Distributionally Robust Games via Coherent Risk Measures

Pith reviewed 2026-05-20 02:49 UTC · model grok-4.3

The pith

Coherent risk measures define distributionally robust games that admit equilibria in data-driven settings with finite payoff samples.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By treating coherent utility measures as a primitive of player preferences and substituting them into distributionally robust payoff functions whose ambiguity sets are defined from finite samples, the paper shows existence of equilibria follows from prior results, the games are inherently continuous, a bound holds on expected-utility loss from risk aversion, and equilibrium computation is PPAD-complete in general with membership in PPAD and multilinear complementarity formulations for several concrete coherent measures.

What carries the argument

Coherent risk measures (such as Mean-semideviation and Conditional Value-at-Risk) substituted into the payoffs of distributionally robust games whose ambiguity sets are built from finite samples.

If this is right

- Equilibria exist for various ambiguity sets in data-driven games once coherent risk measures define the robust payoffs.

- The games are continuous rather than finite matrix games, which fundamentally changes equilibrium structure and blocks direct use of standard correlated-equilibrium notions.

- A bound holds on the loss in expected utility a player suffers by adopting a risk-averse attitude.

- Equilibrium computation is PPAD-complete in general and lies in PPAD for several specific coherent utility measure games.

- Multilinear complementarity programs provide a practical formulation for computing equilibria in these games.

Where Pith is reading between the lines

- The same substitution technique could be tested on repeated or dynamic games to see whether risk attitudes produce qualitatively different long-run behavior.

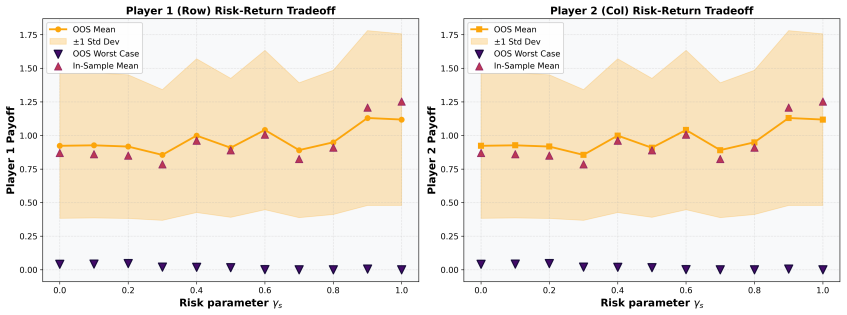

- Numerical out-of-sample robustness observed in the experiments suggests the equilibria may remain stable when new samples arrive after the ambiguity sets are fixed.

- The continuity of the games implies that standard discrete solution concepts may need continuous analogs when risk measures are present.

Load-bearing premise

That prior existence theorems for distributionally robust equilibria continue to apply after coherent risk measures replace ordinary expected utility and ambiguity sets are formed from finite samples.

What would settle it

A concrete finite-sample game instance using a coherent risk measure such as CVaR for which no equilibrium exists, or a polynomial-time algorithm for the general case, would refute the existence and complexity claims.

Figures

read the original abstract

We study strategic interaction in data-driven games where players face uncertainty about payoff distributions inferred from finite samples. To model calibrated attitudes toward such uncertainty, we formulate distributionally robust games with a special focus on coherent utility (risk) measures, including Mean-semideviation and Conditional Value-at-Risk. This framework treats risk sensitivity as a primitive feature of player preferences while retaining a formal connection to distributional robustness. We make a number of contributions that are enumerated next. (1) We use prior results for the existence of distributionally robust equilibria to show the existence of equilibria in data-driven settings for various ambiguity sets, and (2) show that these games are inherently continuous, rather than finite matrix games, which fundamentally alters equilibrium structure and precludes direct extensions of standard correlated equilibrium notions. (3) We bound the loss in expected utility that a player can expect from being risk-averse. (4) We further characterize the computational complexity of equilibrium computation, proving PPAD-completeness in general and PPAD membership for several coherent utility measure games. (5) We present multilinear complementarity program formulations for several coherent utility measure games. (6) Numerical experiments reveal the robustness and out of sample performance of the game solutions. Our results unify risk-theoretic modeling and equilibrium analysis, providing a principled foundation for risk-aware strategic decision-making in data-driven environments.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript studies distributionally robust games in data-driven settings where players employ coherent risk measures (Mean-semideviation and Conditional Value-at-Risk) to express calibrated attitudes toward uncertainty in payoff distributions inferred from finite samples. It claims to (1) establish existence of equilibria by invoking prior DRO equilibrium results after substitution of coherent risk measures and construction of ambiguity sets from samples, (2) show that the resulting games are inherently continuous (altering equilibrium structure and precluding direct extension of correlated equilibrium notions), (3) bound the loss in expected utility from risk aversion, (4) prove PPAD-completeness of equilibrium computation in general with PPAD membership for several coherent utility games, (5) give multilinear complementarity program formulations, and (6) present numerical experiments on robustness and out-of-sample performance.

Significance. If the existence claim and complexity results hold after verification of the requisite regularity conditions, the work would usefully connect coherent risk measures with equilibrium analysis, supplying both theoretical foundations and concrete computational tools (formulations and complexity classification) for risk-aware strategic decision-making under distributional uncertainty. The numerical component adds practical grounding.

major comments (1)

- [Abstract, contribution (1)] Abstract, contribution (1): The existence of equilibria in the data-driven setting is obtained by direct substitution of coherent risk measures into prior DRO equilibrium theorems together with finite-sample ambiguity sets. Prior theorems of this type require the effective (risk-adjusted) payoff to remain continuous or upper semi-continuous in the joint mixed-strategy profile for every distribution in the ambiguity set, as well as suitable compactness of the ambiguity set in a compatible topology. The manuscript provides no explicit verification that these conditions are inherited when the underlying payoff is only measurable with respect to an empirical measure supported on finitely many points; this step is load-bearing for the central existence claim.

minor comments (2)

- The specific ambiguity sets (e.g., Wasserstein balls or moment-based sets) employed for the existence and complexity results should be stated explicitly in the main text with references to their convexity and compactness properties.

- Notation for the risk-adjusted payoff functions and the mapping from empirical samples to ambiguity sets could be introduced earlier and used consistently to improve readability of the formulations in Section 4.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive review. The major comment correctly identifies a point where the manuscript's invocation of prior results would benefit from more explicit verification of the requisite regularity conditions. We address this below and will revise the manuscript accordingly.

read point-by-point responses

-

Referee: [Abstract, contribution (1)] Abstract, contribution (1): The existence of equilibria in the data-driven setting is obtained by direct substitution of coherent risk measures into prior DRO equilibrium theorems together with finite-sample ambiguity sets. Prior theorems of this type require the effective (risk-adjusted) payoff to remain continuous or upper semi-continuous in the joint mixed-strategy profile for every distribution in the ambiguity set, as well as suitable compactness of the ambiguity set in a compatible topology. The manuscript provides no explicit verification that these conditions are inherited when the underlying payoff is only measurable with respect to an empirical measure supported on finitely many points; this step is load-bearing for the central existence claim.

Authors: We thank the referee for highlighting this important technical point. The existence claim in contribution (1) does rely on direct substitution into prior DRO equilibrium results, and the manuscript does not contain an explicit paragraph verifying that continuity (or upper semi-continuity) of the risk-adjusted payoffs and compactness of the ambiguity sets are preserved under finite-sample constructions. In the data-driven setting the ambiguity sets are balls (e.g., Wasserstein or moment-based) centered at the empirical measure, which is supported on finitely many points; such sets are compact in the weak topology. Coherent risk measures such as CVaR and mean-semideviation are continuous with respect to weak convergence on compact supports, and the finite-support structure ensures that the map from mixed-strategy profiles to the induced payoff distributions is continuous. Consequently the effective (risk-adjusted) payoffs inherit the required regularity. We agree that this reasoning should be stated explicitly rather than left implicit and will add a dedicated verification paragraph (with appropriate citations to continuity properties of coherent risk measures) in the revised manuscript. revision: yes

Circularity Check

Existence via external prior results; no reduction to self-inputs by construction

full rationale

The paper's central existence claim (contribution 1) invokes prior results on distributionally robust equilibria after substituting coherent risk measures and defining ambiguity sets from samples. This is an application of external theorems rather than a self-definitional loop or a fitted parameter renamed as a prediction. No equations or steps in the abstract reduce the claimed equilibria to the paper's own fitted values or unverified self-citations by construction. Computational complexity (PPAD) and formulation contributions are separate and do not rely on the existence step for their validity. The derivation remains self-contained against the cited external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Prior results establish existence of distributionally robust equilibria for the ambiguity sets considered

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.