences.Probability Theory and Related Fields, 151(3), 435–474

1959

-

[26]

Pelger, M. (2020). Understanding systematic risk: A high-frequency approach.The Jour- nal of Finance, 75(4), 2179–2220. 41

2020

-

[27]

Ross, S. A. (1976). The arbitrage theory of capital asset pricing.Journal of Economic Theory, 13(3), 341–360

1976

-

[28]

J., Levina, E., and Zhu, J

Rothman, A. J., Levina, E., and Zhu, J. (2009). Generalized thresholding of large covari- ance matrices.Journal of the American Statistical Association, 104(485), 177–186

2009

-

[29]

H., and Watson, M

Stock, J. H., and Watson, M. W. (1989). New indexes of coincident and leading economic indicators.NBER Macroeconomics Annual, 4, 351–394

1989

-

[30]

H., and Watson, M

Stock, J. H., and Watson, M. W. (1998). Diffusion indexes.NBER Working Paper Series

1998

-

[31]

Xu, F., Huang, J., and Wen, Z. (2015). High dimensional covariance matrix estimation using multi-factor models from incomplete information.Science China Mathematics, 58(4), 829–844

2015

-

[32]

Yang, Y., Chen, C., and Chen, S. (2024). Covariance matrix estimation for high- throughput biomedical data with interconnected communities.The American Statisti- cian, 78(4), 401–411. 42

2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.