Is Trend Still Your Friend?: A Microstructural Account of the Demise of Short-Term Trend-Following

Pith reviewed 2026-07-03 01:08 UTC · model grok-4.3

The pith

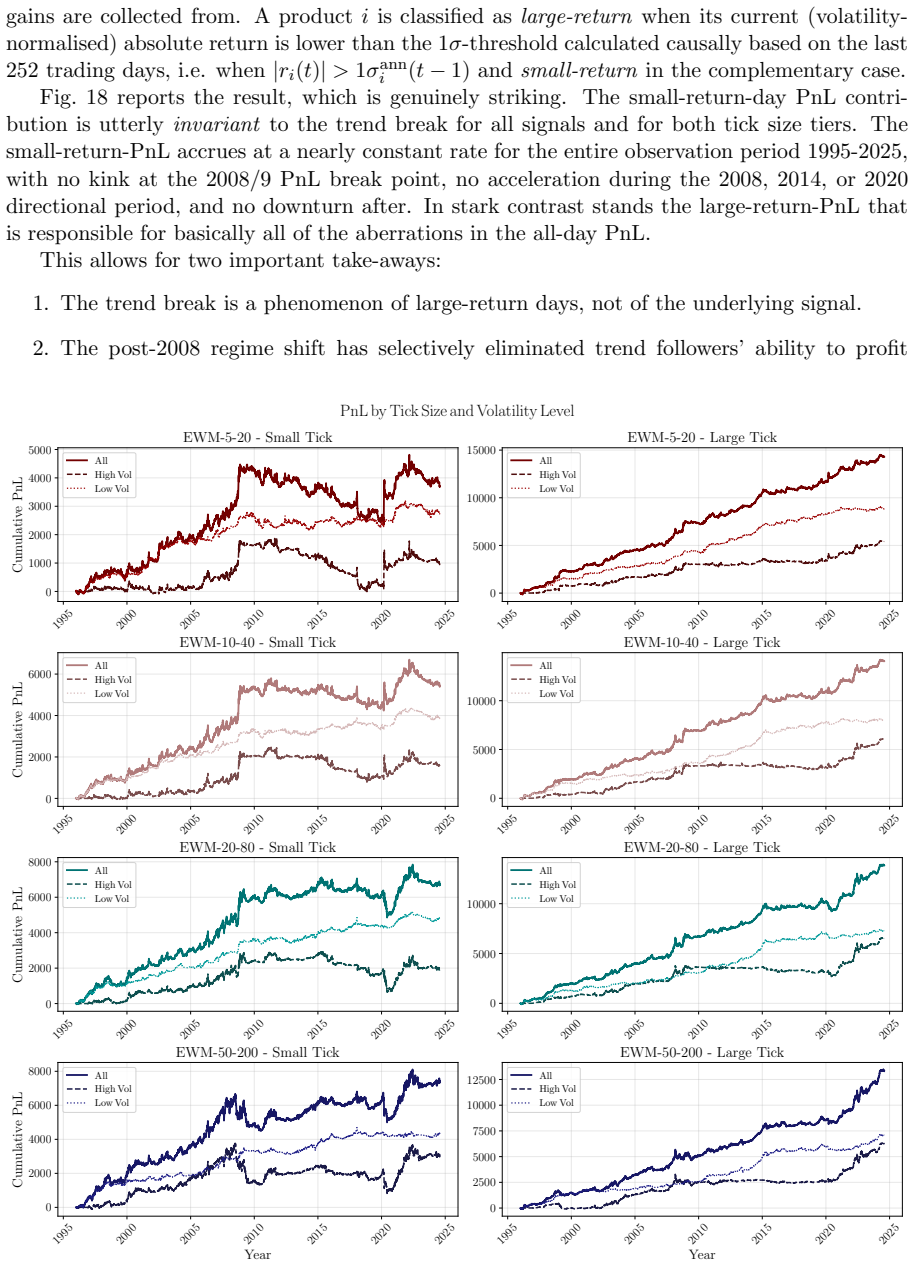

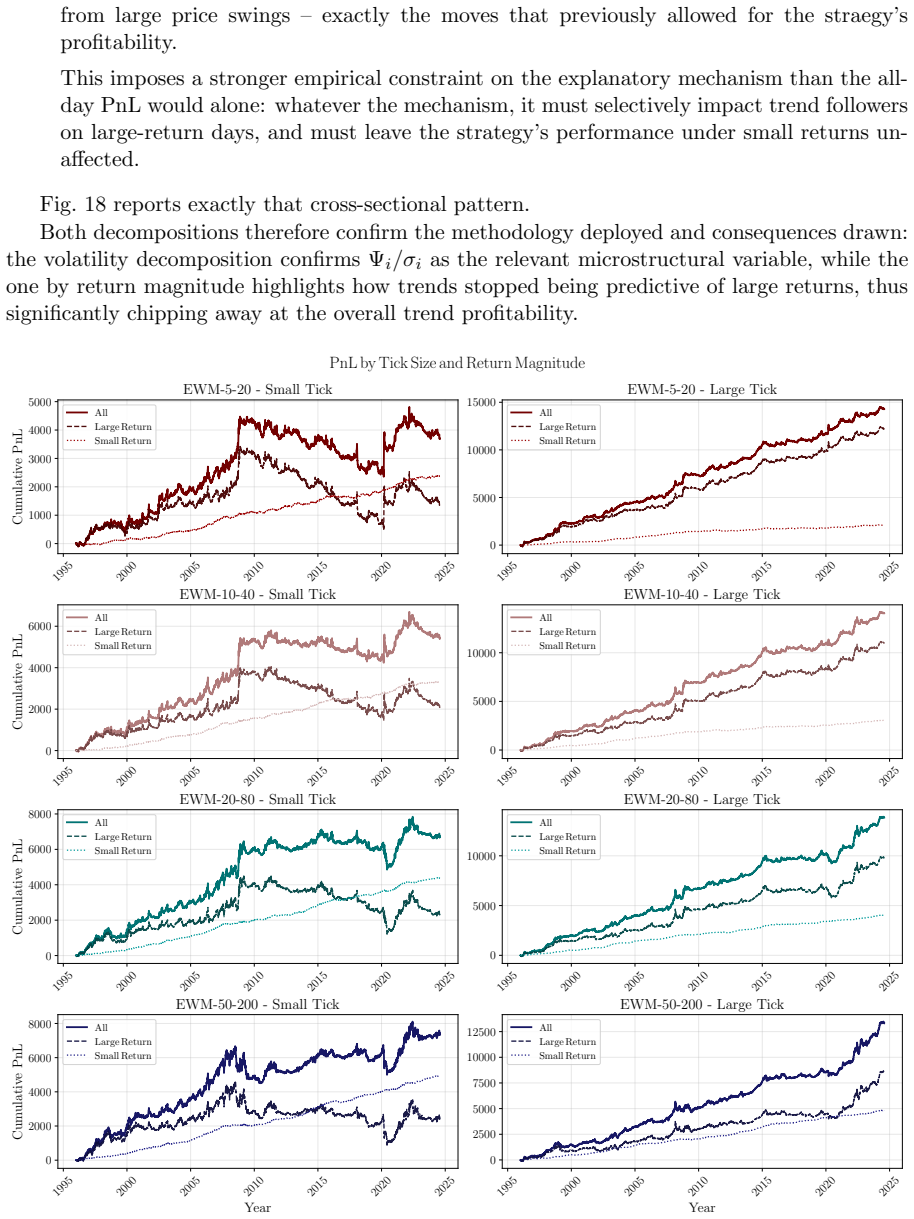

Short-term trend following stopped working on small-tick futures after 2008 because high-frequency traders withdraw liquidity ahead of predictable directional trades.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

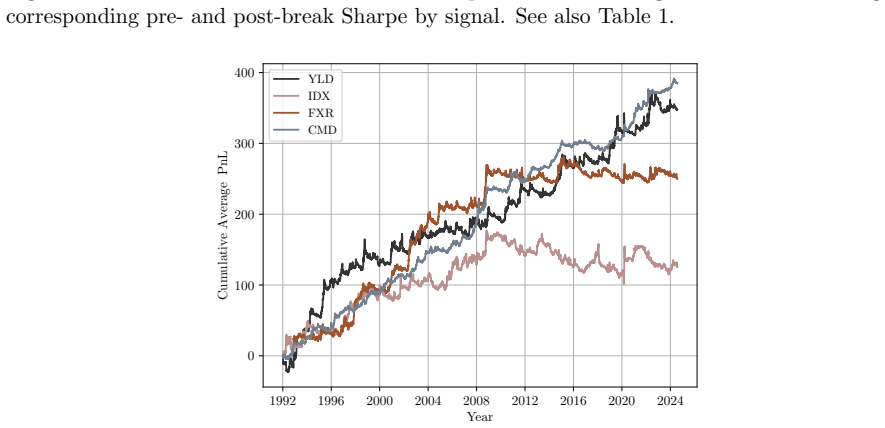

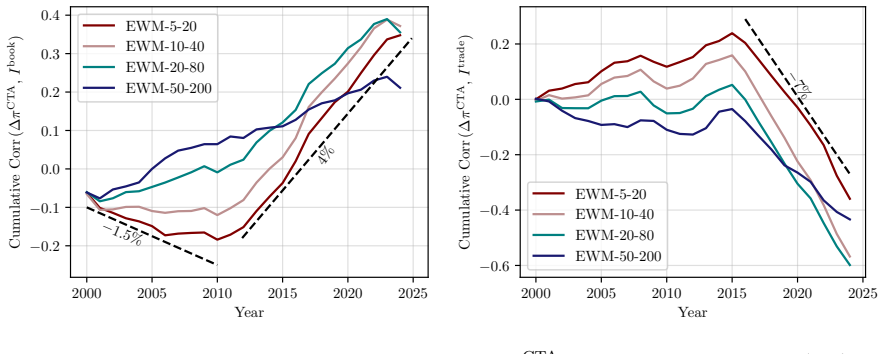

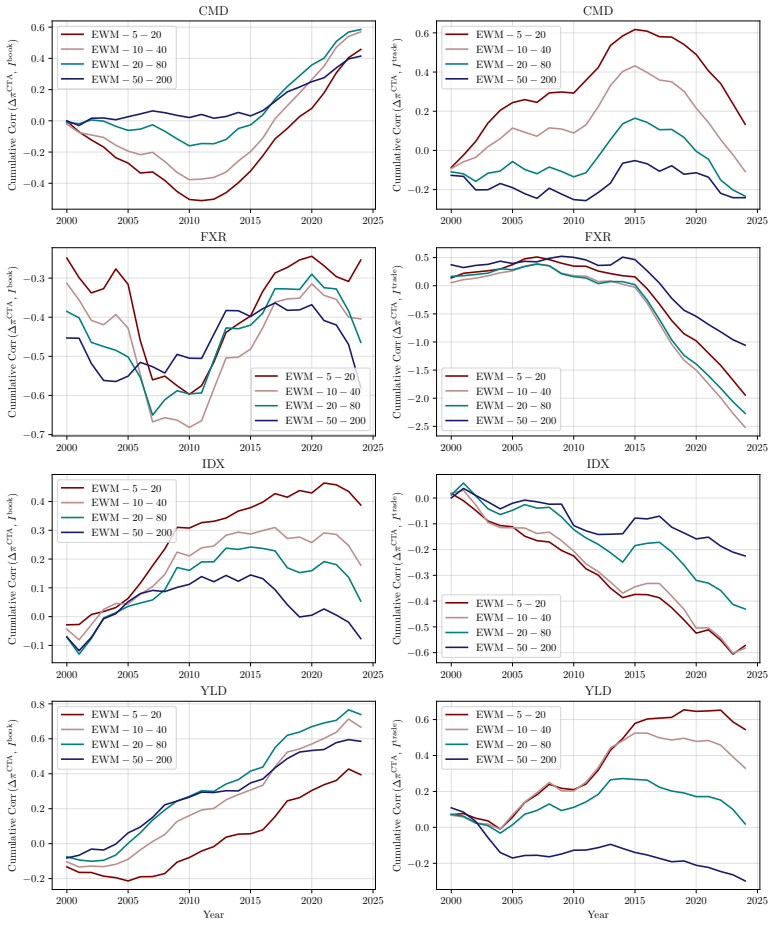

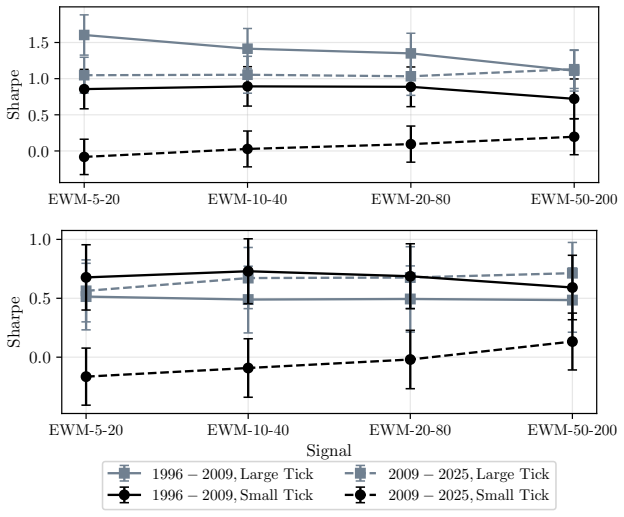

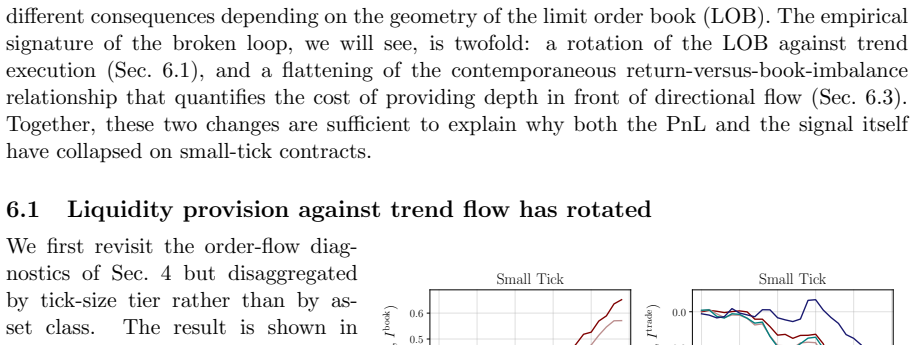

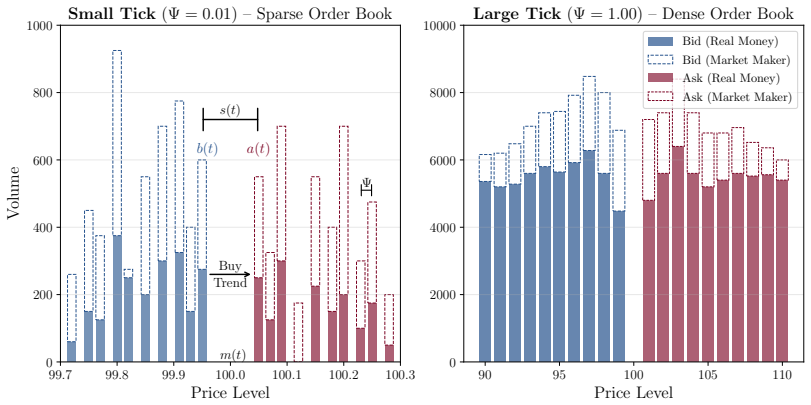

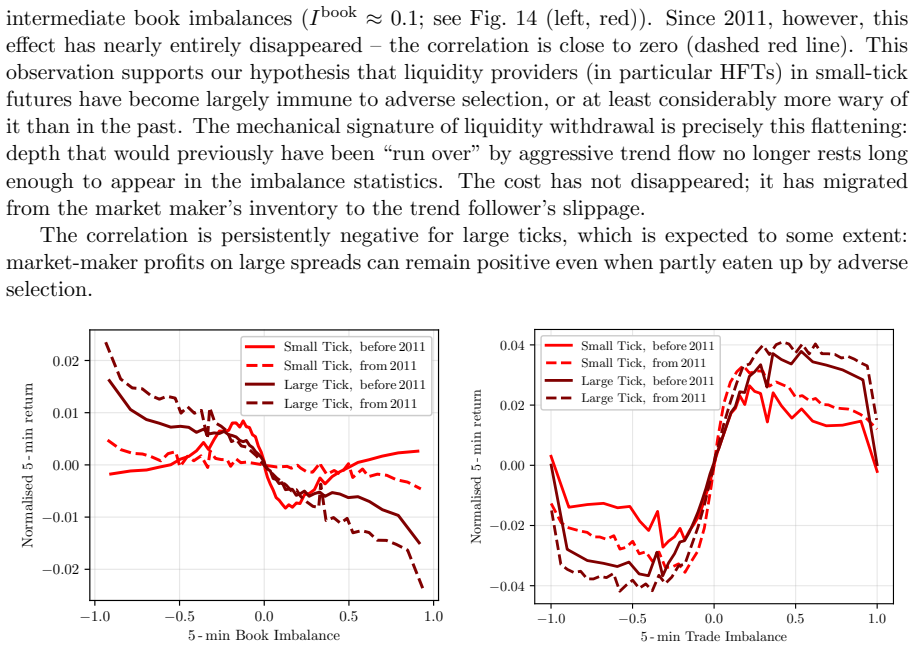

Trend PnL has collapsed on small-tick contracts across all signal horizons since 2008 while remaining essentially intact on large-tick ones. The distinguishing cross-sectional variable is volatility-normalised tick size, not asset class or liquidity. This pattern is explained by the post-crisis rise of HFT market making, whose liquidity-withdrawal behaviour in front of predictable flow breaks the impact feedback loop that once allowed trend followers to execute at reasonable cost and thereby reinforced the very moves their signals detected.

What carries the argument

The self-fulfilling impact feedback loop in which trend signals generate directional trades whose market impact reinforces the price moves that generated the signal.

If this is right

- The first three candidate explanations fail on grounds of timing, magnitude, or cross-sectional heterogeneity.

- Post-2008 trend PnL collapsed on small-tick contracts across all signal horizons.

- Trend PnL remained essentially intact on large-tick contracts.

- Neither asset class nor liquidity replicates the performance dichotomy.

- The transition to HFT-dominated market making broke the impact channel on small-tick contracts while residual depth preserved it on large-tick contracts.

Where Pith is reading between the lines

- The result suggests that execution algorithms designed to mask directional intent could restore some of the lost edge on small-tick contracts.

- Similar feedback loops may be vulnerable in other asset classes where HFT dominates thin order books.

- Monitoring changes in quoted depth around known trend-signal times could provide an early indicator of whether the loop remains intact.

Load-bearing premise

The performance split by volatility-normalised tick size is caused by HFT liquidity-withdrawal behaviour breaking the impact feedback loop rather than by some other unmeasured factor that happens to correlate with tick size.

What would settle it

A direct observation of whether HFT market makers withdraw limit orders more aggressively in front of trend-following orders on small-tick contracts than on large-tick contracts; the absence of such differential withdrawal would falsify the account.

Figures

read the original abstract

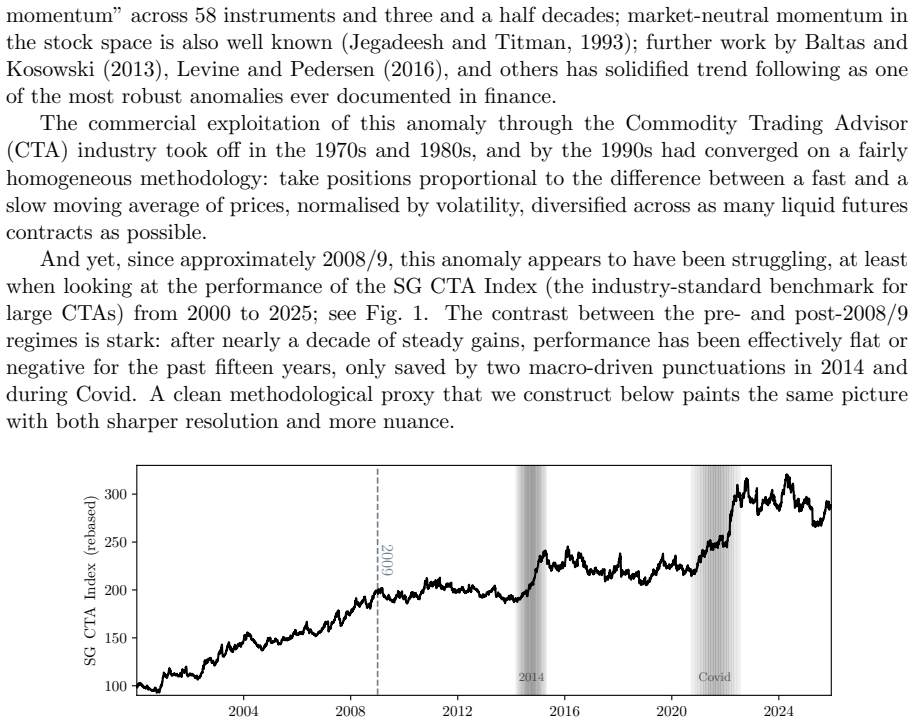

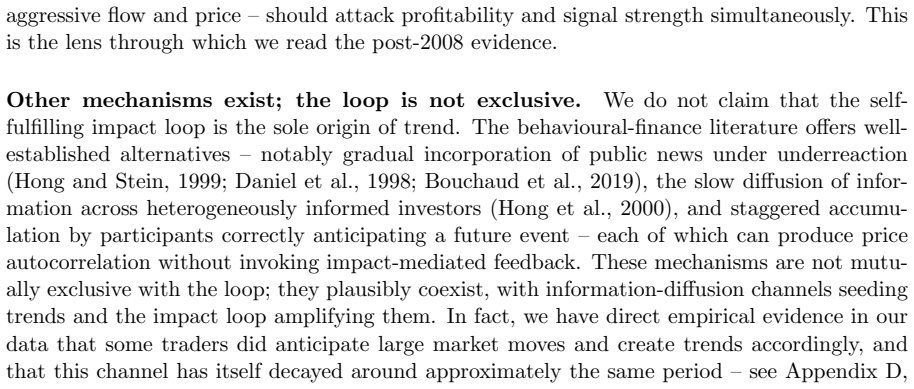

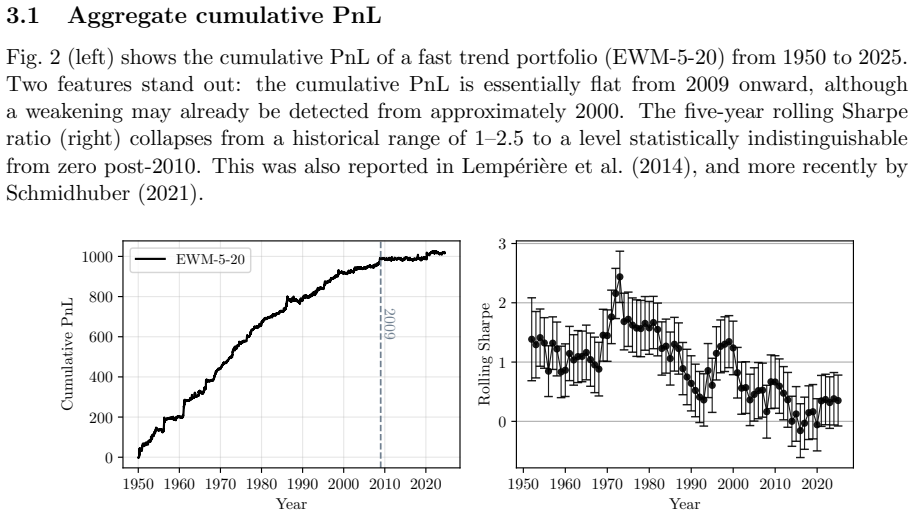

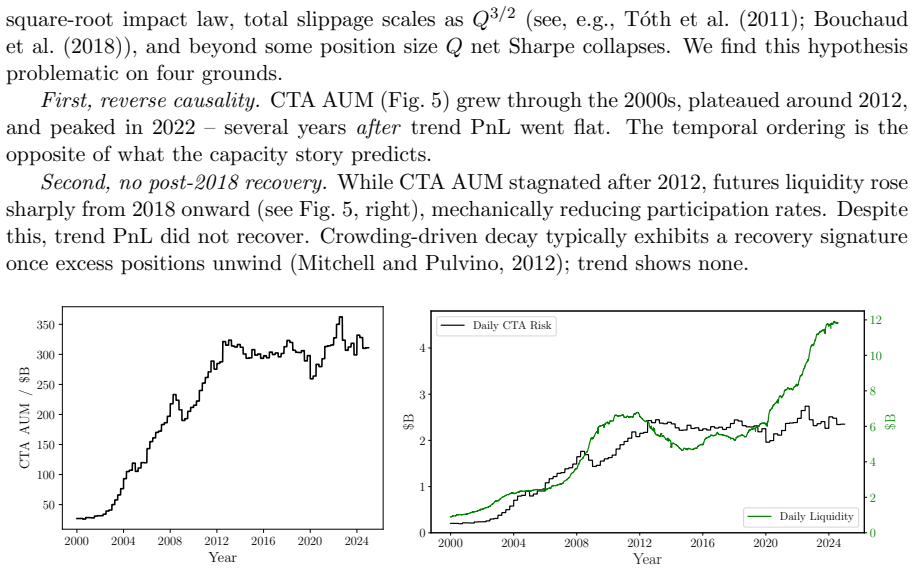

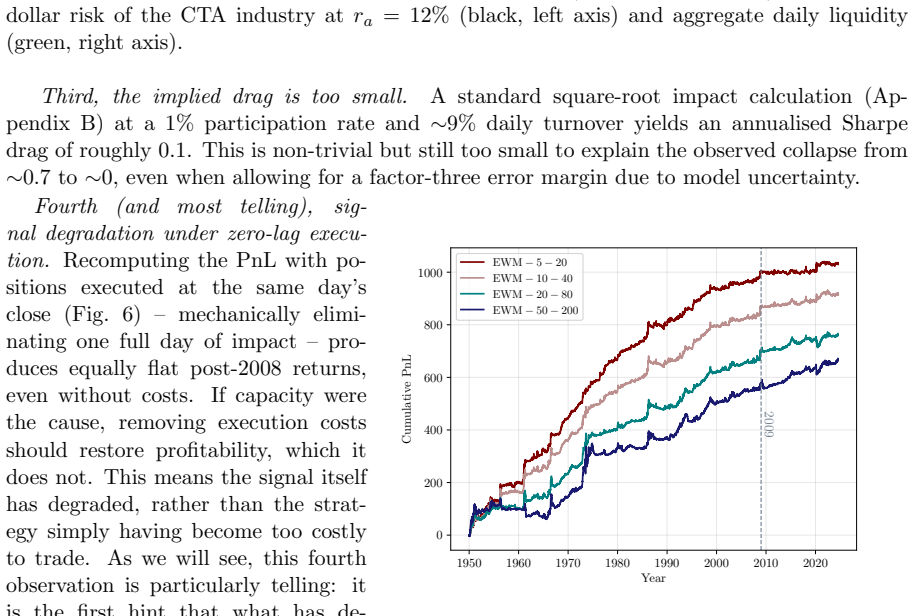

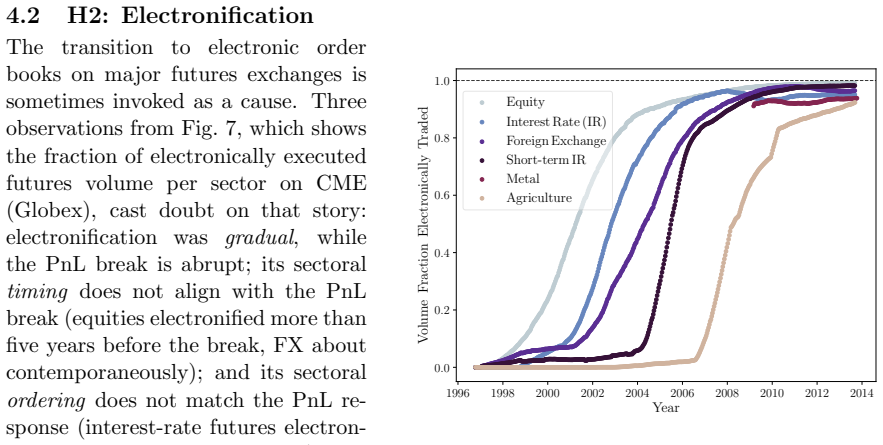

Systematic trend following has, on average, been profitable for at least two centuries; yet since approximately 2009, short-term trends have ceased to deliver reliable returns. Using a cross-section of roughly 100 liquid futures contracts spanning 1995-2025, together with an industry-representative CTA proxy, we document the break and characterise its dependence on signal speed and asset class. We evaluate four candidate explanations - capacity constraints, market electronification, a regime change in CTA-versus-order-flow interactions, and a microstructural mechanism - and find that the first three fail on grounds of timing, magnitude, or cross-sectional heterogeneity. Our central empirical finding is that the cross-sectional variable distinguishing degraded from surviving trends is the volatility-normalised tick size: post-2008 trend PnL has collapsed on small-tick contracts across all signal horizons, while remaining essentially intact on large-tick ones. Neither asset class nor liquidity replicates this dichotomy. We interpret this result through a self-fulfilling feedback loop that, in our view, lies at the heart of the trend anomaly itself: trend signals trigger directional trades, whose market impact reinforces the very price moves that generated the signal. Both the profitability and the persistence of trend are sustained by this impact channel, which requires that trend followers can execute aggressively at reasonable cost. We argue that the post-crisis transition to HFT-dominated market making, whose liquidity-withdrawal behaviour in front of predictable directional flow has sharply contrasting consequences for sparse (small-tick) and dense (large-tick) limit order books, has broken this loop on small-tick contracts. On large-tick contracts, residual depth remains sufficient, and the loop continues to operate.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper documents a post-2009 collapse in short-term trend-following PnL using ~100 liquid futures contracts (1995-2025) and a CTA proxy. It shows the decay is concentrated on small volatility-normalised tick size contracts across horizons while large-tick contracts remain intact, and rejects capacity constraints, market electronification, and CTA-order-flow regime change on timing/magnitude/heterogeneity grounds. The authors interpret the tick-size split via a self-reinforcing impact loop that HFT liquidity withdrawal has disrupted on sparse (small-tick) books but not dense (large-tick) ones.

Significance. If the reported cross-sectional dichotomy by volatility-normalised tick size is robust, the result supplies a concrete microstructural channel for the post-crisis decay of short-term trend profitability and explains why the anomaly survived on some instruments. The explicit rejection of three competing explanations on observable dimensions (timing, asset-class heterogeneity) is a strength; the large futures panel and industry proxy add empirical weight.

major comments (2)

- [Abstract] Abstract (central empirical finding paragraph): the claim that volatility-normalised tick size is the sole cross-sectional variable that replicates the post-2008 PnL split is presented without the precise definition of the normalisation (volatility estimator, look-back, scaling), the statistical test for the small-tick vs large-tick difference, or any table showing the split after controlling for liquidity or asset class. This is load-bearing for the paper's main result.

- [Abstract] Abstract (final paragraph on microstructural mechanism): the interpretation that HFT liquidity-withdrawal behaviour broke the self-reinforcing impact loop on small-tick contracts is advanced without any direct measurement (pre/post-2008 price-impact coefficients, effective spreads on trend-sized orders, or slippage stratified by tick size). The timing/heterogeneity arguments against the other three explanations therefore rest on an untested causal channel.

minor comments (1)

- [Abstract] The abstract states 'roughly 100 liquid futures contracts' but does not list the exact universe or the liquidity filter applied; a table or appendix listing contracts and filters would improve reproducibility.

Simulated Author's Rebuttal

We thank the referee for the constructive comments on the abstract and the proposed mechanism. We address each point below, clarifying where details appear in the manuscript and noting where revisions or acknowledgments are appropriate.

read point-by-point responses

-

Referee: [Abstract] Abstract (central empirical finding paragraph): the claim that volatility-normalised tick size is the sole cross-sectional variable that replicates the post-2008 PnL split is presented without the precise definition of the normalisation (volatility estimator, look-back, scaling), the statistical test for the small-tick vs large-tick difference, or any table showing the split after controlling for liquidity or asset class. This is load-bearing for the paper's main result.

Authors: The definition of volatility-normalised tick size (tick size scaled by a 252-day rolling volatility estimate) appears in Section 2.2, the difference-in-differences test comparing post-2008 performance across the tick-size split is reported in Table 5 (with liquidity and asset-class controls), and the controlled cross-sectional results are shown in Figure 4 and Table 6. The abstract summarises these findings; we will add a concise parenthetical definition and a reference to the controlled tests to improve precision without exceeding length constraints. revision: yes

-

Referee: [Abstract] Abstract (final paragraph on microstructural mechanism): the interpretation that HFT liquidity-withdrawal behaviour broke the self-reinforcing impact loop on small-tick contracts is advanced without any direct measurement (pre/post-2008 price-impact coefficients, effective spreads on trend-sized orders, or slippage stratified by tick size). The timing/heterogeneity arguments against the other three explanations therefore rest on an untested causal channel.

Authors: The mechanism is offered as the interpretation that best organises the documented cross-sectional dichotomy and the timing evidence that rules out the three alternatives (Sections 5.1–5.3). We do not supply direct pre/post-2008 impact or slippage measurements stratified by tick size; the paper relies on the observable heterogeneity and the failure of competing explanations on those same dimensions. We will add an explicit caveat in the abstract and conclusion noting that the channel remains inferential pending direct impact evidence. revision: partial

- Direct pre/post-2008 price-impact coefficients, effective spreads on trend-sized orders, or slippage stratified by tick size

Circularity Check

No significant circularity; central result is empirical cross-sectional observation

full rationale

The paper's strongest claim is an empirical observation: post-2008 trend PnL collapsed on small volatility-normalised tick contracts but remained intact on large-tick ones, with asset class and liquidity failing to replicate the split. This is presented as a data-driven finding across ~100 futures contracts, not a derivation or prediction that reduces by the paper's own equations to fitted inputs or self-referential definitions. The four candidate explanations are rejected on timing/magnitude/heterogeneity grounds, and the microstructural feedback-loop account is offered as interpretation rather than a closed mathematical result. No self-citation load-bearing steps, ansatz smuggling, or renaming of known results appear in the provided text; the analysis is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Trend signals trigger directional trades whose market impact reinforces the price moves that generated the signal

invented entities (1)

-

HFT liquidity-withdrawal behaviour in front of predictable directional flow

no independent evidence

Reference graph

Works this paper leans on

-

[1]

2013 , publisher=

Nonlinear oscillations, dynamical systems, and bifurcations of vector fields , author=. 2013 , publisher=

2013

-

[2]

1993 , publisher=

Nonlinear dynamical economics and chaotic motion , author=. 1993 , publisher=

1993

-

[3]

The Journal of Finance , volume=

Sticky expectations and the profitability anomaly , author=. The Journal of Finance , volume=. 2019 , publisher=

2019

-

[4]

The Journal of finance , volume=

A unified theory of underreaction, momentum trading, and overreaction in asset markets , author=. The Journal of finance , volume=. 1999 , publisher=

1999

-

[5]

The Journal of finance , volume=

Bad news travels slowly: Size, analyst coverage, and the profitability of momentum strategies , author=. The Journal of finance , volume=. 2000 , publisher=

2000

-

[6]

The Journal of Finance , volume=

Does academic research destroy stock return predictability? , author=. The Journal of Finance , volume=. 2016 , publisher=

2016

-

[7]

Journal of Accounting and Economics , volume=

Have capital market anomalies attenuated in the recent era of high liquidity and trading activity? , author=. Journal of Accounting and Economics , volume=. 2014 , publisher=

2014

-

[8]

The Journal of finance , volume=

Returns to buying winners and selling losers: Implications for stock market efficiency , author=. The Journal of finance , volume=. 1993 , publisher=

1993

-

[9]

Quantitative Finance , volume=

Can heterogeneous agent models explain the alleged mispricing of the S&P 500? , author=. Quantitative Finance , volume=. 2021 , publisher=

2021

-

[10]

Industrial and Corporate Change , volume=

Market force, ecology and evolution , author=. Industrial and Corporate Change , volume=. 2002 , publisher=

2002

-

[11]

2023 , publisher=

Bayesian filtering and smoothing , author=. 2023 , publisher=

2023

-

[12]

The annals of Mathematical Statistics , volume=

A maximization technique occurring in the statistical analysis of probabilistic functions of Markov chains , author=. The annals of Mathematical Statistics , volume=. 1970 , publisher=

1970

-

[13]

JR Stat Soc Ser B , volume=

Maximum likelihood from incomplete data via the EM algorithm , author=. JR Stat Soc Ser B , volume=

-

[14]

Journal of the American Statistical Association , volume=

The EM approach to the multiple indicators and multiple causes model via the estimation of the latent variable , author=. Journal of the American Statistical Association , volume=. 1981 , publisher=

1981

-

[15]

Avraham Beja and M. Barry Goldman , title =. doi:10.1111/j.1540-6261.1980.tb02151.x , url =

-

[16]

2007 , publisher=

The complete turtletrader: The legend, the lessons, the results , author=. 2007 , publisher=

2007

-

[17]

Donchian , title =

Richard D. Donchian , title =. Commodity Yearbook , pages =

-

[18]

Journal of Asset Management , volume=

Breaking into the blackbox: Trend following, stop losses and the frequency of trading--The case of the S&P500 , author=. Journal of Asset Management , volume=. 2013 , publisher=

2013

-

[19]

Available at SSRN 1968996 , year=

Momentum strategies in futures markets and trend-following funds , author=. Available at SSRN 1968996 , year=

-

[20]

Journal of finance , volume=

Efficient capital markets , author=. Journal of finance , volume=

-

[21]

The Journal of Finance , volume=

Efficient capital markets: II , author=. The Journal of Finance , volume=. 1991 , publisher=

1991

-

[22]

Do Stock Prices Move Too Much to Be Justified by Subsequent Changes in Dividends? , volume =

Shiller, Robert , year =. Do Stock Prices Move Too Much to Be Justified by Subsequent Changes in Dividends? , volume =

-

[23]

The Review of Economic Studies , volume=

On the behaviour of commodity prices , author=. The Review of Economic Studies , volume=. 1992 , publisher=

1992

-

[24]

Journal of International Economics , volume=

Empirical exchange rate models of the seventies: Do they fit out of sample? , author=. Journal of International Economics , volume=. 1983 , publisher=

1983

-

[25]

The Review of Economic Studies , volume=

Yield spreads and interest rate movements: A bird's eye view , author=. The Review of Economic Studies , volume=. 1991 , publisher=

1991

-

[26]

G. William Schwert , keywords =. Chapter 15 Anomalies and market efficiency , series =. 2003 , booktitle =. doi:https://doi.org/10.1016/S1574-0102(03)01024-0 , url =

-

[27]

The Journal of Finance , volume=

Value and momentum everywhere , author=. The Journal of Finance , volume=. 2013 , publisher=

2013

-

[28]

Journal of financial economics , volume=

Some anomalous evidence regarding market efficiency , author=. Journal of financial economics , volume=

-

[29]

New York: Whittlesey House , author=

Security Analysis. New York: Whittlesey House , author=. New York: McGraw-Hill Book Company , year=

-

[30]

The Journal of Finance , volume=

Does the stock market overreact? , author=. The Journal of Finance , volume=. 1985 , publisher=

1985

-

[31]

Journal of portfolio management , volume=

Persuasive evidence of market inefficiency , author=. Journal of portfolio management , volume=

-

[32]

The Journal of Finance , volume=

Does the stock market rationally reflect fundamental values? , author=. The Journal of Finance , volume=. 1986 , publisher=

1986

-

[33]

The Journal of Finance , volume=

Stock prices, earnings, and expected dividends , author=. The Journal of Finance , volume=. 1988 , publisher=

1988

-

[34]

The Journal of Finance , volume=

The cross-section of expected stock returns , author=. The Journal of Finance , volume=. 1992 , publisher=

1992

-

[35]

Journal of financial economics , volume=

Size, value, and momentum in international stock returns , author=. Journal of financial economics , volume=. 2012 , publisher=

2012

-

[36]

The Journal of finance , volume=

Contrarian investment, extrapolation, and risk , author=. The Journal of finance , volume=. 1994 , publisher=

1994

-

[37]

2018 , journal=

Black was right: Price is within a factor 2 of Value , author=. 2018 , journal=

2018

-

[38]

The Journal of Finance , volume=

Evidence of predictable behavior of security returns , author=. The Journal of Finance , volume=. 1990 , publisher=

1990

-

[39]

The Journal of Finance , volume=

Positive feedback investment strategies and destabilizing rational speculation , author=. The Journal of Finance , volume=. 1990 , publisher=

1990

-

[40]

The Journal of Finance , volume=

Returns to buying winners and selling losers: Implications for stock market efficiency , author=. The Journal of Finance , volume=. 1993 , publisher=

1993

-

[41]

The Quarterly Journal of Economics , volume=

Fads, martingales, and market efficiency , author=. The Quarterly Journal of Economics , volume=. 1990 , publisher=

1990

-

[42]

The Journal of Finance , volume=

On persistence in mutual fund performance , author=. The Journal of Finance , volume=. 1997 , publisher=

1997

-

[43]

Journal of financial economics , volume=

Time series momentum , author=. Journal of financial economics , volume=. 2012 , publisher=

2012

-

[44]

Scientific Reports , volume=

The excess volatility puzzle explained by financial noise amplification from endogenous feedbacks , author=. Scientific Reports , volume=. 2022 , publisher=

2022

-

[45]

Journal of Investment Strategies , year=

Two centuries of trend following , author=. Journal of Investment Strategies , year=

-

[46]

1987 , institution =

Investor behavior in the October 1987 stock market crash: Survey evidence , author=. 1987 , institution =

1987

-

[47]

2000 , publisher=

Irrational Exuberance, Princeton Univ , author=. 2000 , publisher=

2000

-

[48]

The New Palgrave Dictionary of Economics, 2nd Edition

Excess volatility , author=. The New Palgrave Dictionary of Economics, 2nd Edition. Palgrave Macmillan , volume=

-

[49]

Google Scholar , year=

Advances in Behavioral Finance (Russell Sage Foundation, New York) , author=. Google Scholar , year=

-

[50]

2005 , publisher=

Advances in behavioral finance, Volume II , author=. 2005 , publisher=

2005

-

[51]

Nature , volume=

Scaling and criticality in a stochastic multi-agent model of a financial market , author=. Nature , volume=. 1999 , publisher=

1999

-

[52]

Routledge International Handbook of Complexity Economics , pages=

Exploration of the Parameter Space in Macroeconomic Models , author=. Routledge International Handbook of Complexity Economics , pages=. 2024 , publisher=

2024

-

[53]

Proceedings of the National Academy of Sciences , volume=

How market ecology explains market malfunction , author=. Proceedings of the National Academy of Sciences , volume=. 2021 , publisher=

2021

-

[54]

Reports on Progress in Physics , volume=

Information geometry for multiparameter models: New perspectives on the origin of simplicity , author=. Reports on Progress in Physics , volume=. 2022 , publisher=

2022

-

[55]

A century of evidence on trend-following investing , author=. 2017 , journal=. doi:10.3905/jpm.2017.44.1.015 , publisher=

-

[56]

Quantitative Finance , volume=

The inelastic market hypothesis: a microstructural interpretation , author=. Quantitative Finance , volume=. 2022 , publisher=

2022

-

[57]

The Journal of Finance , volume=

Noise , author=. The Journal of Finance , volume=. 1986 , publisher=

1986

-

[58]

arXiv preprint arXiv:2405.12768 , year=

Ponzi funds , author=. arXiv preprint arXiv:2405.12768 , year=

-

[59]

2021 , institution =

In Search of the Origins of Financial Fluctuations: The Inelastic Markets Hypothesis , author =. 2021 , institution =

2021

-

[60]

in Two Volumes

A Treatise on Money, by John Maynard Keynes... in Two Volumes... , author=. 1930 , publisher=

1930

-

[61]

Journal of political Economy , volume=

Returns to speculators: Telser versus Keynes , author=. Journal of political Economy , volume=. 1960 , publisher=

1960

-

[62]

2018 , publisher=

Trades, quotes and prices: financial markets under the microscope , author=. 2018 , publisher=

2018

-

[63]

The Journal of Finance , volume=

Investor psychology and security market under-and overreactions , author=. The Journal of Finance , volume=. 1998 , publisher=

1998

-

[64]

Allen Lane and Penguin Books, New York , year=

Fast and slow thinking , author=. Allen Lane and Penguin Books, New York , year=

-

[65]

2017 , publisher=

New experimental evidence on expectations formation , author=. 2017 , publisher=

2017

-

[66]

Handbook of Computational Economics , volume=

Heterogeneous agent models in economics and finance , author=. Handbook of Computational Economics , volume=. 2006 , publisher=

2006

-

[67]

Handbook of Computational Economics , volume=

Agent-based computational finance , author=. Handbook of Computational Economics , volume=. 2006 , publisher=

2006

-

[68]

Handbook of financial markets: Dynamics and evolution , pages=

Heterogeneity, market mechanisms, and asset price dynamics , author=. Handbook of financial markets: Dynamics and evolution , pages=. 2009 , publisher=

2009

-

[69]

Handbook of Computational Economics , volume=

Heterogeneous agent models in finance , author=. Handbook of Computational Economics , volume=. 2018 , publisher=

2018

-

[70]

Annals of Operations Research , volume=

The dynamics of speculative behaviour , author=. Annals of Operations Research , volume=. 1992 , publisher=

1992

-

[71]

Journal of Economic Dynamics and Control , volume=

An analysis of the effect of noise in a heterogeneous agent financial market model , author=. Journal of Economic Dynamics and Control , volume=. 2011 , publisher=

2011

-

[72]

Journal of Economic Dynamics and Control , volume=

Co-existence of trend and value in financial markets: Estimating an extended Chiarella model , author=. Journal of Economic Dynamics and Control , volume=. 2020 , issn =. doi:https://doi.org/10.1016/j.jedc.2019.103791 , publisher=

-

[73]

PLoS Computational Biology , volume=

Universally sloppy parameter sensitivities in systems biology models , author=. PLoS Computational Biology , volume=. 2007 , publisher=

2007

-

[74]

Quantitative Finance , volume=

Quadratic Hawkes processes for financial prices , author=. Quantitative Finance , volume=. 2017 , publisher=

2017

-

[75]

arXiv preprint arXiv:2001.04185 , year=

Zooming in on equity factor crowding , author=. arXiv preprint arXiv:2001.04185 , year=

-

[76]

The Footprint of Trend-Following: Can CTAs really move the market? , journal =

Quantica. The Footprint of Trend-Following: Can CTAs really move the market? , journal =

-

[77]

When Trend-Following Hits Capacity: A Case Study on Commodities , journal =

Quantica. When Trend-Following Hits Capacity: A Case Study on Commodities , journal =

-

[78]

and Hornbach, Matthew and tentes, Aristeidis and Qian, Krystal and Liu, Mingyong , title =

Lorenzen, Jakob Christian and Kessler, Stephan M. and Hornbach, Matthew and tentes, Aristeidis and Qian, Krystal and Liu, Mingyong , title =. Morgan Stanley Research , year =

-

[79]

Econometrica: Journal of the Econometric Society , pages=

Continuous auctions and insider trading , author=. Econometrica: Journal of the Econometric Society , pages=. 1985 , publisher=

1985

-

[80]

Journal of Economic Dynamics and Control , volume=

Behavioral heterogeneity in stock prices , author=. Journal of Economic Dynamics and Control , volume=. 2007 , publisher=

2007

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.