Realtime price impact detection

Pith reviewed 2026-06-27 04:38 UTC · model grok-4.3

The pith

A timing test detects per-action price impact by checking whether adverse market moves arrive surprisingly soon after a trader's actions.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

Price impact can be detected on a per-action basis by testing for statistical surprise in the timing of adverse market events after a trader's action, providing a direct signature of causation and information leakage without needing large samples of fills.

What carries the argument

A statistical test for surprise in the timing of adverse events that occur after the trader's action.

If this is right

- Traders can distinguish their own impact from competing liquidity demand and choose opposite responses in each case.

- Dynamic adjustments become feasible without waiting for hundreds of fills to estimate slippage.

- The method supplies per-action signals that can be used inside live execution algorithms.

Where Pith is reading between the lines

- If the timing test proves reliable it could be layered onto existing execution systems to reduce leakage on a trade-by-trade basis.

- The same synchronicity idea might apply to detecting impact in limit-order placement or cancellation sequences.

Load-bearing premise

Unusually rapid adverse market moves after an action are caused by that action rather than by unrelated participants or random timing.

What would settle it

Real execution data in which the timing-surprise measure shows no reliable association with subsequent price moves that can be attributed to the trader's own orders.

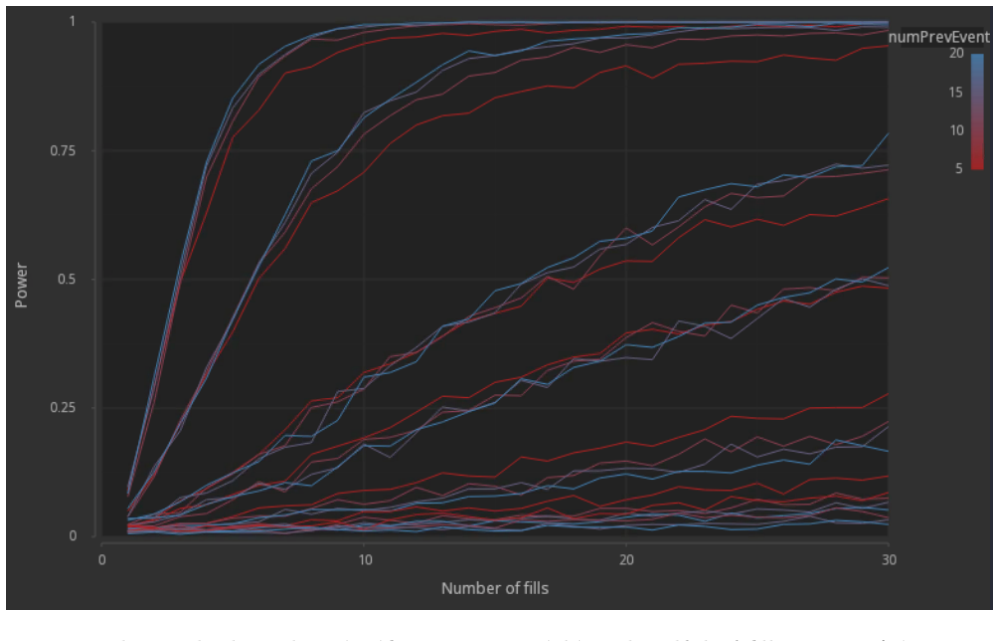

Figures

read the original abstract

An important question for an algo trader working an order is to understand if their actions are moving the market against them -- i.e., causing market impact. The conventional answer usually is one of two: (i) monitor price slippage in real-time, potentially reducing adverse activity with increased slippage, or (ii) do away with dynamic trading adjustments and rely on semi-static rules based on ex-post estimates of slippage over a large sample of events. Realtime monitoring fails because reliably estimating slippage is statistically expensive -- it requires hundreds of fills before it can be told apart from background volatility. More fundamentally however, it does not establish causality. Observed adverse price moves may be caused by the trader's own actions, or by an unrelated participant competing for the same liquidity and capturing the same alpha. The optimal response (say, slow down vs.\ speed up) is opposite in the two cases. We propose a method that detects price impact, on a per-action basis, by measuring the timing synchronicity between a trader's actions and subsequent adverse market events. The method at heart is a test for statistical \emph{surprise} in the timing of adverse events post trader action. We must be clear in that we do make a leap of faith here and assume that surprisingly fast adverse market events are evidence of causation and that the action triggered them -- a direct signature of impact and information leakage. Validating it requires real execution data; we set out the empirical tests that would do so.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a method for realtime, per-action detection of price impact by testing for statistical surprise in the timing of adverse market events following trader actions. It contrasts this with conventional real-time slippage monitoring (statistically expensive and non-causal) and ex-post estimates, while explicitly labeling as a 'leap of faith' the assumption that timing synchronicity indicates the action caused the adverse events. The manuscript outlines empirical tests for validation using real execution data but presents no results, derivations, or data.

Significance. If the core assumption can be justified and the method validated, the approach would enable causal rather than correlational inference on impact, allowing traders to respond differently to self-induced versus external adverse moves. The paper's clear articulation of the assumption and the validation path is a strength, though the absence of any supporting analysis limits immediate applicability.

major comments (1)

- [Abstract] Abstract: The central claim that the timing-based statistical surprise test detects price impact (rather than mere correlation) rests entirely on the untested assumption that 'surprisingly fast adverse market events are evidence of causation and that the action triggered them'. This is explicitly called a 'leap of faith' with no derivation, bounds, simulation results, or robustness checks against confounders such as private information or competing participants provided anywhere in the manuscript.

minor comments (1)

- The statistical test for 'surprise' in event timing is described only at a high level; adding a formal definition, pseudocode, or reference to a standard test (e.g., Poisson process timing) would improve clarity and allow readers to assess the proposal's feasibility.

Simulated Author's Rebuttal

We thank the referee for the careful reading and for identifying the central assumption in our proposal. The manuscript is explicitly framed as a methodological outline that labels the key step a 'leap of faith' and sets out the empirical validation path; we address the comment below and will make targeted revisions.

read point-by-point responses

-

Referee: [Abstract] Abstract: The central claim that the timing-based statistical surprise test detects price impact (rather than mere correlation) rests entirely on the untested assumption that 'surprisingly fast adverse market events are evidence of causation and that the action triggered them'. This is explicitly called a 'leap of faith' with no derivation, bounds, simulation results, or robustness checks against confounders such as private information or competing participants provided anywhere in the manuscript.

Authors: We agree that the assumption is untested in the current manuscript. The text already states this limitation plainly ('we do make a leap of faith here') and notes that validation 'requires real execution data' for which we outline the necessary empirical tests. The contribution is the proposal of the timing-synchronicity test itself together with the validation roadmap, not a claim of validated causality. In revision we will expand the discussion to address potential confounders (private information, competing participants) and how the proposed tests could help isolate them; we will also add a short section on possible simulation-based bounds where these can be constructed without proprietary data. revision: partial

- Provision of actual empirical results, derivations, or data, which the manuscript states cannot be supplied without access to real trader execution records.

Circularity Check

No circularity: proposal rests on explicit untested assumption with no derivations or self-citation chains

full rationale

The manuscript is a high-level method proposal without equations, fitted parameters, or derivations. The central claim explicitly flags its key step as a 'leap of faith' assumption rather than a derived result. No load-bearing steps reduce to self-definition, fitted inputs renamed as predictions, or self-citation. The work is self-contained as a testable proposal whose validity is left to future empirical checks.

Axiom & Free-Parameter Ledger

axioms (1)

- ad hoc to paper Surprisingly fast adverse market events are evidence of causation from the trader's action

Reference graph

Works this paper leans on

-

[1]

Lawless, J.F., Fredette, M., Frequentist prediction intervals and predictive distributions, Biometrika, Vol 92, Issue 3, pp.\ 529--542, 2005. doi:10.1093/biomet/92.3.529

-

[2]

Monotone Regression Splines in Action

Bjørnstad, J.F., Predictive likelihood: a review, Statistical Science, Vol 5, Issue 2, pp.\ 242--254, 1990. doi:10.1214/ss/1177012175

-

[3]

Schmidt, D.F., Makalić, E., Universal models for the exponential distribution, IEEE Transactions on Information Theory, Vol 55, Issue 7, pp.\ 3087--3090, 2009. doi:10.1109/TIT.2009.2018331

-

[4]

Fisher, R.A., Statistical Methods for Research Workers, 1925 (Oliver and Boyd: Edinburgh)

1925

-

[5]

Farmer, J.D., Market force, ecology and evolution, Industrial and Corporate Change, Vol 11, Issue 5, pp.\ 895--953, 2002. doi:10.1093/icc/11.5.895

-

[6]

Hawkes, A.G., Spectra of some self-exciting and mutually exciting point processes, Biometrika, Vol 58, Issue 1, pp.\ 83--90, 1971. doi:10.1093/biomet/58.1.83

-

[7]

Jeffreys, H., An invariant form for the prior probability in estimation problems, Proceedings of the Royal Society of London A, Vol 186, No 1007, pp.\ 453--461, 1946. doi:10.1098/rspa.1946.0056

-

[8]

Navigating dark liquidity (How Fisher catches Poisson in the Dark)

Zovko, I.I., Navigating dark liquidity (How Fisher catches Poisson in the Dark), working paper, 2017. arXiv:1710.06350, doi:10.48550/arXiv.1710.06350

work page internal anchor Pith review Pith/arXiv arXiv doi:10.48550/arxiv.1710.06350 2017

-

[9]

Easley, D., L\'opez de Prado, M., O'Hara, M., Flow toxicity and liquidity in a high-frequency world, Review of Financial Studies, Vol 25, Issue 5, pp.\ 1457--1493, 2012. doi:10.1093/rfs/hhs053

-

[10]

doi:10.1080/14697688.2026.2619539

Cartea, \'A., Duran-Martin, G., S\'anchez-Betancourt, L., Detecting toxic flow, Quantitative Finance, Vol 26, 2026. doi:10.1080/14697688.2026.2619539

-

[11]

doi:10.1080/14697688.2014.897000

Bacry, E., Muzy, J.F., Hawkes model for price and trades high-frequency dynamics, Quantitative Finance, Vol 14, Issue 7, pp.\ 1147--1166, 2014. doi:10.1080/14697688.2014.897000

-

[12]

Engle, R.F., Russell, J.R., Autoregressive conditional duration: a new model for irregularly spaced transaction data, Econometrica, Vol 66, Issue 5, pp.\ 1127--1162, 1998. doi:10.2307/2999632

-

[13]

Engle, R.F., The econometrics of ultra-high-frequency data, Econometrica, Vol 68, Issue 1, pp.\ 1--22, 2000. doi:10.1111/1468-0262.00091

-

[14]

A subordinated stochastic pro- cess model with finite variance for speculative prices

Clark, P.K., A subordinated stochastic process model with finite variance for speculative prices, Econometrica, Vol 41, Issue 1, pp.\ 135--155, 1973. doi:10.2307/1913889

-

[15]

An\'e, T., Geman, H., Order flow, transaction clock, and normality of asset returns, Journal of Finance, Vol 55, Issue 5, pp.\ 2259--2284, 2000. doi:10.1111/0022-1082.00286

-

[16]

doi:10.1080/14697688.2016.1201589

Oomen, R., Last look, Quantitative Finance, Vol 17, Issue 7, pp.\ 1057--1070, 2017. doi:10.1080/14697688.2016.1262545

-

[17]

doi:10.1080/14697688.2016.1201589

Oomen, R., Execution in an aggregator, Quantitative Finance, Vol 17, Issue 3, pp.\ 383--404, 2017. doi:10.1080/14697688.2016.1201589

-

[18]

doi:10.1080/14697688.2018.1504167

Butz, M., Oomen, R., Internalisation by electronic FX spot dealers, Quantitative Finance, Vol 19, Issue 1, pp.\ 35--56, 2019. doi:10.1080/14697688.2018.1504167

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.