Taxing Artificial Intelligence

Pith reviewed 2026-07-03 05:59 UTC · model grok-4.3

The pith

Taxation can address AI harms by correcting activity, redistributing costs and gains, and funding regulatory capacity, beyond Pigouvian correction alone.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

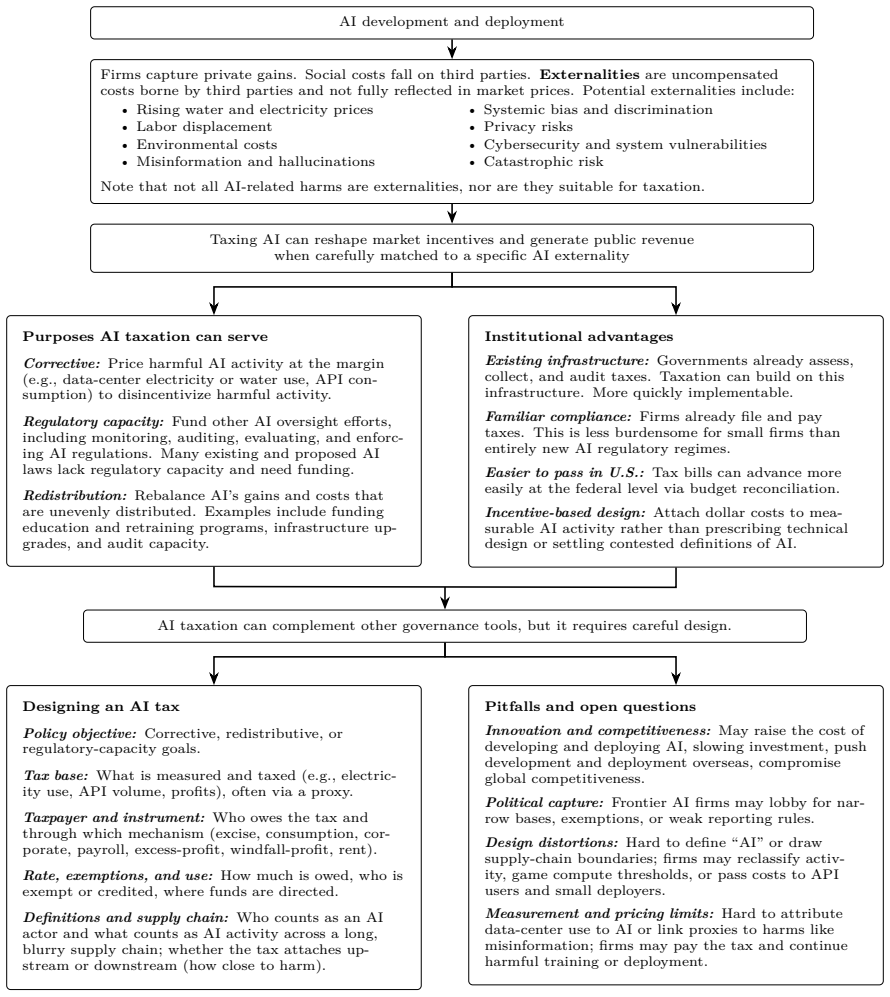

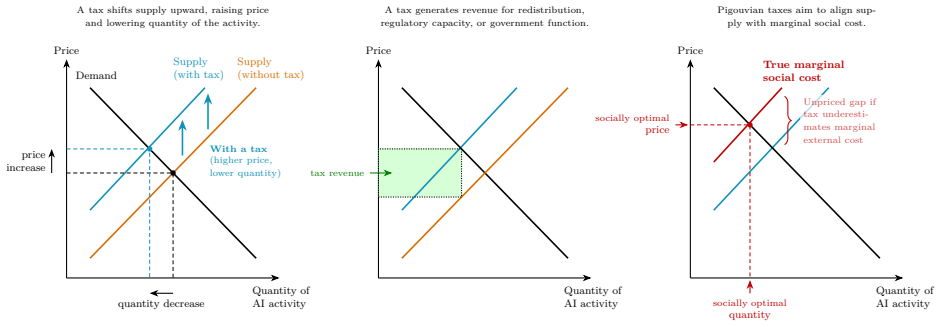

AI taxation should not be viewed solely as Pigouvian correction for externalities. Instead, it can correct harmful activity, redistribute unevenly borne costs and gains, and fund regulatory capacity. The paper surveys the main AI externalities and evaluates instruments including corporate income and rent-based taxes, consumption taxes on AI-related services, and excise taxes tied to specific activities, assessing each for feasibility, measurement challenges, incidence, leakage, and innovation costs. Because externalities differ in nuanced ways, tax policy must be designed to fit the particular harms and objectives.

What carries the argument

Survey of tax instruments (corporate income and rent-based taxes, consumption taxes on AI services, excise taxes on specific activities) and their evaluation against measurement problems, incidence, leakage, and innovation costs to match distinct AI externalities.

If this is right

- Tax design must be matched to the specific type of AI harm rather than applied uniformly.

- Excise instruments can target particular activities like high-compute training runs.

- Corporate and consumption taxes can shift gains toward those bearing displacement or environmental costs.

- Revenue from these taxes can support the administrative capacity needed for AI oversight.

- Policy must weigh feasibility and pitfalls for each instrument against the objective it serves.

Where Pith is reading between the lines

- Such taxes might alter the relative speed of different AI development paths by raising costs for activities with high externalities.

- The approach could link to existing labor or environmental tax regimes when AI harms overlap with those domains.

- Pilot implementations in specific sectors could test whether measurement of AI usage is practical at scale.

- Revenue recycling rules would determine whether redistribution actually reaches affected communities or stays at the national level.

Load-bearing premise

The listed tax instruments can be designed and implemented without prohibitive measurement problems, leakage, or innovation costs.

What would settle it

Data from implemented AI taxes showing persistent leakage to other jurisdictions or measurable slowdown in innovation without corresponding gains in redistribution or regulatory funding.

Figures

read the original abstract

While AI promises major benefits, its development and deployment can shift costs onto others, including environmental pressures on local communities, labor and creative displacement, and systemic risks from rapid frontier development. Taxation is an integral part of policy design, and recent academic, industry, and policy debates have begun to consider whether tax instruments can help address these harms. In this paper, we explore the viability of AI taxation. More broadly, AI taxation should not be understood only as Pigouvian correction. In the AI context, taxation can also correct harmful activity, redistribute unevenly borne costs and gains, and fund regulatory capacity. We discuss the main externalities associated with AI and survey possible tax instruments, including corporate income and rent-based taxes, consumption taxes on AI-related services, and excise instruments tied to specific AI activities. We further assess the benefits and pitfalls of these instruments, including feasibility, measurement problems, incidence, leakage, and innovation costs. Because AI externalities differ in nuanced ways, tax policy must be carefully designed and matched to the specific harms and policy objectives.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript claims that AI taxation should not be understood solely as Pigouvian correction for externalities. Instead, in the AI context it can also correct harmful activities, redistribute unevenly borne costs and gains, and fund regulatory capacity. It surveys key externalities (environmental pressures on communities, labor and creative displacement, systemic risks from frontier development) and possible instruments (corporate income and rent-based taxes, consumption taxes on AI services, excise taxes tied to specific activities), while assessing benefits and pitfalls including feasibility, measurement problems, incidence, leakage, and innovation costs. The conclusion is that tax policy must be carefully designed and matched to specific harms and objectives.

Significance. If the reframing holds, the paper offers a timely multi-objective conceptual framework for integrating taxation into AI governance debates. Its explicit treatment of design pitfalls as open questions rather than resolved provides a balanced basis for further policy analysis. The absence of formal models or empirical tests is consistent with the exploratory scope.

major comments (1)

- [Abstract] Abstract: the central reframing distinguishes 'Pigouvian correction' from the ability of taxation to 'correct harmful activity,' but Pigouvian taxes are by definition intended to correct externalities arising from harmful activities; this overlap is not addressed and risks undermining the claim that taxation serves distinct additional functions beyond standard externality correction.

minor comments (1)

- The manuscript would benefit from additional references to prior work on AI externalities and regulatory taxation to better situate its contribution within existing policy literature.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive review. The recommendation for minor revision is appreciated, and we address the single major comment below.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central reframing distinguishes 'Pigouvian correction' from the ability of taxation to 'correct harmful activity,' but Pigouvian taxes are by definition intended to correct externalities arising from harmful activities; this overlap is not addressed and risks undermining the claim that taxation serves distinct additional functions beyond standard externality correction.

Authors: We agree that the abstract's phrasing creates an unintended overlap. Pigouvian taxes are indeed designed to internalize externalities arising from harmful activities, so distinguishing 'correct harmful activity' as a separate function risks weakening the central claim. Our intent was to argue that taxation in the AI domain can pursue objectives beyond externality correction—specifically redistribution of unevenly distributed costs and gains, and financing regulatory capacity—while still acknowledging Pigouvian uses. We will revise the abstract (and any parallel language in the introduction) to remove the ambiguous phrasing, explicitly frame Pigouvian correction as one possible role, and reserve the 'also' language for the distinct functions of redistribution and regulatory funding. This change will be made in the next version. revision: yes

Circularity Check

No significant circularity

full rationale

The paper is a conceptual survey and policy discussion with no equations, derivations, fitted parameters, or mathematical models. It draws on standard economic principles of externalities, Pigouvian taxes, and redistribution without reducing any claim to its own inputs by construction. No self-citation load-bearing steps, uniqueness theorems, or ansatzes are invoked. The central reframing (taxation serving corrective, redistributive, and revenue functions) rests on external economic literature and explicit discussion of implementation pitfalls, making the argument self-contained.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption AI development and deployment generate identifiable negative externalities that policy instruments including taxation can address.

Reference graph

Works this paper leans on

-

[1]

Ryan Abbott and Bret Bogenschneider. 2018. Should Robots Pay Taxes? Tax Policy in the Age of Automation.Harvard Law & Policy Review12 (2018), 145–175. doi:10.2139/ssrn.2932483

-

[2]

AEP Ohio. 2026. PUCO Approves AEP Ohio Rate Settlement and a More Transparent Bill Format. https://www.aepohio.com/company/news/view?releaseID=11835News release. Published April 1,

2026

-

[3]

Accessed May 30, 2026

2026

-

[4]

International Energy Agency. 2025. AI Is Set to Drive Surging Electricity Demand from Data Centres While Offering the Potential to Transform How the Energy Sector Works.https://www.iea.org/ne ws/ai-is-set-to-drive-surging-electricity-demand-from-data-centres-while-offering-t he-potential-to-transform-how-the-energy-sector-works

2025

-

[5]

2025.Energy and AI

International Energy Agency. 2025.Energy and AI. World Energy Outlook Special Report. Interna- tional Energy Agency.https://iea.blob.core.windows.net/assets/de9dea13-b07d-42c5-a39 8-d1b3ae17d866/EnergyandAI.pdfAccessed May 30, 2026

2025

-

[6]

United States Environmental Protection Agency. 2007. Report to Congress on Server and Data Center Energy Efficiency.https://www.energystar.gov/ia/partners/prod_development/downloads/EP A_Datacenter_Report_Congress_Final1.pdf

2007

-

[7]

2017.Artificial intelligence and economic growth

Philippe Aghion, Benjamin F Jones, and Charles I Jones. 2017.Artificial intelligence and economic growth. Technical Report. National Bureau of Economic Research. 28

2017

-

[8]

Artificialintelligenceriskmanagementframework(AIRMF1.0).URL: https://nvlpubs

NISTAI.2023. Artificialintelligenceriskmanagementframework(AIRMF1.0).URL: https://nvlpubs. nist. gov/nistpubs/ai/nist. ai(2023), 100–1

2023

-

[9]

Shuroug A Alowais, Sahar S Alghamdi, Nada Alsuhebany, Tariq Alqahtani, Abdulrahman I Alshaya, Sumaya NAlmohareb, AtheerAldairem, MohammedAlrashed, Khalid BinSaleh, HishamABadreldin, et al. 2023. Revolutionizing healthcare: the role of artificial intelligence in clinical practice.BMC medical education23, 1 (2023), 689

2023

-

[10]

Dario Amodei. 2024. The Adolescence of Technology.https://www.darioamodei.com/essay/the-a dolescence-of-technology

2024

-

[11]

Dario Amodei. 2026. Policy on the AI Exponential.https://darioamodei.com/post/policy-on-t he-ai-exponentialEssay, published June 2026

2026

-

[12]

Virginia General Assembly. 2026. Data Center Electricity Consumption Tax.https://budget.lis .virginia.gov/amendment/2026/2/HB30/Introduced/CR/3-5.24/1c/HB30 Conference Report, Item 3-5.24 #1c

2026

-

[13]

Ohio Manufacturers’ Association. 2026. Inflated Ohio Utility Load Forecasts Drive Electric Prices Higher.https://www.ohiomfg.com/wp-content/uploads/2026/02/RetoolingOhio_AEP_Feb.pdf Accessed May 31, 2026

2026

-

[14]

Alan J Auerbach. 2006. Who bears the corporate tax? A review of what we know.Tax policy and the economy20 (2006), 1–40

2006

-

[15]

Ryan S Baker and Aaron Hawn. 2022. Algorithmic bias in education.International journal of artificial intelligence in education32, 4 (2022), 1052–1092

2022

-

[16]

Solon Barocas and Andrew D Selbst. 2016. Big data’s disparate impact.California law review(2016), 671–732

2016

-

[17]

Robert Bartlett, Adair Morse, Richard Stanton, and Nancy Wallace. 2022. Consumer-lending discrim- ination in the FinTech era.Journal of Financial Economics143, 1 (2022), 30–56

2022

-

[18]

1988.The theory of environmental policy

William J Baumol and Wallace E Oates. 1988.The theory of environmental policy. Cambridge uni- versity press

1988

-

[19]

Jeremy Bearer-Friend and Sarah Polcz. 2025. Sharing the Algorithm: The Tax Solution to Generative AI.Columbia Journal of Tax Law17, 1 (2025), 1–40. doi:10.52214/cjtl.v17i1.14478

-

[20]

Stuart Bender. 2025. Generative-AI, the media industries, and the disappearance of human creative labour.Media Practice and Education26, 2 (2025), 200–217

2025

-

[21]

Yoshua Bengio, Geoffrey Hinton, Andrew Yao, et al. 2024. Managing Extreme AI Risks Amid Rapid Progress.Science384 (2024), 842–845

2024

-

[22]

2025.Examining AI Safety as a Global Public Good: Implications, Challenges, and Research Priorities

Kayla Blomquist, Elisabeth Siegel, Ben Harack, Kwan Yee Ng, Tom David, Brian Tse, Charles Martinet, Matt Sheehan, Scott Singer, Imane Bello, Zakariyau Yusuf, Robert Trager, Fadi Salem, Seán Ó hÉigeartaigh, Jing Zhao, and Kai Jia. 2025.Examining AI Safety as a Global Public Good: Implications, Challenges, and Research Priorities. Technical Report. Oxford M...

2025

-

[23]

Ulrik Boesen. 2021. Excise tax application and trends.Tax foundation753 (2021). 29

2021

-

[24]

Rishi Bommasani, Drew A Hudson, Ehsan Adeli, Russ Altman, Simran Arora, Sydney von Arx, Michael S Bernstein, Jeannette Bohg, Antoine Bosselut, Emma Brunskill, et al. 2021. On the oppor- tunities and risks of foundation models.arXiv preprint arXiv:2108.07258(2021)

work page internal anchor Pith review Pith/arXiv arXiv 2021

- [25]

-

[26]

Rishi Bommasani, Kevin Klyman, Shayne Longpre, Betty Xiong, Sayash Kapoor, Nestor Maslej, Arvind Narayanan, and Percy Liang. 2024. Foundation model transparency reports. InProceedings of the AAAI/ACM Conference on AI, Ethics, and Society, Vol. 7. 181–195

2024

-

[27]

Rishi Bommasani, Dilara Soylu, Thomas I Liao, Kathleen A Creel, and Percy Liang. 2024. Ecosystem graphs: Documentingthefoundationmodelsupplychain.InProceedings of the AAAI/ACM Conference on AI, Ethics, and Society, Vol. 7. 196–209

2024

-

[28]

Y. Bonaparte. 2026. Should We Tax Robots? Innovation, Productivity, and the Future of Fiscal Policy. doi:10.2139/ssrn.4701234

-

[29]

N Bostrom. 2013. Existential risk prevention as global priority. Global Policy, 4 (1), 15-31

2013

-

[30]

Donald J Boudreaux and Roger Meiners. 2019. Externality: Origins and classifications.Nat. Res. J. 59 (2019), 1

2019

-

[31]

Robert Brauneis. 2025. Copyright and the Training of Human Authors and Generative Machines.The Columbia Journal of Law & the Arts48, 1 (2025), 1–59. doi:10.52214/jla.v48i1.13529

-

[32]

Tom Brown, Benjamin Mann, Nick Ryder, Melanie Subbiah, Jared D Kaplan, Prafulla Dhariwal, Arvind Neelakantan, Pranav Shyam, Girish Sastry, Amanda Askell, et al. 2020. Language models are few-shot learners.Advances in neural information processing systems33 (2020), 1877–1901

2020

-

[33]

Miles Brundage, Shahar Avin, Jack Clark, Helen Toner, Peter Eckersley, Ben Garfinkel, Allan Dafoe, Paul Scharre, Thomas Zeitzoff, Bobby Filar, et al. 2018. The malicious use of artificial intelligence: Forecasting, prevention, and mitigation.arXiv preprint arXiv:1802.07228(2018)

-

[34]

Miles Brundage, Noemi Dreksler, Aidan Homewood, Sean McGregor, Patricia Paskov, Conrad Stosz, Girish Sastry, A Feder Cooper, George Balston, Steven Adler, et al. 2026. Frontier AI Auditing: Toward Rigorous Third-Party Assessment of Safety and Security Practices at Leading AI Companies. arXiv preprint arXiv:2601.11699(2026)

-

[35]

Erik Brynjolfsson, Bharat Chandar, and Ruyu Chen. 2025. Canaries in the Coal Mine? Six Facts about the Recent Employment Effects of Artificial Intelligence.https://digitaleconomy.stanfor d.edu/app/uploads/2025/12/CanariesintheCoalMine_Nov25.pdf

2025

-

[36]

Erik Brynjolfsson, Danielle Li, and Lindsey Raymond. 2025. Generative AI at work.The Quarterly Journal of Economics140, 2 (2025), 889–942

2025

-

[37]

Daniel Bunn, Cristina Enache, and Ulrik Boesen. 2021. Consumption tax policies in OECD countries. Washington, D. C: Tax Foundation(2021)

2021

-

[38]

Thomas Buocz, Sebastian Pfotenhauer, and Iris Eisenberger. 2023. Regulatory sandboxes in the AI Act: reconciling innovation and safety?Law, Innovation and Technology15, 2 (2023), 357–389

2023

-

[39]

2025.Genai misinformation, trust, and news consumption: Evidence from a field experiment

Filipe R Campante, Ruben Durante, Felix Hagemeister, and Ananya Sen. 2025.Genai misinformation, trust, and news consumption: Evidence from a field experiment. Technical Report. National Bureau of Economic Research. 30

2025

-

[40]

Nicolas Carlini, Jamie Hayes, Milad Nasr, Matthew Jagielski, Vikash Sehwag, Florian Tramer, Borja Balle, Daphne Ippolito, and Eric Wallace. 2023. Extracting training data from diffusion models. (2023), 5253–5270

2023

-

[41]

Nicholas Carlini, Florian Tramer, Eric Wallace, Matthew Jagielski, Ariel Herbert-Voss, Katherine Lee, Adam Roberts, Tom Brown, Dawn Song, Ulfar Erlingsson, et al. 2021. Extracting training data from large language models. In30th USENIX security symposium (USENIX Security 21). 2633–2650

2021

- [42]

-

[43]

2017.Income Redistribution Through Taxes and Transfers Across OECD Countries

Orsetta Causa and Mikkel Hermansen. 2017.Income Redistribution Through Taxes and Transfers Across OECD Countries. OECD Economics Department Working Paper 1453. OECD. doi:10.1787/ bc7569c6-en

2017

-

[44]

Cen, Lindsey Gailmard, Rishi Bommasani, Daniel E

Sarah H. Cen, Lindsey Gailmard, Rishi Bommasani, Daniel E. Ho, and Percy Liang. 2025. Mapping the AI Supply Chain: An Analysis of the Complex Relationships in the AI Ecosystem.Forthcoming. (2025)

2025

-

[45]

Texas Senate Research Center. 2025. Bill Analysis: C.S.H.B. 149, Texas Responsible Artificial Intelli- gence Governance Act.https://capitol.texas.gov/tlodocs/89R/analysis/html/HB00149S.htm 89th Legislature, Regular Session. Committee Report, substituted. Dated May 20, 2025. Accessed May 30, 2026

2025

-

[46]

Alan Chan, Herbie Bradley, and Nitarshan Rajkumar. 2023. Reclaiming the digital commons: A public data trust for training data. InProceedings of the 2023 AAAI/ACM Conference on AI, Ethics, and Society. 855–868

2023

-

[47]

Vikram Chand, Svetislav Kostić, and Ariene Reis. 2020. Taxing artificial intelligence and robots: Critical assessment of potential policy solutions and recommendation for alternative approaches.World Tax Journal12, 4 (2020), 711–761

2020

-

[48]

Zhan-Ming Chen, Qiyang Xiong, Jiahui Duan, Jianhong Ma, Zhuo Chen, and Shan Guo. 2025. AI carbon footprint in China sets to double post-2030 carbon peaking.Energy Economics(2025), 108880

2025

-

[49]

Vince Chhabria. 2025. Order Denying the Plaintiffs’ Motion for Partial Summary Judgment and Granting Meta’s Cross-Motion for Partial Summary Judgment.https://law.justia.com/cases/f ederal/district-courts/california/candce/3:2023cv03417/415175/598/Kadrey et al. v. Meta Platforms, Inc., No. 23-cv-03417-VC, Document 598, N.D. Cal., filed June 25, 2025

2025

-

[50]

Cilluffo and Molly F

Anthony A. Cilluffo and Molly F. Sherlock. 2022. Payroll Taxes: An Overview of Taxes Imposed and Past Payroll Tax Relief.https://www.congress.gov/crs-product/R47062Accessed June 12, 2026

2022

-

[51]

Cristina E Ciocirlan and Bruce Yandle. 2003. The political economy of green taxation in OECD countries.European Journal of Law and Economics15, 3 (2003), 203–218

2003

-

[52]

Jennifer Cobbe, Michael Veale, and Jatinder Singh. 2023. Understanding accountability in algorithmic supply chains. InProceedings of the 2023 ACM Conference on Fairness, Accountability, and Trans- parency. 1186–1197

2023

-

[53]

Estefania Vergara Cobos, Selcen Cakir, S Straub, CZ Qiang, and C Torgusson. 2024. A review of the economic costs of cyber incidents.World Bank, Washington, DC, USA, Rep193919 (2024)

2024

-

[54]

Congressional Research Service. 2024. The Budget Reconciliation Process.https://crsreports.c ongress.gov/product/pdf/R/R44058 31

2024

-

[55]

Spencer J. Cox. 2026. Executive Order 2026-03: Establishing a Higher Bar for Data Center Develop- ment in Utah.https://governor.utah.gov/wp-content/uploads/2026.05.29-EO-Higher-Bar-f or-Data-Center-Development-1.pdfExecutive order, State of Utah

2026

-

[56]

Janet Currie and Firouz Gahvari. 2007. Transfers in Cash and In Kind: Theory Meets the Data. https://www.nber.org/system/files/working_papers/w13557/revisions/w13557.rev0.pdf

2007

-

[57]

Ernesto Dal Bó. 2006. Regulatory capture: A review.Oxford review of economic policy22, 2 (2006), 203–225

2006

-

[58]

James B Davies. 1991. The distributive effects of wealth taxes.Canadian public policy/analyse de Politiques(1991), 279–308

1991

-

[59]

Tatevik Davtyan. 2025. The US approach to AI regulation: Federal laws, policies, and strategies explained.Journal of Law, Technology, & the Internet16, 2 (2025), 223

2025

-

[60]

Donald DeLuca. 2007. Selected Paper from the 2007 IRS Research Conference: Aggregate Estimates of Small Business Taxpayer Compliance Burden.https://www.irs.gov/pub/irs-soi/07resconf deluca.pdf

2007

-

[61]

Michael P Devereux and Rachel Griffith. 1998. Taxes and the Location of Production: Evidence from a Panel of US Multinationals.Journal of public Economics68, 3 (1998), 335–367

1998

-

[62]

Christina Dimitropoulou. 2024. Robot Taxation: A Normative Tax Policy Analysis-Domestic and International Tax Considerations.IBFD Doctoral Series(2024)

2024

-

[63]

Ren Bin Lee Dixon and Heather Frase. 2025. Ai incidents: Key components for a mandatory reporting regime.Georgetown Center for Security and Emerging Technology(2025)

2025

-

[64]

Marcus Drometer, Marco Frank, Maria Hofbauer Pérez, Carla Rhode, Sebastian Schworm, and Tanja Stitteneder. 2018. Wealth and inheritance taxation: An overview and country comparison.ifo DICE Report16, 2 (2018), 45–54

2018

-

[65]

1994.Excise taxes

John Fitzgerald Due. 1994.Excise taxes. Vol. 1251. World Bank Publications

1994

-

[66]

Jerome Dumortier, Fengxiu Zhang, and John Marron. 2017. State and federal fuel taxes: The road ahead for US infrastructure funding.Transport Policy53 (2017), 39–49

2017

-

[67]

Kai Ebert, Nicolas Alder, Ralf Herbrich, and Philipp Hacker. 2026. AI, climate, and regulation: From data centers to the AI Act.Computer Law & Security Review61 (2026), 106326

2026

-

[68]

The Economist. 2025. Can AI Replace Junior Workers?The Economist(2025).https://www.econ omist.com/graphic-detail/2025/10/13/can-ai-replace-junior-workers

2025

-

[69]

Tyna Eloundou, Sam Manning, Pamela Mishkin, and Daniel Rock. 2024. GPTs are GPTs: Labor market impact potential of LLMs.Science384, 6702 (2024), 1306–1308

2024

-

[70]

Kristofer Erickson. 2024. AI and work in the creative industries: digital continuity or discontinuity? Creative Industries Journal(2024), 1–21

2024

-

[71]

Brett Hemenway Falk and Gerry Tsoukalas. 2026. The AI layoff trap.arXiv preprint arXiv:2603.20617 (2026)

work page internal anchor Pith review Pith/arXiv arXiv 2026

- [72]

-

[73]

Richard Fang, Rohan Bindu, Akul Gupta, and Daniel Kang. 2024. Llm agents can autonomously exploit one-day vulnerabilities.arXiv preprint arXiv:2404.08144(2024). 32

work page internal anchor Pith review Pith/arXiv arXiv 2024

-

[74]

Francesco Filippucci, Peter Gal, Cecilia Susanna Jona Lasinio, et al. 2024. The impact of artificial intelligence on productivity, distribution and growth. (2024)

2024

-

[75]

Jessica Fjeld, Nele Achten, Hannah Hilligoss, Adam Nagy, and Madhulika Srikumar. 2020. Principled artificial intelligence: Mapping consensus in ethical and rights-based approaches to principles for AI. Berkman Klein Center Research Publication2020-1 (2020)

2020

-

[76]

Victor Fleischer. 2015. Curb your enthusiasm for Pigovian taxes.Vand. L. Rev.68 (2015), 1673

2015

-

[77]

I Can’t Drink the Water

Michelle Fleury and Nathalie Jimenez. 2025. “I Can’t Drink the Water” - Life Next to a US Data Centre.BBC News(2025).https://www.bbc.com/news/articles/cy8gy7lv448o

2025

-

[78]

Luciano Floridi, Matthias Holweg, Mariarosaria Taddeo, Javier Amaya, Jakob Mökander, and Yuni Wen. 2022. CapAI-A procedure for conducting conformity assessment of AI systems in line with the EU artificial intelligence act.Available at SSRN 4064091(2022)

2022

-

[79]

Food and Drug Administration

U.S. Food and Drug Administration. 2024. FDA User Fees Explained.https://www.fda.gov/indu stry/fda-user-fee-programs/fda-user-fees-explained

2024

-

[80]

Platform for Collaboration on Tax. 2018. Taxation and the Sustainable Development Goals.https: //www.tax-platform.org/sites/pct/files/publications/130559-WP-ReportFinalMar.pdf

2018

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.