A two-stage stochastic programming framework for oil and gas exploration well portfolio optimization under geological and economic uncertainty

Pith reviewed 2026-06-29 16:21 UTC · model grok-4.3

The pith

A two-stage stochastic optimization framework selects oil and gas exploration well portfolios by incorporating geological learning from early results.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The framework formulates exploration planning as a two-stage stochastic program in which here-and-now selections of frontier traps, appraisal projects, and mature appraisal units are followed by scenario-dependent recourse projects such as follow-up appraisal, reserve upgrading, conversion to proved reserves, rolling extension, and data re-evaluation; geological learning is represented by a logit-scale posterior updating rule that links first-stage outcomes to the success probabilities of recourse projects, and the model is solved by combining sample average approximation with NSGA-II for the first stage and scenario-wise constrained 0-1 optimization for the second stage to maximize expected

What carries the argument

posterior-informed two-stage stochastic multi-objective optimization framework with logit-scale posterior updating mechanism

If this is right

- The model produces an interpretable risk-return frontier for portfolio selection under uncertainty.

- It supports adaptive exploration planning that incorporates geological learning from first-stage outcomes.

- Downside-risk control is achieved through explicit minimization of conditional value-at-risk.

- Reserve-reliability requirements are enforced via chance constraints on success rate and reserve targets.

- The solution procedure combines sample average approximation with NSGA-II and scenario-wise 0-1 optimization.

Where Pith is reading between the lines

- The same two-stage structure with explicit recourse and learning updates could apply to other sequential investment decisions where early outcomes revise later probabilities.

- Calibration of the logit-scale parameters would likely require fitting to historical drilling records from the specific basin.

- Static expected-value optimization would omit the value of information that the recourse stage explicitly models.

- The chance-constraint formulation could be extended to additional reliability metrics such as production-rate targets.

Load-bearing premise

Geological learning is accurately captured by a logit-scale posterior updating mechanism that links first-stage success or failure to the success probabilities of related recourse projects.

What would settle it

Field data in which the risk-return performance of model-selected portfolios deviates substantially from the predicted frontier or in which observed geological outcomes fail to follow the logit-scale update rule used in the model.

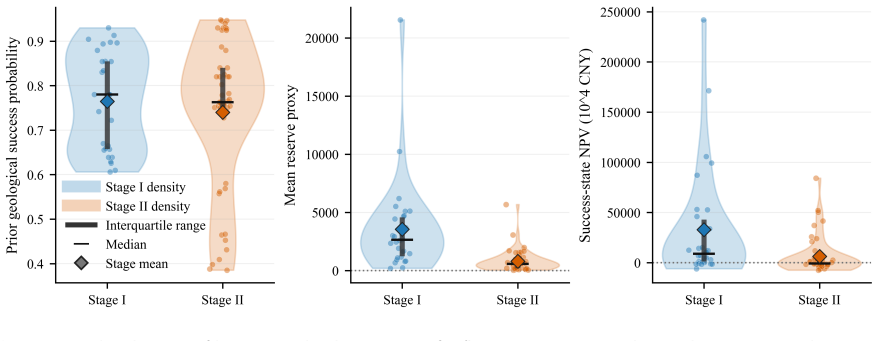

Figures

read the original abstract

Annual oil and gas exploration planning involves selecting a limited portfolio of drilling and appraisal-related projects before geological outcomes are known. This decision is affected by uncertainties in geological success, reserve size, and economic value, while also subject to budget, well-count, success-rate, and reserve-reliability requirements. A strategy based only on expected value is therefore insufficient, as early drilling results may change the value of subsequent follow-up opportunities. This study develops a posterior-informed two-stage stochastic multi-objective optimization framework for exploration well selection under uncertainty. The first stage selects a here-and-now portfolio of frontier traps, appraisal projects, and mature appraisal units. After first-stage outcomes are observed, the second stage determines scenario-dependent recourse projects, including follow-up appraisal, reserve upgrading, conversion-to-proved reserves, rolling extension, and data re-evaluation projects. Geological learning is modeled using a logit-scale posterior updating mechanism that links first-stage success or failure to the success probabilities of related recourse projects. The model maximizes expected net present value and minimizes conditional value-at-risk, while imposing chance constraints on drilling success rate and individual and joint reserve targets. To solve the model, sample average approximation is combined with NSGA-II for first-stage portfolio search and a scenario-wise constrained 0-1 optimization procedure for second-stage evaluation. A numerical case study shows that the proposed framework provides an interpretable risk-return frontier and supports adaptive exploration planning under geological learning, downside-risk control, and reserve-reliability requirements.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops a posterior-informed two-stage stochastic multi-objective optimization framework for selecting oil and gas exploration well portfolios under geological success, reserve size, and economic uncertainties. First-stage decisions select a portfolio of frontier traps, appraisal projects, and mature units subject to budget and well-count limits; second-stage recourse actions (follow-up appraisal, reserve upgrading, etc.) are determined after outcomes are observed. Geological learning is incorporated via a logit-scale posterior updating rule linking first-stage results to updated success probabilities. The model maximizes expected NPV while minimizing CVaR, subject to chance constraints on success rate and reserve targets. It is solved by combining sample average approximation with NSGA-II for the first stage and scenario-wise 0-1 optimization for the second stage. A numerical case study is presented to illustrate an interpretable risk-return frontier and adaptive planning capabilities.

Significance. If the modeling choices and numerical results are robust, the work offers a practical advance in stochastic optimization for exploration planning by integrating geological learning, downside-risk control via CVaR, and reserve-reliability constraints into a single adaptive framework. The combination of NSGA-II with scenario-wise recourse evaluation provides a computationally tractable way to generate Pareto fronts that decision makers can interpret, which addresses a recognized gap between expected-value planning and risk-aware adaptive strategies in the oil and gas sector.

minor comments (3)

- The abstract states that the logit-scale posterior updating 'links first-stage success or failure to the success probabilities of related recourse projects,' but the precise functional form, parameter estimation procedure, and any sensitivity analysis for these parameters are not described; this should be added with explicit equations in the model formulation section.

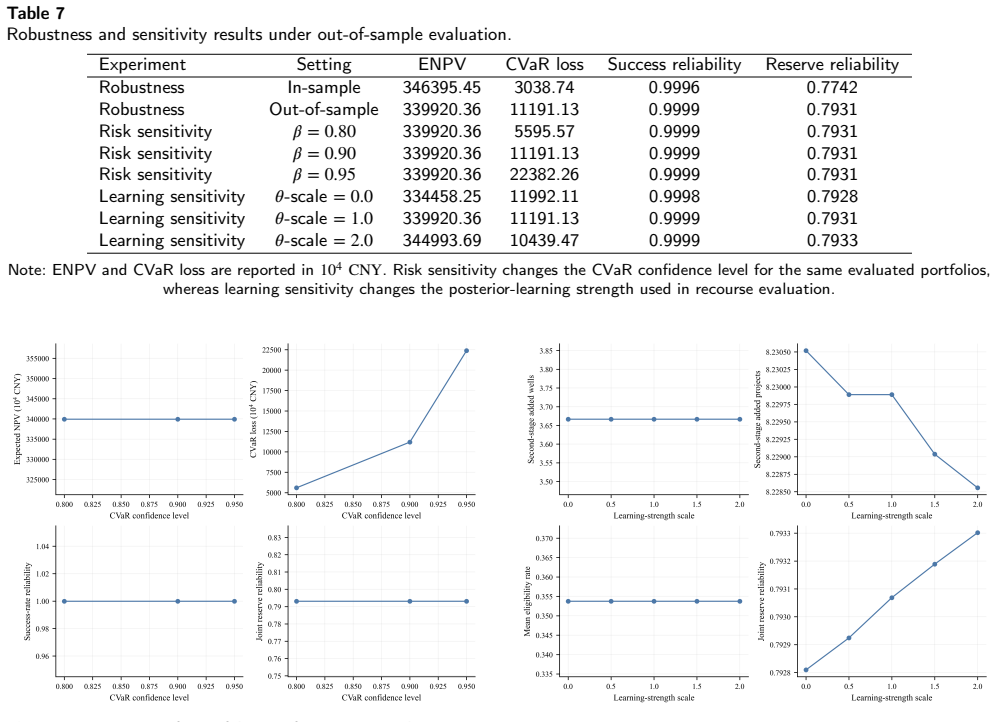

- The numerical case study is said to demonstrate an 'interpretable risk-return frontier,' yet no details are given on the number of scenarios, the specific CVaR confidence level chosen, or quantitative metrics (e.g., out-of-sample performance or comparison against a myopic expected-value benchmark); these should be reported in a dedicated results subsection with tables or figures.

- Notation for the multi-objective weighting between expected NPV and CVaR, as well as the chance-constraint violation probabilities, should be introduced consistently and early in the mathematical model to avoid ambiguity when reading the solution algorithm description.

Simulated Author's Rebuttal

We thank the referee for the positive summary, significance assessment, and recommendation of minor revision. The report provides no specific major comments to address point by point.

Circularity Check

No significant circularity; framework is a modeling construct evaluated externally

full rationale

The paper presents a two-stage stochastic multi-objective optimization model with chance constraints and a logit-scale posterior updating rule for geological learning. The first-stage decisions select a portfolio, second-stage recourse is scenario-dependent, and the solution uses SAA combined with NSGA-II. The numerical case study evaluates the framework against external metrics such as expected NPV, CVaR, and reserve-reliability targets. No step reduces a claimed prediction or result to a quantity defined by the model's own fitted parameters or by a self-citation chain; the logit updating and multi-objective formulation are explicit modeling choices whose validity is application-specific rather than self-referential. The derivation chain is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (3)

- Number of scenarios

- Logit-scale posterior parameters

- CVaR confidence level and weighting

axioms (2)

- domain assumption Uncertainties in geological success, reserve size, and economic value can be represented by a finite set of scenarios

- ad hoc to paper The logit-scale posterior updating mechanism accurately links first-stage outcomes to recourse project probabilities

Reference graph

Works this paper leans on

-

[1]

W. C. LaCosta, A. V. Milkov, Petroleum exploration portfolios gen- erated with different optimization approaches: Lessons for decision- makers, Journal of Petroleum Science and Engineering 214 (2022) 110459. doi:https://doi.org/10.1016/j.petrol.2022.110459

-

[2]

S. Suslick, D. Schiozer, Risk analysis applied to petroleum explo- rationandproduction:anoverview,JournalofPetroleumScienceand Engineering 44 (1) (2004) 1–9, risk Analysis Applied to Petroleum Exploration and Production.doi:https://doi.org/10.1016/j.petrol. 2004.02.001

-

[3]

A. V. Milkov, Risk tables for less biased and more consistent estima- tionofprobabilityofgeologicalsuccess(pos)forsegmentswithcon- ventional oil and gas prospective resources, Earth-Science Reviews 150 (2015) 453–476. doi:https://doi.org/10.1016/j.earscirev. 2015.08.006

-

[4]

doi:https://doi.org/10.1016/j.petrol.2004.02.005

M.R.Walls,Combiningdecisionanalysisandportfoliomanagement to improve project selection in the exploration and production firm, Journal of Petroleum Science and Engineering 44 (1) (2004) 55– 65, risk Analysis Applied to Petroleum Exploration and Production. doi:https://doi.org/10.1016/j.petrol.2004.02.005

-

[5]

S. M. Santos, V. E. Botechia, D. J. Schiozer, A. T. Gaspar, Expected value, downside risk and upside potential as decision criteria in productionstrategyselectionforpetroleumfielddevelopment,Journal ofPetroleumScienceandEngineering157(2017)81–93. doi:https: //doi.org/10.1016/j.petrol.2017.07.002

-

[6]

Scalar field vacuum expectation value in- duced by gravitational wave background

R. Ahmadi, R. B. Bratvold, An exposition of least square monte carlo approach for real options valuation, Geoenergy Science and Engineering 222 (2023) 111230. doi:https://doi.org/10.1016/j. petrol.2022.111230

work page doi:10.1016/j 2023

-

[7]

D. Aghajani, R. B. Bratvold, V. Hagspiel, O. Noshchenko, V. K. Toutain,Amulti-objectivedecision-makingframeworkforthechoice betweenmutuallyexclusivealternativesunderuncertainty:Assessing the competitiveness of offshore wind for a gas field electrification on thencs,EnergyEconomics141(2025)108032. doi:https://doi.org/ 10.1016/j.eneco.2024.108032

-

[8]

C. Yong, M. Tong, Z. Yang, J. Zhou, Conventional natural gas projectinvestmentanddecisionmakingundermultipleuncertainties, Energies 16 (5) (2023).doi:10.3390/en16052342

-

[9]

H. Liu, T. Zhang, How to optimize the investment decision of shale gas multi-objective green development for energy sustain- able development?, Journal of Petroleum Exploration and Produc- tion Technology 15 (12) (2025) 192.doi:https://doi.org/10.1007/ s13202-025-02084-7

2025

-

[10]

S. Nadarajah, N. Secomandi, A review of the operations literature on real options in energy, European Journal of Operational Research 309 (2) (2023) 469–487.doi:https://doi.org/10.1016/j.ejor.2022. 09.014

-

[11]

O. Noshchenko, V. Hagspiel, Environmental and economic multi- objective realoptions analysis: Electrification choicesfor field devel- opment investment planning, Energy 295 (2024) 131053.doi:https: //doi.org/10.1016/j.energy.2024.131053

-

[12]

M. A. G. Dias, R. E. P. Borges, Valuing oil reserve volumes under price uncertainty, Journal of Economics and Business 137 (2025) 106277, recent Developments and Challenges in Real Options.doi: https://doi.org/10.1016/j.jeconbus.2025.106277

-

[13]

Y. G. Lopes, A. T. d. Almeida, A multicriteria decision model for selecting a portfolio of oil and gas exploration projects, Pesquisa Operacional 33 (3) (2013) 417–441.doi:https://doi.org/10.1590/ S0101-74382013005000011

2013

-

[14]

Y.G.Lopes,A.T.deAlmeida,Assessmentofsynergiesforselectinga project portfolio in the petroleum industry based on a multi-attribute utility function, Journal of Petroleum Science and Engineering 126 (2015)131–140.doi:https://doi.org/10.1016/j.petrol.2014.12.012

-

[15]

Tarhan, I

B. Tarhan, I. E. Grossmann, V. Goel, Stochastic programming ap- proachfortheplanningofoffshoreoilorgasfieldinfrastructureunder decision-dependent uncertainty, Industrial & Engineering Chemistry Research 48 (6) (2009) 3078–3097

2009

-

[17]

G. Martinelli, J. Eidsvik, K. Hokstad, R. Hauge, Strategies for petroleumexplorationonthebasisofbayesiannetworks:Acasestudy, SPE Journal 19 (04) (2013) 564–575.doi:10.2118/159722-PA

-

[18]

G. Martinelli, J. Eidsvik, R. Hauge, Dynamic decision making for graphical models applied to oil exploration, European Journal of Operational Research 230 (3) (2013) 688–702.doi:https://doi.org/ 10.1016/j.ejor.2013.04.057

-

[19]

V. Gupta, I. E. Grossmann, Multistage stochastic programming ap- proach for offshore oilfield infrastructure planning under produc- tion sharing agreements and endogenous uncertainties, Journal of Petroleum Science and Engineering 124 (2014) 180–197.doi:https: //doi.org/10.1016/j.petrol.2014.10.006

-

[20]

J. Kettunen, M. A. Lejeune, Data-driven project portfolio selection: Decision-dependent stochastic programming formulations with reli- ability and time to market requirements, Computers & Operations Research 143 (2022) 105737. doi:https://doi.org/10.1016/j.cor. 2022.105737

-

[22]

P. Artzner, F. Delbaen, J.-M. Eber, D. Heath, Coherent measures of risk, Mathematical Finance 9 (3) (1999) 203–228.doi:https: //doi.org/10.1111/1467-9965.00068

-

[23]

R. T. Rockafellar, S. Uryasev, et al., Optimization of conditional value-at-risk,Journalofrisk2(2000)21–42. doi:10.21314/JOR.2000. 038

-

[24]

Krokhmal, J

P. Krokhmal, J. Palmquist, S. Uryasev, Portfolio optimization with conditional value-at-risk objective and constraints, Journal of risk 4 (2002) 43–68

2002

-

[25]

doi:10.1137/ S1052623499363220

A.J.Kleywegt,A.Shapiro,T.Homem-deMello,Thesampleaverage approximation method for stochastic discrete optimization, SIAM Journal on Optimization 12 (2) (2002) 479–502. doi:10.1137/ S1052623499363220

2002

-

[26]

K. Deb, A. Pratap, S. Agarwal, T. Meyarivan, A fast and elitist mul- tiobjective genetic algorithm: Nsga-ii, IEEE Transactions on Evolu- tionaryComputation6(2)(2002)182–197. doi:10.1109/4235.996017

-

[27]

R.E.Kass,A.E.Raftery,Bayesfactors,JournaloftheAmericanSta- tistical Association 90 (430) (1995) 773–795.doi:10.1080/01621459. 1995.10476572

-

[28]

F.P.Agterberg,Q.Cheng,Conditionalindependencetestforweights- of-evidence modeling, Natural Resources Research 11 (4) (2002) 249–255.doi:10.1023/A:1021193827501

-

[29]

P. W. Monigle, T. S. Hedayati, F. J. Goulding, Integrated and im- proved direct hydrocarbon indicators: A step forward in petroleum risk discrimination, AAPG Bulletin 109 (5) (2025) 617–636.doi: 10.1306/04042524030

-

[30]

R. Rockafellar, S. Uryasev, Conditional value-at-risk for general loss distributions,JournalofBanking&Finance26(7)(2002)1443–1471. doi:https://doi.org/10.1016/S0378-4266(02)00271-6. First Author et al.:Preprint submitted to Elsevier Page 17 of 17

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.