Non-Spanning Identification of Scheduled Event Risk in Option Pricing

Pith reviewed 2026-06-27 05:20 UTC · model grok-4.3

The pith

Non-spanning expiries separate the no-event volatility surface from scheduled event jumps in option pricing.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

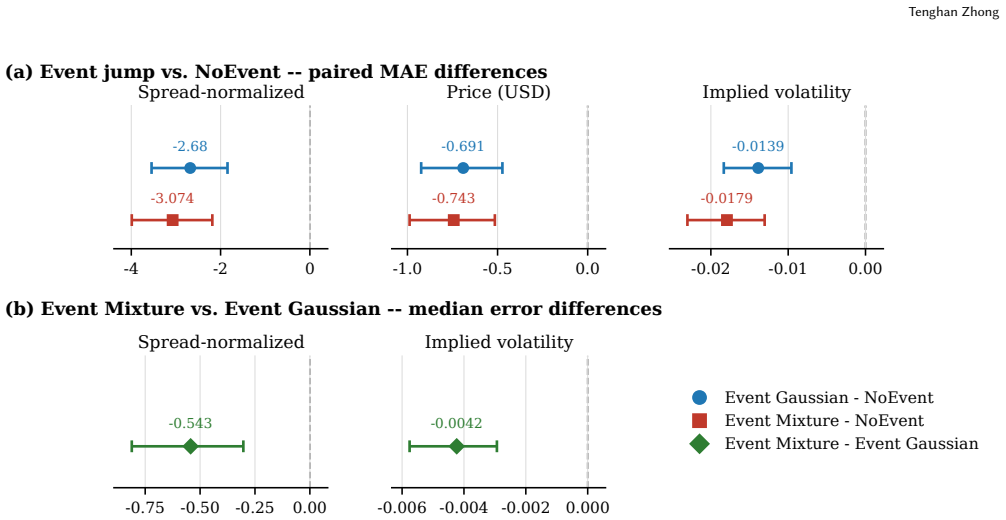

By restricting the no-event volatility surface fit to non-spanning expiries and using event-spanning training quotes only for jump calibration, Gaussian and two-component mixture jumps deliver improved held-out pricing performance on event-spanning SPX options, most notably in robust median errors and non-directional strategies, while a contaminated-surface test demonstrates that absorbing event premia into the surface produces strong but spurious results.

What carries the argument

The non-spanning identification protocol, which fits the continuous volatility surface exclusively on non-event-spanning expiries and calibrates scheduled jumps on event-spanning quotes.

If this is right

- Gaussian and two-component mixture jumps calibrated under the protocol reduce held-out pricing errors on event-spanning quotes.

- The largest improvements appear in robust median errors and in volatility-sensitive combinations such as straddles and strangles rather than directional risk reversals.

- Fitting the no-event surface with event-spanning quotes included produces apparently strong performance by absorbing premia instead of isolating jumps.

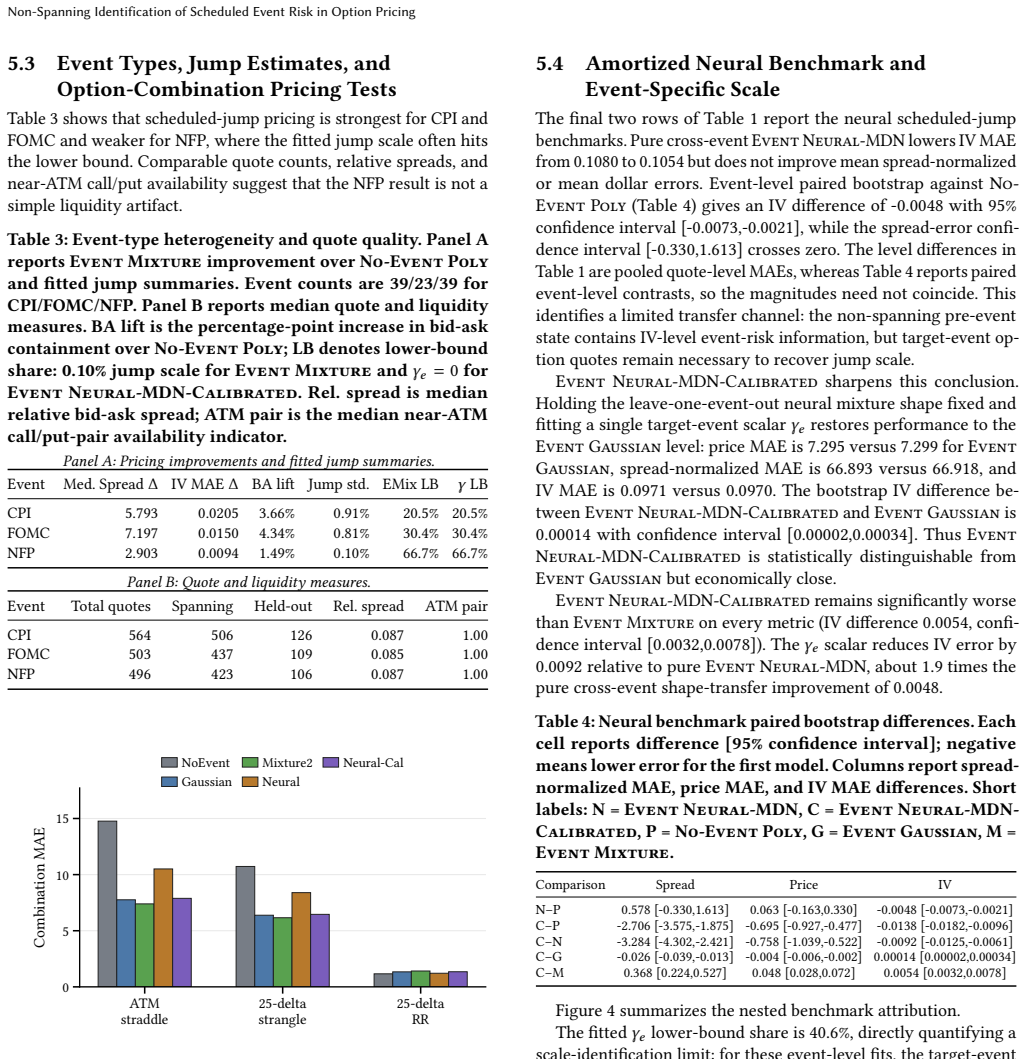

- Scheduled-jump identification performs best for CPI and FOMC events and more weakly for NFP.

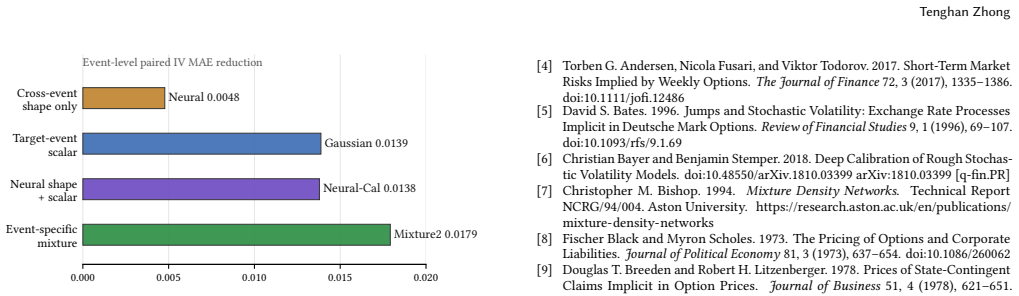

- Amortized mixture models show limited cross-event transfer, with pure leave-one-event-out versions improving some volatility errors but not all pricing metrics.

Where Pith is reading between the lines

- The same non-spanning separation could be tested on single-stock options around earnings dates to isolate firm-specific event risk from the background surface.

- Models that skip this separation may systematically over-attribute price variation around announcements to continuous volatility rather than discrete jumps.

- Extending the protocol to additional announcement types or to intraday option data could further isolate the size and timing of the jump component.

Load-bearing premise

Expiries that avoid scheduled events can produce a volatility surface entirely free of event premia.

What would settle it

A model that fits the no-event surface to a mix of spanning and non-spanning quotes and then matches or exceeds the separated protocol's held-out performance on event quotes without any explicit jump component would falsify the identification claim.

Figures

read the original abstract

Short-dated index options make scheduled macro-announcement risk visible in market prices, but visibility does not imply identification: a flexible no-event surface fitted to event-spanning quotes can absorb event premia, while a jump calibrated without event-spanning quotes is unidentified. To separate the continuous surface from the scheduled jump, we model Federal Open Market Committee (FOMC) decisions, Consumer Price Index (CPI) releases, and nonfarm payroll (NFP) reports as deterministic-time jumps in risk-neutral option pricing and propose a non-spanning identification protocol. Non-spanning expiries identify the no-event volatility surface, event-spanning training quotes calibrate the scheduled jump, and held-out event-spanning quotes are used only for pricing evaluation. On PM-settled S\&P 500 index (SPX) options from May 2022 to August 2025, Gaussian and two-component mixture jumps improve held-out event-spanning pricing, with the clearest gains in robust median pricing errors and in event-volatility option combinations (straddles and strangles) rather than directional risk reversals. A contaminated-surface stress test confirms the identification concern: allowing event-spanning training quotes into the no-event surface fit produces strong held-out performance by absorbing event premia rather than identifying scheduled jump risk. An amortized mixture density network (MDN) benchmark shows limited cross-event transfer: pure leave-one-event-out amortization reduces implied-volatility errors but not mean dollar or mean spread-normalized pricing errors, while the scale-calibrated variant restores Gaussian-level performance yet remains below event-specific mixture calibration. Scheduled-jump identification is strongest for CPI and FOMC and weaker for NFP.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims that scheduled event risk in short-dated index options can be identified separately from the continuous volatility surface using a non-spanning protocol: non-spanning expiries fit the no-event surface, event-spanning training quotes calibrate Gaussian or mixture jump parameters for FOMC, CPI, and NFP events, and held-out event-spanning quotes evaluate pricing performance. Empirical results on PM-settled SPX options from May 2022 to August 2025 show improvements in held-out pricing, particularly robust median errors and event-volatility combinations like straddles and strangles. The contaminated-surface stress test confirms that violating the protocol by allowing event-spanning quotes into the surface fit leads to absorption of event premia rather than genuine identification. Comparisons to amortized MDN benchmarks are also presented.

Significance. If the central claim holds, the work provides a practical and validated method for separating scheduled jump risk from diffusive volatility in option pricing, which is significant for accurate pricing and hedging around macro announcements. The inclusion of a stress test that directly tests the identification vulnerability is a strength, as is the use of held-out data for evaluation and the comparison to machine learning benchmarks. This could influence how event risk is modeled in quantitative finance.

major comments (2)

- [Identification protocol (as described in abstract and methods)] The central assumption that non-spanning expiries identify a clean no-event volatility surface uncontaminated by scheduled event premia is load-bearing for the identification claim; while the contaminated-surface stress test shows the consequence of violation, the manuscript should specify the exact criteria and distance thresholds used to select non-spanning expiries to allow replication and assess robustness.

- [Empirical results on jump calibration] Jump parameters are fitted directly to the event-spanning training quotes, which raises the question of how much of the held-out improvement is due to the non-spanning separation versus the flexibility of the jump model itself; a comparison to fitting jumps without the non-spanning surface would clarify if the protocol adds value beyond the jump specification.

minor comments (2)

- [Abstract] The abstract mentions 'the clearest gains in robust median pricing errors'; it would be helpful to define 'robust median' explicitly or reference the table where it is reported.

- [MDN benchmark] The description of the amortized mixture density network benchmark could include more details on the network architecture and training to facilitate comparison.

Simulated Author's Rebuttal

We thank the referee for the positive evaluation and the recommendation for minor revision. The comments are constructive and we address each one below, indicating the revisions that will be incorporated.

read point-by-point responses

-

Referee: [Identification protocol (as described in abstract and methods)] The central assumption that non-spanning expiries identify a clean no-event volatility surface uncontaminated by scheduled event premia is load-bearing for the identification claim; while the contaminated-surface stress test shows the consequence of violation, the manuscript should specify the exact criteria and distance thresholds used to select non-spanning expiries to allow replication and assess robustness.

Authors: We agree that explicit specification of the selection criteria is required for replication. In the revised manuscript we will add a dedicated paragraph in Section 3 detailing the precise distance thresholds (minimum calendar days from any scheduled event) and any auxiliary filters applied to designate non-spanning expiries. We will also include a short robustness table showing how pricing metrics change when these thresholds are varied by ±2 days. revision: yes

-

Referee: [Empirical results on jump calibration] Jump parameters are fitted directly to the event-spanning training quotes, which raises the question of how much of the held-out improvement is due to the non-spanning separation versus the flexibility of the jump model itself; a comparison to fitting jumps without the non-spanning surface would clarify if the protocol adds value beyond the jump specification.

Authors: The contaminated-surface stress test already isolates the role of the protocol by showing that, when event-spanning quotes are allowed into the surface fit, the model absorbs event premia into the diffusive surface rather than identifying the jump, producing strong in-sample but non-identifying results. To make the incremental contribution of the non-spanning step fully transparent, the revision will add a direct side-by-side benchmark: jump parameters calibrated to event-spanning quotes on top of a contaminated surface versus the same jump model on top of the non-spanning surface, with held-out metrics reported for both. revision: yes

Circularity Check

No significant circularity identified

full rationale

The paper's central protocol separates no-event surface calibration (non-spanning expiries) from jump calibration (event-spanning training quotes) with explicit held-out evaluation and a contaminated-surface stress test that isolates absorption effects. No step reduces a claimed prediction or identification result to its own fitted inputs by construction; the held-out gains and stress-test contrast are independent checks rather than tautological. No self-citation load-bearing steps or ansatz smuggling appear in the described chain.

Axiom & Free-Parameter Ledger

free parameters (1)

- Gaussian and mixture jump parameters

axioms (2)

- standard math Risk-neutral pricing holds for the option surface

- domain assumption Scheduled events occur at deterministic times and can be isolated from the continuous process

Reference graph

Works this paper leans on

-

[1]

Damien Ackerer, Natasa Tagasovska, and Thibault Vatter. 2020. Deep Smooth- ing of the Implied Volatility Surface. InAdvances in Neural Information Processing Systems, Vol. 33. Curran Associates, Inc., Red Hook, NY, USA, 11552–11563. https://proceedings.neurips.cc/paper_files/paper/2020/hash/ 858e47701162578e5e627cd93ab0938a-Abstract.html

2020

-

[2]

Lykourgos Alexiou, Amit Goyal, Alexandros Kostakis, and Leonidas Rompolis

-

[3]

Review of Finance29, 4 (2025), 963–1007

Pricing Event Risk: Evidence from Concave Implied Volatility Curves. Review of Finance29, 4 (2025), 963–1007. doi:10.1093/rof/rfaf016

-

[4]

Andersen, Nicola Fusari, and Viktor Todorov

Torben G. Andersen, Nicola Fusari, and Viktor Todorov. 2015. Parametric In- ference and Dynamic State Recovery from Option Panels.Econometrica83, 3 (2015), 1081–1145. doi:10.3982/ECTA10719

-

[5]

Andersen, Nicola Fusari, and Viktor Todorov

Torben G. Andersen, Nicola Fusari, and Viktor Todorov. 2017. Short-Term Market Risks Implied by Weekly Options.The Journal of Finance72, 3 (2017), 1335–1386. doi:10.1111/jofi.12486

-

[6]

David S. Bates. 1996. Jumps and Stochastic Volatility: Exchange Rate Processes Implicit in Deutsche Mark Options.Review of Financial Studies9, 1 (1996), 69–107. doi:10.1093/rfs/9.1.69

-

[7]

Christian Bayer and Benjamin Stemper. 2018. Deep Calibration of Rough Stochas- tic Volatility Models. doi:10.48550/arXiv.1810.03399 arXiv:1810.03399 [q-fin.PR]

work page internal anchor Pith review Pith/arXiv arXiv doi:10.48550/arxiv.1810.03399 2018

-

[8]

Christopher M. Bishop. 1994.Mixture Density Networks. Technical Report NCRG/94/004. Aston University. https://research.aston.ac.uk/en/publications/ mixture-density-networks

1994

-

[9]

Fischer Black and Myron Scholes. 1973. The Pricing of Options and Corporate Liabilities.Journal of Political Economy81, 3 (1973), 637–654. doi:10.1086/260062

-

[10]

Prices of state-contingent claims implicit in option prices

Douglas T. Breeden and Robert H. Litzenberger. 1978. Prices of State-Contingent Claims Implicit in Option Prices.Journal of Business51, 4 (1978), 621–651. doi:10.1086/296025

-

[11]

Christa Cuchiero, Wahid Khosrawi-Sardroudi, and Josef Teichmann. 2020. A Generative Adversarial Network Approach to Calibration of Local Stochastic Volatility Models.Risks8, 4 (2020), 1–31. doi:10.3390/risks8040101 Article 101

-

[12]

2004.Earnings Announcements and Equity Options

Andrew Dubinsky and Michael Johannes. 2004.Earnings Announcements and Equity Options. Working Paper. Columbia Business School. https://business. columbia.edu/faculty/research/earnings-announcements-and-equity-options

2004

- [13]

-

[14]

Matthias R. Fengler. 2009. Arbitrage-Free Smoothing of the Implied Volatility Surface.Quantitative Finance9, 4 (2009), 417–428. doi:10.1080/14697680802595585

-

[15]

Jim Gatheral and Antoine Jacquier. 2014. Arbitrage-Free SVI Volatility Surfaces. Quantitative Finance14, 1 (2014), 59–71. doi:10.1080/14697688.2013.819986

- [16]

-

[17]

Steven L. Heston. 1993. A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options.Review of Financial Studies6, 2 (1993), 327–343. doi:10.1093/rfs/6.2.327

- [18]

-

[19]

James M. Hutchinson, Andrew W. Lo, and Tomaso Poggio. 1994. A Nonparametric Approach to Pricing and Hedging Derivative Securities via Learning Networks. The Journal of Finance49, 3 (1994), 851–889. doi:10.1111/j.1540-6261.1994.tb00081. x

-

[20]

Londono, Mehrdad Samadi, and Annette Vissing-Jorgensen

Ben Knox, Juan M. Londono, Mehrdad Samadi, and Annette Vissing-Jorgensen

-

[21]

Equity Premium Events. AEA Annual Meeting paper. doi:10.2139/ssrn. 4773692 SSRN version posted April 8, 2024 and last revised August 31, 2025

-

[22]

Shuaiqiang Liu, Cornelis W. Oosterlee, and Sander M. Bohte. 2019. Pricing Options and Computing Implied Volatilities Using Neural Networks.Risks7, 1 (2019), 1–22. doi:10.3390/risks7010016 Article 16

-

[23]

Juan M. Londono and Mehrdad Samadi. 2023.The Price of Macroeconomic Uncer- tainty: Evidence from Daily Options. International Finance Discussion Paper 1376. Board of Governors of the Federal Reserve System. doi:10.17016/IFDP.2023.1376

-

[24]

Juan M. Londono and Mehrdad Samadi. 2025. Which Days Matter for Global Equity Markets? Using Options to Price Events in the Global Calendar. FEDS Notes, Board of Governors of the Federal Reserve System. doi:10.17016/2380- 7172.3908

-

[25]

Robert C. Merton. 1976. Option Pricing When Underlying Stock Returns Are Discontinuous.Journal of Financial Economics3, 1–2 (1976), 125–144. doi:10. 1016/0304-405X(76)90022-2

1976

-

[26]

Viktor Todorov and Yang Zhang. 2022. Information Gains from Using Short- Dated Options for Measuring and Forecasting Volatility.Journal of Applied Econometrics37, 2 (2022), 368–391. doi:10.1002/jae.2864

-

[27]

Ruben Wiedemann, Antoine Jacquier, and Lukas Gonon. 2025. Operator Deep Smoothing for Implied Volatility. Thirteenth International Conference on Learn- ing Representations. https://proceedings.iclr.cc/paper_files/paper/2025/hash/ f115f619b62833aadc5acb058975b0e6-Abstract-Conference.html

2025

-

[28]

Jonathan H. Wright. 2020.Event-Day Options. Working Paper 28306. National Bureau of Economic Research. doi:10.3386/w28306

-

[29]

Yongxin Yang, Wenqi Chen, Chao Shu, and Timothy Hospedales. 2025. Hy- perIV: Real-Time Implied Volatility Smoothing. InProceedings of the 42nd In- ternational Conference on Machine Learning (Proceedings of Machine Learning Research, Vol. 267). PMLR, Vancouver, Canada, 70550–70564. https://proceedings. mlr.press/v267/yang25d.html

2025

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.