Generalized Rank Regression

Pith reviewed 2026-05-25 03:51 UTC · model grok-4.3

The pith

The generalized rank regression estimator admits a non-asymptotic Bahadur representation, is asymptotically normal under mild conditions, and shares asymptotically equivalent variances with composite quantile regression.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Generalized rank regression (GRR) extends rank-based methods to non-monotonic score functions. The GRR estimator admits a non-asymptotic Bahadur representation, is asymptotically normal under mild conditions, and shares asymptotically equivalent variances with composite quantile regression. A two-stage sub-gradient descent algorithm computes the estimator, and a multiplier bootstrap procedure supports inference.

What carries the argument

The GRR estimator defined via a possibly non-monotonic score function inside a rank-based objective, together with its non-asymptotic Bahadur representation that yields the asymptotic normality result.

If this is right

- GRR estimators remain computable via the two-stage sub-gradient descent procedure even though the objective is non-convex and non-smooth.

- Multiplier bootstrap yields valid inference for the GRR estimator.

- GRR achieves the same asymptotic efficiency as composite quantile regression while preserving rank-regression robustness properties.

- The method applies to data with heavy-tailed or non-Gaussian errors where classical least-squares methods lose efficiency.

Where Pith is reading between the lines

- The variance equivalence may allow practitioners to choose between GRR and composite quantile regression based on computational convenience or finite-sample behavior rather than asymptotic efficiency.

- Extensions to high-dimensional or dependent-data settings could follow the same Bahadur-representation strategy if the score-function conditions are preserved.

- The non-monotonic score functions open the possibility of tailoring the estimator to specific error distributions without losing the rank-invariance property.

Load-bearing premise

The mild conditions required for asymptotic normality hold in practice and the two-stage sub-gradient descent algorithm converges to a statistically desirable solution.

What would settle it

A large-scale simulation in which the finite-sample distribution of the GRR estimator deviates from normality or its empirical variance fails to match that of composite quantile regression at the rate predicted by the Bahadur representation.

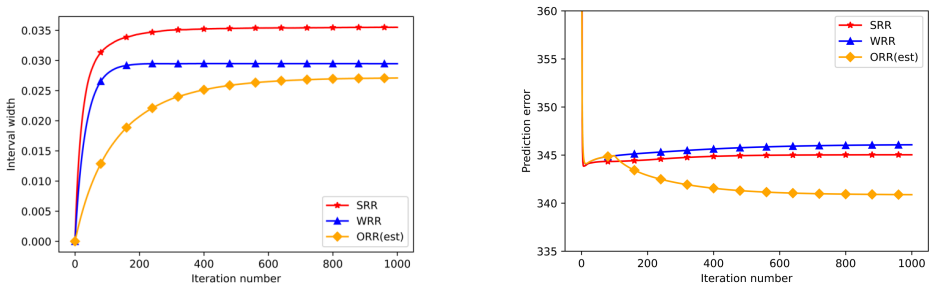

Figures

read the original abstract

Rank regression offers robustness to outliers and heavy-tailed response distributions, invariance to monotonic transformations, and improved efficiency under non-Gaussian errors, making it a versatile tool for analyzing complex data. This paper introduces Generalized Rank Regression (GRR), an extension of classical rank-based methods that accommodates non-monotonic score functions. While aimed at enhancing the statistical efficiency of robust estimators, this generalization results in a potentially non-convex and non-smooth objective function, presenting challenges for both theoretical analysis and algorithmic implementation. We derive a non-asymptotic Bahadur representation of the proposed estimator and establish its asymptotic normality under mild conditions. To address the optimization challenges, we propose a new two-stage sub-gradient descent algorithm that enables efficient computation of GRR estimators with desirable statistical properties. Furthermore, we develop a multiplier bootstrap procedure for conducting statistical inference. A close connection between GRR and variants of quantile regression is uncovered, which demonstrates that GRR and composite quantile regression share asymptotically equivalent variances. The advantages of GRR are illustrated through extensive simulation studies and a real data application.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript introduces Generalized Rank Regression (GRR) as an extension of classical rank regression that accommodates non-monotonic score functions. It claims to derive a non-asymptotic Bahadur representation for the GRR estimator, establish its asymptotic normality under mild conditions, propose a two-stage sub-gradient descent algorithm for computation despite the potentially non-convex non-smooth objective, develop a multiplier bootstrap for inference, and demonstrate that GRR shares asymptotically equivalent variances with composite quantile regression. These theoretical results are illustrated with simulation studies and a real-data application.

Significance. If the central claims hold for the estimator returned by the proposed algorithm, GRR would provide a flexible robust regression method with invariance properties, potential efficiency gains, and direct links to quantile regression methods, supported by practical computation and inference tools.

major comments (2)

- [Theoretical development and algorithm description] The non-asymptotic Bahadur representation and asymptotic normality are stated to hold for the GRR estimator under mild conditions, yet the manuscript provides no argument that the output of the two-stage sub-gradient descent algorithm satisfies the first-order conditions or uniform convergence rates required for these expansions when the objective is non-convex and non-smooth (as occurs for non-monotonic scores). This is load-bearing for all subsequent claims about the computed estimator.

- [Connection to quantile regression] The claimed asymptotic variance equivalence with composite quantile regression is derived from the population estimating equation; it is unclear whether this equivalence continues to hold for the estimator actually returned by the algorithm, as opposed to an arbitrary critical point.

minor comments (2)

- The abstract refers to 'mild conditions' for asymptotic normality without listing them; these should be stated explicitly in the main text near the theorem statements.

- Notation for the score function and its monotonicity properties should be introduced consistently before the objective function is defined.

Simulated Author's Rebuttal

We thank the referee for their careful reading and constructive comments. Below we respond point-by-point to the major comments.

read point-by-point responses

-

Referee: [Theoretical development and algorithm description] The non-asymptotic Bahadur representation and asymptotic normality are stated to hold for the GRR estimator under mild conditions, yet the manuscript provides no argument that the output of the two-stage sub-gradient descent algorithm satisfies the first-order conditions or uniform convergence rates required for these expansions when the objective is non-convex and non-smooth (as occurs for non-monotonic scores). This is load-bearing for all subsequent claims about the computed estimator.

Authors: We agree this link requires explicit clarification. The Bahadur representation and asymptotic normality are derived for any estimator satisfying the first-order condition 0 belonging to the subdifferential of the sample objective. The two-stage algorithm is constructed so that its output satisfies this stationarity condition to within numerical tolerance (first stage supplies a robust initialization; second stage performs subgradient steps until the norm of a subgradient element falls below a threshold). In the revision we will add a dedicated paragraph in Section 3.2 stating that all theoretical results apply to any stationary point returned by the algorithm and will report additional diagnostics confirming that the computed solutions meet the required first-order condition in both simulations and the real-data example. revision: yes

-

Referee: [Connection to quantile regression] The claimed asymptotic variance equivalence with composite quantile regression is derived from the population estimating equation; it is unclear whether this equivalence continues to hold for the estimator actually returned by the algorithm, as opposed to an arbitrary critical point.

Authors: The asymptotic variance equivalence follows directly from the fact that GRR and composite quantile regression share the identical population estimating equation; any consistent sequence of solutions to the corresponding sample estimating equation therefore possesses the same influence function and the same asymptotic variance. Because every critical point of the sample objective satisfies the sample estimating equation (subgradient contains zero), the equivalence holds for any stationary point the algorithm returns. We will insert a short clarifying sentence after the variance-equivalence statement to make this explicit. revision: partial

Circularity Check

No circularity: independent theoretical derivations and algorithmic proposal

full rationale

The paper defines the GRR estimator from a generalized rank objective (potentially non-convex), then separately derives a non-asymptotic Bahadur representation and asymptotic normality under mild conditions, proposes a two-stage sub-gradient algorithm, and shows variance equivalence to composite quantile regression. No quoted equations or steps reduce any claimed result to a fitted parameter, self-definition, or self-citation chain by construction. The connection to quantile regression is presented as an uncovered equivalence rather than a renaming or tautology. The derivation chain remains self-contained against external benchmarks for M-estimator theory.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Optimal convex M -estimation via score matching , author=. 2026 , journal=

work page 2026

-

[2]

Estimation of a probability density function and its derivatives , author=. Ann. Math. Stat. , volume=. 1969 , publisher=

work page 1969

-

[3]

Robust Statistics: The Approach Based on the Influence Function , author=. 1986 , publisher=

work page 1986

-

[4]

V. P. Godambe , title =. Ann. Math. Stat. , number =

-

[5]

A geometric interpretation of inferences based on ranks in the linear model , author=. J. Amer. Statist. Assoc. , volume=. 1983 , publisher=

work page 1983

-

[6]

Contributions to probability and statistics , pages=

A survey of sampling from contaminated distributions , author=. Contributions to probability and statistics , pages=. 1960 , publisher=

work page 1960

-

[7]

Wainwright, Martin J , Journal =. Sharp thresholds for high-dimensional and noisy sparsity recovery using _1 -constrained quadratic programming (

-

[8]

Statistical Learning with Sparsity: the Lasso and Generalizations , Year =

Hastie, Trevor and Tibshirani, Robert and Wainwright, Martin , Publisher =. Statistical Learning with Sparsity: the Lasso and Generalizations , Year =

-

[9]

Chang, Xiangyu and Lin, Shao-Bo and Zhou, Ding-Xuan , title =. J. Mach. Learn. Res. , pages =. 2017 , issue_date =

work page 2017

-

[10]

D. A. S. Fraser , title =. 1956 , publisher =

work page 1956

-

[11]

B. M. Nguelifack and I. Kemajou-Brown , title =. J. Stat. Comput. Simul. , year =

-

[12]

van der Vaart, A. W. , year=. Asymptotic Statistics , publisher=

-

[13]

Wan and Shuyi Zhang and Yong Zhou , title =

Lanjue Chen and Alan T.K. Wan and Shuyi Zhang and Yong Zhou , title =. J. Mach. Learn. Res. , year =

- [14]

-

[15]

Strang, Gilbert , title =

-

[16]

Nonparametric estimate of regression coefficients , volume =

Jana Jureckova , journal =. Nonparametric estimate of regression coefficients , volume =

-

[17]

Asymptotic linearity of a rank statistic in regression parameter , volume =

Jana Jureckova , journal =. Asymptotic linearity of a rank statistic in regression parameter , volume =

-

[18]

Rank estimates and asymptotic linearity in regression parameters , booktitle =. 1999 , series =

work page 1999

-

[19]

On the method of bounded differences , booktitle=

McDiarmid, Colin , editor=. On the method of bounded differences , booktitle=. 1989 , pages=

work page 1989

-

[20]

Introduction to Nonparametric Estimation , author=. 2008 , publisher=

work page 2008

-

[21]

Tyurin, I. S. , title =. Theory Probab. Appl. , volume =

-

[22]

F. Gotze , Journal =. On the rate of convergence in the multivariate CLT , Volume =

-

[23]

Probability inequalities for the sum of independent random variables , volume =

George Bennett , journal =. Probability inequalities for the sum of independent random variables , volume =

-

[24]

City University of Hong Kong , pages=

McDiarmid’s inequalities of Bernstein and Bennett forms , author=. City University of Hong Kong , pages=

-

[25]

Lan Wang and Bo Peng and Jelena Bradic and Runze Li and Yunan Wu , title =. J. Amer. Statist. Assoc. , volume =. 2020 , publisher =

work page 2020

- [26]

-

[27]

Louis A. Jaeckel , journal =. Estimating regression coefficients by minimizing the dispersion of the residuals , volume =

-

[28]

Conformalized quantile regression , volume =

Romano, Yaniv and Patterson, Evan and Candes, Emmanuel , booktitle =. Conformalized quantile regression , volume =

-

[29]

Proceedings of the AAAI Conference on Artificial Intelligence , author=

Distributional reinforcement learning with quantile regression , volume=. Proceedings of the AAAI Conference on Artificial Intelligence , author=

-

[30]

Xuejun Jiang and Jiancheng Jiang and Xinyuan Song , journal =. Oracle model selection for nonlinear models based on weighted composite quantile regression , volume =

-

[31]

Prentice, R. L. , title = ". Biometrika , volume =

-

[32]

Linear rank statistics in regression analysis with censored or truncated data , journal =. 1992 , author =

work page 1992

-

[33]

On early stopping in gradient descent learning , author=. Constr. Approx. , volume=

-

[34]

Daniel Soudry and Elad Hoffer and Mor Shpigel Nacson and Suriya Gunasekar and Nathan Srebro , title =. J. Mach. Learn. Res. , year =

-

[35]

International Conference on Learning Representations , year=

Implicit gradient regularization , author=. International Conference on Learning Representations , year=

-

[36]

Xuming He and Xiaoou Pan and Kean Ming Tan and Wen-Xin Zhou , title =. Ann. Statist. , number =

-

[37]

Guillaume Carlier and Victor Chernozhukov and Alfred Galichon , title =. Ann. Statist. , number =

- [38]

-

[39]

Rank-based max-sum tests for mutual independence of high-dimensional random vectors , journal =. 2024 , author =

work page 2024

-

[40]

Distributed testing and estimation under sparse high dimensional models

Battey, Heather and Fan, Jianqing and Liu, Han and Lu, Junwei and Zhu, Ziwei. Distributed testing and estimation under sparse high dimensional models. Ann. Statist. 2018

work page 2018

-

[41]

Variable selection and coefficient estimation via regularized rank regression , volume =

Chenlei Leng , journal =. Variable selection and coefficient estimation via regularized rank regression , volume =

-

[42]

A Bernstein-type inequality for U-statistics and U-processes , journal =. 1995 , author =

work page 1995

-

[43]

Hui Zou and Ming Yuan , title =. Ann. Statist. , number =

-

[44]

Proceedings of the 34th International Conference on Machine Learning , pages =

Efficient Distributed Learning with Sparsity , author =. Proceedings of the 34th International Conference on Machine Learning , pages =. 2017 , editor =

work page 2017

-

[45]

Moving Beyond Sub-Gaussianity in High-Dimensional Statistics: Applications in Covariance Estimation and Linear Regression. arXiv e-prints , keywords =

-

[46]

Conference on Learning Theory , pages=

Reconstruction from anisotropic random measurements , author=. Conference on Learning Theory , pages=. 2012 , organization=

work page 2012

-

[47]

A unified framework for high-dimensional analysis of M -estimators with decomposable regularizers , author=. Statist. Sci. , volume=. 2012 , publisher=

work page 2012

-

[48]

Wang, Hansheng and Li, Runze and Tsai, Chih-Ling , title = ". Biometrika , volume =

-

[49]

and Liu, Qiang and Sun, Yuekai and Taylor, Jonathan E

Lee, Jason D. and Liu, Qiang and Sun, Yuekai and Taylor, Jonathan E. , title =. J. Mach. Learn. Res. , month = jan, pages =. 2017 , issue_date =

work page 2017

-

[50]

Tony Cai, T. and Guo, Zijian , title =. Journal of the Royal Statistical Society: Series B (Statistical Methodology) , volume =

-

[51]

High-dimensional semi-supervised learning: in search for optimal inference of the mean. arXiv e-prints , keywords =

-

[52]

Optimal Semi-supervised Estimation and Inference for High-dimensional Linear Regression. arXiv e-prints , keywords =

-

[53]

Anru Zhang and Lawrence D. Brown and T. Tony Cai , title =. Ann. Statist. , number =

-

[54]

Regression shrinkage and selection via the lasso , Volume =

Tibshirani, Robert , Journal =. Regression shrinkage and selection via the lasso , Volume =

-

[55]

Constructive Approximation , volume=

Distributed kernel-based gradient descent algorithms , author=. Constructive Approximation , volume=. 2018 , publisher=

work page 2018

-

[56]

Xi Chen and Weidong Liu and Xiaojun Mao and Zhuoyi Yang , title =. J. Mach. Learn. Res. , year =

- [57]

-

[58]

Statistics for High-Dimensional Data: Methods, Theory and Applications , author=. 2011 , publisher=

work page 2011

-

[59]

Negahban and Pradeep Ravikumar and Martin J

Sahand N. Negahban and Pradeep Ravikumar and Martin J. Wainwright and Bin Yu , title =. Statist. Sci. , number =

-

[60]

Simultaneous analysis of Lasso and Dantzig selector , author=. Ann. Statist. , volume=. 2009 , publisher=

work page 2009

-

[61]

Brown and Michael Sklar and Richard Berk and Andreas Buja and Linda Zhao , title =

David Azriel and Lawrence D. Brown and Michael Sklar and Richard Berk and Andreas Buja and Linda Zhao , title =. J. Amer. Statist. Assoc. , volume =. 2021 , publisher =

work page 2021

-

[62]

Debiasing and Distributed Estimation for High-Dimensional Quantile Regression , year=

Zhao, Weihua and Zhang, Fode and Lian, Heng , journal=. Debiasing and Distributed Estimation for High-Dimensional Quantile Regression , year=

-

[63]

Heng Lian and Zengyan Fan , title =. J. Mach. Learn. Res. , year =

-

[64]

Zheng-Chu Guo and Lei Shi and Qiang Wu , title =. J. Mach. Learn. Res. , year =

-

[65]

arXiv preprint arXiv:2011.14185 , year=

Optimal Semi-supervised Estimation and Inference for High-dimensional Linear Regression , author=. arXiv preprint arXiv:2011.14185 , year=

-

[66]

Efficient and adaptive linear regression in semi-supervised settings

Chakrabortty, Abhishek and Cai, Tianxi. Efficient and adaptive linear regression in semi-supervised settings. Ann. Statist. 2018. doi:10.1214/17-AOS1594

-

[67]

Yuchen Zhang and John C. Duchi and Martin J. Wainwright , Journal =. Communication-efficient algorithms for statistical optimization , Volume =

-

[68]

Communication efficient distributed optimization using an approximate Newton-type method , Volume =

Ohad Shamir and Nati Srebro and Tong Zhang , Booktitle =. Communication efficient distributed optimization using an approximate Newton-type method , Volume =

-

[69]

On Quadratic Convergence of DC Proximal Newton Algorithm in Nonconvex Sparse Learning , volume =

Li, Xingguo and Yang, Lin and Ge, Jason and Haupt, Jarvis and Zhang, Tong and Zhao, Tuo , booktitle =. On Quadratic Convergence of DC Proximal Newton Algorithm in Nonconvex Sparse Learning , volume =

-

[70]

Individual Data Protected Integrative Regression Analysis of High-dimensional Heterogeneous Data. arXiv e-prints , keywords =

-

[71]

Yin, Dong and Chen, Yudong and Kannan, Ramchandran and Bartlett, Peter , booktitle =. 2018 , volume =

work page 2018

-

[72]

Minsker, Stanislav , title =. Electron. J. Statist. , year =. doi:10.1214/19-EJS1647 , fjournal =

-

[73]

Integrative High Dimensional Multiple Testing with Heterogeneity under Data Sharing Constraints. arXiv e-prints , keywords =

-

[74]

A fast iterative shrinkage-thresholding algorithm for linear inverse problems , author=. SIAM J. Imaging Sci. , volume=. 2009 , publisher=

work page 2009

- [75]

-

[76]

I-LAMM for sparse learning: Simultaneous control of algorithmic complexity and statistical error

Fan, Jianqing and Liu, Han and Sun, Qiang and Zhang, Tong. I-LAMM for sparse learning: Simultaneous control of algorithmic complexity and statistical error. Ann. Statist. 2018. doi:10.1214/17-AOS1568

-

[77]

Bootstrap confidence sets under model misspecification , author=. Ann. Statist. , volume=

-

[78]

Statistical consistency and asymptotic normality for high-dimensional robust M-estimators , volume =

Po-Ling Loh , journal =. Statistical consistency and asymptotic normality for high-dimensional robust M-estimators , volume =

-

[79]

Michael I. Jordan and Jason D. Lee and Yun Yang , title =. J. Amer. Statist. Assoc. , volume =. 2019 , publisher =

work page 2019

-

[80]

ell\_1 -regression with Heavy-tailed Distributions , Year =

Zhang, Lijun and Zhou, Zhi-Hua , Booktitle =. ell\_1 -regression with Heavy-tailed Distributions , Year =

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.