Tail Risk Management with Puts and Trend Following: A CVaR Framework for Crashes and Drawdowns

Pith reviewed 2026-07-02 01:37 UTC · model grok-4.3

The pith

A CVaR framework integrates put options and trend following by exploiting their different response times to crashes and drawdowns.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

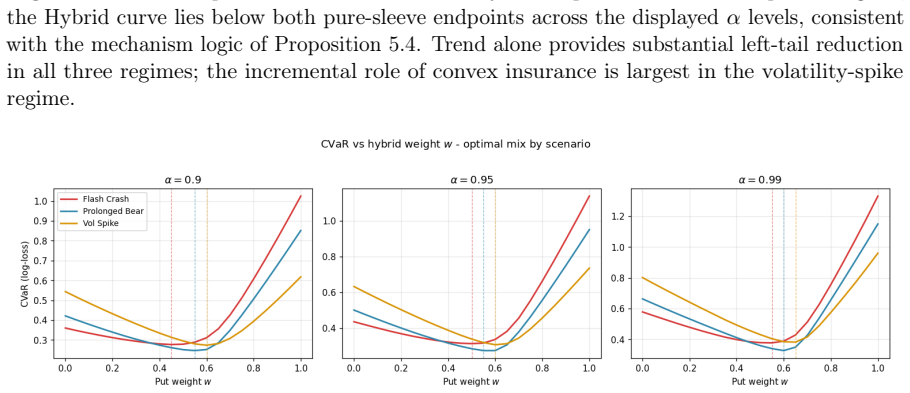

The central claim is that the Markov state consisting of wealth, spot price, stochastic variance and an exponentially weighted log-return signal generates an HJB equation whose solution yields sufficient conditions for an interior hybrid allocation between the two protection sleeves, together with a CVaR policy-gradient identity and a four-axis diagnostic that separates conditional convexity, tail-event reliability, non-stress carry and drawdown persistence.

What carries the argument

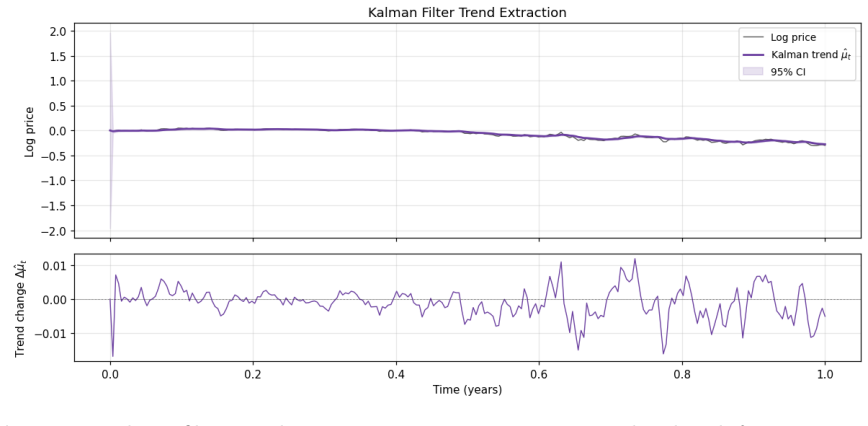

The continuous-time CVaR Hamilton-Jacobi-Bellman equation in viscosity form whose state includes an exponentially weighted log-return trend signal.

If this is right

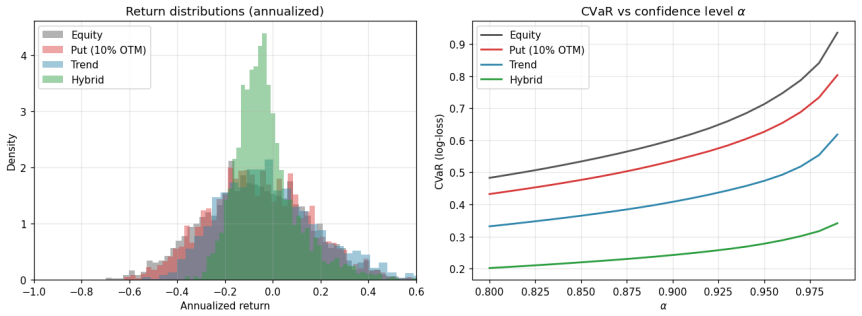

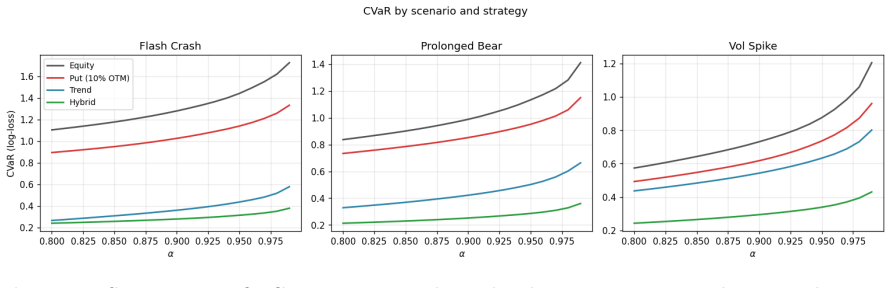

- Fixed equal-weight and grid-optimized hybrids reduce terminal CVaR relative to pure put or pure trend strategies in the reported Monte Carlo regimes.

- Sufficient and local conditions exist for interior hybrid allocations between the two sleeves.

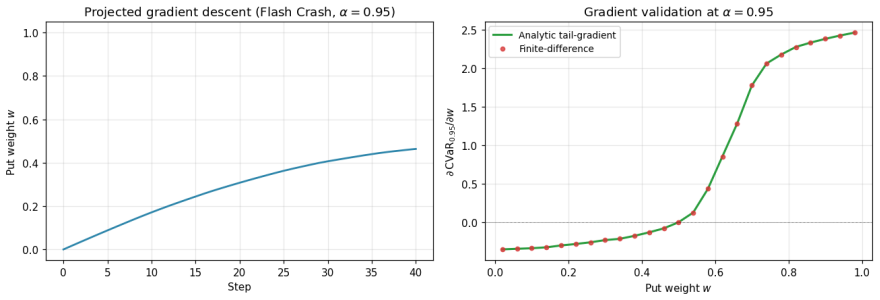

- A CVaR policy-gradient identity can be used to optimize the allocation.

- The four-axis diagnostic layer separates conditional convexity, tail-event reliability, non-stress carry, and drawdown persistence.

Where Pith is reading between the lines

- The framework suggests that mandates could calibrate the weight between sleeves according to the expected frequency of jump versus persistent drawdown regimes.

- Extending the diagnostic layer to include transaction costs or liquidity effects would test the robustness of the temporal separation.

- The modeling of options as traded assets implies that any real-world implementation must account for the discrete nature of option rolls and margin requirements.

- Similar state-augmented CVaR problems could be formulated for other pairs of protection instruments with differing activation lags.

Load-bearing premise

The option sleeve behaves as a continuously marked-to-market traded asset whose return process fully incorporates premium drag, diffusion exposure, and jump repricing.

What would settle it

Empirical observation that the hybrid allocation fails to reduce realized CVaR below the better of the two pure sleeves across multiple historical crash and drawdown episodes would falsify the claimed benefit of the combined mandate.

Figures

read the original abstract

Tail-risk management is not only an instrument-selection problem. It is an allocation problem across loss mechanisms: abrupt crash states, volatility repricing, and persistent drawdowns require different forms of protection. This paper develops a continuous-time CVaR framework that places two common protection sleeves -- long out-of-the-money put options and systematic trend-following overlays -- inside one coherent tail-risk mandate. The option sleeve is modeled as a marked-to-market traded asset, so premium drag, diffusion exposure, and jump repricing enter through its physical return process rather than through inconsistent terminal-payoff accounting. The resulting Markov state contains wealth, spot, stochastic variance, and an exponentially weighted log-return signal, and we derive the associated Hamilton--Jacobi--Bellman equation in viscosity form. The main analytical separation is temporal: convex insurance reprices immediately on jump impact, whereas trend following is late on the first shock because its signal must cross zero, but becomes increasingly defensive during persistent drawdowns without requiring fresh option premium. We then give sufficient and local conditions for an interior hybrid allocation, derive a CVaR policy-gradient identity, and introduce a four-axis diagnostic layer separating conditional convexity, tail-event reliability, non-stress carry, and drawdown persistence. Stylized Monte Carlo experiments illustrate the mechanism: fixed equal-weight hybrids and grid-optimized hybrids reduce terminal CVaR relative to either pure sleeve in the reported regimes, while the exact weight location remains calibration-dependent. The contribution is a transparent risk-management framework for deciding how much convex crash protection and how much signal-driven drawdown protection a mandate should hold.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a continuous-time CVaR framework for tail-risk management that integrates long out-of-the-money put options and systematic trend-following overlays within a single mandate. The option sleeve is modeled as a marked-to-market traded asset whose physical return process incorporates premium drag, diffusion, and jump repricing; the resulting Markov state (wealth, spot, stochastic variance, exponentially weighted log-return signal) yields a viscosity-form HJB equation. The central analytical result is a temporal separation: puts reprice immediately on jumps while trend following lags on the first shock but strengthens during persistent drawdowns. The paper supplies sufficient and local conditions for interior hybrid allocations, a CVaR policy-gradient identity, a four-axis diagnostic layer, and stylized Monte Carlo experiments showing that both fixed and optimized hybrids reduce terminal CVaR relative to pure sleeves.

Significance. If the modeling assumptions hold, the work supplies a coherent, analytically tractable framework for allocating across distinct loss mechanisms (abrupt crashes versus persistent drawdowns) that is directly usable in mandate design. The explicit treatment of the option sleeve inside the physical-measure dynamics, the derivation of interior hybrid conditions from the viscosity HJB, and the CVaR policy-gradient identity are concrete strengths that move beyond ad-hoc sleeve selection.

major comments (2)

- [Modeling section (pre-HJB)] The temporal separation and interior hybrid optimality conditions rest entirely on the modeling choice that the put sleeve follows a continuously marked-to-market physical return process (including instantaneous jump repricing). This assumption is load-bearing for the HJB derivation and the claimed separation; the manuscript should supply the explicit SDE for the put's return process and verify that the viscosity solution remains valid under it.

- [Monte Carlo experiments] The Monte Carlo section reports that 'fixed equal-weight hybrids and grid-optimized hybrids reduce terminal CVaR' but provides no parameter values, number of paths, or regime definitions. Without these, the quantitative claim cannot be assessed and the calibration-dependence caveat cannot be evaluated.

minor comments (2)

- [State variable definition] Define the precise functional form of the exponentially weighted log-return signal (decay parameter, initialization) when the state vector is introduced.

- [Diagnostic layer] The four-axis diagnostic layer (conditional convexity, tail-event reliability, non-stress carry, drawdown persistence) is introduced but not given explicit formulas or numerical illustrations; a short table or set of equations would improve clarity.

Simulated Author's Rebuttal

We thank the referee for the thorough review and constructive feedback. We address the two major comments point by point below and will revise the manuscript to incorporate the requested details.

read point-by-point responses

-

Referee: [Modeling section (pre-HJB)] The temporal separation and interior hybrid optimality conditions rest entirely on the modeling choice that the put sleeve follows a continuously marked-to-market physical return process (including instantaneous jump repricing). This assumption is load-bearing for the HJB derivation and the claimed separation; the manuscript should supply the explicit SDE for the put's return process and verify that the viscosity solution remains valid under it.

Authors: We agree that the explicit SDE is required to make the modeling assumptions fully transparent and to support the HJB derivation and temporal separation result. While the manuscript describes the components of the put sleeve's physical return process (premium drag, diffusion, and jump repricing), it does not present the SDE in equation form. In the revised version we will insert the complete SDE in the pre-HJB modeling section and add a short paragraph confirming that the viscosity solution remains valid under the stated dynamics. revision: yes

-

Referee: [Monte Carlo experiments] The Monte Carlo section reports that 'fixed equal-weight hybrids and grid-optimized hybrids reduce terminal CVaR' but provides no parameter values, number of paths, or regime definitions. Without these, the quantitative claim cannot be assessed and the calibration-dependence caveat cannot be evaluated.

Authors: We accept that the Monte Carlo section is insufficiently documented for reproducibility and evaluation. The text refers to 'reported regimes' and notes that results are 'calibration-dependent,' yet supplies neither the numerical parameter values, the number of paths, nor the precise regime definitions. In the revision we will expand this section with the complete set of simulation parameters, path count, regime specifications, and any calibration details used. revision: yes

Circularity Check

No significant circularity; derivation self-contained under explicit modeling assumptions

full rationale

The paper states an explicit modeling choice (option sleeve as marked-to-market traded asset whose returns enter the physical process) and derives the HJB equation, temporal separation, and hybrid conditions from the resulting Markov state (wealth, spot, variance, signal). No equations reduce predictions to fitted parameters by construction, no self-citations are load-bearing, and no ansatz or uniqueness theorem is smuggled in. The framework is presented as derived from standard viscosity solutions under the stated dynamics; results are conditional on the modeling choice rather than tautological.

Axiom & Free-Parameter Ledger

free parameters (1)

- hybrid allocation weights

axioms (1)

- standard math Existence of a viscosity solution to the HJB equation for the Markov control problem

Reference graph

Works this paper leans on

-

[1]

Spectral measures of risk: A coherent representation of subjective risk aversion

Acerbi, Carlo (2002). “Spectral measures of risk: A coherent representation of subjective risk aversion”. In:Journal of Banking & Finance26.7, pp. 1505–1518.doi:10.1016/ S0378-4266(02)00281-9. Aı¨t-Sahalia, Yacine, Julio Cacho-Diaz, and Roger J. A. Laeven (2015). “Modeling financial contagion using mutually exciting jump processes”. In:Journal of Financia...

-

[2]

Artzner, Philippe, Freddy Delbaen, Jean-Marc Eber, and David Heath (1999). “Coherent measures of risk”. In:Mathematical Finance9.3, pp. 203–228.doi:10.1111/1467- 9965.00068

-

[3]

Second-order elliptic integro-differential equations: viscosity solutions’ theory revisited

Barles, Guy and Cyril Imbert (2008). “Second-order elliptic integro-differential equations: viscosity solutions’ theory revisited”. In:Annales de l’Institut Henri Poincaré C, Analyse non linéaire25.3, pp. 567–585.doi:10.1016/j.anihpc.2007.02.007. 29 Bhansali,Vineer(2014).Tail Risk Hedging: Creating Robust Portfolios for Volatile Markets. New York: McGraw-Hill

-

[4]

Understanding index option returns

Broadie, Mark, Mikhail Chernov, and Michael Johannes (2009). “Understanding index option returns”. In:Review of Financial Studies22.11, pp. 4493–4529.doi:10.1093/ rfs/hhp032

2009

-

[5]

(2005).Asset Pricing: Revised Edition

Cochrane, John H. (2005).Asset Pricing: Revised Edition. Princeton, NJ: Princeton University Press

2005

-

[6]

Fleming, Wendell H. and H. Mete Soner (2006).Controlled Markov Processes and Viscosity Solutions. 2nd ed. New York: Springer.doi:10.1007/0-387-31071-1

-

[7]

Heston, Steven L. (1993). “A closed-form solution for options with stochastic volatility with applications to bond and currency options”. In:Review of Financial Studies6.2, pp. 327–343.doi:10.1093/rfs/6.2.327

-

[8]

Simulating sensitivities of conditional value at risk

Hong, L. Jeff and Guangwu Liu (2009). “Simulating sensitivities of conditional value at risk”. In:Management Science55.2, pp. 281–293.doi:10.1287/mnsc.1080.0901

-

[9]

Hurst, Brian, Yao Hua Ooi, and Lasse Heje Pedersen (2013). “Demystifying Managed Futures”. In:Journal of Investment Management11.3, pp. 42–58. — (2017). “A century of evidence on trend-following investing”. In:Journal of Portfolio Management44.1, pp. 15–29.doi:10.3905/jpm.2017.44.1.015

-

[10]

White Paper

Ilmanen, Antti, Thomas Maloney, and Adrienne Ross (July 2020).Tail risk hedging: Contrasting put and trend strategies. White Paper. AQR Capital Management.url: https://www.aqr.com/Insights/Research/White-Papers/Tail-Risk-Hedging- Contrasting-Put-and-Trend-Strategies

2020

-

[11]

Still not cheap: Portfolio protection in calm markets

Israelov, Roni and Lars N. Nielsen (2017). “Still not cheap: Portfolio protection in calm markets”. In:Journal of Portfolio Management43.5, pp. 108–120.doi:10.3905/jpm. 2017.43.5.108. Jakobsen,EspenR.andKennethH.Karlsen(2006).“A“maximumprincipleforsemicontin- uous functions” applicable to integro-partial differential equations”. In:Nonlinear Dif- ferentia...

work page doi:10.3905/jpm 2017

-

[12]

Conditional risk premia in currency markets and other asset classes

Lettau, Martin, Matteo Maggiori, and Michael Weber (2014). “Conditional risk premia in currency markets and other asset classes”. In:Journal of Financial Economics114.2, pp. 197–225.doi:10.1016/j.jfineco.2014.07.001

-

[13]

A comparison of biased simulation schemes for stochastic volatility models

Lord, Roger, Remmert Koekkoek, and Dick Van Dijk (2010). “A comparison of biased simulation schemes for stochastic volatility models”. In:Quantitative Finance10.2, pp. 177–194.doi:10.1080/14697680802392496

-

[14]

Markowitz, Harry (1952). “Portfolio selection”. In:Journal of Finance7.1, pp. 77–91.doi: 10.2307/2975974

-

[15]

Lifetime portfolio selection under uncertainty: The continuous- time case

Merton, Robert C. (1969). “Lifetime portfolio selection under uncertainty: The continuous- time case”. In:Review of Economics and Statistics51.3, pp. 247–257.doi:10.2307/ 1926560. — (1971). “Optimum consumption and portfolio rules in a continuous-time model”. In: Journal of Economic Theory3.4, pp. 373–413.doi:10.1016/0022-0531(71)90038-X. 30

-

[16]

Moskowitz, Tobias J., Yao Hua Ooi, and Lasse Heje Pedersen (2012). “Time series momentum”. In:Journal of Financial Economics104.2, pp. 228–250.doi:10.1016/ j.jfineco.2011.11.003. Øksendal, Bernt and Agnès Sulem (2005).Applied Stochastic Control of Jump Diffusions. Berlin: Springer.doi:10.1007/b137590

-

[17]

Berlin: Springer.doi:10.1007/978-3-540-89500-8

Pham, Huyên (2009).Continuous-Time Stochastic Control and Optimization with Finan- cial Applications. Berlin: Springer.doi:10.1007/978-3-540-89500-8

-

[18]

Optimization of conditional value-at-risk,

Rockafellar, R. Tyrrell and Stanislav Uryasev (2000). “Optimization of conditional value- at-risk”. In:Journal of Risk2.3, pp. 21–41.doi:10.21314/JOR.2000.038. 31

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.