Conformal Prediction Intervals with Tail-Specific Guarantees

Pith reviewed 2026-06-26 21:44 UTC · model grok-4.3

The pith

Conformal prediction intervals can be built to guarantee calibrated coverage separately in the upper and lower tails while preserving global marginal coverage.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

By taking the intersection of a lower one-sided conformal interval and an upper one-sided conformal interval, each constructed to achieve its own marginal coverage, the resulting two-sided interval inherits explicit tail-specific coverage guarantees together with the global marginal coverage of 1 minus alpha. Finite-sample validity holds under exchangeability; asymptotic validity holds for non-exchangeable sequences.

What carries the argument

Intersection of one-sided conformal intervals that each achieve marginal coverage.

If this is right

- The two-sided interval maintains coverage of at least 1-alpha globally while also covering the lower tail and upper tail at their respective calibrated levels.

- Finite-sample tail-specific guarantees apply whenever the data are exchangeable.

- Asymptotic tail-specific guarantees apply to non-exchangeable data sequences.

- Directional calibration improves on skewed distributions relative to classical two-sided conformal intervals.

- The construction supports applications that require asymmetric tail control, such as financial return maximization with left-tail risk limits.

Where Pith is reading between the lines

- The same intersection construction could be applied to other conformal methods that produce one-sided intervals.

- In settings with strong dependence, the asymptotic results may still require verification on the specific dependence structure.

- When tail costs are highly asymmetric, the separate calibration allows explicit trade-offs between upper and lower coverage levels that standard intervals do not expose.

- The method extends naturally to multivariate responses if one-sided conformal bounds can be defined coordinate-wise.

Load-bearing premise

The building-block one-sided conformal intervals achieve their claimed marginal coverage.

What would settle it

An exchangeable dataset in which the empirical frequency that observations fall below the lower endpoint of the two-sided interval is strictly less than the claimed tail level, while the one-sided lower interval itself meets its marginal guarantee.

Figures

read the original abstract

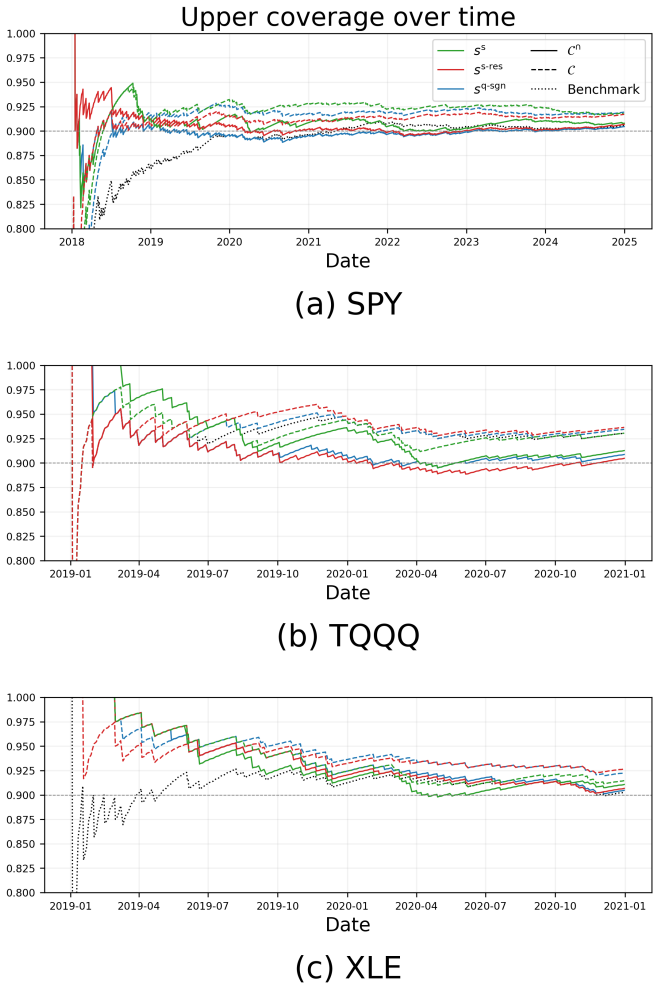

This paper extends classical conformal frameworks for constructing prediction intervals with global marginal coverage $1-\alpha$ to intervals that provide explicitly calibrated guarantees for the upper and lower tails separately. Focusing on split conformal prediction, we first construct lower and upper one-sided conformal intervals that achieve marginal validity, and then derive the induced two-sided interval by intersection. Theoretical results prove both tail-specific and global marginal coverage of the induced two-sided interval. Results are presented first for the exchangeable setting, where coverage has finite-sample guarantees, and then for non-exchangeable data, where guarantees are asymptotic. Simulation studies show that the proposed approach achieves improved directional calibration relative to classical two-sided intervals, especially relevant in skewed data. Finally, the benefit of the proposed framework is showcased in a financial application, where one aims for return maximization while seeking strict control on the left tail.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper extends split conformal prediction to construct two-sided intervals that deliver explicit marginal coverage guarantees separately for the lower tail (P(Y < L) ≤ α) and upper tail (P(Y > U) ≤ α), in addition to the usual global coverage ≥ 1−2α. One-sided split conformal intervals are built as building blocks and the two-sided interval is obtained by their intersection. Finite-sample validity is claimed under exchangeability; asymptotic validity is claimed for non-exchangeable data under standard regularity conditions. Simulations are reported to show improved directional calibration versus classical two-sided conformal intervals (especially on skewed data), and a financial application is presented for return maximization with left-tail control.

Significance. If the derivations hold, the contribution supplies a simple, assumption-light way to obtain tail-specific control within the conformal framework. This is practically relevant for risk-sensitive domains such as finance. The finite-sample guarantees under exchangeability and the explicit use of the union-bound argument for global coverage are clear strengths; the simulation evidence on skewed distributions further supports utility. The approach does not introduce new free parameters or invented entities beyond standard conformal machinery.

minor comments (1)

- The abstract states that the two-sided interval is formed by intersection of one-sided intervals; a brief explicit statement of the resulting coverage statements (e.g., via union bound) in the main text would improve readability for readers unfamiliar with the construction.

Simulated Author's Rebuttal

We thank the referee for their positive summary, significance assessment, and recommendation to accept the manuscript. No major comments were raised, so we have no points to address.

Circularity Check

No significant circularity identified

full rationale

The derivation begins from the established finite-sample marginal coverage property of one-sided split conformal intervals under exchangeability (a standard result independent of this paper) and forms the two-sided interval by intersection. Tail-specific bounds and the global coverage guarantee then follow directly from the one-sided properties via the union bound, without any redefinition, parameter fitting presented as prediction, or load-bearing self-citation. The asymptotic non-exchangeable extension likewise invokes only routine regularity conditions from the conformal literature. All steps are self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption Data points are exchangeable (any permutation equally likely) for finite-sample coverage guarantees

Reference graph

Works this paper leans on

-

[1]

The Annals of Statistics , volume=

Conformal prediction beyond exchangeability , author=. The Annals of Statistics , volume=. 2023 , publisher=

2023

-

[2]

Journal of the American Statistical Association , volume=

Distribution-free prediction intervals under covariate shift, with an application to causal inference , author=. Journal of the American Statistical Association , volume=. 2025 , publisher=

2025

-

[3]

Journal of Banking & Finance , volume=

Beyond Sharpe ratio: Optimal asset allocation using different performance ratios , author=. Journal of Banking & Finance , volume=. 2008 , publisher=

2008

-

[4]

Information and Inference: A Journal of the IMA , volume=

The limits of distribution-free conditional predictive inference , author=. Information and Inference: A Journal of the IMA , volume=. 2021 , publisher=

2021

-

[5]

Journal of Banking & Finance , volume=

Two-sided coherent risk measures and their application in realistic portfolio optimization , author=. Journal of Banking & Finance , volume=. 2008 , publisher=

2008

-

[6]

2015 , publisher=

Quantitative risk management: concepts, techniques and tools-revised edition , author=. 2015 , publisher=

2015

-

[7]

Biometrics , volume=

Dose-finding based on efficacy--toxicity trade-offs , author=. Biometrics , volume=

-

[8]

The American Statistician , volume=

Computing and graphing highest density regions , author=. The American Statistician , volume=. 1996 , publisher=

1996

-

[9]

International Statistical Review , year=

Alternative Approaches for Estimating Highest-Density Regions , author=. International Statistical Review , year=

-

[10]

Vovk, Vladimir and Gammerman, Alexander and Shafer, Glenn , year=

-

[11]

Journal of the Royal Statistical Society Series B: Statistical Methodology , volume=

Distribution-free prediction bands for non-parametric regression , author=. Journal of the Royal Statistical Society Series B: Statistical Methodology , volume=. 2014 , publisher=

2014

-

[12]

Journal of the American Statistical Association , volume=

Distribution-free predictive inference for regression , author=. Journal of the American Statistical Association , volume=. 2018 , publisher=

2018

-

[13]

Fong, Edwin and Holmes, Chris C , booktitle =

-

[14]

Bernoulli , number =

Peter Hoff , title =. Bernoulli , number =. 2023 , doi =

2023

-

[15]

Bersson, Elizabeth and Hoff, Peter D , title =. 2024 , month =. doi:10.1093/jssam/smae010 , url =

-

[16]

Conformalized quantile regression , author=

-

[17]

Classification with valid and adaptive coverage , author=

-

[18]

Box, George E. P. and Tiao, George C. , year =. Bayesian inference in statistical analysis , isbn =

-

[19]

Journal of Multivariate Analysis , volume=

An optimum tolerance region for multivariate regression , author=. Journal of Multivariate Analysis , volume=. 1980 , publisher=

1980

-

[20]

Journal of the American Statistical Association , volume=

A method of obtaining prediction intervals , author=. Journal of the American Statistical Association , volume=. 1973 , publisher=

1973

-

[21]

2004 , publisher=

Monte Carlo statistical methods , author=. 2004 , publisher=

2004

-

[22]

The Annals of Statistics , volume=

Predictive inference with the jackknife+ , author=. The Annals of Statistics , volume=. 2021 , publisher=

2021

-

[23]

Annals of Mathematics and Artificial Intelligence , volume=

Cross-conformal predictors , author=. Annals of Mathematics and Artificial Intelligence , volume=. 2015 , publisher=

2015

-

[24]

Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics , pages =

Flexible distribution-free conditional predictive bands using density estimators , author =. Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics , pages =. 2020 , editor =

2020

-

[25]

Izbicki, Rafael and Shimizu, Gilson and Stern, Rafael B , journal=

-

[26]

2009 International Conference on Machine Learning and Applications , pages=

Conditional prediction intervals for linear regression , author=. 2009 International Conference on Machine Learning and Applications , pages=. 2009 , organization=

2009

-

[27]

Journal of the American Statistical Association , volume =

Peter Hoff , title =. Journal of the American Statistical Association , volume =. 2022 , publisher =

2022

-

[28]

Ignatiadis, Nikolaos and Sen, Bodhisattva , journal =

-

[29]

1980 , publisher=

Diaconis, Persi and Freedman, David , journal=. 1980 , publisher=

1980

-

[30]

1938 , organization=

de Finetti, Bruno , booktitle=. 1938 , organization=

1938

-

[31]

Journal of Official Statistics , volume=

Machine Learning Methods for Estimation in Official Statistics , author=. Journal of Official Statistics , volume=. 2025 , publisher=

2025

-

[32]

2015 , publisher=

Small area estimation , author=. 2015 , publisher=

2015

-

[33]

Datta, Jyotishka and Polson, Nicholas G and Sokolov, Vadim and Zantedeschi, Daniel , journal=

-

[34]

2001 , publisher=

In all likelihood: statistical modelling and inference using likelihood , author=. 2001 , publisher=

2001

-

[35]

Science , volume=

Prediction-powered inference , author=. Science , volume=. 2023 , publisher=

2023

-

[36]

Electronic Journal of Statistics , volume=

Distribution-free conditional median inference , author=. Electronic Journal of Statistics , volume=. 2021 , publisher=

2021

-

[37]

Electronic Journal of Statistics , volume =

Barber, Rina Foygel , title =. Electronic Journal of Statistics , volume =. 2020 , doi =

2020

-

[38]

Journal of Machine Learning Research , year =

Aki Vehtari and Daniel Simpson and Andrew Gelman and Yuling Yao and Jonah Gabry , title =. Journal of Machine Learning Research , year =

-

[39]

Proceedings of the 39th International Conference on Machine Learning , series=

Adaptive Conformal Predictions for Time Series , author=. Proceedings of the 39th International Conference on Machine Learning , series=. 2022 , publisher=

2022

-

[40]

2015 , publisher=

Causal inference in statistics, social, and biomedical sciences , author=. 2015 , publisher=

2015

-

[41]

and Petrie, Ted , title =

Baum, Leonard E. and Petrie, Ted , title =. Annals of Mathematical Statistics , volume =

-

[42]

Machine Learning , volume=

Finite-time analysis of the multiarmed bandit problem , author=. Machine Learning , volume=. 2002 , publisher=

2002

-

[43]

The Annals of Applied Statistics , author =

Learn then test:. The Annals of Applied Statistics , author =

-

[44]

Hirshberg and Ruohan Zhan and Stefan Wager and Susan Athey , title =

Vitor Hadad and David A. Hirshberg and Ruohan Zhan and Stefan Wager and Susan Athey , title =. Proceedings of the National Academy of Sciences , volume =

-

[45]

2021 , publisher =

Gareth James and Daniela Witten and Trevor Hastie and Robert Tibshirani , title =. 2021 , publisher =

2021

-

[46]

Advances in Neural Information Processing Systems , volume=

Adaptive conformal inference under distribution shift , author=. Advances in Neural Information Processing Systems , volume=

-

[47]

International Conference on Artificial Intelligence and Statistics , pages=

Nonstationary bandit learning via predictive sampling , author=. International Conference on Artificial Intelligence and Statistics , pages=. 2023 , organization=

2023

-

[48]

International Conference on Artificial Intelligence and Statistics , pages=

Bandit algorithms: Letting go of logarithmic regret for statistical robustness , author=. International Conference on Artificial Intelligence and Statistics , pages=. 2021 , organization=

2021

-

[49]

Biometrics , volume=

On the finite-sample and asymptotic error control of a randomization-probability test for response-adaptive clinical trials , author=. Biometrics , volume=. 2025 , publisher=

2025

-

[50]

European Journal of Operational Research , volume=

The multi-armed bandit problem under the mean-variance setting , author=. European Journal of Operational Research , volume=. 2025 , publisher=

2025

-

[51]

The Thirty-ninth Annual Conference on Neural Information Processing Systems , year =

Martingale Posterior Neural Networks for Fast Sequential Decision Making , author=. The Thirty-ninth Annual Conference on Neural Information Processing Systems , year =

-

[52]

Nina Deliu and Brunero Liseo , year=

-

[53]

Bernoulli , volume=

Conformal prediction: a unified review of theory and new challenges , author=. Bernoulli , volume=. 2023 , publisher=

2023

-

[54]

arXiv preprint arXiv:2511.13608 , year=

A Gentle Introduction to Conformal Time Series Forecasting , author=. arXiv preprint arXiv:2511.13608 , year=

-

[55]

2024 , journal =

Optimal Resource Allocation Using Multi-Armed Bandits , author=. 2024 , journal =

2024

-

[56]

2005 , publisher=

Quantile regression , author=. 2005 , publisher=

2005

-

[57]

Statistical Methods in Medical Research , volume=

A note on response-adaptive randomization from a Bayesian prediction viewpoint , author=. Statistical Methods in Medical Research , volume=. 2025 , publisher=

2025

-

[58]

SIAM journal on computing , volume=

The nonstochastic multiarmed bandit problem , author=. SIAM journal on computing , volume=

-

[59]

A. P. Dempster and N. M. Laird and D. B. Rubin , title =. Journal of the Royal Statistical Society: Series B (Methodological) , volume =

-

[60]

MacDonald and Roland Langrock , title =

Walter Zucchini and Iain L. MacDonald and Roland Langrock , title =. 2016 , publisher =

2016

-

[61]

Bacon , title =

Carl R. Bacon , title =. 2022 , publisher =

2022

-

[62]

Royal Society Open Science , year =

Xiaoguang Huo and Feng Fu , title =. Royal Society Open Science , year =

-

[63]

Journal of Machine Learning Research , volume =

Conformal Inference for Online Prediction with Arbitrary Distribution Shifts , author =. Journal of Machine Learning Research , volume =

-

[64]

arXiv preprint , year =

Temporal Conformal Prediction (TCP): A Distribution-Free Statistical and Machine Learning Framework for Adaptive Risk Forecasting , author =. arXiv preprint , year =

-

[65]

Journal of Risk and Financial Management , volume =

Reliable Value at Risk Estimations with Conformal Prediction , author =. Journal of Risk and Financial Management , volume =. 2022 , publisher =

2022

-

[66]

Journal of Risk and Financial Management , volume =

Adaptive Conformal Inference for Computing Market Risk Measures: An Analysis with Four Thousand Crypto-Assets , author =. Journal of Risk and Financial Management , volume =. 2023 , publisher =

2023

-

[67]

The Journal of Derivatives , volume =

Techniques for Verifying the Accuracy of Risk Measurement Models , author =. The Journal of Derivatives , volume =

-

[68]

International Economic Review , volume =

Evaluating Interval Forecasts , author =. International Economic Review , volume =

-

[69]

and Barber, Rina Foygel and Cand\`

Tibshirani, Ryan J. and Barber, Rina Foygel and Cand\`. Conformal prediction under covariate shift , journal=

-

[70]

Taming Tail Risk in Financial Markets: Conformal Risk Control for Nonstationary Portfolio VaR , author=. arXiv:2602.03903 , year=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.