The Remittance Blueprint: Data-driven Intelligence for Sri Lanka

Pith reviewed 2026-06-29 04:31 UTC · model grok-4.3

The pith

Remittance inflows to Sri Lanka are driven primarily by exchange rate movements and global oil prices rather than domestic economic indicators.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

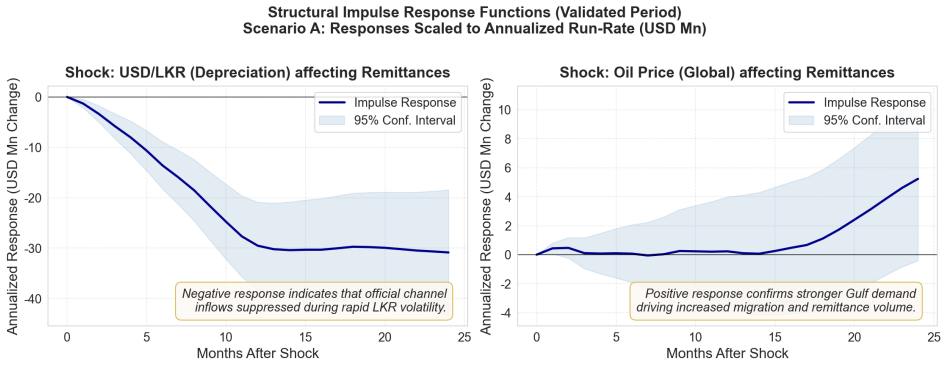

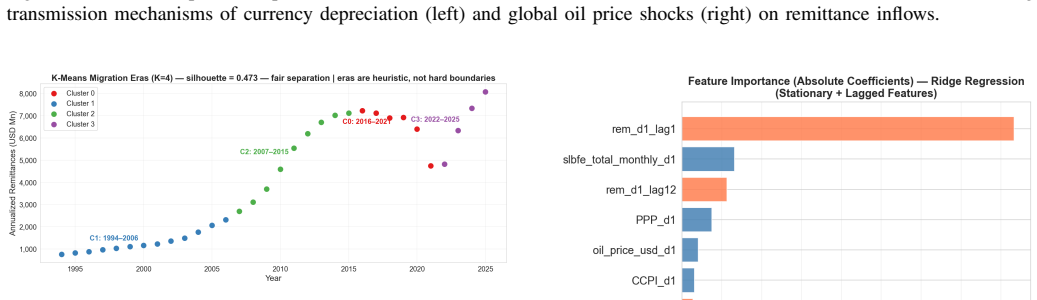

Remittance inflows are primarily driven by external macroeconomic variables, specifically exchange rate dynamics and global oil prices, rather than domestic indicators. Impulse response analysis confirms the asymmetric impact of currency depreciation and oil price shocks. Multivariate machine learning models outperform traditional univariate approaches, with Ridge Regression achieving a 73.8 percent accuracy improvement over SARIMA, and the framework projects 2026 remittances at 9,001 million USD under stable conditions.

What carries the argument

Vector autoregression and vector error correction models combined with supervised regression learners applied to a 384-month harmonized dataset after ADF and Johansen stationarity corrections.

If this is right

- Exchange rate stability becomes a direct lever for remittance predictability.

- Oil price shocks produce lasting asymmetric effects on inflow volumes.

- Skilled migration and formal financial channels gain priority as resilience measures.

- Univariate forecasting methods systematically underperform for policy planning.

Where Pith is reading between the lines

- Countries with similar migrant profiles may exhibit comparable external dependence in remittance data.

- Efforts to boost domestic employment could indirectly affect remittances only through migration rates rather than through income effects.

- Policy makers could test hedging instruments tied to oil prices to offset remittance volatility.

Load-bearing premise

The 384-month dataset accurately captures the underlying relationships after stationarity corrections and that the chosen external variables are not themselves driven by unmodeled domestic factors or reverse causality.

What would settle it

An analysis that attributes more explanatory power to domestic variables such as unemployment or fiscal policy than to exchange rates and oil prices when modeling the same remittance series would falsify the central claim.

Figures

read the original abstract

This study analyzes Sri Lankan migration and remittances over 32 years (1994-2025). Using a 384-month harmonized dataset, we apply exploratory data analysis, stationarity corrected time-series modeling (ADF, Johansen, VAR/VECM), and supervised learning. Results reveal remittance inflows are primarily driven by external macroeconomic variables, specifically exchange rate dynamics and global oil prices, rather than domestic indicators. Impulse response analysis confirms the asymmetric impact of currency depreciation and oil price shocks. Predictively, multivariate machine learning models outperform traditional univariate approaches; Ridge Regression achieves a 73.8% accuracy improvement over SARIMA (Annualized RMSE: USD 494.8 Mn). The optimized framework projects 2026 remittances at USD 9,001 million under stable conditions. These findings highlight the structural dependence of remittances on global economies, emphasizing the need for robust exchange rate policies, skilled migration, and formal financial channels to enhance long-term economic resilience.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper analyzes Sri Lankan remittance inflows over 32 years (1994-2025) with a 384-month harmonized dataset. It applies EDA, ADF/Johansen tests, VAR/VECM modeling with impulse responses, and supervised ML. The central claim is that remittances are primarily driven by external variables (exchange rates, oil prices) rather than domestic indicators, with asymmetric shock impacts; Ridge Regression achieves 73.8% accuracy improvement over SARIMA (RMSE USD 494.8 Mn), and the model projects 2026 remittances at USD 9,001 million under stable conditions.

Significance. If the identification and validation gaps are closed, the work could offer policy-relevant evidence on Sri Lanka's structural dependence on global factors, with the ML-forecasting component providing a practical extension of the econometric results. The projection supplies a concrete, falsifiable output, and the emphasis on external drivers aligns with small-open-economy intuition, but these strengths are currently undercut by the absence of identification and full reporting.

major comments (2)

- [VAR/VECM and Impulse Response Analysis] VAR/VECM and impulse-response sections: no identification scheme (recursive ordering, sign restrictions, or instruments) is reported to establish exogeneity of exchange-rate and oil-price shocks. In a small open economy, remittances can affect the exchange rate via foreign-currency supply, so the claim that external variables are the primary drivers cannot be isolated from reverse causality without this step.

- [Results and Model Comparisons] Results section (model comparisons and projection): the abstract states a 73.8 % accuracy gain and specific RMSE for Ridge Regression, yet no coefficient tables, out-of-sample validation details, or robustness checks are supplied, preventing evaluation of the multivariate-versus-univariate claim or the 2026 projection.

minor comments (2)

- [Data and Methods] The 384-month dataset harmonization procedure (sources, interpolation, or handling of 2025 observations) is not described in sufficient detail for replication.

- [Projection and Policy Implications] The projection assumes 'stable conditions' without specifying the exact exogenous paths or conducting sensitivity checks around those assumptions.

Simulated Author's Rebuttal

We thank the referee for the constructive comments, which identify key areas where additional rigor is needed. We address each major comment below and indicate the revisions that will be incorporated.

read point-by-point responses

-

Referee: [VAR/VECM and Impulse Response Analysis] VAR/VECM and impulse-response sections: no identification scheme (recursive ordering, sign restrictions, or instruments) is reported to establish exogeneity of exchange-rate and oil-price shocks. In a small open economy, remittances can affect the exchange rate via foreign-currency supply, so the claim that external variables are the primary drivers cannot be isolated from reverse causality without this step.

Authors: We agree that the absence of an explicit identification scheme limits the ability to isolate causal effects and rule out reverse causality from remittances to the exchange rate. The current manuscript reports reduced-form VAR/VECM estimates and impulse responses without specifying any ordering, sign restrictions, or instruments. In the revised version we will introduce a recursive Cholesky identification with exchange rate and oil prices ordered first, consistent with small-open-economy timing assumptions, and will present the identified impulse responses together with a discussion of how this affects the interpretation of external drivers. revision: yes

-

Referee: [Results and Model Comparisons] Results section (model comparisons and projection): the abstract states a 73.8 % accuracy gain and specific RMSE for Ridge Regression, yet no coefficient tables, out-of-sample validation details, or robustness checks are supplied, preventing evaluation of the multivariate-versus-univariate claim or the 2026 projection.

Authors: We acknowledge that the results section does not provide coefficient tables, a clear description of the out-of-sample validation procedure, or robustness checks, which prevents independent assessment of the reported accuracy gains and the 2026 projection. In the revision we will add (i) coefficient tables for both the VAR/VECM and the Ridge Regression model, (ii) explicit details on the train-test split and any cross-validation used to obtain the 73.8 % improvement and RMSE of USD 494.8 Mn, and (iii) robustness checks including alternative lag orders, subsample stability, and sensitivity of the 2026 projection to different assumptions, accompanied by uncertainty bands. revision: yes

Circularity Check

No circularity: standard econometric pipeline on external data

full rationale

The paper applies ADF/Johansen tests, VAR/VECM impulse responses, and Ridge Regression on a 384-month dataset to attribute remittances to exchange rates and oil prices, then projects 2026 values. No quoted equations, self-citations, or steps reduce any reported prediction or claim to a fitted constant or prior result by construction. The multivariate forecast is an output of the fitted model rather than an input renamed as prediction. The chain is self-contained against the stated data and methods.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Sri lanka’s labour migration trends, remittances and economic growth,

S. S. Ramanayake and C. S. Wijetunga, “Sri lanka’s labour migration trends, remittances and economic growth,”South Asia Research, vol. 38, no. 3 suppl, pp. 61S–81S, 2018

2018

-

[2]

Sri lanka’s labour migration trends, remittances and economic growth,

P. Wickramasekara, “Sri lanka’s labour migration trends, remittances and economic growth,”Geneva: International Labour Organization, 2018

2018

-

[3]

The new economics of labor migration,

O. Stark and D. E. Bloom, “The new economics of labor migration,” The american Economic review, vol. 75, no. 2, pp. 173–178, 1985

1985

-

[4]

Distribution of the estimators for autoregressive time series with a unit root,

D. A. Dickey and W. A. Fuller, “Distribution of the estimators for autoregressive time series with a unit root,”Journal of the American statistical association, vol. 74, no. 366a, pp. 427–431, 1979

1979

-

[5]

Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root?

D. Kwiatkowski, P. C. Phillips, P. Schmidt, and Y . Shin, “Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root?”Journal of econometrics, vol. 54, no. 1-3, pp. 159–178, 1992

1992

-

[6]

Statistical analysis of cointegration vectors,

S. Johansen, “Statistical analysis of cointegration vectors,”Journal of economic dynamics and control, vol. 12, no. 2-3, pp. 231–254, 1988

1988

-

[7]

Co-integration and error correction: representation, estimation, and testing,

R. F. Engle and C. W. Granger, “Co-integration and error correction: representation, estimation, and testing,”Econometrica: journal of the Econometric Society, pp. 251–276, 1987

1987

-

[8]

The hypothesis of the mobility transition,

W. Zelinsky, “The hypothesis of the mobility transition,”Geographical review, pp. 219–249, 1971

1971

-

[9]

The internal dynamics of migration processes: A theoret- ical inquiry,

H. De Haas, “The internal dynamics of migration processes: A theoret- ical inquiry,”Journal of ethnic and migration studies, vol. 36, no. 10, pp. 1587–1617, 2010

2010

-

[10]

A rank-invariant method of linear and polynomial regression analysis,

H. Theil, “A rank-invariant method of linear and polynomial regression analysis,”Indagationes mathematicae, vol. 12, no. 85, p. 173, 1950

1950

-

[11]

Estimates of the regression coefficient based on kendall’s tau,

P. K. Sen, “Estimates of the regression coefficient based on kendall’s tau,”Journal of the American statistical association, vol. 63, no. 324, pp. 1379–1389, 1968

1968

-

[12]

O. C. Herfindahl,Concentration in the steel industry. Columbia university, 1997

1997

-

[13]

The Potential of Mobile Network Big Data as a Tool in Colombo’s Transportation and Urban Planning,

S. Lokanathan, G. E. Kreindler, N. H. N. de Silva, Y . Miyauchi, D. Dhananjaya, and R. Samarajiva, “The Potential of Mobile Network Big Data as a Tool in Colombo’s Transportation and Urban Planning,” Information Technologies & International Development, vol. 12, no. 2, pp. pp–63, 2016

2016

-

[14]

Using Mobile Network Big Data for Informing Transportation and Urban Planning in Colombo,

S. Lokanathan, N. de Silva, G. Kreindler, Y . Miyauchi, and D. Dhanan- jaya, “Using Mobile Network Big Data for Informing Transportation and Urban Planning in Colombo,” November 2014

2014

-

[15]

Individual comparisons by ranking methods,

F. Wilcoxon, “Individual comparisons by ranking methods,” inBreak- throughs in statistics: Methodology and distribution. Springer, 1992, pp. 196–202

1992

-

[16]

A cluster separation measure,

D. L. Davies and D. W. Bouldin, “A cluster separation measure,”IEEE transactions on pattern analysis and machine intelligence, no. 2, pp. 224–227, 1979

1979

-

[17]

A dendrite method for cluster analysis,

T. Cali ´nski and J. Harabasz, “A dendrite method for cluster analysis,” Communications in Statistics-theory and Methods, vol. 3, no. 1, pp. 1– 27, 1974

1974

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.