Bounds for Standard Errors in Combined Data

Pith reviewed 2026-06-25 21:14 UTC · model grok-4.3

The pith

Lower bounds on standard errors for parameters from moment conditions across samples can be derived without any information on cross-sample correlations.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

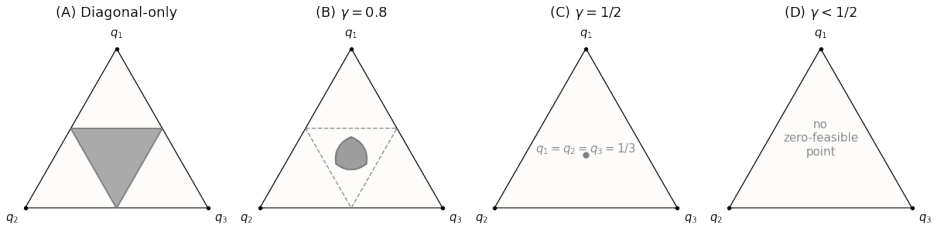

We propose methods for constructing lower bounds on the standard errors of parameters estimated from moment conditions obtained across different samples. Sharp explicit bounds are derived by exploiting geometric inequalities when no information about correlations across samples is available. Furthermore, we develop computationally tractable sharp bounds for more general settings with no or partial correlation information, which can be obtained by solving a simple semidefinite program.

What carries the argument

Geometric inequalities that characterize the feasible set of standard errors when cross-sample correlations are unknown, together with a semidefinite program that computes the same set under partial correlation information.

If this is right

- The explicit geometric bounds apply directly to menu-cost and Heterogeneous Agent New-Keynesian models estimated from multiple data sources.

- The semidefinite-program bounds apply to two-sample instrumental-variable estimators when only partial correlation information is available.

- The methods supply conservative standard-error statements for any estimator whose asymptotic variance depends on an unknown cross-sample covariance matrix.

- Implementation requires only the individual-sample moment variances and the ability to solve a small semidefinite program.

Where Pith is reading between the lines

- The same bounding technique could be applied to meta-analyses that combine published estimates whose underlying micro-data are unavailable.

- Extending the geometry to nonlinear moment conditions or to finite-sample corrections would be a direct next step.

- If the bounds prove tight in practice, they could replace ad-hoc robustness checks that assume zero or perfect correlation across samples.

Load-bearing premise

The geometric inequalities and semidefinite program formulations correctly characterize the feasible set of standard errors under the stated information constraints on cross-sample correlations.

What would settle it

Compute the actual standard error in a simulation or empirical example where the full correlation matrix across samples is known; if that value lies below the paper's reported lower bound, the characterization is incorrect.

Figures

read the original abstract

We propose methods for constructing lower bounds on the standard errors of parameters estimated from moment conditions obtained across different samples. Sharp explicit bounds are derived by exploiting geometric inequalities when no information about correlations across samples is available. Furthermore, we develop computationally tractable sharp bounds for more general settings with no or partial correlation information, which can be obtained by solving a simple semidefinite program. Finally, we illustrate the practical usefulness of our method through three empirical cases: two macroeconomics examples involving menu cost and Heterogeneous Agent New-Keynesian models; and a two sample instrumental variable microeconomic study.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes methods for constructing lower bounds on the standard errors of parameters estimated from moment conditions obtained across different samples. Sharp explicit bounds are derived by exploiting geometric inequalities when no information about correlations across samples is available. Furthermore, it develops computationally tractable sharp bounds for more general settings with no or partial correlation information, which can be obtained by solving a simple semidefinite program. The approach is illustrated through three empirical cases: two macroeconomics examples involving menu cost and Heterogeneous Agent New-Keynesian models, and a two-sample instrumental variable microeconomic study.

Significance. If the geometric inequalities and SDP characterizations are correct and sharp, the results provide a useful tool for obtaining conservative standard errors in combined-data settings common in empirical economics, where cross-sample correlations are typically unknown. The explicit bounds for the no-information case and the tractable SDP formulation represent a practical advance over ad-hoc adjustments, with potential for adoption in robustness checks for macro and micro applications.

major comments (2)

- [§4.1, Eq. (12)] §4.1, Eq. (12): the claimed sharpness of the geometric bound relies on the feasible set being exactly the interval between the extremal correlations compatible with the marginal variances; however, the derivation does not explicitly verify that the resulting quadratic form attains the bound under the positive-semidefinite constraint on the full covariance matrix.

- [§5.2, SDP formulation (15)–(17)] §5.2, SDP formulation (15)–(17): the relaxation to a simple SDP is presented as delivering sharp bounds, but the manuscript does not include a proof that the dual or the KKT conditions confirm attainment at the boundary for the partial-correlation case; without this, it is unclear whether the numerical solution is always tight.

minor comments (3)

- The notation for the combined moment vector and the block covariance matrix is introduced without a clear summary table; adding one would improve readability when moving between the no-information and partial-information cases.

- In the menu-cost application, the reported bounds are compared to conventional SEs but the exact sample sizes and moment conditions used in each subsample are not tabulated, making it hard to replicate the numerical values.

- The abstract states that the SDP is 'simple,' yet the implementation details (solver, tolerance, and how the correlation constraints are encoded) appear only in an appendix; moving a short pseudocode block to the main text would help.

Simulated Author's Rebuttal

We thank the referee for the careful reading, positive assessment, and recommendation of minor revision. We address each major comment below and will add the requested explicit verifications to strengthen the manuscript.

read point-by-point responses

-

Referee: [§4.1, Eq. (12)] §4.1, Eq. (12): the claimed sharpness of the geometric bound relies on the feasible set being exactly the interval between the extremal correlations compatible with the marginal variances; however, the derivation does not explicitly verify that the resulting quadratic form attains the bound under the positive-semidefinite constraint on the full covariance matrix.

Authors: We appreciate this observation. The extremal correlations ρ_min and ρ_max are defined exactly as the boundary values that keep the relevant 2×2 covariance block positive semidefinite given the marginal variances. The quadratic form for the combined estimator’s asymptotic variance is continuous in ρ, so its minimum and maximum over the compact interval [ρ_min, ρ_max] are attained at an endpoint. In the revision we will insert a short paragraph in §4.1 that explicitly confirms the full (joint) covariance matrix remains PSD at these endpoints by construction of the feasible correlation range. revision: yes

-

Referee: [§5.2, SDP formulation (15)–(17)] §5.2, SDP formulation (15)–(17): the relaxation to a simple SDP is presented as delivering sharp bounds, but the manuscript does not include a proof that the dual or the KKT conditions confirm attainment at the boundary for the partial-correlation case; without this, it is unclear whether the numerical solution is always tight.

Authors: We agree that an explicit tightness argument would improve clarity. The SDP (15)–(17) minimizes a linear objective over a compact convex spectrahedron. Standard SDP theory guarantees attainment; to verify that the optimum occurs at a boundary point corresponding to the claimed sharp bound, we will add a brief paragraph in §5.2 that invokes the KKT conditions (or the dual SDP) to show complementarity implies the correlation parameters lie at the boundary of the feasible set. This verification will be included in the revision. revision: yes

Circularity Check

No significant circularity; derivation relies on external geometric inequalities and SDP

full rationale

The paper derives sharp bounds on standard errors from moment conditions across samples by applying geometric inequalities for the no-correlation-information case and formulating a semidefinite program for partial information. These steps use standard external mathematical tools (geometric inequalities on covariance matrices and SDP optimization over feasible correlation sets) that do not reduce to the paper's own fitted quantities or self-referential definitions. No load-bearing self-citations, ansatzes smuggled via prior work, or renaming of known results appear in the derivation chain. The central claim remains independent of its inputs and is self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Geometric inequalities can be applied to characterize the feasible region of standard errors given moment conditions across samples

- domain assumption Semidefinite programming yields computationally tractable sharp bounds under partial correlation information

Reference graph

Works this paper leans on

-

[1]

Available at SSRN 5738770 , year=

Inference for the Marginal Value of Public Funds , author=. Available at SSRN 5738770 , year=

-

[2]

Econometrica , volume=

Identifying treatment effects under data combination , author=. Econometrica , volume=. 2014 , publisher=

2014

-

[3]

Review of Economic Studies , volume=

Partially linear models under data combination , author=. Review of Economic Studies , volume=. 2025 , publisher=

2025

-

[4]

Econometric Theory , volume=

Sharp bounds on the distribution of treatment effects and their statistical inference , author=. Econometric Theory , volume=. 2010 , publisher=

2010

-

[5]

Journal of economic perspectives , volume=

Assessing the case for social experiments , author=. Journal of economic perspectives , volume=. 1995 , publisher=

1995

-

[6]

Frank, M. J. and Nelsen, R. B. and Schweizer, B. , date =. Best-possible bounds for the distribution of a sum - a problem of Kolmogorov , url =. Probability Theory and Related Fields , number =. 1987 , bdsk-url-1 =. doi:10.1007/BF00569989 , id =

-

[7]

Review of Economic Studies , volume=

Standard errors for calibrated parameters , author=. Review of Economic Studies , volume=. 2025 , publisher=

2025

-

[8]

The Review of Economic Studies , pages =

Cocci, Matthew D and Plagborg-Møller, Mikkel , title =. The Review of Economic Studies , pages =. 2024 , month =. doi:10.1093/restud/rdae099 , url =

-

[9]

arXiv: 2109.08109v1 , primaryClass=

Standard Errors for Calibrated Parameters , author=. arXiv: 2109.08109v1 , primaryClass=. 2024 , eprint=

arXiv 2024

-

[10]

Annual Review of Economics , volume=

Partial identification in econometrics , author=. Annual Review of Economics , volume=. 2010 , publisher=

2010

-

[11]

and Sklar, A

Schweizer, B. and Sklar, A. , isbn =. Probabilistic metric spaces / B. Schweizer and A. Sklar. , year =

-

[12]

Theory of Probability & its Applications , volume=

Estimates for the distribution function of a sum of two random variables when the marginal distributions are fixed , author=. Theory of Probability & its Applications , volume=. 1982 , publisher=

1982

-

[13]

Williamson and Tom Downs , doi =

Robert C. Williamson and Tom Downs , doi =. Probabilistic arithmetic. I. Numerical methods for calculating convolutions and dependency bounds , url =. International Journal of Approximate Reasoning , keywords =. 1990 , bdsk-url-1 =

1990

-

[14]

The Review of Economic Studies , volume =

Hahn, Jinyong and Kuersteiner, Guido and Mazzocco, Maurizio , title = ". The Review of Economic Studies , volume =. 2019 , month =. doi:10.1093/restud/rdz016 , url =

-

[15]

doi:10.1017/s0266466622000391 , year = 2022, month =

Hahn, Jinyong and Kuersteiner, Guido and Mazzocco, Maurizio , title =. doi:10.1017/s0266466622000391 , year = 2022, month =

-

[16]

forthcoming Econometric Theory , year =

Hahn, Jinyong and Kuersteiner, Guido and Mazzocco, Maurizio , title =. forthcoming Econometric Theory , year =. doi:10.48550/ARXIV.1903.04655 , url =

-

[17]

Econometric Theory , volume=

Joint time-series and cross-section limit theory under mixingale assumptions , author=. Econometric Theory , volume=. 2022 , publisher=

2022

-

[18]

Econometric Theory , pages=

Central Limit Theory for Combined Cross Section and Time Series with an Application to Aggregate Productivity Shocks , author=. Econometric Theory , pages=. 2022 , publisher=

2022

-

[19]

Central Limit Theory for Combined Cross-Section and Time Series , publisher =. arXiv:1610.01697 , year =. doi:10.48550/ARXIV.1610.01697 , author =

-

[20]

The Review of Economic Studies , volume=

Estimation with aggregate shocks , author=. The Review of Economic Studies , volume=. 2020 , publisher=

2020

-

[21]

The Econometrics of Data Combination , url =

Geert Ridder and Robert Moffitt , doi =. The Econometrics of Data Combination , url =. 2007 , bdsk-url-1 =

2007

-

[22]

Liechty, John C. and Liechty, Merrill W. and Müller, Peter , title = ". Biometrika , volume =. 2004 , month =. doi:10.1093/biomet/91.1.1 , url =

-

[23]

Statistical Science , keywords =

Mohsen Pourahmadi , doi =. Statistical Science , keywords =. 2011 , bdsk-url-1 =

2011

-

[24]

Journal of Business & Economic Statistics , Year =

Omar Aguilar and Mike West , doi =. Bayesian Dynamic Factor Models and Portfolio Allocation , url =. 2000 , bdsk-url-1 =. https://www.tandfonline.com/doi/pdf/10.1080/07350015.2000.10524875 , journal =

-

[25]

Kuersteiner, Guido M. and Prucha, Ingmar R. , title=. Journal of Econometrics , year=2013, volume=. doi:10.1016/j.jeconom.2013.02 , url=

-

[26]

Peter C. B. Phillips and Hyungsik R. Moon , journal =. Linear Regression Limit Theory for Nonstationary Panel Data , urldate =

-

[27]

Piatek, R. Maintaining (Locus of) Control? Data Combination for the Identification and Inference of Factor Structure Models , url =. Journal of Applied Econometrics , number =. 2016 , bdsk-url-1 =. doi:https://doi.org/10.1002/jae.2456 , eprint =

-

[28]

Long-term Causal Inference Under Persistent Confounding via Data Combination , publisher =

Imbens, Guido and Kallus, Nathan and Mao, Xiaojie and Wang, Yuhao , keywords =. Long-term Causal Inference Under Persistent Confounding via Data Combination , publisher =. 2022 , copyright =. doi:10.48550/ARXIV.2202.07234 , url =

-

[29]

The Review of Economic Studies , volume=

Combining micro and macro data in microeconometric models , author=. The Review of Economic Studies , volume=. 1994 , publisher=

1994

-

[30]

Journal of political Economy , volume=

Differentiated products demand systems from a combination of micro and macro data: The new car market , author=. Journal of political Economy , volume=. 2004 , publisher=

2004

-

[31]

Journal of political Economy , volume=

Quantifying the benefits of new products: The case of the minivan , author=. Journal of political Economy , volume=. 2002 , publisher=

2002

-

[32]

American Economic Review , volume=

Monetary policy according to HANK , author=. American Economic Review , volume=. 2018 , publisher=

2018

-

[33]

Journal of political economy , volume=

The macroeconomic implications of rising wage inequality in the United States , author=. Journal of political economy , volume=. 2010 , publisher=

2010

-

[34]

Econometric Theory , volume=

Central Limit Theory for Combined Cross Section and Time Series With an Application to Aggregate Productivity Shocks , author=. Econometric Theory , volume=. 2024 , publisher=

2024

-

[35]

Journal of economic perspectives , volume=

The empirical foundations of calibration , author=. Journal of economic perspectives , volume=. 1996 , publisher=

1996

-

[36]

The Review of Economics and Statistics , volume=

Two-sample instrumental variables estimators , author=. The Review of Economics and Statistics , volume=. 2010 , publisher=

2010

-

[37]

Journal of public economics , volume=

Are public housing projects good for kids? , author=. Journal of public economics , volume=. 2000 , publisher=

2000

-

[38]

Journal of the American statistical Association , volume=

The effect of age at school entry on educational attainment: an application of instrumental variables with moments from two samples , author=. Journal of the American statistical Association , volume=. 1992 , publisher=

1992

-

[39]

2004 , publisher =

Convex Optimization , author =. 2004 , publisher =

2004

-

[40]

Econometrica , volume =

Price Setting with Menu Cost for Multiproduct Firms , author =. Econometrica , volume =

-

[41]

American Economic Review , volume =

The Real Effects of Monetary Shocks in Sticky Price Models: A Sufficient Statistic Approach , author =. American Economic Review , volume =

-

[42]

Econometrica , volume =

Using the Sequence-Space Jacobian to Solve and Estimate Heterogeneous-Agent Models , author =. Econometrica , volume =

-

[43]

American Economic Review , volume =

The Power of Forward Guidance Revisited , author =. American Economic Review , volume =

-

[44]

National Bureau of Economic Research Working Paper Series , year =

Heterogeneity and Aggregate Fluctuations , author =. National Bureau of Economic Research Working Paper Series , year =

-

[45]

American Economic Journal: Macroeconomics , volume =

The Transmission of Monetary Policy Shocks , author =. American Economic Journal: Macroeconomics , volume =

-

[46]

Journal of Applied Econometrics , volume=

Weak-instrument robust inference for two-sample instrumental variables regression , author=. Journal of Applied Econometrics , volume=. 2018 , publisher=

2018

-

[47]

Renkin, Tobias and Z. Credit. American Economic Journal: Macroeconomics , keywords =. 2024 , bdsk-url-1 =. doi:10.1257/mac.20220079 , issn =

-

[48]

Are public housing projects good for kids? , url =

Currie, Janet and Yelowitz, Aaron , date-added =. Are public housing projects good for kids? , url =. Journal of Public Economics , keywords =. 2000 , bdsk-url-1 =. doi:10.1016/S0047-2727(99)00065-1 , file =

-

[49]

Inoue, Atsushi and Solon, Gary , date-added =. Two-. The Review of Economics and Statistics , month = aug, number =. 2010 , bdsk-url-1 =. doi:10.1162/REST_a_00011 , file =

-

[50]

Barone, Guglielmo and Mocetti, Sauro , date-added =. Intergenerational. The Review of economic studies , language =. 2021 , bdsk-url-1 =. doi:10.1093/restud/rdaa075 , file =

-

[51]

Olivetti, Claudia and Paserman, M. Daniele , date-added =. In the. American Economic Review , keywords =. 2015 , bdsk-url-1 =. doi:10.1257/aer.20130821 , file =

-

[52]

and Levell, Peter and Low, Hamish , date-added =

Crossley, Thomas F. and Levell, Peter and Low, Hamish , date-added =. House price rises and borrowing to invest , url =. Journal of Economic Behavior & Organization , keywords =. 2024 , bdsk-url-1 =. doi:10.1016/j.jebo.2024.05.002 , file =

-

[53]

Early-life famine exposure, hunger recall, and later-life health , url =

Deng, Zichen and Lindeboom, Maarten , copyright =. Early-life famine exposure, hunger recall, and later-life health , url =. Journal of Applied Econometrics , keywords =. 2022 , bdsk-url-1 =. doi:10.1002/jae.2897 , file =

-

[54]

Klevmarken, Anders , copyright =. Missing. 1982 , bdsk-url-1 =

1982

-

[55]

On the moduli space of polygons in the Euclidean plane , volume =

Kapovich, Michael and Millson, John , journal =. On the moduli space of polygons in the Euclidean plane , volume =

-

[56]

Econometrica , volume=

Tests of conditional predictive ability , author=. Econometrica , volume=. 2006 , publisher=

2006

-

[57]

Journal of Econometrics , volume=

Bootstrapping factor-augmented regression models , author=. Journal of Econometrics , volume=. 2014 , publisher=

2014

-

[58]

International economic review , pages=

Econometric issues in the analysis of regressions with generated regressors , author=. International economic review , pages=. 1984 , publisher=

1984

-

[59]

Journal of Monetary Economics , volume=

Innocent Bystanders? Monetary policy and inequality , author=. Journal of Monetary Economics , volume=. 2017 , publisher=

2017

-

[60]

American economic review , volume=

A new measure of monetary shocks: Derivation and implications , author=. American economic review , volume=. 2004 , publisher=

2004

-

[61]

American Economic Journal: Macroeconomics , volume=

Monetary policy surprises, credit costs, and economic activity , author=. American Economic Journal: Macroeconomics , volume=. 2015 , publisher=

2015

-

[62]

Econometrica , volume =

Time To Build and Aggregate Fluctuations , author =. Econometrica , volume =

-

[63]

Econometrica , volume =

Consumption Over the Life Cycle , author =. Econometrica , volume =

-

[64]

Econometrica , volume =

A Model of Consumption Response to Fiscal Stimulus Payments , author =. Econometrica , volume =

-

[65]

American Economic Review , volume =

Default Risk and Income Fluctuations in Emerging Economies , author =. American Economic Review , volume =

-

[66]

Econometrica , volume =

An Anatomy of International Trade: Evidence From French Firms , author =. Econometrica , volume =

-

[67]

Journal of Economic Perspectives , volume =

Identification in Macroeconomics , author =. Journal of Economic Perspectives , volume =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.