Stochastic LQ Optimal Control with Random Coefficients and a Terminal Mean-Field Cost

Pith reviewed 2026-06-29 15:53 UTC · model grok-4.3

The pith

Lagrangian duality and BSDE decomposition give sufficient conditions for solvability of stochastic LQ control with random coefficients and terminal mean-field cost.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The paper establishes two types of sufficient conditions for the solvability of the multidimensional non-homogeneous stochastic LQ optimal control problem with random coefficients and terminal mean-field cost by employing the Lagrangian duality method together with a decomposition approach for linear BSDEs, and derives the corresponding optimal controls. In the deterministic-coefficient case, the condition is weaker than the standard one in existing literature.

What carries the argument

Lagrangian duality method combined with decomposition approach for linear backward stochastic differential equations, producing well-posed Riccati-type equations or equivalent conditions.

If this is right

- Explicit optimal controls are obtained once the derived conditions are verified.

- The results apply directly to mean-variance portfolio selection models with multiple risky assets.

- More general random-coefficient problems become tractable compared with earlier mean-field LQ frameworks.

- Numerical verification is feasible for concrete multi-asset portfolio instances.

Where Pith is reading between the lines

- The same duality-plus-decomposition technique may extend to other linear-quadratic problems whose costs contain additional mean-field interactions at intermediate times.

- The weaker deterministic condition could be tested against known solvable examples to quantify the enlargement of the solvable set.

- The approach suggests a route for deriving closed-form solutions in related mean-variance problems with regime-switching coefficients.

Load-bearing premise

The Lagrangian duality method combined with the decomposition approach for linear BSDEs yields well-posed Riccati-type equations or equivalent conditions that guarantee existence of an optimal control.

What would settle it

A concrete instance of the deterministic-coefficient problem in which the paper's weaker condition holds yet the associated Riccati equations fail to be well-posed or no optimal control exists.

Figures

read the original abstract

This paper investigates a multidimensional non-homogeneous stochastic linear-quadratic optimal control problem featuring random coefficients and a terminal mean-field term in the cost functional, enabling its direct application to mean-variance models in financial engineering. Employing the Lagrangian duality method together with a decomposition approach for linear backward stochastic differential equations, we provide two types of sufficient conditions for solvability and derive the corresponding optimal controls. In particular, in the deterministic-coefficient case, our condition is weaker than the standard condition found in the existing literature on mean-field stochastic LQ problems. Finally, a numerical example drawn from optimal portfolio selection with multiple assets under mean-variance utility demonstrates the applicability of our results.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper studies a multidimensional non-homogeneous stochastic linear-quadratic optimal control problem with random coefficients and a terminal mean-field cost term. It employs the Lagrangian duality method combined with a decomposition approach for linear BSDEs to derive two types of sufficient conditions guaranteeing solvability, obtains the corresponding optimal controls, and claims that the condition is weaker than the standard one in the deterministic-coefficient case. Applicability is illustrated via a numerical mean-variance portfolio selection example with multiple assets.

Significance. If the sufficient conditions are rigorously justified and the derived Riccati equations are well-posed, the work would advance mean-field stochastic LQ control by accommodating random coefficients and providing a weaker solvability criterion than prior literature, with direct relevance to financial applications such as mean-variance optimization.

major comments (2)

- [Main theorems on sufficient conditions] The statements of the main solvability theorems (presumably in the section presenting the two types of sufficient conditions) do not list explicit integrability or regularity assumptions on the random coefficients that ensure the resulting Riccati-type equations are well-posed and that the duality gap vanishes. This leaves the existence claim unsecured precisely at the step where the Lagrangian duality + BSDE decomposition is applied to random coefficients.

- [Comparison with existing literature] The claim that the condition is weaker than the standard condition in the deterministic-coefficient case (stated in the abstract and presumably proved in the comparison subsection) requires an explicit side-by-side statement of the literature condition versus the new one, including the precise point at which the improvement occurs (e.g., a specific matrix inequality or terminal condition).

minor comments (2)

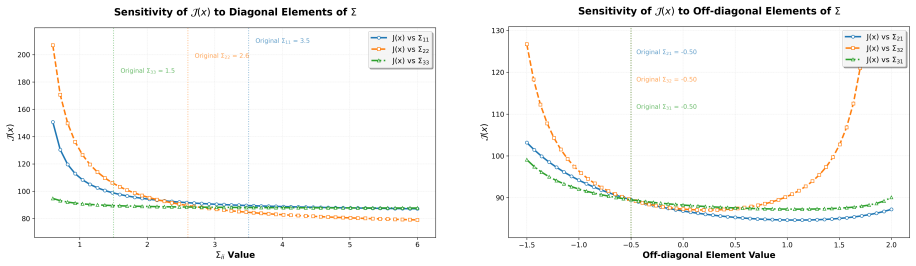

- [Numerical example] In the numerical portfolio example, the specific values of the random coefficients, the dimension, and the discretization scheme for the BSDEs should be stated explicitly to permit reproducibility.

- [Notation and definitions] Notation for the mean-field terminal cost term should be introduced once and used consistently; currently the abstract and main text appear to switch between equivalent but non-identical symbols.

Simulated Author's Rebuttal

We thank the referee for the careful reading and constructive comments on our manuscript. We respond to each major comment below and will revise the manuscript to address the points raised.

read point-by-point responses

-

Referee: [Main theorems on sufficient conditions] The statements of the main solvability theorems (presumably in the section presenting the two types of sufficient conditions) do not list explicit integrability or regularity assumptions on the random coefficients that ensure the resulting Riccati-type equations are well-posed and that the duality gap vanishes. This leaves the existence claim unsecured precisely at the step where the Lagrangian duality + BSDE decomposition is applied to random coefficients.

Authors: We agree that the integrability and regularity assumptions on the random coefficients must be stated explicitly in the main theorems to secure the well-posedness of the Riccati equations and the vanishing of the duality gap under the Lagrangian duality and BSDE decomposition approach. In the revised version we will insert these assumptions directly into the theorem statements, consistent with the conditions needed for the linear BSDE decomposition. revision: yes

-

Referee: [Comparison with existing literature] The claim that the condition is weaker than the standard condition in the deterministic-coefficient case (stated in the abstract and presumably proved in the comparison subsection) requires an explicit side-by-side statement of the literature condition versus the new one, including the precise point at which the improvement occurs (e.g., a specific matrix inequality or terminal condition).

Authors: We agree that an explicit side-by-side comparison is necessary for clarity. In the revision we will add a dedicated paragraph or table that quotes the standard condition from the literature and our condition, identifying the precise relaxation (for instance, a weaker terminal matrix inequality or a relaxed positivity requirement). revision: yes

Circularity Check

No significant circularity; derivation relies on external duality and BSDE methods without self-referential reduction

full rationale

The paper applies Lagrangian duality combined with linear BSDE decomposition to obtain sufficient conditions for solvability of the stochastic LQ problem with random coefficients and terminal mean-field cost. It explicitly compares its deterministic-coefficient condition to the existing literature (claiming it is weaker) rather than deriving it from self-citation or prior author results. No equations or steps are shown to reduce by construction to fitted parameters, self-defined quantities, or ansatzes imported via self-citation. The central existence claim is presented as following from the cited methods under (unspecified) regularity, which is a standard modeling assumption rather than a circular closure. This is the most common honest finding for a methods-driven control paper whose core argument does not collapse to renaming or fitting its own inputs.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

3, 419–444

Jean-Michel Bismut,Linear quadratic optimal stochastic control with random coefficients, SIAM Journal on Control and Optimization14(1976), no. 3, 419–444

1976

-

[2]

Uncertain

Yuyang Chen and Peng Luo,Non-homogeneous stochastic linear-quadratic optimal control prob- lems with multidimensional state and regime switching, Probab. Uncertain. Quant. Risk10 (2025), no. 1, 13–30

2025

-

[3]

Kai Ding, Xun Li, Siyu Lv, Zuo Quan Xu,Infinite horizon discounted LQ optimal control problems for mean-field switching diffusions, Systems and Control Letters204(2025), 106212

2025

-

[4]

6, 3673–3689

Kai Du,Solvability conditions for indefinite linear quadratic optimal stochastic control prob- lems and associated stochastic riccati equations, SIAM Journal on Control and Optimization53 (2015), no. 6, 3673–3689

2015

-

[5]

1, 426– 460

Ying Hu, Xiaomin Shi, and Zuo Quan Xu,Constrained stochastic lq control with regime switching and application to portfolio selection, The Annals of Applied Probability32(2022), no. 1, 426– 460

2022

-

[6]

Control Relat

Ying Hu, Xiaomin Shi, and Zuo Quan Xu,Non-homogeneous stochastic LQ control with regime switching and random coefficients, Math. Control Relat. Fields14(2024), no. 2, 671–694

2024

-

[7]

2, 255–288

Michael Kohlmann and Shanjian Tang,Global adapted solution of one-dimensional backward stochastic riccati equations, with application to the mean–variance hedging, Stochastic Processes and their Applications97(2002), no. 2, 255–288

2002

-

[8]

Control Optim.42(2003), no

Michael Kohlmann and Shanjian Tang,Minimization of risk and linear quadratic optimal control theory, SIAM J. Control Optim.42(2003), no. 3, 1118–1142

2003

-

[9]

5, 1392–1407

Michael Kohlmann and Xun Yu Zhou,Relationship between backward stochastic differential equations and stochastic controls: a linear-quadratic approach, SIAM Journal on Control and Optimization38(2000), no. 5, 1392–1407

2000

-

[10]

5, 1540–1555

Xun Li, Xun Yu Zhou, and Andrew EB Lim,Dynamic mean-variance portfolio selection with no-shorting constraints, SIAM Journal on Control and Optimization40(2002), no. 5, 1540–1555

2002

-

[11]

1, 101–120

Andrew EB Lim and Xun Yu Zhou,Mean-variance portfolio selection with random parameters in a complete market, Mathematics of Operations Research27(2002), no. 1, 101–120

2002

-

[12]

David G Luenberger,Optimization by vector space methods, John Wiley & Sons, 1997

1997

-

[13]

11, 77–91

Harry Markowitz,Modern portfolio theory, Journal of Finance7(1952), no. 11, 77–91

1952

-

[14]

Algebra Control Optim.14(2024), no

Hongwei Mei, Qingmeng Wei, and Jiongmin Yong,Linear-quadratic optimal control problem for mean-field stochastic differential equations with a type of random coefficients, Numer. Algebra Control Optim.14(2024), no. 4, 813–852

2024

-

[15]

Huyˆ en Pham,Linear quadratic optimal control of conditional mckean-vlasov equation with ran- dom coefficients and applications, Probability, Uncertainty and Quantitative Risk1(2016), no. 1, 7

2016

-

[16]

1, 221–229

Zhongmin Qian and Xun Yu Zhou,Existence of solutions to a class of indefinite stochastic riccati equations, SIAM journal on Control and Optimization51(2013), no. 1, 221–229. 21

2013

-

[17]

3, 1099–1127

Jingrui Sun,Mean-field stochastic linear quadratic optimal control problems: open-loop solvabil- ities, ESAIM: Control, Optimisation and Calculus of Variations23(2017), no. 3, 1099–1127

2017

-

[18]

Jingrui Sun, Jie Xiong, and Jiongmin Yong,Indefinite stochastic linear-quadratic optimal control problems with random coefficients: closed-loop representation of open-loop optimal controls, Ann. Appl. Probab.31(2021), no. 1, 460–499

2021

-

[19]

Control Optim.42(2003), no

Shanjian Tang,General linear quadratic optimal stochastic control problems with random coef- ficients: linear stochastic Hamilton systems and backward stochastic Riccati equations, SIAM J. Control Optim.42(2003), no. 1, 53–75

2003

-

[20]

Control Optim.53(2015), no

Shanjian Tang,Dynamic programming for general linear quadratic optimal stochastic control with random coefficients, SIAM J. Control Optim.53(2015), no. 2, 1082–1106

2015

-

[21]

Control Optim.61(2023), 22–46

Ran Tian and Zhiyong Yu,Mean-field type FBSDEs under domination-monotonicity conditions and application to LQ problems, SIAM J. Control Optim.61(2023), 22–46

2023

-

[22]

4, 681–697

William M Wonham,On a matrix riccati equation of stochastic control, SIAM Journal on Control 6(1968), no. 4, 681–697

1968

- [23]

-

[24]

4, 3042–3060

Jie Xiong, and Wen Xu,Mean-field stochastic linear quadratic control problem with random coefficients, SIAM Journal on Control63(2025), no. 4, 3042–3060

2025

-

[25]

4, 2809–2838

Jiongmin Yong,Linear-quadratic optimal control problems for mean-field stochastic differential equations, SIAM journal on Control and Optimization51(2013), no. 4, 2809–2838

2013

-

[26]

Jiongmin Yong,Linear-quadratic optimal control problems for mean-field stochastic differential equations — time-consistent solutions, Trans. Amer. Math. Soc.,369(2017), 5467–5523

2017

-

[27]

Haisen Zhang and Xianfeng Zhang,Stochastic linear quadratic optimal control problems with expectation-type linear equality constraints on the terminal states, Systems & Control Letters 177(2023), 105551

2023

-

[28]

Haisen Zhang and Xianfeng Zhang,Lagrangian dual method for solving stochastic linear quadratic optimal control problems with terminal state constraints, ESAIM: Control, Optimi- sation and Calculus of Variations30(2024), 22

2024

-

[29]

Xun Yu Zhou and Duan Li,Continuous-time mean-variance portfolio selection: A stochastic lq framework, Applied Mathematics and Optimization42(2000), 19–33. 22

2000

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.