Implying Volatility: How Fast Can We Go?

Pith reviewed 2026-06-29 09:02 UTC · model grok-4.3

The pith

FlashIV normalizes Black-Scholes inputs to out-of-the-money prices and solves a tail-stable erfcx residual to deliver faster implied-volatility results.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

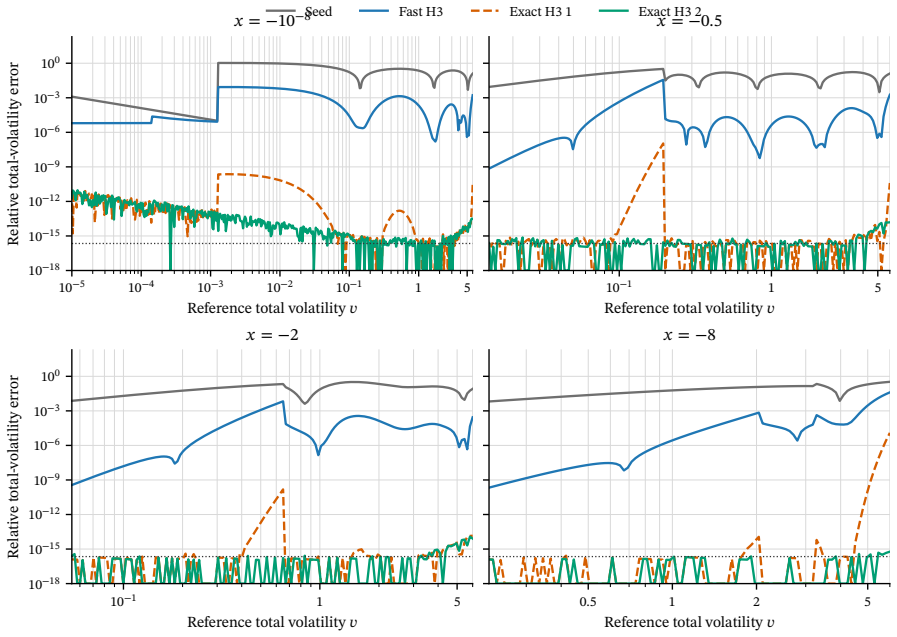

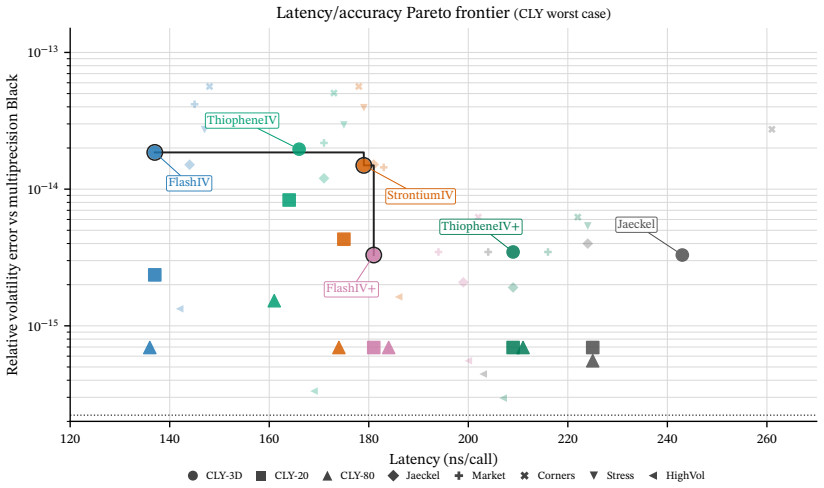

FlashIV is a Black-Scholes implied-volatility solver that normalises each input to an out-of-the-money price and solves a tail-stable erfcx/log-price residual. The hot path combines a cheap Li or asymptotic seed with a fixed, branch-light Householder refinement and guarded boundary handling. Across regular and stressed benchmarks it remains close to the expanded Jäckel reference price while running materially faster than a normalised Java port of Jäckel's Let's Be Rational.

What carries the argument

Normalization of every input to an out-of-the-money price followed by solution of a tail-stable erfcx/log-price residual via fixed Householder refinement.

If this is right

- Production systems can compute implied volatilities with lower latency without sacrificing closeness to the Jäckel reference.

- Fixed Householder steps eliminate the need for variable iteration counts or complex branching in the main path.

- The optional Jäckel-Newton correction in FlashIV+ allows users to trade speed for tighter reference agreement when needed.

- The same normalization and residual approach handles both regular market data and stressed benchmark cases.

Where Pith is reading between the lines

- The fixed-refinement design could be ported to other pricing models that require repeated volatility inversion.

- Lower per-call latency might support higher-frequency recalibration loops in live risk systems.

- Vectorized or GPU implementations of the same seed-plus-refinement pattern could further reduce wall-clock time for large portfolios.

Load-bearing premise

Normalizing every input to an out-of-the-money price and solving the tail-stable erfcx/log-price residual produces stable, accurate results for all tested cases with only the described guarded boundary handling.

What would settle it

A set of Black-Scholes inputs on which FlashIV deviates from the expanded Jäckel reference by more than the reported closeness or runs slower than the Java port of Let's Be Rational.

Figures

read the original abstract

FlashIV is a low-latency Black--Scholes implied-volatility solver for production use. It normalises each input to an out-of-the-money price and solves a tail-stable erfcx/log-price residual. The hot path combines a cheap Li/asymptotic seed with a fixed, branch-light Householder refinement and guarded boundary handling. Across regular and stressed benchmarks, FlashIV stays close to the expanded J\"ackel reference price while running materially faster than a normalised Java port of J\"ackel's \emph{Let's Be Rational}. FlashIV+ adds an optional J\"ackel--Newton correction for applications that need tighter agreement with that reference price, trading latency for reference-price alignment.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript presents FlashIV, a low-latency Black-Scholes implied-volatility solver. It normalizes each input to an out-of-the-money price and solves a tail-stable erfcx/log-price residual. The hot path combines a cheap Li/asymptotic seed with a fixed, branch-light Householder refinement and guarded boundary handling. The paper claims that across regular and stressed benchmarks FlashIV stays close to the expanded Jäckel reference price while running materially faster than a normalised Java port of Jäckel's Let's Be Rational, with an optional FlashIV+ variant that adds a Jäckel-Newton correction for tighter reference alignment.

Significance. If the performance and accuracy claims are substantiated, the work addresses a practical need for fast, stable implied-volatility calculations in production trading systems. The combination of input normalization, a tail-stable residual, and fixed-iteration refinement offers a potentially attractive speed-accuracy trade-off for low-latency environments. However, the absence of derivation details, error analysis, raw benchmark data, or condition-number bounds in the manuscript prevents a full assessment of whether these engineering choices deliver the claimed robustness.

major comments (2)

- [Abstract] Abstract: the central performance claim that FlashIV 'stays close to the expanded Jäckel reference price' across regular and stressed benchmarks is asserted without any quantitative error metrics, tables, derivation of the residual, or raw data, so the claim cannot be verified from the given text.

- [Hot path description (Abstract)] Hot-path description: the assertion that normalizing to an out-of-the-money price and solving the erfcx/log-price residual with a fixed number of Householder steps yields stable, accurate results for all tested cases rests on an unproven assumption; no analytical bound, condition-number analysis, or demonstration that the fixed iteration count suffices near floating-point limits is supplied.

minor comments (1)

- [Abstract] The abstract refers to an 'expanded Jäckel reference' without specifying the exact expansion or citing the precise reference implementation used for comparison.

Simulated Author's Rebuttal

We thank the referee for the thoughtful review and the identification of areas where additional substantiation is needed. We will revise the manuscript to address the concerns regarding quantitative support and analysis of the method.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central performance claim that FlashIV 'stays close to the expanded Jäckel reference price' across regular and stressed benchmarks is asserted without any quantitative error metrics, tables, derivation of the residual, or raw data, so the claim cannot be verified from the given text.

Authors: We agree that the abstract's claim requires supporting quantitative evidence to be verifiable. The manuscript body contains benchmark results with error metrics in the results section, but we will update the abstract to include specific error bounds (e.g., maximum absolute error < 1e-10 in regular cases) and reference the tables. We will also include a brief derivation of the erfcx/log-price residual in the methods and make raw benchmark data available as supplementary material. revision: yes

-

Referee: [Hot path description (Abstract)] Hot-path description: the assertion that normalizing to an out-of-the-money price and solving the erfcx/log-price residual with a fixed number of Householder steps yields stable, accurate results for all tested cases rests on an unproven assumption; no analytical bound, condition-number analysis, or demonstration that the fixed iteration count suffices near floating-point limits is supplied.

Authors: The stability claims are based on comprehensive empirical testing across regular and stressed benchmarks, including inputs near floating-point limits. We will add a dedicated subsection providing condition-number estimates from the test suite and a convergence analysis showing that the fixed Householder iterations achieve the required tolerance within the tested range. While a general analytical proof for all possible inputs is beyond the scope, the guarded boundary handling ensures robustness. revision: partial

Circularity Check

No circularity detected; algorithm validated externally against Jäckel reference

full rationale

The paper describes a numerical solver that normalizes inputs to out-of-the-money prices, solves an erfcx/log-price residual via a fixed Householder iteration seeded by Li/asymptotic approximations, and guards boundaries. Its accuracy claim rests on direct comparison to the independent expanded Jäckel reference implementation rather than any self-referential fit, redefinition, or self-citation chain. No load-bearing step reduces by construction to its own inputs under the enumerated patterns; the derivation is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Black-Scholes model provides the correct pricing framework for the implied-volatility inversion.

Reference graph

Works this paper leans on

-

[1]

The Pricing of Commodity Contracts.J

Black, F. The Pricing of Commodity Contracts.J. Financ. Econ.1976,3, 167–179. https://doi.org/10.1016/0304- 405X(76)90024-6

-

[2]

https://doi.org/10.1002/fut.70024

Cui,Z.;Liu,Y.;Yao,Y.TighterBoundsforImpliedVolatilityWiththeDiracDeltaFamilyMethod.J.FuturesMarkets 2025,45,e70024. https://doi.org/10.1002/fut.70024

-

[3]

Jäckel,P.Let’sBeRational.Wilmott2017,2015,40–53. https://doi.org/10.1002/wilm.10395

-

[4]

Availableonline: https://chasethedevil

LeFloc’h,F.MonotonicityoftheBlack–ScholesOptionPricesinPractice. Availableonline: https://chasethedevil. github.io/post/vol_monotonicity_in_practice/(accessedon19May2026)

-

[5]

Faster Monotone Implied Volatility Solver

LeFloc’h,F.FasterMonotoneImpliedVolatilitySolver. Availableonline: https://arxiv.org/abs/2605.22427(2026)

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[6]

Availableonline: https://ssrn.com/abstract=952727 (accessedon1May2026)

Li,M.YouDon’tHavetoBotherNewtonforImpliedVolatility. Availableonline: https://ssrn.com/abstract=952727 (accessedon1May2026)

-

[7]

An Explicit Implied Volatility Formula.Int

Stefanica, D.; Radoičić, R. An Explicit Implied Volatility Formula.Int. J. Theor. Appl. Finance2017,20, 1750048. https://doi.org/10.1142/S0219024917500480

-

[8]

Choi, J.; Huh, J.; Su, N. Tighter ‘Uniform Bounds for Black–Scholes Implied Volatility’ and the Applications to Root-Finding.Oper. Res. Lett.2024,57,107189. https://doi.org/10.1016/j.orl.2024.107189

-

[9]

Birnbaum,Z.W.AnInequalityforMill’sRatio.Ann. Math. Statist.1942,13,245–246. https://doi.org/10.1214/aoms/ 1177731611

-

[10]

On Information and Sufficiency,

Sampford, M.R. Some Inequalities on Mill’s Ratio and Related Functions.Ann. Math. Statist.1953,24, 130–132. https://doi.org/10.1214/aoms/1177729093

-

[11]

Abramowitz,M.;Stegun,I.A.HandbookofMathematicalFunctions;NationalBureauofStandards,AppliedMathe- maticsSeries55: Washington,DC,USA,1964

1964

-

[12]

Traub,J.F.IterativeMethodsfortheSolutionofEquations;ChelseaPublishingCompany: NewYork,NY,USA,1982

1982

-

[13]

Householder,A.S.TheNumericalTreatmentofaSingleNonlinearEquation;McGraw-Hill: NewYork,NY,USA,1970

1970

-

[14]

Healy,J.AppliedQuantitativeFinanceforEquityDerivatives,4thed.;self-published,2024

2024

-

[15]

Availableonline: https://ssrn.com/abstract=2420757 (accessedon16May2026)

LeFloc’h,F.FastandAccurateAnalyticBasisPointVolatility. Availableonline: https://ssrn.com/abstract=2420757 (accessedon16May2026). 14

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.