Mitigating Adverse Selection in Concentrated Liquidity AMMs with Dynamic Fees: An Agent-Based Model Approach

Pith reviewed 2026-06-26 06:02 UTC · model grok-4.3

The pith

Dynamic fee schedules in concentrated liquidity AMMs can improve liquidity provider profitability by increasing fee income during periods of stale-price risk.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

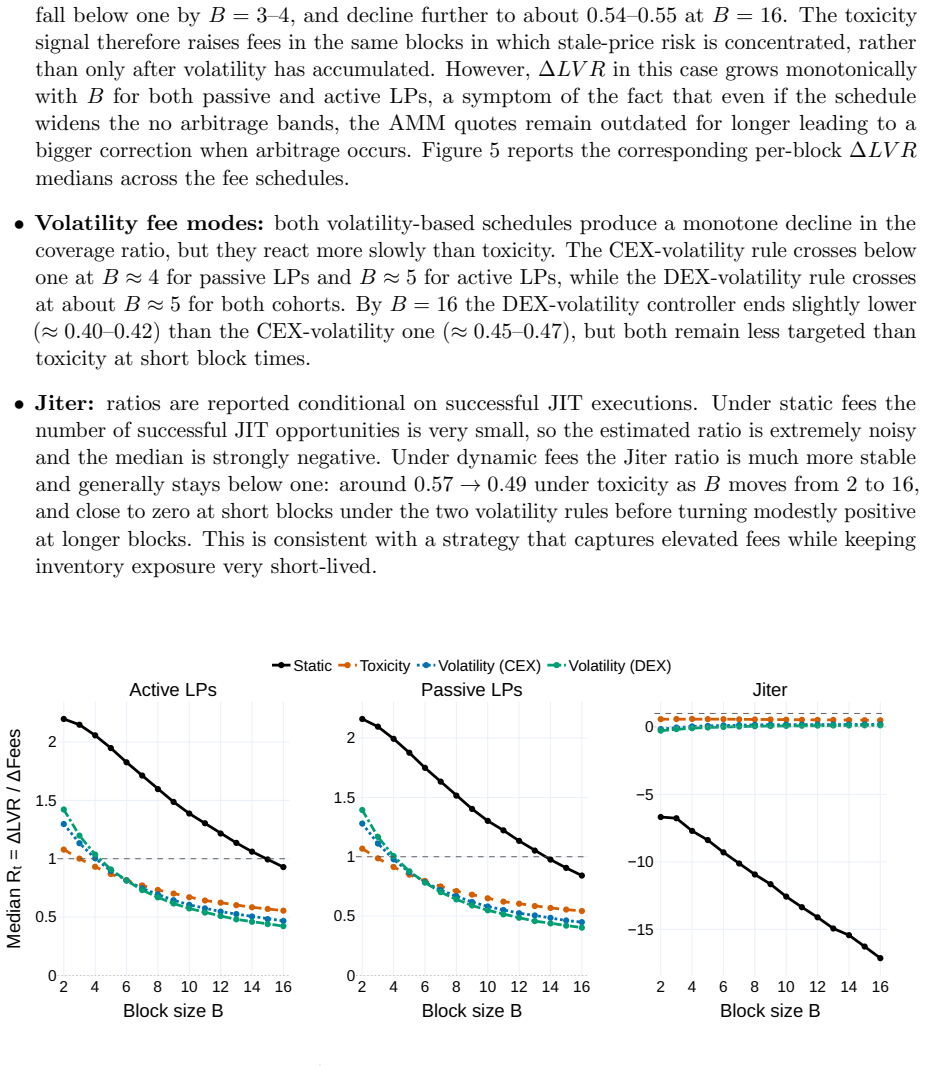

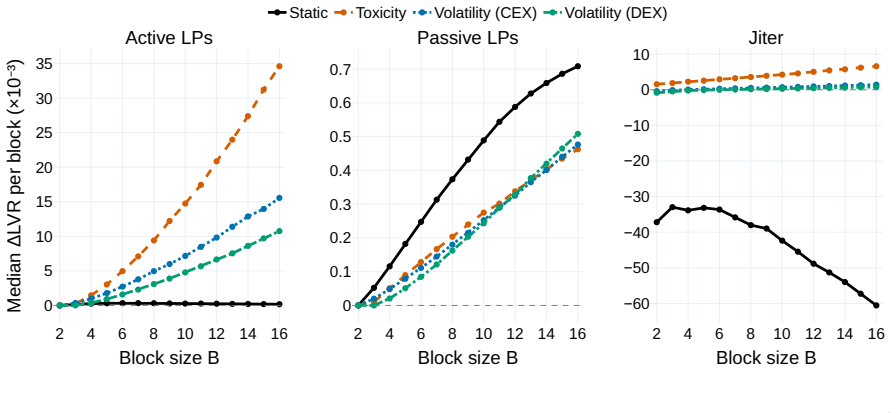

In the agent-based simulations, dynamic fee adjustments driven by volatility and toxicity proxies allow liquidity providers to achieve positive hedged profit and loss by raising fee income in states associated with stale-price risk. The aggregate results support the idea that these fees compensate for loss-versus-rebalancing more directly than they reduce it, depending on the specific configuration of the fee schedule.

What carries the argument

An agent-based model of a concentrated liquidity AMM interacting with a Heston stochastic reference market, incorporating heterogeneous agents including latency-sensitive arbitrageurs, smart routers, MEV searchers, and active LPs, used to evaluate dynamic fee schedules based on volatility and order-flow toxicity.

If this is right

- Liquidity providers can achieve positive hedged P&L under dynamic fee rules in the simulated environment.

- Fee income increases particularly in states with stale-price risk.

- Dynamic fees may influence realized LVR but primarily act through compensation rather than reduction.

- These effects depend on the specific configuration of the fee adjustment rules.

Where Pith is reading between the lines

- If the model holds, real-world AMMs could implement on-chain volatility or toxicity oracles to set fees dynamically.

- Extending the model to include more complex agent strategies might reveal interactions between fee changes and trading behavior.

- Comparing model outputs to historical on-chain LP performance data could validate the compensation mechanism.

Load-bearing premise

The behaviors and interactions of the modeled agents, such as how they respond to fee changes, accurately reflect real blockchain trading dynamics.

What would settle it

Running the same dynamic fee rules on actual historical Uniswap v3 pool data and observing whether hedged LP profitability increases as predicted by the model.

Figures

read the original abstract

Automated Market Makers based on concentrated liquidity, such as Uniswap v3, significantly improve capital efficiency but expose Liquidity Providers (LPs) to adverse selection costs, formalized as Loss-Versus-Rebalancing (LVR). While theoretical literature quantifies these costs, the interplay between realistic blockchain microstructure and endogenous pricing mechanisms remains under-explored. This paper develops a granular Agent-Based Model of a Uniswap v3 pool interacting with a stochastic reference market governed by Heston volatility dynamics. The framework incorporates discrete block propagation, mempool latency, and a heterogeneous population of agents, including latency-sensitive arbitrageurs, smart routers, Maximal Extractable Value searchers, and active LPs benchmarked against a frictionless rebalancing strategy. We propose and evaluate dynamic fee schedules driven by volatility and order-flow toxicity proxies intended to compensate LPs for adverse-selection losses. Our simulations investigate the conditions under which LPs can achieve positive hedged Profit and Loss (fees minus LVR). The analysis suggests that dynamic fee adjustments can improve hedged LP profitability mainly by increasing fee income in states associated with stale-price risk. Depending on the configuration, these rules may also affect realized LVR, but the current aggregate results support compensation for LVR more directly than a reduction of LVR itself.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops an agent-based model of a Uniswap v3 concentrated liquidity pool interacting with a Heston stochastic reference market that incorporates discrete blocks, mempool latency, and heterogeneous agents (latency-sensitive arbitrageurs, smart routers, MEV searchers, active LPs). It proposes dynamic fee schedules driven by volatility and order-flow toxicity proxies to compensate LPs for adverse selection (LVR), and reports simulation results indicating that these fees improve hedged LP P&L primarily by increasing fee income in stale-price states rather than by reducing realized LVR.

Significance. If the simulation framework were externally validated, the work would provide a useful bridge between theoretical LVR analysis and realistic blockchain microstructure, offering concrete guidance on dynamic fee design for concentrated liquidity AMMs. The ABM setup allows endogenous exploration of agent responses that static models cannot capture. At present, however, the lack of calibration to on-chain data substantially weakens the applicability of the reported compensation effect.

major comments (3)

- Abstract: the dynamic fee schedules are driven by volatility and toxicity proxies that are themselves simulation outputs; any measured improvement in hedged P&L therefore reduces, by construction, to the choice of those internally defined rules rather than an independent external benchmark.

- Model description and agent rules: the heterogeneous population (latency-sensitive arbitrageurs, MEV searchers, smart routers, active LPs) and their interaction rules (order placement, toxicity detection, rebalancing) are specified with only three free parameters plus Heston-driven prices and discrete blocks, yet no calibration or out-of-sample matching to observed Uniswap v3 metrics (arbitrage volume, LP returns net of LVR during volatility spikes) is reported.

- Simulation results and analysis: robustness checks, parameter sensitivity, and comparison to real on-chain data are not described, leaving the central claim that dynamic fees compensate for LVR more directly than they reduce it dependent on unvalidated internal agent behaviors.

Simulated Author's Rebuttal

We thank the referee for the detailed and constructive report. The comments correctly identify that the current version presents an exploratory ABM without external calibration or robustness checks. We agree these elements would strengthen applicability and will incorporate clarifications, sensitivity analyses, and explicit scope limitations in a revised manuscript. Below we respond point by point.

read point-by-point responses

-

Referee: Abstract: the dynamic fee schedules are driven by volatility and toxicity proxies that are themselves simulation outputs; any measured improvement in hedged P&L therefore reduces, by construction, to the choice of those internally defined rules rather than an independent external benchmark.

Authors: We agree that the reported P&L improvement is conditional on the specific internally generated proxies and fee rules chosen. The manuscript's intent is to demonstrate how such rules, when embedded in a microstructure-aware ABM, can produce compensation effects; it does not claim external optimality. We will revise the abstract to state explicitly that results are conditional on the proposed volatility- and toxicity-driven schedules and to emphasize the exploratory nature of the exercise. revision: partial

-

Referee: Model description and agent rules: the heterogeneous population (latency-sensitive arbitrageurs, MEV searchers, smart routers, active LPs) and their interaction rules (order placement, toxicity detection, rebalancing) are specified with only three free parameters plus Heston-driven prices and discrete blocks, yet no calibration or out-of-sample matching to observed Uniswap v3 metrics (arbitrage volume, LP returns net of LVR during volatility spikes) is reported.

Authors: The model was deliberately kept parsimonious (three free parameters) to isolate the effects of latency, toxicity detection, and dynamic fees. Full calibration against on-chain Uniswap v3 data (arbitrage volumes, LP returns) was not performed and would require substantial additional empirical work. We will add an explicit limitations subsection discussing this choice and outlining a calibration roadmap; we will also report sensitivity of key outcomes to the three free parameters. revision: partial

-

Referee: Simulation results and analysis: robustness checks, parameter sensitivity, and comparison to real on-chain data are not described, leaving the central claim that dynamic fees compensate for LVR more directly than they reduce it dependent on unvalidated internal agent behaviors.

Authors: We accept that the absence of robustness checks and on-chain comparisons limits the strength of the central claim. In revision we will (i) add parameter-sensitivity tables for the three free parameters, (ii) include additional simulation runs under alternative agent-behavior specifications, and (iii) insert a dedicated limitations paragraph that qualifies the compensation result as model-dependent pending external validation. revision: partial

Circularity Check

No significant circularity detected

full rationale

The paper constructs an agent-based model with Heston-driven reference prices, discrete blocks, and heterogeneous agents to evaluate proposed dynamic fee rules based on volatility and toxicity proxies. The reported outcome (improved hedged P&L via higher fee income in stale-price states) is a simulation result, not a reduction by construction to the fee-setting rules or to fitted parameters. No self-definitional steps, fitted-input predictions, or load-bearing self-citations appear in the abstract or described framework. The model is self-contained with independent stochastic dynamics and agent rules that are not tautological with the measured compensation effect.

Axiom & Free-Parameter Ledger

free parameters (3)

- Heston volatility parameters

- Dynamic fee coefficients

- Agent behavior parameters

axioms (2)

- domain assumption The Heston model is an appropriate description of the reference market price dynamics.

- domain assumption Discrete block propagation and mempool latency sufficiently capture blockchain microstructure effects on adverse selection.

invented entities (1)

-

Volatility- and toxicity-driven dynamic fee schedule

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Adams, N

H. Adams, N. Zinsmeister, and D. H. Robinson. Uniswap v2 core, 2020

2020

-

[2]

Adams, N

H. Adams, N. Zinsmeister, M. Salem, R. Keefer, and D. Robinson. Uniswap v3 Core Whitepaper. https://uniswap.org/whitepaper-v3.pdf, 2021

2021

-

[3]

Algebra Integral: Adaptive Fee Technical Reference

Algebra Finance. Algebra Integral: Adaptive Fee Technical Reference. https://docs.algebra. finance/algebra-integral-technical-reference/adaptive-fee , 2026. Accessed 2026-01- 09

2026

-

[4]

Algebra Protocol Tech Paper

Algebra Protocol. Algebra Protocol Tech Paper. https://docs.algebra.finance/Algebra% 20Protocol%20Tech%20paper.pdf, 2026. Accessed 2026-01-09

2026

-

[5]

Angeris, H.-T

G. Angeris, H.-T. Kao, R. Chiang, C. Noyes, and T. Chitra. An Analysis of Uniswap Markets. Cryptoeconomic Systems, 1(1), 2021

2021

-

[6]

Avellaneda and S

M. Avellaneda and S. Stoikov. High-frequency trading in a limit order book.Quantitative Finance, 8(3):217–224, 2008

2008

-

[7]

W. A. Brock, C. H. Hommes, and F. O. O. Wagener. More hedging instruments may destabilize markets.Journal of Economic Dynamics and Control, 33(11):1912–1928, 2009

1912

-

[8]

A. Canidio and R. Fritsch. Arbitrageurs’ profits, lvr, and sandwich attacks: batch trading as an amm design response.arXiv preprint arXiv:2307.02074, 2025

-

[9]

Carro, R

A. Carro, R. Toral, and M. San Miguel. Markets, herding and response to external information. PLoS ONE, 10(7):e0133287, 2015

2015

-

[10]

Cartea, F

´A. Cartea, F. Drissi, and M. Monga. Decentralised finance and automated market making: Execution and speculation.Journal of Economic Dynamics and Control, 177:105134, 2025

2025

-

[11]

Cartea, S

´A. Cartea, S. Jaimungal, and J. Penalva.Algorithmic and High-Frequency Trading. Cambridge University Press, Cambridge, 2015

2015

-

[12]

Chakraborti, I

A. Chakraborti, I. M. Toke, M. Patriarca, and F. Abergel. Econophysics review: Ii. agent-based models.Quantitative Finance, 11(7):1013–1041, 2011. 35

2011

-

[13]

S. N. Cohen, M. Sabat’e-Vidales, D. ˇSiˇ ska, and L. Szpruch. Inefficiency of CFMs: Hedging Perspective and Agent-Based Simulations. InFinancial Cryptography and Data Security. FC 2023 International Workshops, volume 13953 ofLecture Notes in Computer Science, pages 303–319. Springer, 2023

2023

-

[14]

CryptoSwap / Curve v2 Whitepaper

Curve Finance. CryptoSwap / Curve v2 Whitepaper. https://curve.fi/files/ crypto-pools-paper.pdf, 2026. Accessed 2026-01-09

2026

-

[15]

Stableswap-NG Pools: Dynamic Fee Formula

Curve Finance. Stableswap-NG Pools: Dynamic Fee Formula. https://docs.curve.finance/ stableswap-exchange/stableswap-ng/pools/overview/, 2026. Accessed 2026-01-09

2026

-

[16]

Daian, S

P. Daian, S. Goldfeder, T. Kell, Y. Li, X. Zhao, I. Bentov, L. Breidenbach, and A. Juels. Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. In2020 IEEE Symposium on Security and Privacy (SP), pages 910–927, 2020

2020

-

[17]

D. M. Di Nosse, F. Gatta, F. Lillo, and S. Jaimungal. Deviations from Tradition: Stylized Facts in the Era of DeFi.Quantitative Finance, 2026

2026

-

[18]

Z. Fan, F. Marmolejo-Coss´ ıo, D. J. Moroz, M. Neuder, R. Rao, and D. C. Parkes. Strategic liquidity provision in uniswap v3. In5th Conference on Advances in Financial Technologies (AFT 2023), 2023

2023

-

[19]

Fritsch and A

R. Fritsch and A. Canidio. Measuring arbitrage losses and profitability of amm liquidity. In Companion Proceedings of the ACM Web Conference 2024, pages 1761–1767, 2024

2024

-

[20]

K. Gao, P. Vytelingum, S. Weston, W. Luk, and C. Guo. High-frequency financial market simulation and flash crash scenarios analysis: An agent-based modelling approach.Journal of Artificial Societies and Social Simulation, 27(2):8, 2024

2024

-

[21]

Gu´ eant.The Financial Mathematics of Market Liquidity: From Optimal Execution to Market Making

O. Gu´ eant.The Financial Mathematics of Market Liquidity: From Optimal Execution to Market Making. CRC Press, Boca Raton, FL, 2016

2016

-

[22]

M. Hafner and H. Dietl. Impermanent loss conditions: An analysis of decentralized exchange platforms.arXiv preprint arXiv:2401.07689, 2024

-

[23]

Heimbach, E

L. Heimbach, E. Schertenleib, and R. Wattenhofer. Risks and returns of uniswap v3 liquidity providers. InProceedings of the 4th ACM Conference on Advances in Financial Technologies (AFT ’22), 2022

2022

-

[24]

S. L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options.The Review of Financial Studies, 6(2):327–343, 1993

1993

-

[25]

Ho and H

T. Ho and H. R. Stoll. The dynamics of dealer markets under competition.The Journal of Finance, 38(4):1053–1074, 1983

1983

-

[26]

S. J. Leal, M. Napoletano, A. Roventini, and G. Fagiolo. Rock around the clock: An agent-based model of low- and high-frequency trading.Journal of Evolutionary Economics, 26(1):49–76, 2016

2016

-

[27]

Developer Docs: Liquidity Book Fees

LFJ (Trader Joe). Developer Docs: Liquidity Book Fees. https://developers.lfj.gg/ concepts/fees, 2026. Accessed 2026-01-09

2026

-

[28]

Maire and M

B. Maire and M. Wunsch. Market neutral liquidity provision.Ledger, 9:115–134, 2024. 36

2024

-

[29]

Maitrier, G

G. Maitrier, G. Loeper, K. Kanazawa, and J.-P. Bouchaud. The ‘double’ square-root law: evi- dence for the mechanical origin of market impact using tokyo stock exchange data.Quantitative Finance, 26(4):491–503, 2026

2026

-

[30]

Mannaro, M

K. Mannaro, M. Marchesi, and A. Setzu. Using an artificial financial market for assessing the impact of tobin-like transaction taxes.Journal of Economic Behavior & Organization, 67(2):445–462, 2008

2008

-

[31]

DLMM Formulas: Fee Calculation Formulas

Meteora. DLMM Formulas: Fee Calculation Formulas. https://docs.meteora.ag/overview/ products/dlmm/dlmm-formulas, 2026. Accessed 2026-01-09

2026

-

[32]

J. Milionis, C. C. Moallemi, T. Roughgarden, and A. L. Zhang. Automated market making and loss-versus-rebalancing.arXiv preprint arXiv:2208.06046, 2023

-

[33]

T. Mizuta. An agent-based model for designing a financial market that works well. In2020 IEEE Symposium Series on Computational Intelligence (SSCI), pages 400–406, 2020

2020

-

[34]

Pellizzari and F

P. Pellizzari and F. Westerhoff. Some effects of transaction taxes under different microstructures. Journal of Economic Behavior & Organization, 72(3):850–863, 2009

2009

-

[35]

Raberto, S

M. Raberto, S. Cincotti, S. M. Focardi, and M. Marchesi. Agent-based simulation of a financial market.Physica A: Statistical Mechanics and its Applications, 299(1–2):319–327, 2001

2001

-

[36]

T´ oth, Y

B. T´ oth, Y. Lemp´ eri` ere, C. Deremble, J. de Lataillade, J. Kockelkoren, and J.-P. Bouchaud. Anomalous price impact and the critical nature of liquidity in financial markets.Phys. Rev. X, 1:021006, Oct 2011

2011

-

[37]

Wan and A

X. Wan and A. Adams. Just-in-time liquidity on the uniswap protocol.Available at SSRN 4382303, 2022

2022

-

[38]

Westerhoff and R

F. Westerhoff and R. Dieci. The effectiveness of keynes–tobin transaction taxes when het- erogeneous agents can trade in different markets: A behavioral finance approach.Journal of Economic Dynamics and Control, 30(2):293–322, 2006

2006

-

[39]

I. Yagi, Y. Masuda, and T. Mizuta. Analysis of the impact of high-frequency trading on artificial market liquidity.IEEE Transactions on Computational Social Systems, 7(6):1324–1334, 2020

2020

- [40]

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.