Affine Option Pricing with Hawkes-Type Endogenous Jump Activity

Pith reviewed 2026-06-29 01:53 UTC · model grok-4.3

The pith

The two-dimensional state process with endogenous jump activity admits an affine transform representation.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The coupled log-price and activity-state dynamics, constructed via state-dependent thinning of a Poisson random measure with normalized asymmetric tempered-stable jump sizes and bounded excitation g(y)=1-e^{-a y^2}, admit an affine transform representation. The associated generalized Riccati system is derived and shown to be well-posed on the real axis with forward invariance of the relevant complex half-plane. European options are then priced by a Fourier-cosine method that requires only the real-axis transform, under the risk-neutral drift restriction and a sufficient true-martingale condition obtained from the mean-subcriticality assumption.

What carries the argument

The affine transform representation of the two-dimensional state process (log-price and activity scale), which yields the generalized Riccati system.

If this is right

- Pathwise existence and uniqueness of the coupled dynamics hold under the mean-subcriticality condition.

- A risk-neutral drift restriction together with a sufficient martingale condition is obtained explicitly.

- European option prices are computed via the Fourier-cosine method using only the real-axis transform.

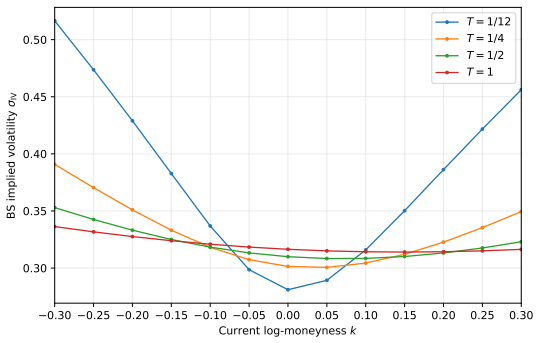

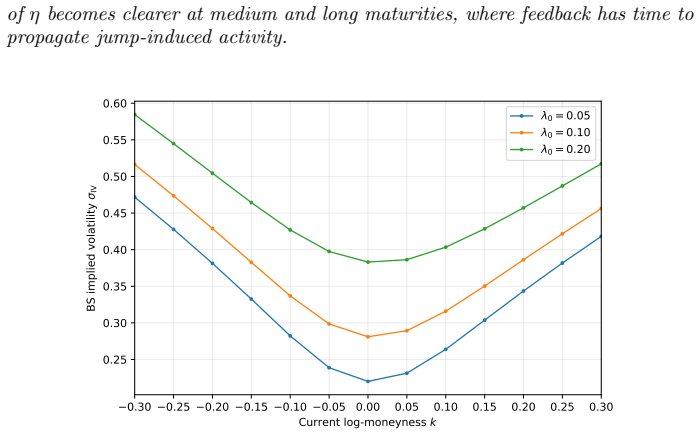

- Numerical experiments produce the model-implied volatility surface and show current activity shifting near-term volatility levels.

- Endogenous feedback controls the persistence of jump-induced skew across different maturities.

Where Pith is reading between the lines

- The same affine closure might be preserved if the excitation function is replaced by other bounded maps that keep total excitation finite.

- The real-axis well-posedness could simplify calibration routines that avoid complex-plane contour choices.

- The framework suggests a route for adding self-exciting jumps to other affine models without losing the transform representation.

- Market data on maturity-dependent skew could be used to test whether the estimated feedback strength matches the model's mean-subcriticality bound.

Load-bearing premise

The bounded excitation function together with the mean-subcriticality condition keeps average excitation finite and guarantees existence of the risk-neutral measure and the martingale property.

What would settle it

Monte Carlo paths of the price and activity process whose empirical characteristic function deviates from the solution of the Riccati system on the real axis, or simulated discounted prices that fail to be martingales.

Figures

read the original abstract

We develop a risk-neutral option-pricing model where the activity scale of an infinite-activity jump process is endogenously driven by the asset's own realized price jumps. Jump sizes are governed by a normalized asymmetric tempered-stable L\'evy shape, while a predictable activity scale controls the overall jump intensity and is normalized to coincide with the local jump-induced quadratic-variation rate. Endogenous feedback is introduced through the bounded excitation function $g(y)=1-e^{-ay^2}$, so that small realized jumps excite future activity approximately in proportion to squared jump size while the total average excitation remains finite. We construct the coupled log-price and activity-state dynamics by state-dependent thinning of a Poisson random measure, prove pathwise existence and uniqueness, derive the mean-subcriticality condition, and obtain both the risk-neutral drift restriction and a sufficient true-martingale condition. The resulting two-dimensional state process admits an affine transform representation. We derive the associated generalized Riccati system and prove real-axis well-posedness with forward invariance of the relevant complex half-plane. European options are priced by a Fourier-cosine (COS) method, which requires only the real-axis transform, and are benchmarked against a damped Carr--Madan (CM) inversion. Numerical experiments illustrate the model-implied volatility surface and show how current activity shifts near-term volatility levels, while endogenous feedback affects the persistence of jump-induced skew across maturities.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper develops a risk-neutral option-pricing model in which the activity scale of an infinite-activity jump process is endogenously driven by the asset's own realized price jumps. Jump sizes follow a normalized asymmetric tempered-stable Lévy shape, activity is updated via the bounded excitation function g(y)=1-e^{-a y^2}, and the coupled log-price/activity dynamics are constructed by state-dependent thinning of a Poisson random measure. The authors prove pathwise existence and uniqueness, derive the mean-subcriticality condition together with risk-neutral drift and true-martingale restrictions, establish the affine transform representation, derive the associated generalized Riccati system, and prove real-axis well-posedness with forward invariance of the relevant complex half-plane. European options are priced via the Fourier-cosine method and benchmarked against damped Carr-Madan inversion, with numerical illustrations of the implied volatility surface and the effects of current activity and endogenous feedback.

Significance. If the stated existence, uniqueness, martingale, and Riccati well-posedness results hold, the work supplies a tractable affine framework that incorporates Hawkes-type endogenous jump feedback while preserving the ability to price options by Fourier methods. The bounded excitation function together with the mean-subcriticality condition is a key technical device that keeps average excitation finite; the real-axis well-posedness result directly enables the COS pricing routine. These features distinguish the model from standard affine jump-diffusions and allow examination of how jump-induced skew persists across maturities.

major comments (2)

- [dynamics construction / generator derivation] The central claim that the two-dimensional state process is affine rests on the generator being affine after the state-dependent thinning construction. The manuscript should explicitly verify (in the section deriving the infinitesimal generator) that no non-affine remainder terms arise from the interaction between the bounded g(y) and the mark distribution of the tempered-stable measure.

- [mean-subcriticality and martingale conditions] The mean-subcriticality condition is invoked both for the true-martingale property and for the risk-neutral drift restriction. The paper should state the precise inequality (in terms of the parameters a and the tempering coefficients) and show that it is sufficient to close the integrability argument for the compensator of the thinned random measure.

minor comments (3)

- [model specification] The abstract refers to 'tempering parameters of the asymmetric tempered-stable Lévy measure' without listing their symbols; these should be introduced with explicit notation when the Lévy measure is first defined.

- [numerical experiments] In the numerical section the COS versus damped Carr-Madan comparison would benefit from tabulated relative pricing errors or convergence rates rather than qualitative statements alone.

- [Riccati well-posedness] A short remark clarifying why the forward invariance of the complex half-plane guarantees that the real-axis Riccati solution suffices for the COS method would improve readability for readers unfamiliar with the complex-plane analysis.

Simulated Author's Rebuttal

We thank the referee for the positive evaluation and the precise suggestions. Both major comments concern points of explicitness in the derivations rather than errors in the results; we will incorporate the requested verifications and statements in the revised manuscript.

read point-by-point responses

-

Referee: [dynamics construction / generator derivation] The central claim that the two-dimensional state process is affine rests on the generator being affine after the state-dependent thinning construction. The manuscript should explicitly verify (in the section deriving the infinitesimal generator) that no non-affine remainder terms arise from the interaction between the bounded g(y) and the mark distribution of the tempered-stable measure.

Authors: We agree that an explicit verification improves clarity. The state-dependent thinning is constructed so that the compensator of the thinned measure is exactly the activity coordinate multiplied by the fixed integral ∫ g(y) u(dy), where u is the normalized tempered-stable mark measure; because g(y) depends only on the mark and not on the state, and the mark measure is state-independent, the resulting generator applied to exponential-affine functions remains affine in the two state variables with no remainder. In the revision we will add a short paragraph immediately after the generator derivation that writes out this calculation and confirms the absence of non-affine terms. revision: yes

-

Referee: [mean-subcriticality and martingale conditions] The mean-subcriticality condition is invoked both for the true-martingale property and for the risk-neutral drift restriction. The paper should state the precise inequality (in terms of the parameters a and the tempering coefficients) and show that it is sufficient to close the integrability argument for the compensator of the thinned random measure.

Authors: The mean-subcriticality condition appears in Theorem 2.3 as the requirement that the expected excitation under the normalized mark measure stays below the reciprocal of the maximal tempering-adjusted moment; we will expand it explicitly to the inequality a ∫ y^{2} u_{\alpha,\beta}(dy) < 1 (with u_{\alpha,\beta} the normalized asymmetric tempered-stable measure) and add a short integrability lemma showing that this bound, together with the linear growth control on the compensator, guarantees that the integrated intensity remains finite almost surely. This will be inserted in Section 2.3 of the revision. revision: yes

Circularity Check

No significant circularity; derivation self-contained

full rationale

The paper constructs the two-dimensional state process explicitly from state-dependent thinning of a Poisson random measure whose mark distribution is independent of state and whose activity update uses the bounded function g(y). The generator is therefore affine in the state variables by the explicit form of the dynamics, so the characteristic function satisfies the generalized Riccati system by the standard affine-process argument; this is not a reduction of the claim to its own inputs. No self-citations appear as load-bearing premises, no parameters are fitted then renamed as predictions, and the mean-subcriticality condition is derived from the model to guarantee integrability rather than assumed to force the affine representation. The well-posedness proof on the real axis likewise proceeds from the boundedness and subcriticality assumptions without circular redefinition.

Axiom & Free-Parameter Ledger

free parameters (2)

- a

- tempering parameters of the asymmetric tempered-stable Lévy measure

axioms (2)

- domain assumption Mean-subcriticality condition

- standard math Pathwise existence and uniqueness of the state-dependent thinned Poisson random measure

Reference graph

Works this paper leans on

-

[1]

Modeling financial contagion using mutually exciting jump processes.Journal of Financial Economics, 117(3):585–606, 2015

Yacine A¨ ıt-Sahalia, Julio Cacho-Diaz, and Roger JA Laeven. Modeling financial contagion using mutually exciting jump processes.Journal of Financial Economics, 117(3):585–606, 2015

2015

-

[2]

Hawkes processes in finance.Market Microstructure and Liquidity, 1(01):1550005, 2015

Emmanuel Bacry, Iacopo Mastromatteo, and Jean-Fran¸ cois Muzy. Hawkes processes in finance.Market Microstructure and Liquidity, 1(01):1550005, 2015. 42

2015

-

[3]

Set invariance in control.Automatica, 35(11):1747–1767, 1999

Franco Blanchini. Set invariance in control.Automatica, 35(11):1747–1767, 1999

1999

-

[4]

The fine struc- ture of asset returns: An empirical investigation.The journal of Business, 75(2):305–332, 2002

Peter Carr, H´ elyette Geman, Dilip B Madan, and Marc Yor. The fine struc- ture of asset returns: An empirical investigation.The journal of Business, 75(2):305–332, 2002

2002

-

[5]

Option valuation using the fast fourier trans- form.Journal of computational finance, 2(4):61–73, 1999

Peter Carr and Dilip Madan. Option valuation using the fast fourier trans- form.Journal of computational finance, 2(4):61–73, 1999

1999

-

[6]

Coddington and Norman Levinson.Theory of Ordinary Differential Equations

Earl A. Coddington and Norman Levinson.Theory of Ordinary Differential Equations. McGraw–Hill, 1955

1955

-

[7]

Chapman and Hall/CRC, 2003

Rama Cont and Peter Tankov.Financial modelling with jump processes. Chapman and Hall/CRC, 2003

2003

-

[8]

Springer, 2003

Daryl J Daley and David Vere-Jones.An introduction to the theory of point processes: volume I: elementary theory and methods. Springer, 2003

2003

-

[9]

Courier Corporation, 2007

Philip J Davis and Philip Rabinowitz.Methods of numerical integration. Courier Corporation, 2007

2007

-

[10]

Exponential and uni- form ergodicity of markov processes.The Annals of Probability, 23(4):1671– 1691, 1995

Douglas Down, Sean P Meyn, and Richard L Tweedie. Exponential and uni- form ergodicity of markov processes.The Annals of Probability, 23(4):1671– 1691, 1995

1995

-

[11]

Affine pro- cesses and applications in finance.The Annals of Applied Probability, 13(3):984–1053, 2003

Darrell Duffie, Damir Filipovi´ c, and Walter Schachermayer. Affine pro- cesses and applications in finance.The Annals of Applied Probability, 13(3):984–1053, 2003

2003

-

[12]

Transform analysis and asset pricing for affine jump-diffusions.Econometrica, 68(6):1343–1376, 2000

Darrell Duffie, Jun Pan, and Kenneth Singleton. Transform analysis and asset pricing for affine jump-diffusions.Econometrica, 68(6):1343–1376, 2000

2000

-

[13]

On the range of options prices.Finance and Stochastics, 1(2):131–140, 1997

Ernst Eberlein and Jean Jacod. On the range of options prices.Finance and Stochastics, 1(2):131–140, 1997

1997

-

[14]

Affine point pro- cesses and portfolio credit risk.SIAM Journal on Financial Mathematics, 1(1):642–665, 2010

Eymen Errais, Kay Giesecke, and Lisa R Goldberg. Affine point pro- cesses and portfolio credit risk.SIAM Journal on Financial Mathematics, 1(1):642–665, 2010

2010

-

[15]

A novel pricing method for euro- pean options based on fourier-cosine series expansions.SIAM Journal on Scientific Computing, 31(2):826–848, 2009

Fang Fang and Cornelis W Oosterlee. A novel pricing method for euro- pean options based on fourier-cosine series expansions.SIAM Journal on Scientific Computing, 31(2):826–848, 2009

2009

-

[16]

Calculation of gauss quadrature rules

Gene H Golub and John H Welsch. Calculation of gauss quadrature rules. Mathematics of computation, 23(106):221–230, 1969

1969

-

[17]

Spectra of some self-exciting and mutually exciting point processes.Biometrika, 58(1):83–90, 1971

Alan G Hawkes. Spectra of some self-exciting and mutually exciting point processes.Biometrika, 58(1):83–90, 1971. 43

1971

-

[18]

A cluster process representation of a self-exciting process.Journal of applied probability, 11(3):493–503, 1974

Alan G Hawkes and David Oakes. A cluster process representation of a self-exciting process.Journal of applied probability, 11(3):493–503, 1974

1974

-

[19]

The cumulant process and esscher’s change of measure.Finance and stochastics, 6(4):397–428, 2002

Jan Kallsen and Albert N Shiryaev. The cumulant process and esscher’s change of measure.Finance and stochastics, 6(4):397–428, 2002

2002

-

[20]

Clarendon Press, 1992

John Frank Charles Kingman.Poisson processes, volume 3. Clarendon Press, 1992

1992

-

[21]

Exponential stock models driven by tem- pered stable processes.Journal of Econometrics, 181(1):53–63, 2014

Uwe K¨ uchler and Stefan Tappe. Exponential stock models driven by tem- pered stable processes.Journal of Econometrics, 181(1):53–63, 2014

2014

-

[22]

Sur l’int´ egrabilit´ e uniforme des mar- tingales exponentielles.Zeitschrift f¨ ur Wahrscheinlichkeitstheorie und ver- wandte Gebiete, 42(3):175–203, 1978

Dominique L´ epingle and Jean M´ emin. Sur l’int´ egrabilit´ e uniforme des mar- tingales exponentielles.Zeitschrift f¨ ur Wahrscheinlichkeitstheorie und ver- wandte Gebiete, 42(3):175–203, 1978

1978

-

[23]

Strong solutions of jump-type stochastic equations

Zenghu Li and Fei Pu. Strong solutions of jump-type stochastic equations. Electronic Communications in Probability, 17(33):1–13, 2012

2012

-

[24]

Option pricing when underlying stock returns are dis- continuous.Journal of financial economics, 3(1-2):125–144, 1976

Robert C Merton. Option pricing when underlying stock returns are dis- continuous.Journal of financial economics, 3(1-2):125–144, 1976

1976

-

[25]

Stability of markovian processes III: Foster–lyapunov criteria for continuous-time processes.Advances in Applied Probability, 25(3):518–548, 1993

Sean P Meyn and Richard L Tweedie. Stability of markovian processes III: Foster–lyapunov criteria for continuous-time processes.Advances in Applied Probability, 25(3):518–548, 1993

1993

-

[26]

Tempering stable processes.Stochastic processes and their applications, 117(6):677–707, 2007

Jan Rosi´ nski. Tempering stable processes.Stochastic processes and their applications, 117(6):677–707, 2007

2007

-

[27]

Scipy 1.0: fundamental algorithms for scientific computing in python.Nature methods, 17(3):261–272, 2020

Pauli Virtanen, Ralf Gommers, Travis E Oliphant, Matt Haberland, Tyler Reddy, David Cournapeau, Evgeni Burovski, Pearu Peterson, Warren Weckesser, Jonathan Bright, et al. Scipy 1.0: fundamental algorithms for scientific computing in python.Nature methods, 17(3):261–272, 2020

2020

-

[28]

Springer Berlin Heidelberg New York, 1996

Gerhard Wanner and Ernst Hairer.Solving ordinary differential equations II, volume 375. Springer Berlin Heidelberg New York, 1996. 44

1996

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.