Ab initio simulation of market dynamics

Pith reviewed 2026-05-25 06:29 UTC · model grok-4.3

The pith

Simulations of traders with multi-good utility functions require time-preference for stable prices to form.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

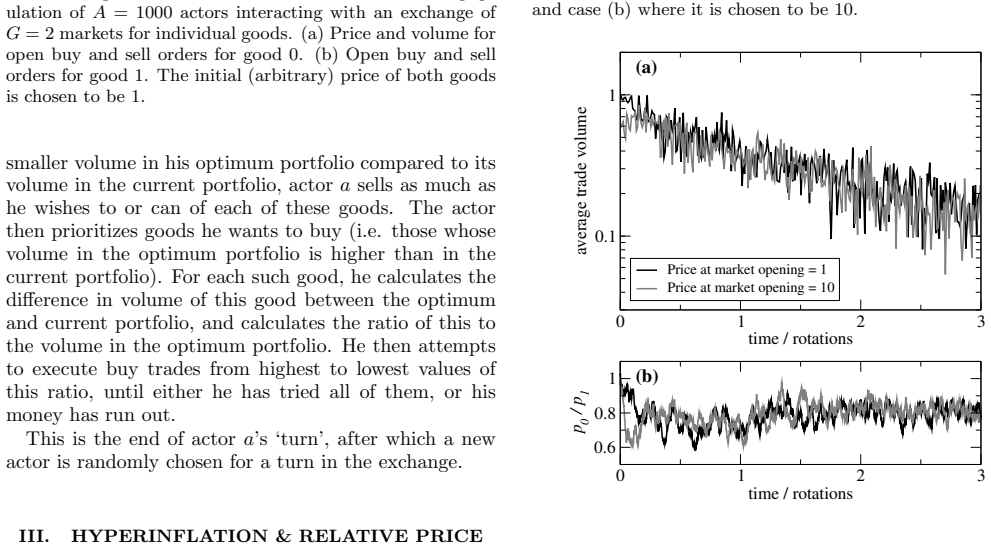

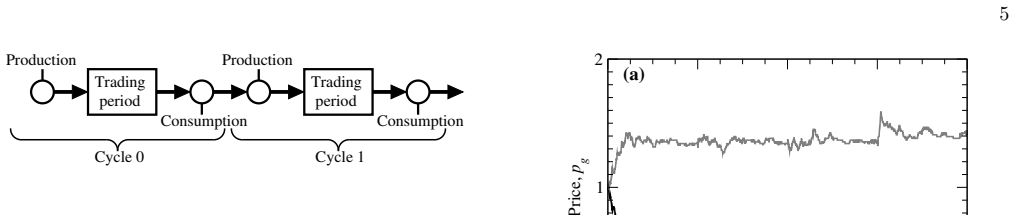

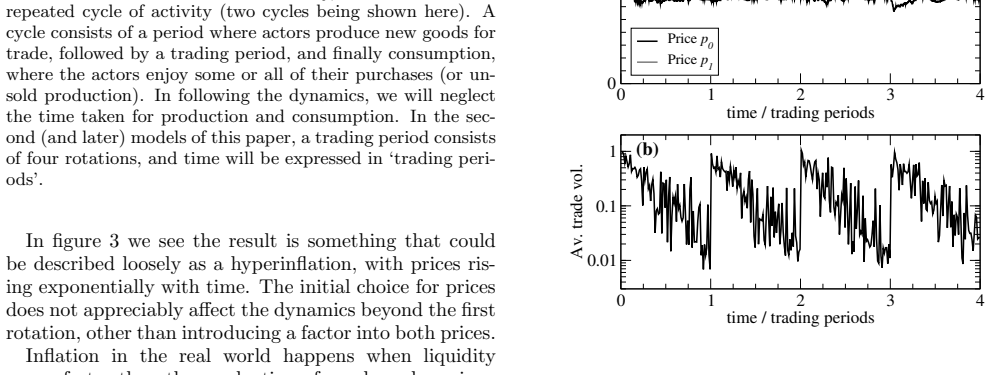

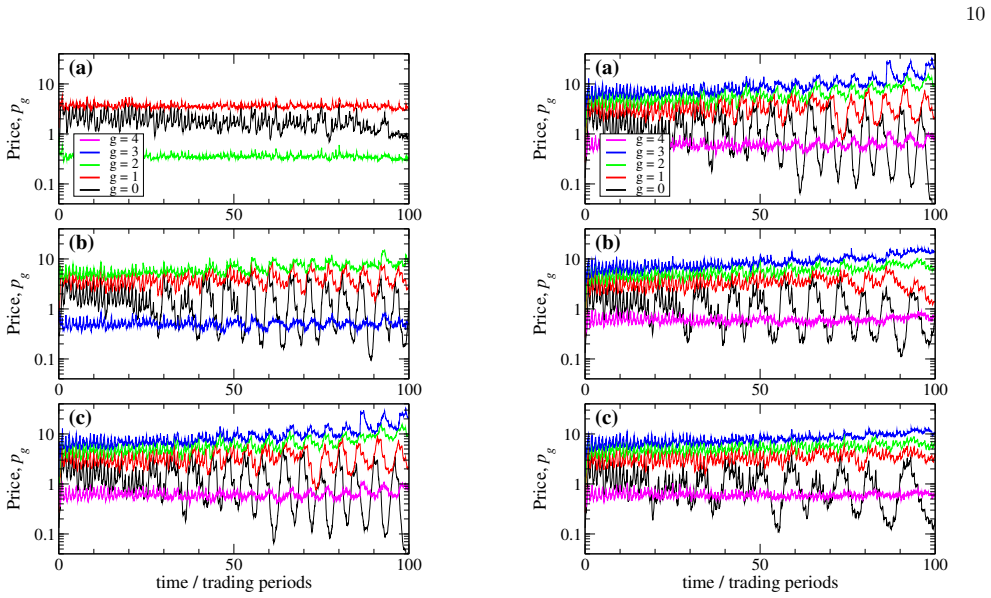

A collection of actors whose utility functions capture compromises across goods, when placed in double-auction markets, generate self-consistent prices that remain stable only if the actors discount future utility; the fluctuations around those prices obey algebraic tails, and explicit inflation expectations produce complex oscillatory dynamics that can be damped or sustained.

What carries the argument

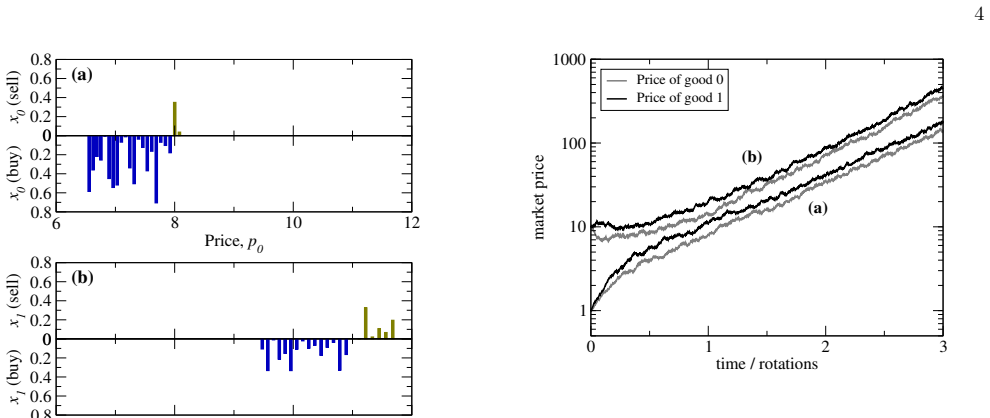

Utility-function models of actors trading multiple goods for money, executed through per-good double-auction market rules.

If this is right

- Stable price formation occurs only when actors include time-preference.

- Price fluctuations exhibit distributions with algebraic tails.

- Inflation expectations produce complex damped or undamped price oscillations.

- Input-output economic models remain difficult to stabilize under the same utility and market assumptions.

Where Pith is reading between the lines

- Different utility functional forms could be tested to stabilize input-output structures while preserving algebraic tails.

- Empirical price series could be examined for algebraic tails to check consistency with the simulated dynamics.

- The requirement for time-preference points to a minimal psychological ingredient needed to prevent perpetual price drift in agent models.

Load-bearing premise

The chosen functional form for each actor's utility across multiple goods produces self-consistent rational compromises without artifacts forced by the double-auction rules.

What would settle it

Running the simulation without time-preference and observing stable prices, or recording price fluctuations whose distribution lacks algebraic tails.

Figures

read the original abstract

We provide simple models for the utility function (or psychology) of an actor trading a multitude of goods for money. In this framework, money has no intrinsic consumption value, but is required as a medium of exchange. A collection of such actors are then simulated interacting through market rules which create a double auction for each of the goods. This framework captures the self-consistent, rational behavior of independent actors, including how they make compromises between purchases of different goods; so goes beyond price-demand curves, and also generates the small-scale fluctuations from individual trades. We find that stable price formation requires a model that includes time-preference for the actors. Fluctuations in prices show a distribution with algebraic tails. Including inflation expectations leads to complex, damped or un-damped price oscillations. We attempt to model the dynamics of input-output economic models, but find it difficult to keep prices stable with the assumptions employed.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript develops simple utility models for agents trading multiple goods (with money as a pure medium of exchange) and simulates their interactions via double-auction markets. It reports that stable price formation requires incorporating time-preference, that price fluctuations exhibit algebraic tails, and that inflation expectations produce damped or undamped oscillations; an attempt to embed input-output models is also described but encounters stability problems.

Significance. If the central simulation results prove robust to the specific functional forms and rules employed, the work would provide a useful bottom-up demonstration of how temporal preferences and inflation expectations shape emergent market stability and fluctuation statistics, complementing traditional price-demand analyses with explicit multi-good compromise behavior.

major comments (3)

- [Abstract] Abstract: the claim that stable price formation 'requires' a model including time-preference is load-bearing for the main result, yet the manuscript provides no explicit functional forms for the utility (or psychology) of trading multiple goods, nor the precise double-auction clearing rules; without these it is impossible to determine whether the necessity is general or an artifact of the chosen specifications, directly engaging the stress-test concern.

- [Abstract] Abstract and results sections: the reported algebraic tails and inflation-induced oscillations are presented without the exact parameter choices, statistical tests used to establish the power-law behavior, or quantitative measures of damping, rendering the fluctuation claims unverifiable from the given information.

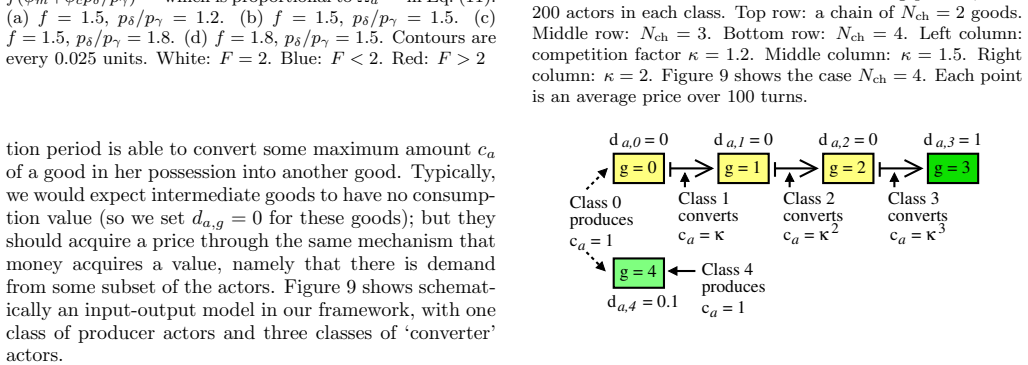

- [Input-output attempt] Input-output modeling paragraph: the statement that it is 'difficult to keep prices stable with the assumptions employed' is presented without the concrete modifications attempted or the resulting instability metrics, so the difficulty cannot be assessed as a general limitation versus a modeling choice.

minor comments (1)

- [Abstract] The abstract uses 'ab initio' while describing the models as 'simple'; a brief clarification of what is taken as given versus derived would improve precision.

Simulated Author's Rebuttal

We thank the referee for their thoughtful review and constructive suggestions. We address each major comment below and agree that greater specificity is required to support the central claims and allow independent assessment of robustness.

read point-by-point responses

-

Referee: [Abstract] Abstract: the claim that stable price formation 'requires' a model including time-preference is load-bearing for the main result, yet the manuscript provides no explicit functional forms for the utility (or psychology) of trading multiple goods, nor the precise double-auction clearing rules; without these it is impossible to determine whether the necessity is general or an artifact of the chosen specifications, directly engaging the stress-test concern.

Authors: The manuscript develops and simulates specific utility models in which time preference proves necessary for price stability under the double-auction rules employed. We accept that the functional forms and clearing rules must be stated explicitly to permit evaluation of whether the result is model-specific. In the revision we will add a dedicated methods subsection presenting the exact utility expressions, the multi-good compromise rule, and the double-auction matching algorithm. revision: yes

-

Referee: [Abstract] Abstract and results sections: the reported algebraic tails and inflation-induced oscillations are presented without the exact parameter choices, statistical tests used to establish the power-law behavior, or quantitative measures of damping, rendering the fluctuation claims unverifiable from the given information.

Authors: We agree that the fluctuation results require supporting numerical and statistical detail for verification. The revision will report the precise parameter sets used for each simulation, the fitting procedure and goodness-of-fit tests applied to the algebraic tails, and quantitative damping metrics (e.g., exponential decay constants) for the inflation-expectation cases. revision: yes

-

Referee: [Input-output attempt] Input-output modeling paragraph: the statement that it is 'difficult to keep prices stable with the assumptions employed' is presented without the concrete modifications attempted or the resulting instability metrics, so the difficulty cannot be assessed as a general limitation versus a modeling choice.

Authors: The input-output section summarizes exploratory attempts that failed to maintain stability. To make the claim evaluable we will expand the paragraph to list the concrete modifications tested (e.g., changes to production coefficients or expectation rules) together with the quantitative instability measures obtained (price variance, divergence timescales). revision: yes

Circularity Check

No circularity: simulation outputs are independent of fitted inputs or self-citations

full rationale

The paper defines explicit utility models for actors, then runs forward simulations of double-auction markets to observe emergent behaviors (price stability, tails, oscillations). These are direct simulation results, not quantities fitted to data and then re-predicted, nor results that reduce by definition to the same inputs. No self-citations, uniqueness theorems, or ansatzes are invoked as load-bearing steps in the provided text. The derivation chain is therefore self-contained and non-circular.

Axiom & Free-Parameter Ledger

axioms (2)

- domain assumption Actors possess utility functions over bundles of goods that treat money solely as a medium of exchange with no direct consumption value.

- domain assumption Market clearing occurs through independent double auctions for each good.

Reference graph

Works this paper leans on

-

[1]

S-H Chen, ‘Econophysics: Bridges over a turbulent Cur- rent’, Int. Rev. of Financial Analysis,23, pp1-10 (2012)

work page 2012

-

[2]

Phillips, ‘Mechanical models in economic dynam- ics’,‘ Economica17(67), pp283-305 (1950)

A.W. Phillips, ‘Mechanical models in economic dynam- ics’,‘ Economica17(67), pp283-305 (1950)

work page 1950

-

[3]

J. Angle, ‘The surplus theory of social stratification and the size distribution of personal wealth’, Social Forces, 65(2), pp293-326 (1986)

work page 1986

-

[4]

A. Chakraborti and B. Chakrabarti, ‘Statistical mechan- ics of money: How saving propensity affects its distribu- tion’, The European Physical Journal B17pp167-170 (2000)

work page 2000

-

[5]

M. Mitzenmacher, ‘A brief history of generative mod- els for power law and lognormal dsirtbuitions’, Internet Mathematics1(2), pp226-251 (2008)

work page 2008

- [6]

-

[7]

W. Leontief,The Structure of the American Economy, 1919-1939: An Empirical Application of Equilibrium Analysis, Oxford University Press, 1951

work page 1919

-

[8]

W. Hildenbrand, ‘Random preferences and equilibrium analysis’, Journal of Economic Theory,3pp414-429 (1971)

work page 1971

-

[9]

Ising, ‘Beitrag zur Theorie des Ferromagnetismus’, Z

E. Ising, ‘Beitrag zur Theorie des Ferromagnetismus’, Z. Phys.,31(1), pp253–258 (1925)

work page 1925

-

[10]

H. Follmer, ‘Random economics with many interacting agents’, Journal of Mathematical Economics1(1), pp57- 62 (1974)

work page 1974

-

[11]

T. Veblen, ‘The Theory of the Leisure Class: An Eco- nomic Study of Institutions’, (1899) [Republished under Penguin Twentieth Century Classics, Penguin (1994)]

work page 1994

-

[12]

D. Challet, Y-C Zhang, ‘On the minority game: Analyt- ical and numerical studies’, Physica A,256(3-4), pp514- 532 (1998)

work page 1998

-

[13]

A. Cavagna, J.P. Garrahan, I. Giardina and D. Sher- 12 rington, ‘Thermal model for adaptive competition in a market’, Phys. Rev. Lett.,83(21), 4429 (1999)

work page 1999

-

[14]

J.P. Garrahan, E. Moro and D. Sherrington, ‘Continuous time dynamics of the thermal minority game’, Phys. Rev. E.62R9(R) (2000)

work page 2000

-

[15]

J. Burridge, Y. Gao and Y. Mao, ‘Forgetfulness can help you win games’, Phys. Rev. E92, 032119 (2015)

work page 2015

-

[16]

S. L¨ ubeck, ‘Universal scaling behaviour of non- equilibrium phase transitions’, International Journal of Modern Physics B,18(31-32), pp3977-4118 (2004)

work page 2004

-

[17]

J.M. Hammersley and D.J.A. Welsh, ‘Percolation the- ory and its ramifications’, Contemporary Physics,21(6) pp593-605 (1980)

work page 1980

-

[18]

C. J. Bullock,‘Economic Essays’, pp 502-519, Oxford University Press (1936)

work page 1936

-

[19]

R. Cantillon (author), M. Thornton (ed.) and C. Saucier (Translator),‘An essay on economic theory’, Ludwig von Misis Institute (2018), ISBN-13: 978-1610160018 [Origi- nally published 1775]

work page 2018

-

[20]

F. Michael and M.D. Johnson, ‘Financial market dynam- ics’, Physica A320, pp525-534 (2003)

work page 2003

-

[21]

J.C.L.Simonde De Sismondi,‘New principles of political economy’. Translator: Richard Hyse. ISBN 0-88738-336- X. (1991)

work page 1991

-

[22]

S. Benner,‘Benner’s Prophecies of Future Ups and Downs in Prices: What Years to Make Money on Pig- Iron, Hogs, Corn, and Provisions (Classic Reprint)’, For- gotten Books (London, 2018). ASIN : B008L1EL6E

work page 2018

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.