The Mathematics of Modeling the Future

Pith reviewed 2026-06-26 14:43 UTC · model grok-4.3

The pith

Forecasting is the construction of dynamically coherent conditional distributions constrained by information, geometry, and admissible models.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

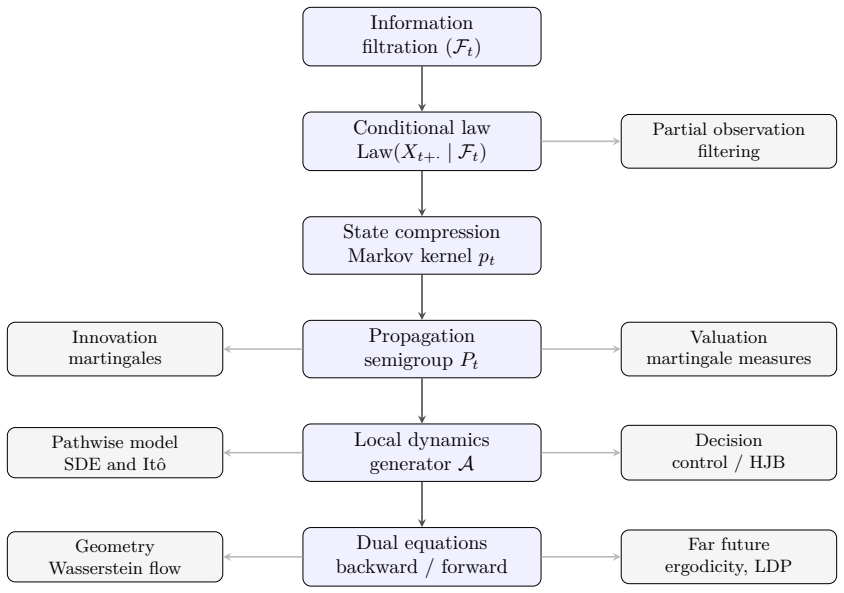

Modeling the future requires specifying conditional laws relative to an evolving information flow and describing their movement across time. Along a single spine, filtrations, conditional probabilities, Markov kernels, semigroups, and infinitesimal generators are connected so that the tower property becomes the semigroup law, Ito's formula yields the backward equation, integration by parts supplies the forward operator, and generator perturbations become model-risk distortions. This produces Kolmogorov equations, stochastic differential equations, Wasserstein gradient flows, and placements within Hilbert, Fisher-Rao, and Wasserstein geometries, with concrete outputs for Gaussian and non-Gaus

What carries the argument

The single spine that aligns filtrations, regular conditional probabilities, Markov kernels, semigroups, and infinitesimal generators into a unified forecasting calculus.

Load-bearing premise

Every listed object such as filtrations, regular conditional probabilities, Markov kernels, and infinitesimal generators can be aligned along one spine without additional technical conditions or loss of applicability to the concrete processes used.

What would settle it

A specific stochastic process where the tower property fails to map directly to the semigroup law or where generator perturbations no longer represent model-risk distortions without breaking the claimed unification.

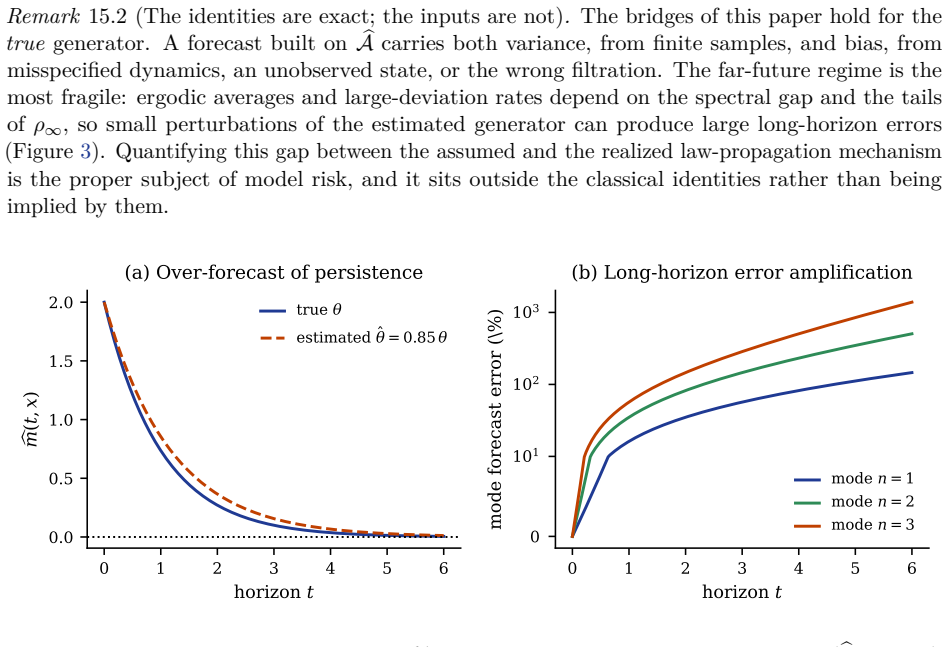

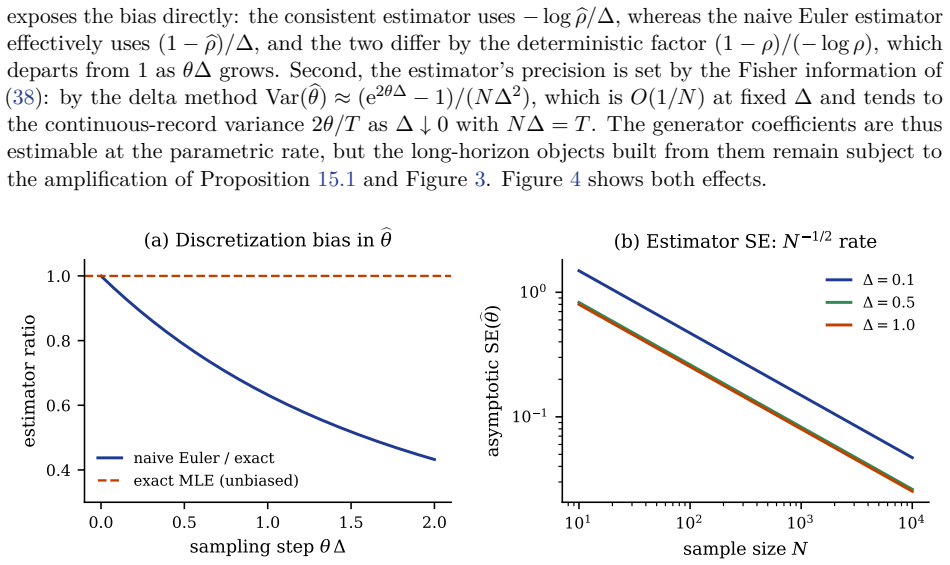

Figures

read the original abstract

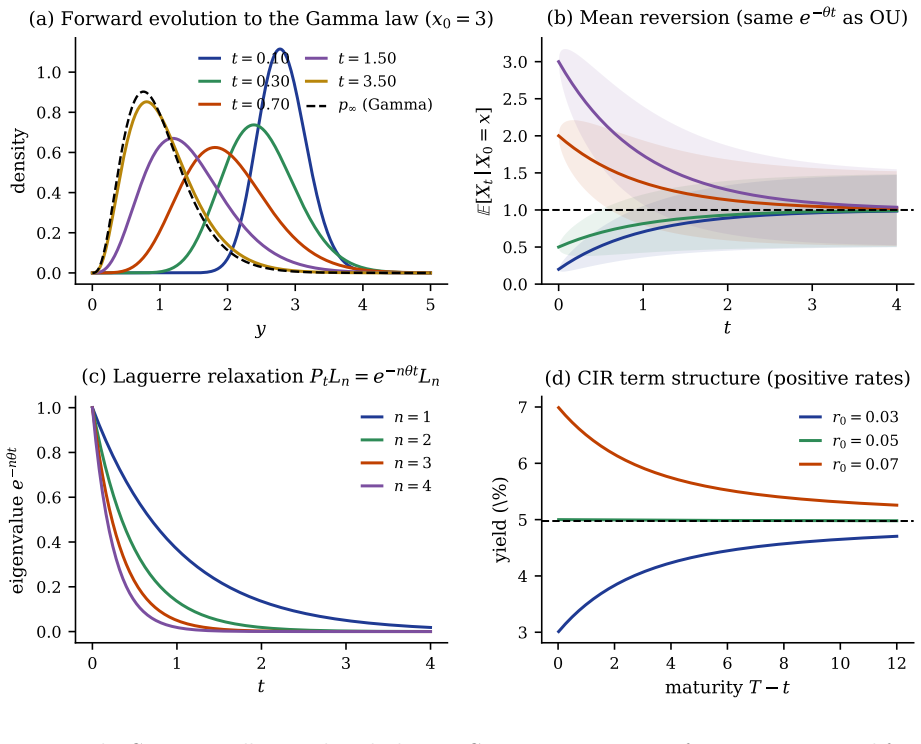

Modeling the future requires specifying conditional laws relative to an evolving information flow and describing their movement across time. This paper provides a unified mathematical synthesis of this problem along a single spine. Filtrations encode known data; conditional expectation and regular conditional probabilities yield point and distributional forecasts; Markov kernels and semigroups propagate observables and laws; and infinitesimal generators encode local dynamics, producing Kolmogorov equations and stochastic differential equations. Along this spine, martingales isolate surprise, filtering handles partial observation, finance prices futures, stochastic control optimizes choices, and ergodic theory describes the far future. The contribution is architectural. We explicitly connect derivations that turn classical objects into a unified forecasting calculus: the tower property becomes the semigroup law; Ito's formula yields the backward equation after conditioning; integration by parts provides the forward operator; and generator perturbations become model-risk distortions. Forecasting is shown not as mere data extrapolation, but the construction of dynamically coherent conditional distributions constrained by information, geometry, and admissible models. These concepts are illustrated via Gaussian Ornstein--Uhlenbeck and non-Gaussian Cox--Ingersoll--Ross processes, demonstrating how abstract machinery produces explicit transition laws, spectral decompositions, term-structure formulae, and asymptotics in diverse geometries. We recast density evolution as a Wasserstein gradient flow, place forecasting within Hilbert, Fisher--Rao, and Wasserstein geometries, provide a discrete-time empirical dictionary, and address model-risk. The result is a compact mathematical map from information to prediction, local dynamics to global laws, and idealized models to empirical forecasting.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper claims to provide a unified mathematical synthesis of forecasting along a single 'spine': filtrations encode information; conditional expectation and regular conditional probabilities yield point and distributional forecasts; Markov kernels and semigroups propagate observables and laws; infinitesimal generators encode local dynamics, producing Kolmogorov equations and SDEs. It explicitly connects the tower property to the semigroup law, Itô's formula to the backward equation after conditioning, integration by parts to the forward operator, and generator perturbations to model-risk distortions. Forecasting is recast as construction of dynamically coherent conditional distributions. These are illustrated via OU and CIR processes to produce explicit transition laws, spectral decompositions, term-structure formulae, and asymptotics; density evolution is recast as a Wasserstein gradient flow; forecasting is placed in Hilbert, Fisher-Rao, and Wasserstein geometries; a discrete-time empirical dictionary and model-risk discussion are included.

Significance. If the claimed connections hold rigorously, the synthesis could offer a compact organizational map useful for linking information flow to prediction in mathematical finance applications such as futures pricing and stochastic control. The concrete derivations for OU and CIR processes creditably demonstrate how the abstract machinery yields term structures and asymptotics in different geometries. The contribution is primarily architectural and expository, relying on classical objects without new theorems, machine-checked proofs, or parameter-free derivations; its significance therefore hinges on whether the re-organization provides substantive insight beyond standard textbook connections.

major comments (2)

- [Abstract] Abstract: the central claim that the listed objects (filtrations, regular conditional probabilities, Markov kernels, infinitesimal generators) align along one spine without additional technical conditions is load-bearing for the generality asserted. Regular conditional probabilities exist only under topological assumptions (e.g., Polish spaces); the semigroup law follows from the tower property only under the strong Markov property and Feller continuity; the link from Itô's formula to the backward equation requires a Feller-Dynkin Markov process. These hold for the OU and CIR illustrations but are not verified or restricted in the general synthesis.

- [Abstract] Abstract (connections paragraph): the assertion of 'explicit connections and derivations' that turn classical objects into a unified forecasting calculus is not accompanied by the actual derivations or error analysis. Without these, it cannot be confirmed whether the claimed reductions (tower property to semigroup law; Itô to backward equation) are rigorous or reduce by construction to properties already present in the standard definitions of the cited objects.

minor comments (1)

- The abstract is information-dense; a schematic diagram of the 'spine' and its connections would improve readability.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive report. The comments correctly identify that the architectural synthesis rests on classical technical conditions and that the claimed connections would benefit from more explicit step-by-step derivations in the text. We address each point below and will revise accordingly.

read point-by-point responses

-

Referee: [Abstract] the central claim that the listed objects (filtrations, regular conditional probabilities, Markov kernels, infinitesimal generators) align along one spine without additional technical conditions is load-bearing... Regular conditional probabilities exist only under topological assumptions (e.g., Polish spaces); the semigroup law follows from the tower property only under the strong Markov property and Feller continuity; the link from Itô's formula to the backward equation requires a Feller-Dynkin Markov process. These hold for the OU and CIR illustrations but are not verified or restricted in the general synthesis.

Authors: We agree that the general claims presuppose standard regularity conditions from the literature. In the revised version we will insert a short preliminary subsection (new Section 2) that explicitly lists the standing assumptions: Polish state spaces for regular conditional probabilities, the strong Markov property together with Feller continuity for the semigroup law, and the Feller-Dynkin setting for the generator-to-Kolmogorov link. We will note that these conditions are satisfied by the OU and CIR examples and that the spine is therefore presented as a unifying map under these classical hypotheses rather than as a claim of unrestricted generality. revision: yes

-

Referee: [Abstract] the assertion of 'explicit connections and derivations' that turn classical objects into a unified forecasting calculus is not accompanied by the actual derivations or error analysis. Without these, it cannot be confirmed whether the claimed reductions (tower property to semigroup law; Itô to backward equation) are rigorous or reduce by construction to properties already present in the standard definitions.

Authors: The connections follow directly from the definitions once the Markov and Feller assumptions are in place: the tower property applied to the Markov kernel yields the semigroup law by construction; conditioning Itô's formula produces the backward equation with no additional error term under the stated regularity. We will expand the manuscript with a dedicated subsection (new Section 3) that writes out these derivations line by line, together with a brief remark on the absence of remainder terms when the process is Feller. This will make the reductions transparent without introducing new theorems. revision: yes

Circularity Check

No circularity; architectural synthesis of classical results

full rationale

The paper's central contribution is an explicit connection of standard objects (tower property to semigroup law, Ito's formula to backward Kolmogorov equation, generator perturbations to model-risk) drawn from classical stochastic process theory. These links are not derived within the paper but invoked as known properties of filtrations, Markov kernels, and Feller-Dynkin processes; the illustrations with OU and CIR processes simply instantiate those properties. No step reduces a claimed result to a fitted parameter, self-citation chain, or definitional tautology; the work is therefore self-contained against external mathematical benchmarks.

Axiom & Free-Parameter Ledger

axioms (3)

- standard math Existence and regularity of conditional probabilities with respect to a filtration

- standard math Markov property and the existence of transition kernels for the processes considered

- standard math Existence of infinitesimal generators for the Ornstein-Uhlenbeck and Cox-Ingersoll-Ross processes

Reference graph

Works this paper leans on

-

[1]

Olav Kallenberg , title =

-

[2]

David Williams , title =

-

[3]

Claude Dellacherie and Paul-Andr\'e Meyer , title =

-

[4]

Ethier and Thomas G

Stewart N. Ethier and Thomas G. Kurtz , title =

-

[5]

Daniel Revuz and Marc Yor , title =

-

[6]

L. C. G. Rogers and David Williams , title =. 2000 , note =

2000

-

[7]

Amnon Pazy , title =

-

[8]

Adam Bobrowski , title =

-

[9]

Norris , title =

James R. Norris , title =

-

[10]

Shreve , title =

Ioannis Karatzas and Steven E. Shreve , title =

-

[11]

Stochastic Differential Equations: An Introduction with Applications , publisher =

Bernt. Stochastic Differential Equations: An Introduction with Applications , publisher =

-

[12]

Stroock and S

Daniel W. Stroock and S. R. Srinivasa Varadhan , title =

-

[13]

Protter , title =

Philip E. Protter , title =

-

[14]

David Applebaum , title =

-

[15]

Alan Bain and Dan Crisan , title =

-

[16]

Liptser and Albert N

Robert S. Liptser and Albert N. Shiryaev , title =

-

[17]

Olivier Capp\'e and Eric Moulines and Tobias Ryd\'en , title =

-

[18]

Freddy Delbaen and Walter Schachermayer , title =

-

[19]

Arbitrage Theory in Continuous Time , publisher =

Tomas Bj. Arbitrage Theory in Continuous Time , publisher =

-

[20]

Darrell Duffie , title =

-

[21]

Journal of Financial Economics , volume =

Oldrich Vasicek , title =. Journal of Financial Economics , volume =

-

[22]

Scheinkman , title =

Lars Peter Hansen and Jos\'e A. Scheinkman , title =. Econometrica , volume =

-

[23]

Fleming and Halil Mete Soner , title =

Wendell H. Fleming and Halil Mete Soner , title =

-

[24]

Jiongmin Yong and Xun Yu Zhou , title =

-

[25]

Meyn and Richard L

Sean P. Meyn and Richard L. Tweedie , title =

-

[26]

Giuseppe Da Prato and Jerzy Zabczyk , title =

-

[27]

Amir Dembo and Ofer Zeitouni , title =

-

[28]

Freidlin and Alexander D

Mark I. Freidlin and Alexander D. Wentzell , title =

-

[29]

SIAM Journal on Mathematical Analysis , volume =

Richard Jordan and David Kinderlehrer and Felix Otto , title =. SIAM Journal on Mathematical Analysis , volume =

-

[30]

Communications in Partial Differential Equations , volume =

Felix Otto , title =. Communications in Partial Differential Equations , volume =

-

[31]

Luigi Ambrosio and Nicola Gigli and Giuseppe Savar\'e , title =

-

[32]

C\'edric Villani , title =

-

[33]

Dominique Bakry and Ivan Gentil and Michel Ledoux , title =

-

[34]

Cox and Jonathan E

John C. Cox and Jonathan E. Ingersoll and Stephen A. Ross , title =. Econometrica , volume =

-

[35]

Annals of Mathematics , volume =

William Feller , title =. Annals of Mathematics , volume =

-

[36]

Taylor , title =

Samuel Karlin and Howard M. Taylor , title =

-

[37]

Shun-ichi Amari , title =

-

[38]

urgen Jost and H\^ong V\^an L\^e and Lorenz Schwachh\

Nihat Ay and J\"urgen Jost and H\^ong V\^an L\^e and Lorenz Schwachh\"ofer , title =

-

[39]

David Nualart , title =

-

[40]

Econometrica , volume =

Yacine A\"it-Sahalia , title =. Econometrica , volume =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.