Ownership Networks and Economic Power in the Italian Energy Sector

Pith reviewed 2026-06-29 19:41 UTC · model grok-4.3

The pith

Global financial actors centralize control over Italian energy infrastructure through common ownership, despite formal state majority.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

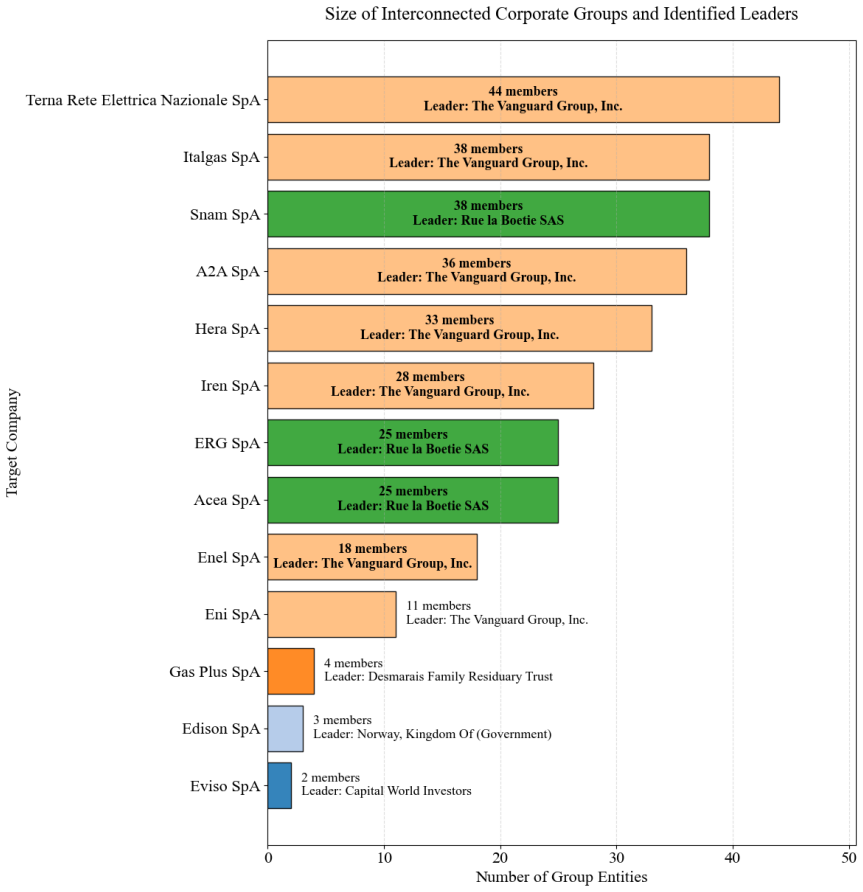

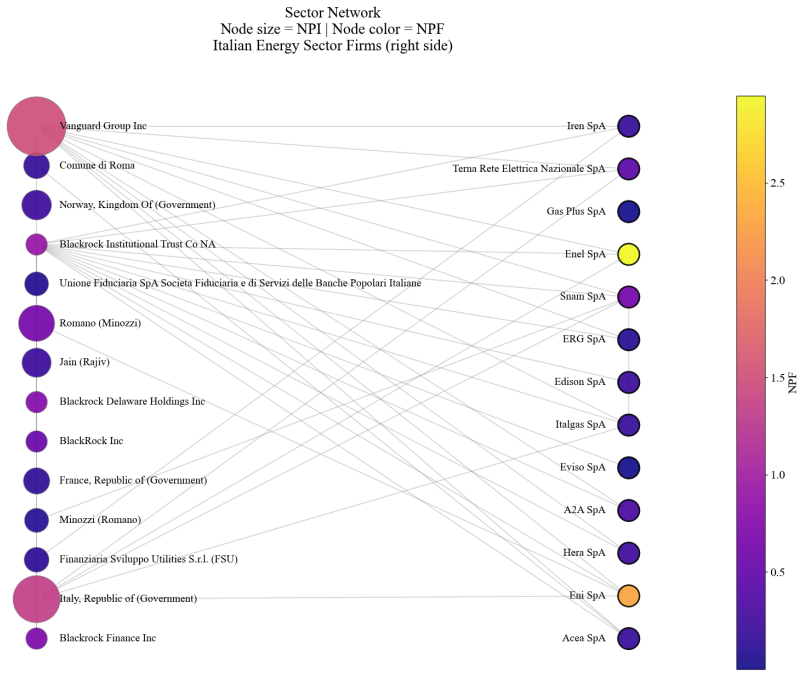

Applying the Aggregate Network Power Index and Aggregate Network Power Flow to the Italian energy sector reveals a Governance Paradox in which the State retains formal majority ownership yet the sector's reliance on global capital markets and common ownership by transnational investors has progressively hollowed out public strategic direction, enabling global financial actors to internalize sectoral competition and foster tacit strategic convergence in the management of critical infrastructure.

What carries the argument

The Aggregate Network Power Index (A-NPI) and Aggregate Network Power Flow (A-NPF), sector-level extensions of the Network Power framework that aggregate firm-level control and influence while accounting for relative economic weight of each operator.

If this is right

- This configuration challenges European strategic autonomy.

- Traditional Foreign Direct Investment screening and antitrust tools may be inadequate for addressing systemic influence through networked ownership.

- Capital centralization enables global financial actors to internalize sectoral competition.

- The pervasive presence of common ownership by transnational institutional investors reduces the effectiveness of state ownership in directing strategy.

Where Pith is reading between the lines

- Similar patterns may appear in energy sectors of other European countries with mixed public-private ownership.

- Antitrust policies could need updates to account for common ownership effects in critical infrastructure.

- Further application of these indices to other sectors could reveal whether the governance paradox is energy-specific or more widespread.

Load-bearing premise

The Aggregate Network Power Index and Aggregate Network Power Flow accurately aggregate firm-level ownership data into reliable measures of systemic control without substantial gaps or distortions in the ownership records.

What would settle it

Detailed ownership records showing no significant common ownership by the same transnational investors across major Italian energy firms, or evidence that strategic decisions by those firms diverge rather than converge.

Figures

read the original abstract

The energy sector is a cornerstone of national strategic autonomy, yet its increasing financialization has transformed ownership structures into complex networked configurations. This paper investigates the distribution of economic power in the Italian energy sector by introducing two sector-level extensions of the Network Power framework: the Aggregate Network Power Index (A-NPI) and the Aggregate Network Power Flow (A-NPF). Unlike traditional macro-level measures, these indices aggregate firm-level control and influence into a systemic framework that accounts for the relative economic weight of each operator. Applying this framework to the Italian case reveals a "Governance Paradox": while the State retains formal majority ownership, the sector's deepening reliance on global capital markets and the pervasive presence of common ownership by transnational institutional investors have progressively hollowed out public strategic direction. The results show that capital centralization enables global financial actors to internalize sectoral competition, fostering a regime of tacit strategic convergence in the management of critical infrastructure. This configuration challenges European strategic autonomy, raising questions about the adequacy of traditional Foreign Direct Investment (FDI) screening and antitrust tools in addressing the systemic influence exerted through networked ownership structures.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces the Aggregate Network Power Index (A-NPI) and Aggregate Network Power Flow (A-NPF) as sector-level extensions of the Network Power framework. These aggregate firm-level ownership data, weighted by economic size, to quantify systemic control and influence. Applied to the Italian energy sector, the analysis identifies a Governance Paradox in which formal state majority ownership coexists with effective influence by transnational institutional investors via common ownership, resulting in internalized competition and tacit strategic convergence in critical infrastructure management.

Significance. If the aggregation steps hold, the work supplies a replicable, data-scoped method for measuring networked economic power in strategic sectors and supplies falsifiable predictions about the effects of common ownership on governance. The explicit scoping of the indices to available ownership records, rather than assuming complete data, is a methodological strength.

major comments (2)

- [§3.2] §3.2, Eq. (3) for A-NPI: the weighting by relative economic size is load-bearing for the centralization claim, yet the text does not report a sensitivity check that replaces the chosen size proxy (e.g., revenues vs. assets) with an alternative; such a check is required to confirm that the Governance Paradox result is not an artifact of the weighting choice.

- [Table 2, §4.3] Table 2 and §4.3: the reported A-NPF flows for the top five investors show high concentration, but the paper does not quantify the share of ownership links that are missing or imputed; without this, the claim that global actors internalize sectoral competition rests on an untested completeness assumption that directly affects the paradox conclusion.

minor comments (2)

- [Abstract] The abstract states conclusions about policy implications without referencing the specific A-NPF thresholds or robustness tables that support them; a one-sentence pointer to the relevant result would improve clarity.

- [§3] Notation for the economic-weight term w_i is introduced in §3 but used without re-definition in the results; a short notation table would reduce reader effort.

Simulated Author's Rebuttal

We thank the referee for the constructive comments and the positive evaluation of the methodological contribution. We address each major comment below.

read point-by-point responses

-

Referee: [§3.2] §3.2, Eq. (3) for A-NPI: the weighting by relative economic size is load-bearing for the centralization claim, yet the text does not report a sensitivity check that replaces the chosen size proxy (e.g., revenues vs. assets) with an alternative; such a check is required to confirm that the Governance Paradox result is not an artifact of the weighting choice.

Authors: We agree that the choice of size proxy merits explicit robustness verification. In the revised manuscript we will add a dedicated sensitivity subsection that recomputes A-NPI under alternative proxies (total assets and, where available, market capitalization) and confirm that the centralization pattern and the Governance Paradox remain qualitatively unchanged. revision: yes

-

Referee: [Table 2, §4.3] Table 2 and §4.3: the reported A-NPF flows for the top five investors show high concentration, but the paper does not quantify the share of ownership links that are missing or imputed; without this, the claim that global actors internalize sectoral competition rests on an untested completeness assumption that directly affects the paradox conclusion.

Authors: The paper already scopes both indices explicitly to observed ownership records and does not assume completeness. To respond directly to the request for transparency, the revision will include a new paragraph (and accompanying table note) that reports the share of ownership links that are directly observed versus imputed or missing in the primary data source for the Italian energy sector. revision: yes

Circularity Check

No significant circularity detected

full rationale

The provided abstract and skeptic analysis introduce A-NPI and A-NPF as extensions of an existing Network Power framework applied to ownership data, but contain no equations, self-citations, or derivations that reduce the central claims (such as the Governance Paradox) to definitional choices, fitted inputs, or self-referential steps. The aggregation is explicitly scoped to available records with noted internal consistency, and no load-bearing premise relies on prior author work that itself assumes the target result. The derivation chain is therefore self-contained.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Aguilera, R. V., K. A. Desender, and M. L´ opez-Puertas Lamy (2024). From universal owners to owners of the universe? how the big three are reshaping corporate governance.Corporate Governance: An International Review 33(3), 462–482. Andres, L. A., J. L. Guasch, and S. Lopez Azumendi (2011). Governance in state-owned en- terprises revisited: The cases of w...

-

[2]

Enel contest highlights complexities and opacity in italian board nomina- tions

Glass Lewis (2023). Enel contest highlights complexities and opacity in italian board nomina- tions. Gruppo CoMar (2026). Analisi capitalizzazione societ` a energetiche quotate al 1°gennaio

2023

-

[3]

Herrmann, N

3ªed. Herrmann, N. D., J. M. McInnis, B. Monsen, and L. T. Starks (2025). Decentralizing voting power.European Corporate Governance Institute–Finance Working Paper(1092). Leal, A. B. and W. L. R. Gallo (2026). Petrobras and the abandonment of the downstream sector in brazil.The Extractive Industries and Society 25, 101766. Mizuno, T., S. Doi, and S. Kuriz...

2025

-

[4]

Pannone, A., A

Paris: OECD Publishing. Pannone, A., A. Abeltino, T. Bacaloni, A. Bernardini, and F. Giancaterini (2026). Financial intermediaries and capital centralization in global fdi: A network approach to tracing transna- tional corporate control. Available at SSRN. Prontera, A., P. Arrigoni, R. Lizzi, and A. Rubino (2025). Relaunching the italian energy tran- siti...

2026

-

[5]

Shapley, L. S. and M. Shubik (1954). A method for evaluating the distribution of power in a committee system.American political science review 48(3), 787–792. Terna (2025). Rapporto mensile sul sistema elettrico - dicembre

1954

-

[6]

(1988).The Theory of Industrial Organization

Tirole, J. (1988).The Theory of Industrial Organization. MIT Press. 27

1988

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.