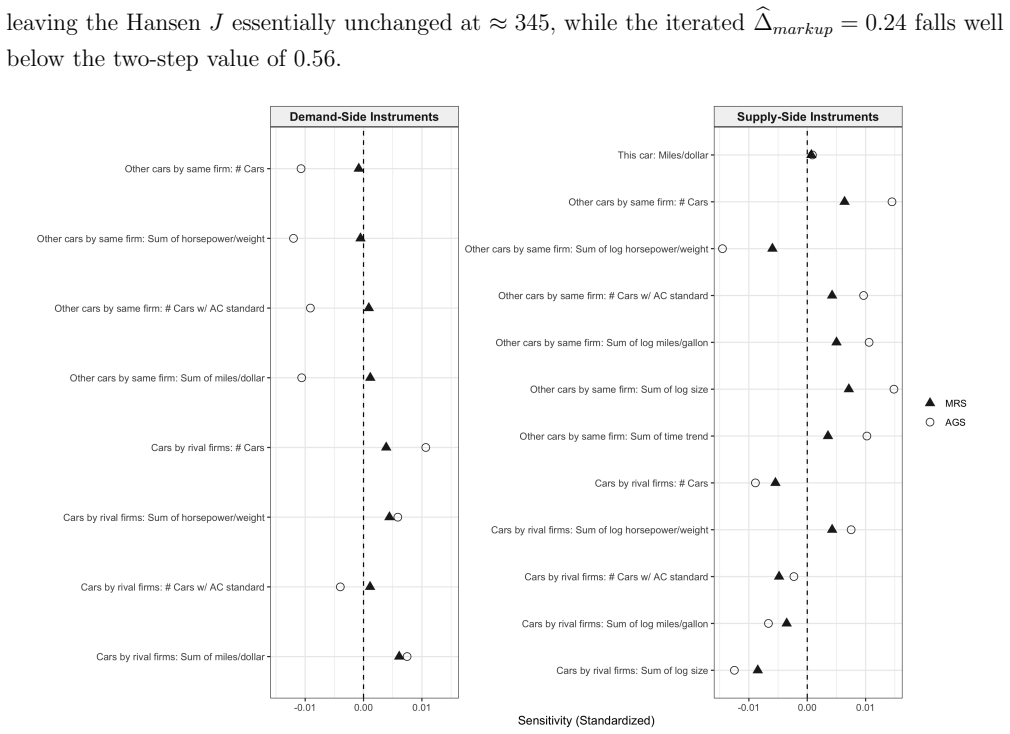

Sensitivity, Informativeness, and Misspecification in GMM Estimation

Pith reviewed 2026-06-30 04:03 UTC · model grok-4.3

The pith

Misspecification can lower the share of GMM estimator variance explained by the moments even when the J-test does not reject.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The informativeness Delta measures the share of an estimator's asymptotic variance explained by sampling variation in the moments. It equals one under correct specification and can fall below one under misspecification even when the Hansen J-test does not reject. The associated sensitivity matrix nests the Andrews-Gentzkow-Shapiro matrix under correct specification. Influence-function representations are derived for one-step, two-step, iterated, and continuously updating GMM. In minimum-distance problems the optimal weight matrix adds estimator variance that the moments do not explain, lowering Delta, whereas simpler weights largely preserve it.

What carries the argument

The informativeness measure Delta, defined as the share of asymptotic variance attributable to moment sampling variation and evaluated at pseudo-true values.

If this is right

- In minimum-distance estimation the optimal weight matrix reduces informativeness by adding variance the moments do not explain.

- Simpler weight matrices largely avoid that variance addition and therefore maintain higher Delta.

- Misspecification can reorder the sensitivity rankings of different parameters.

- Delta can detect structural-efficiency losses that the Hansen J-test does not flag.

Where Pith is reading between the lines

- Reporting Delta alongside the J-test would give practitioners a direct gauge of how much of the reported precision is actually coming from the data moments.

- The same informativeness logic could be applied to other moment-based estimators such as IV or minimum-distance problems outside GMM.

- When Delta is low, model refinement or additional moments may be warranted even if the J-test passes.

- The efficiency-informativeness trade-off suggests that the conventional preference for the optimal weight matrix should be weighed against the loss in Delta in each application.

Load-bearing premise

The derivations assume well-defined pseudo-true values exist and that standard regularity conditions hold for the asymptotic expansions of the GMM estimators.

What would settle it

A simulation or empirical example in which the model is misspecified, the J-test does not reject, yet the computed Delta remains exactly equal to one.

Figures

read the original abstract

This paper develops misspecification-robust sensitivity and informativeness diagnostics for GMM estimators, evaluated at pseudo-true values. The sensitivity matrix nests that of Andrews, Gentzkow, and Shapiro (2017) under correct specification. The informativeness $\Delta$ measures the share of an estimator's asymptotic variance explained by sampling variation in the moments, a notion of structural efficiency that equals one under correct specification and can fall below one under misspecification, even when the Hansen $J$-test does not reject. We derive influence-function representations for one-step, two-step, iterated, and continuously updating GMM. We show that in minimum-distance estimation, estimating the optimal weight matrix adds estimator variance that the moments do not explain, lowering informativeness, while simpler weight matrices largely avoid it. The choice of weight matrix therefore involves a trade-off between classical efficiency and informativeness. In applications to the automobile demand model of Berry, Levinsohn, and Pakes (1995), the consumption insurance model of Blundell, Pistaferri, and Preston (2008), and the income-and-democracy regressions of Acemoglu, Johnson, Robinson, and Yared (2008), misspecification reorders sensitivity rankings, simpler weights preserve the informativeness that the optimal weight loses, and $\Delta$ detects structural-efficiency losses that the $J$-test does not.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops misspecification-robust sensitivity and informativeness diagnostics for GMM estimators evaluated at pseudo-true values. The sensitivity matrix nests that of Andrews, Gentzkow, and Shapiro (2017) under correct specification. The informativeness measure Δ quantifies the share of an estimator's asymptotic variance explained by sampling variation in the moments; it equals one under correct specification and can fall below one under misspecification even when the Hansen J-test does not reject. Influence-function representations are derived for one-step, two-step, iterated, and continuously updating GMM. Applications to the BLP automobile demand model, Blundell-Pistaferri-Preston consumption insurance model, and Acemoglu-Johnson-Robinson-Yared income-democracy regressions illustrate that misspecification reorders sensitivity rankings, simpler weights preserve informativeness lost with optimal weights, and Δ detects structural-efficiency losses missed by the J-test.

Significance. If the derivations hold, the paper supplies useful misspecification-robust tools that extend sensitivity analysis and introduce a direct decomposition-based measure of structural efficiency. The explicit influence-function derivations for multiple GMM variants under standard regularity conditions (pseudo-true values, differentiability, positive-definiteness) are a clear strength and support implementation. The applications demonstrate concrete consequences for sensitivity rankings and the efficiency-informativeness trade-off in weight-matrix choice. These contributions are proportionate to the claims and add diagnostic value beyond the J-test when the central expressions are free of post-hoc adjustments.

minor comments (3)

- [§2.2] §2.2, definition of Δ: the decomposition is presented as direct from the asymptotic variance; a short remark confirming that no additional normalization is imposed would aid readers.

- [Table 2] Table 2 (BLP application): the reported Δ values for optimal vs. identity weighting would benefit from a column showing the associated standard errors or bootstrap intervals to assess precision of the informativeness gap.

- [§6.3] §6.3 (income-democracy application): the text notes reordering of sensitivity rankings but does not report the numerical sensitivity matrix entries; adding these (or a supplementary table) would make the reordering claim easier to verify.

Simulated Author's Rebuttal

We thank the referee for the careful and positive assessment of the manuscript. The summary accurately reflects the paper's contributions on misspecification-robust sensitivity measures and the informativeness statistic Δ for GMM. We appreciate the recommendation for minor revision and the recognition that the influence-function derivations and applications add diagnostic value beyond the J-test.

Circularity Check

No significant circularity; Δ defined from standard asymptotic decomposition

full rationale

The paper defines the informativeness Δ explicitly as the share of asymptotic variance attributable to moment sampling variation, derived via standard influence-function expansions under regularity conditions (pseudo-true values, differentiability, positive-definiteness of Jacobian and weight matrix). These conditions are the usual ones for GMM asymptotics under misspecification and are not derived from or equivalent to the paper's target results. The nesting of the Andrews-Gentzkow-Shapiro sensitivity matrix is a direct algebraic consequence under correct specification, not a self-referential fit. No self-citations are load-bearing; no parameter is fitted to data and then relabeled a prediction; no uniqueness theorem or ansatz is smuggled via prior work by the same authors. The derivation chain is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Standard regularity conditions for GMM asymptotics hold at the pseudo-true values.

invented entities (1)

-

Informativeness measure Δ

no independent evidence

Reference graph

Works this paper leans on

-

[1]

and Segal, Lewis M

Altonji, Joseph G. and Segal, Lewis M. , journal =. Small-sample bias in. 1996 , publisher =

1996

-

[2]

Journal of Econometrics , volume =

The large sample behaviour of the generalized method of moments estimator in misspecified models , author =. Journal of Econometrics , volume =. 2003 , publisher =

2003

-

[3]

arXiv preprint , year =

Sensitivity of regular estimators , author =. arXiv preprint , year =

-

[4]

The Annals of Statistics , volume =

Point estimation with exponentially tilted empirical likelihood , author =. The Annals of Statistics , volume =

-

[5]

The Quarterly Journal of Economics , volume =

Measuring the sensitivity of parameter estimates to estimation moments , author =. The Quarterly Journal of Economics , volume =. 2017 , publisher =

2017

-

[6]

Journal of Econometrics , volume =

A doubly corrected robust variance estimator for linear GMM , author =. Journal of Econometrics , volume =. 2022 , publisher =

2022

-

[7]

Econometrica: Journal of the Econometric Society , pages =

Automobile prices in market equilibrium , author =. Econometrica: Journal of the Econometric Society , pages =. 1995 , publisher =

1995

-

[8]

Quantitative Economics , volume =

The influence function of semiparametric estimators , author =. Quantitative Economics , volume =. 2022 , publisher =

2022

-

[9]

The review of economic studies , volume =

Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations , author =. The review of economic studies , volume =. 1991 , publisher =

1991

-

[10]

Journal of the Royal Statistical Society: Series B (Methodological) , volume =

Assessing sensitivity to an unobserved binary covariate in an observational study with binary outcome , author =. Journal of the Royal Statistical Society: Series B (Methodological) , volume =. 1983 , publisher =

1983

-

[11]

Quantitative Economics , volume =

Minimizing sensitivity to model misspecification , author =. Quantitative Economics , volume =. 2022 , publisher =

2022

-

[12]

Econometrica , volume =

Counterfactual sensitivity and robustness , author =. Econometrica , volume =. 2023 , publisher =

2023

-

[13]

Review of Economics and Statistics , volume =

Sensitivity to calibrated parameters , author =. Review of Economics and Statistics , volume =. 2023 , publisher =

2023

-

[14]

Quantitative Economics , volume =

Sensitivity analysis using approximate moment condition models , author =. Quantitative Economics , volume =. 2021 , publisher =

2021

-

[15]

American Economic Review , volume =

Sensitivity to exogeneity assumptions in program evaluation , author =. American Economic Review , volume =. 2003 , publisher =

2003

-

[16]

Journal of Business & Economic Statistics , volume =

Unobservable selection and coefficient stability: Theory and evidence , author =. Journal of Business & Economic Statistics , volume =. 2019 , publisher =

2019

-

[17]

Journal of the American Statistical Association , year =

Flexible sensitivity analysis for observational studies without observable implications , author =. Journal of the American Statistical Association , year =

-

[18]

Journal of the Royal Statistical Society Series B: Statistical Methodology , volume =

Making sense of sensitivity: Extending omitted variable bias , author =. Journal of the Royal Statistical Society Series B: Statistical Methodology , volume =. 2020 , publisher =

2020

-

[19]

Review of Economics and Statistics , volume =

Plausibly exogenous , author =. Review of Economics and Statistics , volume =. 2012 , publisher =

2012

-

[20]

Journal of Business & Economic Statistics , volume =

A consistent variance estimator for 2sls when instruments identify different lates , author =. Journal of Business & Economic Statistics , volume =. 2018 , publisher =

2018

-

[21]

Econometrica , volume =

Inference for iterated GMM under misspecification , author =. Econometrica , volume =. 2021 , publisher =

2021

-

[22]

Journal of Econometrics , volume =

Asymptotic theory for clustered samples , author =. Journal of Econometrics , volume =. 2019 , publisher =

2019

-

[23]

The Review of Economic Studies , volume =

One-step estimators for over-identified generalized method of moments models , author =. The Review of Economic Studies , volume =. 1997 , publisher =

1997

-

[24]

Journal of econometrics , volume =

A finite sample correction for the variance of linear efficient two-step GMM estimators , author =. Journal of econometrics , volume =. 2005 , publisher =

2005

-

[25]

The Annals of Statistics , pages =

On differentiable functionals , author =. The Annals of Statistics , pages =. 1991 , publisher =

1991

-

[26]

2022 , publisher =

Econometrics , author =. 2022 , publisher =

2022

-

[27]

Journal of econometrics , volume =

On the structure of IV estimands , author =. Journal of econometrics , volume =. 2019 , publisher =

2019

-

[28]

Econometric Society 2025 World Congress Volume , year =

The purpose of an estimator is what it does: Misspecification, estimands, and over-identification , author =. Econometric Society 2025 World Congress Volume , year =

2025

-

[29]

American Economic Review , volume =

Consumption inequality and partial insurance , author =. American Economic Review , volume =. 2008 , publisher =

2008

-

[30]

Journal of the american statistical association , volume =

The influence curve and its role in robust estimation , author =. Journal of the american statistical association , volume =. 1974 , publisher =

1974

-

[31]

Quantitative Economics , volume =

Uncertainty quantification and global sensitivity analysis for economic models , author =. Quantitative Economics , volume =. 2019 , publisher =

2019

-

[32]

The annals of mathematical statistics , volume =

On the asymptotic distribution of differentiable statistical functions , author =. The annals of mathematical statistics , volume =. 1947 , publisher =

1947

-

[33]

Econometrica: Journal of the Econometric Society , pages =

The asymptotic variance of semiparametric estimators , author =. Econometrica: Journal of the Econometric Society , pages =. 1994 , publisher =

1994

-

[34]

Journal of Applied Econometrics , volume =

Estimating household consumption insurance , author =. Journal of Applied Econometrics , volume =. 2021 , publisher =

2021

-

[35]

American Economic Journal: Macroeconomics , volume =

How much consumption insurance beyond self-insurance? , author =. American Economic Journal: Macroeconomics , volume =. 2010 , publisher =

2010

-

[36]

Journal of Econometrics , volume =

Nearly-singular design in GMM and generalized empirical likelihood estimators , author =. Journal of Econometrics , volume =. 2008 , publisher =

2008

-

[37]

2014 , publisher =

Measuring the sensitivity of parameter estimates to sample statistics , author =. 2014 , publisher =

2014

-

[38]

Econometrica , volume =

On the informativeness of descriptive statistics for structural estimates , author =. Econometrica , volume =. 2020 , publisher =

2020

-

[39]

Journal of Economic Dynamics and Control , volume =

What to expect when you're calibrating: Measuring the effect of calibration on the estimation of macroeconomic models , author =. Journal of Economic Dynamics and Control , volume =. 2019 , publisher =

2019

-

[40]

Econometrica: Journal of the econometric society , pages =

Large sample properties of generalized method of moments estimators , author =. Econometrica: Journal of the econometric society , pages =. 1982 , publisher =

1982

-

[41]

Quantitative Economics , volume =

Double robust inference for continuous updating GMM , author =. Quantitative Economics , volume =. 2025 , publisher =

2025

-

[42]

The Rand journal of economics , pages=

Estimating discrete-choice models of product differentiation , author=. The Rand journal of economics , pages=. 1994 , publisher=

1994

-

[43]

American economic review , volume=

Income and democracy , author=. American economic review , volume=. 2008 , publisher=

2008

-

[44]

2009 , publisher=

Matrix mathematics: theory, facts, and formulas , author=. 2009 , publisher=

2009

-

[45]

Econometric theory , volume=

Generic uniform convergence , author=. Econometric theory , volume=. 1992 , publisher=

1992

-

[46]

Working paper , year=

How to weight in moments matching: A new approach and applications to earnings dynamics , author=. Working paper , year=

-

[47]

Journal of the American statistical Association , volume=

Identification of causal effects using instrumental variables , author=. Journal of the American statistical Association , volume=. 1996 , publisher=

1996

-

[48]

Econometrica , volume =

Covariance Matrix Estimation and the Power of the Overidentifying Restrictions Test , author =. Econometrica , volume =. 2000 , publisher =

2000

-

[49]

Handbook of Econometrics , editor =

Large Sample Estimation and Hypothesis Testing , author =. Handbook of Econometrics , editor =. 1994 , publisher =

1994

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.