Agent-to-Agent Finance: Blockchain Payments and Trust Infrastructure for Autonomous AI Agents

Pith reviewed 2026-07-02 16:39 UTC · model grok-4.3

The pith

Autonomous AI agents require blockchain layers for payments, identity and accountability when they act as economic counterparties.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

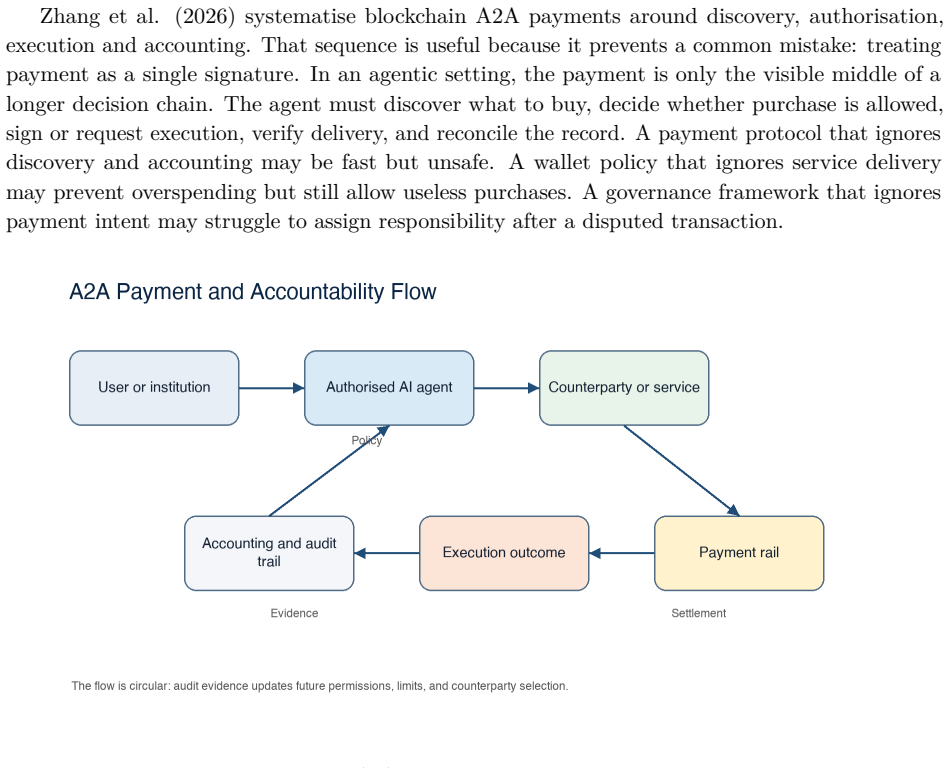

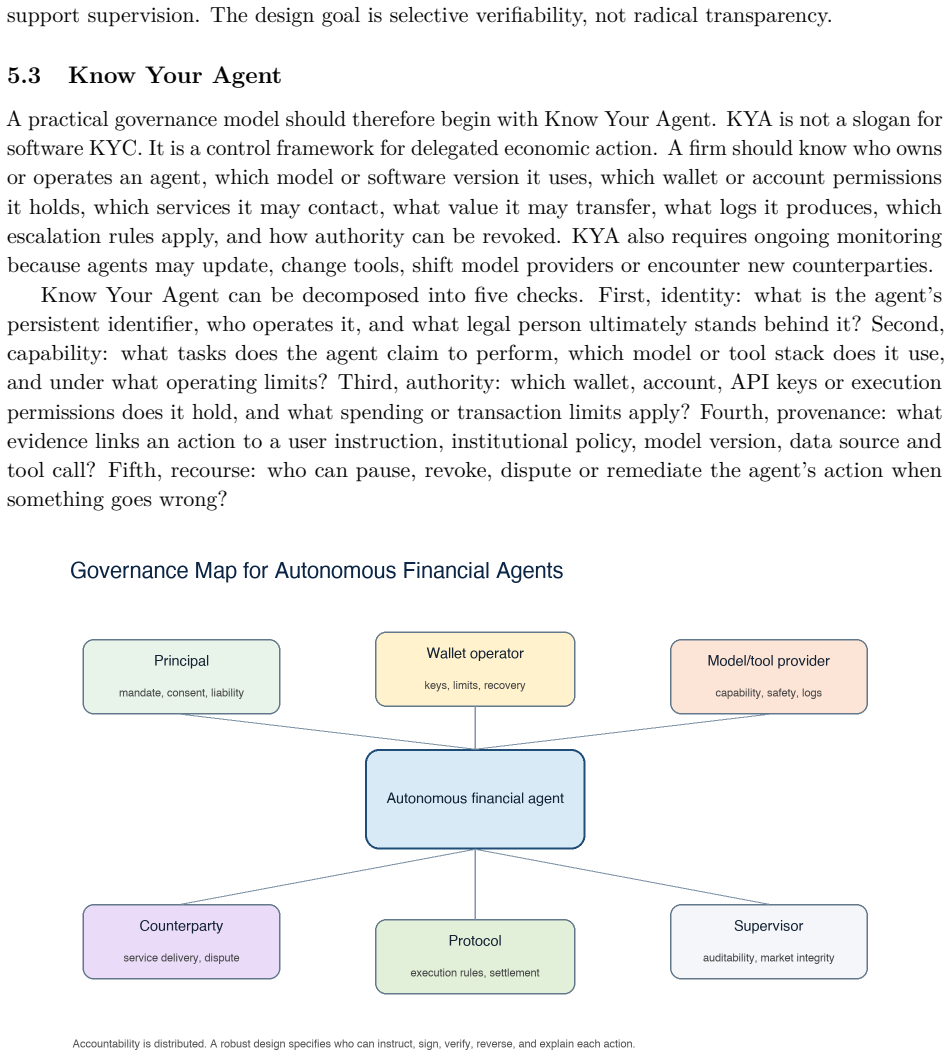

Autonomous AI agents sit between analytical tools and transacting counterparties, interpreting goals, negotiating, accessing computation and initiating payments; this creates distinct infrastructure needs for identity, authorisation, payment, verification, reputation and accountability, which programmable settlement, smart wallets, decentralised registries and verifiable computation can address without blockchain serving as a universal substrate, leaving bounded autonomy as the central design question.

What carries the argument

Bounded autonomy: the design constraint that lets agents initiate and settle transactions while still producing auditable evidence and preserving market accountability.

If this is right

- Agent registries provide discoverable identity and reputation data that counterparties can query before transacting.

- Smart wallets with provenance tracking allow controlled delegation of payment authority to agents.

- Verifiable computation produces evidence that agent decisions and payments can be audited after the fact.

- Intent-based protocols reduce the need for agents to reveal full strategies while still executing payments.

Where Pith is reading between the lines

- Integration with existing DeFi intent engines could let agents mine and execute cross-agent trades at lower coordination cost.

- Regulators may need explicit rules for authorising agent wallets to prevent untraceable economic activity.

- Pilot deployments of agent registries could test whether transaction volume justifies the added verification layer.

Load-bearing premise

Autonomous AI agents will routinely initiate payments and blockchain transactions, creating coordination frictions that existing financial systems cannot handle without new blockchain infrastructure.

What would settle it

Large-scale deployment of AI agents that make payments and negotiate services exclusively through traditional banking rails or centralised APIs, without measurable demand for decentralised registries or verifiable settlement records.

Figures

read the original abstract

Autonomous AI agents are beginning to occupy a position between analytical tools and transacting counterparties. They can interpret goals, call external tools, negotiate with other agents, access data and computation, and in some settings initiate payments or blockchain transactions. This development creates a distinct problem for financial markets: if software agents can act economically, market participants need infrastructure for identity, authorisation, payment, verification, reputation and accountability. This article develops the concept of agent-to-agent finance as the layer of machine-mediated financial interaction in which autonomous agents discover counterparties, purchase services, express transaction intent, execute payments and generate auditable evidence. The argument is not that blockchain is a universal substrate for finance, but that programmable settlement, smart wallets, decentralised registries and verifiable computation can address specific coordination frictions created by autonomous agents. Drawing on recent work on blockchain A2A payments, ERC-8004 agent registries, provenance-based wallets, deterministic inference, DeFi intent mining, and official evidence on AI adoption in financial services, the article situates agent-to-agent finance as an emerging form of financial market infrastructure. It argues that the decisive design question is bounded autonomy: how to let agents transact without making markets more opaque, fragile or unaccountable.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops the concept of 'agent-to-agent finance' as the layer of machine-mediated financial interaction for autonomous AI agents that can negotiate, access data, and initiate payments or blockchain transactions. It argues that programmable settlement, smart wallets, decentralised registries, and verifiable computation can address specific coordination frictions in identity, authorisation, payment, verification, reputation, and accountability. The paper emphasizes bounded autonomy as the key design question to prevent markets from becoming more opaque, fragile, or unaccountable, drawing on blockchain A2A payments, ERC-8004, provenance-based wallets, deterministic inference, DeFi intent mining, and AI adoption evidence.

Significance. If the argument holds, the paper provides a useful conceptual synthesis situating blockchain infrastructure as a potential solution for coordination issues in agent-driven financial activities. It explicitly credits recent work on specific technologies and frames the contribution as identifying an emerging form of financial market infrastructure rather than claiming a solved technical problem. This could stimulate further research in the intersection of AI autonomy and financial systems. The stress-test concern regarding routine agent-initiated payments does not land, as the manuscript scopes its claims to 'in some settings' and possibility rather than necessity or universality.

minor comments (2)

- Abstract: the phrase 'official evidence on AI adoption in financial services' is referenced but the main text should cross-reference the specific sources or reports cited to strengthen traceability.

- The manuscript would benefit from an explicit outline of its sections early in the introduction to clarify how the synthesis of cited works supports the bounded-autonomy framing.

Simulated Author's Rebuttal

We thank the referee for their thoughtful and positive review. The assessment correctly identifies the paper's scope as a conceptual synthesis rather than a solved technical problem, and we appreciate the confirmation that our claims are appropriately bounded to 'in some settings' rather than universal necessity. We are pleased that the referee views the work as potentially stimulating further research at the AI-finance intersection.

Circularity Check

No significant circularity; conceptual proposal with external citations only

full rationale

The paper advances a scoped conceptual argument that programmable settlement, smart wallets, decentralised registries and verifiable computation can address coordination frictions for autonomous agents. It contains no equations, fitted parameters, derivations, or quantitative predictions. All supporting references are to external works on blockchain A2A payments, ERC-8004 registries, DeFi intent mining and official AI-adoption statistics; none reduce to quantities or premises defined inside the paper itself. The bounded-autonomy framing is presented as an open design question rather than a solved claim derived from prior self-citations. The derivation chain is therefore self-contained against external benchmarks and exhibits no self-definitional, fitted-input, or self-citation-load-bearing circularity.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Autonomous AI agents can interpret goals, call tools, negotiate, and initiate payments or blockchain transactions

invented entities (1)

-

agent-to-agent finance

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Alqithami, S. (2026) ’Autonomous Agents on Blockchains: Standards, Execution Models, and Trust Boundaries’, arXiv:2601.04583

-

[2]

Alves, D.R., Patankar, V., Pereira, M., Stephens, J., Vaziri, N. and Kannan, S. (2026) ’EigenAI: Deterministic Inference, Verifiable Results’, arXiv:2602.00182. Bank of England and Financial Conduct Authority (2024) ’Artificial intelligence in UK financial ser- vices-2024’. Availableat:https://www.bankofengland.co.uk/report/2024/artificial-intelligence-in...

-

[3]

Jin, Y., Wu, S., Chen, C., Bao, L., Yang, X. and Chen, J. (2026) ’The Web4 Agent Economy: A Large- Scale Empirical Study of the Landscape, Challenges, and Opportunities’, arXiv:2606.25876

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[4]

From Agent Identity to Agent Economy: Measuring the Operational Readiness of ERC-8004 AI Agents

Mafrur, R. and Khusumanegara, P. (2026) ’From Agent Identity to Agent Economy: Measuring the Operational Readiness of ERC-8004 AI Agents’, arXiv:2606.12128

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[5]

Mao, Q., Zhang, Y., Chen, J., Zhou, W. and Yan, J. (2025) ’Know Your Intent: An Au- tonomous Multi-Perspective LLM Agent Framework for DeFi User Transaction Intent Mining’, arXiv:2511.15456

-

[6]

Nannini, L. et al. (2026) ’AI Agents under EU Law: A Compliance Architecture for AI Providers’, arXiv:2604.04604

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[7]

Can Trustless Agents Be Trusted? An Empirical Study of the ERC-8004 Decentralized AI Agent Ecosystem

Xiong, X., Li, Z., Wei, W., Wang, Q., Knottenbelt, W. and Wang, Z. (2026) ’Can Trustless Agents Be Trusted? An Empirical Study of the ERC-8004 Decentralized AI Agent Ecosystem’, arXiv:2606.26028

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[8]

PASS: A Provenanced Access Subaccount System for Blockchain Wallets

Yu, J., Zhou, S., Yin, H. and Seong, B. (2026) ’PASS: A Provenanced Access Subaccount System for Blockchain Wallets’, arXiv:2604.22602

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[9]

Zeng, Q. et al. (2026) ’When AI Meets Wall Street: A Survey on Trustworthy AI in Fintech’, arXiv:2605.30650

work page internal anchor Pith review Pith/arXiv arXiv 2026

-

[10]

SoK: Blockchain Agent-to-Agent Payments

Yu, J. and Lam, K.-Y. (2026) ’SoK: Blockchain Agent-to-Agent Payments’, arXiv:2604.03733. 22

work page internal anchor Pith review Pith/arXiv arXiv 2026

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.