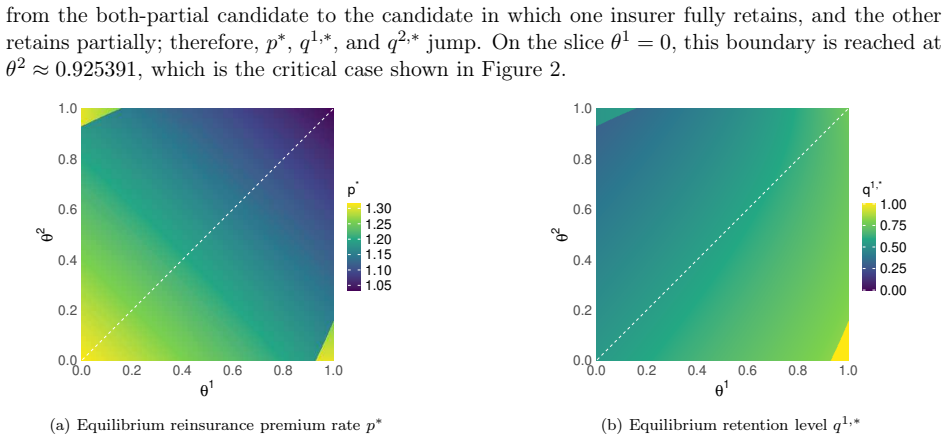

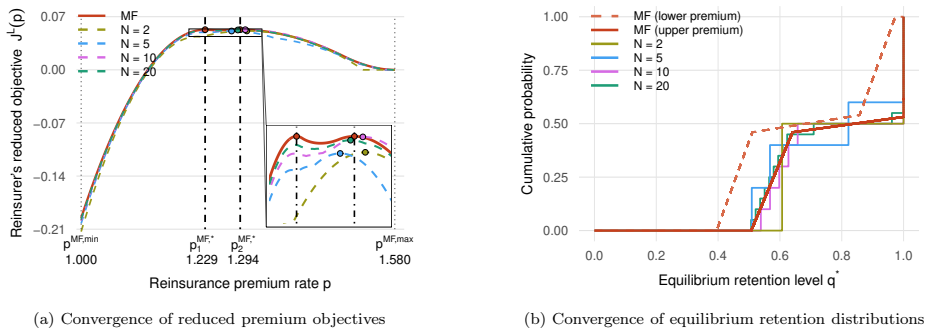

Endogenous Reinsurance Pricing in Large Competitive Insurance Markets: Finite-Player and Mean Field Analysis

Pith reviewed 2026-06-26 01:29 UTC · model grok-4.3

The pith

Relative performance concerns among insurers generate a spillover mechanism that produces a threshold retention structure, reducing the reinsurer's Stackelberg pricing problem to one-dimensional optimization over a compact interval.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

For any fixed premium the insurers' Nash equilibrium retention levels solve a scalar fixed-point equation; the solution is monotone in the premium and therefore partitions the premium axis into three intervals in which all insurers fully cede, retain partially, or retain fully. The reinsurer, acting as Stackelberg leader, optimizes its premium over the compact interval delimited by the two critical thresholds, producing equilibria for both finite populations and the corresponding mean-field model; finite equilibria converge to mean-field equilibria without any uniqueness assumption on the limit premium.

What carries the argument

scalar fixed-point equation whose monotone solution induces a three-regime threshold structure in retention as a function of premium

If this is right

- The reinsurer's optimization reduces to a search over a single compact interval rather than over all possible retention configurations.

- A threshold-continuation algorithm computes finite-player equilibria without enumerating retention patterns.

- Finite-player equilibria converge to mean-field equilibria without requiring uniqueness of the limiting premium.

- Relative-performance concerns can produce strictly positive retention even when reinsurance is offered at an actuarially favorable rate.

- Heterogeneity in insurer risk profiles amplifies the spillover effects that shift the location of the retention thresholds.

Where Pith is reading between the lines

- The same fixed-point reduction may allow similar Stackelberg analyses in other markets where agents care about relative performance, such as asset-management tournaments.

- Regulatory caps on reinsurance premiums could be mapped directly onto the threshold intervals to predict which retention regime prevails.

- The continuation procedure offers a template for computing equilibria in other mean-field games whose best responses admit scalar fixed-point representations.

- If claim risks are correlated across insurers, the scalar fixed point would become a vector fixed point whose dimension equals the number of distinct risk classes.

Load-bearing premise

For every fixed premium the insurers' game possesses an equilibrium retention vector that reduces to a scalar fixed point whose solution increases with premium through the claimed full-cession, partial-retention, and full-retention regimes.

What would settle it

Fix two insurers with different risk exposures, compute their best-response retention functions explicitly, and verify whether their intersection crosses from full cession to partial retention to full retention at two distinct premium thresholds.

Figures

read the original abstract

We study endogenous reinsurance pricing in a competitive insurance market with one strategic reinsurer and many heterogeneous insurers. The reinsurer acts as a Stackelberg leader by choosing a common premium rate and an investment strategy, while insurers decide how much risk to retain and how to invest, taking into account their own performance, their performance relative to the insurer population, and common insurance-claim and financial-market noise. This creates a feedback loop absent from standard reinsurance models with exogenous premiums: a premium change affects insurers directly through the cost of reinsurance, and indirectly through the population's aggregate exposure to common insurance-claim risk. For a fixed premium, we characterize the insurers' equilibrium retention through a scalar fixed point and establish its monotone premium response. This characterization reveals a spillover mechanism generated by relative performance concerns and leads to a threshold structure in which insurers move from full cession to partial retention and then to full retention as the premium increases. Using this structure, we reduce the reinsurer's premium problem to a one-dimensional optimization over a compact premium interval and characterize Stackelberg equilibria in both finite-player and mean field models. In the finite-player case, we develop an efficient threshold continuation procedure that determines equilibrium premiums without enumerating all retention configurations. We also prove convergence from finite-player equilibria to mean field equilibria without requiring the mean field equilibrium premium to be unique. Numerical illustrations show how relative performance concerns amplify spillover effects and can induce retention even when reinsurance remains actuarially favorable. They also demonstrate that Stackelberg equilibria need not be unique in either setting.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper models endogenous reinsurance pricing as a Stackelberg game between one strategic reinsurer (choosing premium and investment) and many heterogeneous insurers (choosing retention and investment) who care about both absolute and relative performance under common claim and market noise. For fixed premium the insurers' game is reduced to a scalar fixed-point equation whose solution is shown to be monotone in premium and to exhibit a three-regime threshold structure (full cession, partial retention, full retention). This structure reduces the reinsurer's problem to one-dimensional optimization over a compact interval; finite-player and mean-field Stackelberg equilibria are characterized, an efficient threshold-continuation algorithm is given for the finite case, and convergence of finite-player equilibria to mean-field equilibria is proved without requiring uniqueness of the mean-field premium. Numerical examples illustrate amplification of spillovers by relative-performance concerns.

Significance. If the fixed-point characterization, monotonicity, and convergence results hold, the work supplies a tractable endogenous-pricing framework that captures feedback absent from exogenous-premium models and yields concrete computational and comparative-static tools. The reduction to scalar fixed point and the convergence statement that does not presuppose uniqueness of the mean-field equilibrium are genuine technical strengths.

minor comments (3)

- The abstract and introduction should state the precise regularity conditions (e.g., moment bounds on claim sizes, Lipschitz constants on the relative-performance term) that guarantee existence and uniqueness of the scalar fixed point for each premium; without these the threshold-structure claim is difficult to verify from the high-level description alone.

- Numerical section: parameter values, grid sizes, and convergence tolerances used to generate the figures should be reported explicitly so that the spillover-amplification and non-uniqueness observations can be reproduced.

- Notation for the mean-field measure and the finite-N empirical measure should be introduced once and used consistently; occasional switches between P^N and the limiting P create minor ambiguity in the convergence argument.

Simulated Author's Rebuttal

We thank the referee for the careful reading, positive summary, and recommendation of minor revision. No major comments were raised in the report.

Circularity Check

No significant circularity in derivation chain

full rationale

The paper's central steps—characterizing insurer equilibrium retention via a scalar fixed point for fixed premium, establishing monotone response and threshold structure from relative performance concerns plus common noise, then reducing the reinsurer's Stackelberg problem to 1D optimization over a compact interval—are presented as derived directly from the game setup. No quoted reduction equates a claimed prediction or result to its inputs by construction, no fitted parameters are relabeled as predictions, and no load-bearing self-citation or imported uniqueness theorem appears in the provided text. The finite-player to mean-field convergence is stated without requiring uniqueness of the mean-field premium. This aligns with standard mean-field game analysis and remains self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Existence of Nash equilibrium in the insurers' retention game for any fixed premium

- domain assumption Common insurance-claim and financial-market noise affecting all insurers

Reference graph

Works this paper leans on

-

[1]

Controlled diffusion models for optimal dividend pay-out

Søren Asmussen and Michael Taksar. Controlled diffusion models for optimal dividend pay-out. Insurance: Mathematics and Economics , 20(1):1–15, 1997

1997

-

[2]

A hybrid stochastic differential reinsurance and investment game with bounded m emory

Yanfei Bai, Zhongbao Zhou, Helu Xiao, Rui Gao, and Feimin Z hong. A hybrid stochastic differential reinsurance and investment game with bounded m emory. European Journal of Operational Research, 296:717–737, 2022

2022

-

[3]

A mean field game appro ach to optimal investment and risk control for competitive insurers

Lijun Bo, Shihua Wang, and Chao Zhou. A mean field game appro ach to optimal investment and risk control for competitive insurers. Insurance: Mathematics and Economics , 116:202–217, 2024

2024

-

[4]

Optimal investment policies for a firm with a ra ndom risk process: Exponential utility and minimizing the probability of ruin

Sid Browne. Optimal investment policies for a firm with a ra ndom risk process: Exponential utility and minimizing the probability of ruin. Mathematics of Operations Research, 20(4):937– 958, 1995

1995

-

[5]

Young, and Bin Zou

Jingyi Cao, Dongchen Li, Virginia R. Young, and Bin Zou. Co -opetition in reinsurance mar- kets: When Pareto meets Stackelberg and Nash. Insurance: Mathematics and Economics , 125:103133, 2025

2025

-

[6]

Stochastic Stackelberg differenti al reinsurance games under time- inconsistent mean-variance framework

Lv Chen and Yang Shen. Stochastic Stackelberg differenti al reinsurance games under time- inconsistent mean-variance framework. Insurance: Mathematics and Economics , 88:120–137, 2019. 44

2019

-

[7]

Optimal inves tment under relative performance concerns

Gilles-Edouard Espinosa and Nizar Touzi. Optimal inves tment under relative performance concerns. Mathematical Finance, 25(2):221–257, 2015

2015

-

[8]

Gerber and Gérard Pafumi

Hans U. Gerber and Gérard Pafumi. Utility functions: Fro m risk theory to finance. North American Actuarial Journal , 2(3):74–91, 1998

1998

-

[9]

Time-consistent investment an d reinsurance strategies for mean-variance insurers in N -agent and mean-field games

Guohui Guan and Xiang Hu. Time-consistent investment an d reinsurance strategies for mean-variance insurers in N -agent and mean-field games. North American Actuarial Jour- nal, 26(4):537–569, 2022

2022

-

[10]

Mean fiel d and n-insurers games for robust optimal reinsurance-investment in correlated markets

Yong He, Lin He, Dengsheng Chen, and Zhezhi Liu. Mean fiel d and n-insurers games for robust optimal reinsurance-investment in correlated markets. Journal of Industrial and Management Optimization, 19(9):6806–6825, 2023

2023

-

[11]

Caines, and Roland P

Minyi Huang, Peter E. Caines, and Roland P. Malhamé. Lar ge-population cost-coupled LQG problems with nonuniform agents: Individual-mass behavio r and decentralized ε-nash equilib- ria. IEEE Transactions on Automatic Control , 52(9):1560–1571, 2007

2007

-

[12]

Malhamé, and Peter E

Minyi Huang, Roland P. Malhamé, and Peter E. Caines. Lar ge population stochastic dynamic games: Closed-loop McKean–Vlasov systems and the Nash cert ainty equivalence principle. Communications in Information and Systems , 6(3):221–252, 2006

2006

-

[13]

Iglehart

Donald L. Iglehart. Diffusion approximations in collec tive risk theory. Journal of Applied Probability, 6(2):285–292, 1969

1969

-

[14]

Mean field and n-agent games for optimal investment under relative performance criteria

Daniel Lacker and Thaleia Zariphopoulou. Mean field and n-agent games for optimal investment under relative performance criteria. Mathematical Finance, 29(4):1003–1038, 2019

2019

-

[15]

Jeux à champ moyen

Jean-Michel Lasry and Pierre-Louis Lions. Jeux à champ moyen. I – Le cas stationnaire. Comptes Rendus Mathématique , 343(9):619–625, 2006

2006

-

[16]

Jeux à champ moyen

Jean-Michel Lasry and Pierre-Louis Lions. Jeux à champ moyen. II – Horizon fini et contrôle optimal. Comptes Rendus Mathématique , 343(10):679–684, 2006

2006

-

[17]

Mean field ga mes

Jean-Michel Lasry and Pierre-Louis Lions. Mean field ga mes. Japanese Journal of Mathematics , 2(1):229–260, 2007

2007

-

[18]

Danping Li and Virginia R. Young. Stackelberg different ial game for reinsurance: Mean- variance framework and random horizon. Insurance: Mathematics and Economics , 102:42–55, 2022

2022

-

[19]

A two-layer stochasti c game approach to reinsurance contracting and competition

Zongxia Liang, Yi Xia, and Bin Zou. A two-layer stochasti c game approach to reinsurance contracting and competition. Insurance: Mathematics and Economics , 119:226–237, 2024

2024

-

[20]

A Stackelberg mean field game approach to optimal reinsurance and investment: One reinsu rer and competitive insurers, 2024

Shuhua Zhang, Shenghua Qian, Xinyu Wang, and Xinyi Kang . A Stackelberg mean field game approach to optimal reinsurance and investment: One reinsu rer and competitive insurers, 2024. SSRN Working Paper. 45

2024

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.