OpenFinGym: A Verifiable Multi-Task Gym Environment for Evaluating Quant Agents

Pith reviewed 2026-06-26 01:27 UTC · model grok-4.3

The pith

OpenFinGym unifies forecasting, market generation, trading and fraud detection into one verifiable gym environment for quant agents.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

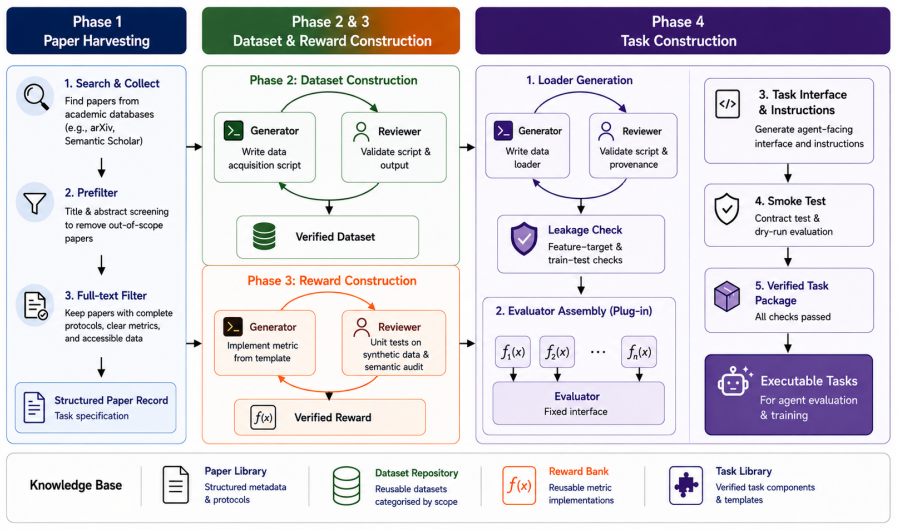

We introduce OpenFinGym, a unified gym environment for quantitative-finance agent development that covers forecasting, market generation, real-time trading, and fraud detection under a single execution and verification interface. OpenFinGym additionally provides an automated task-construction pipeline that turns quantitative finance publications into executable task packages; a containerised runtime with a host-side verifier service that supports scalable agent rollouts and prevents runtime train-test leakage; a paper trading engine with a low-latency data-stream design; deferred-resolution support for long-horizon and event-market forecasts; and integration for SFT and RL post-training.

What carries the argument

OpenFinGym, the unified gym environment with automated task-construction pipeline, containerised runtime, and host-side verifier service that executes and verifies multiple interdependent tasks together.

If this is right

- Agents can be assessed across the full sequence from forecast to execution without switching environments, exposing gaps in generalization.

- Weaknesses in real-market interaction and financially meaningful decision-making become measurable rather than hidden by task isolation.

- Publications can be turned automatically into new verifiable tasks, expanding the set of benchmarks over time.

- Scalable rollouts remain possible while the verifier blocks runtime leakage between training and test data.

Where Pith is reading between the lines

- Teams building finance agents may shift focus from single-metric optimization toward agents that maintain consistency across chained tasks.

- The containerised verifier pattern could be adopted for secure multi-step evaluation in other applied domains such as robotics or code generation.

- Deferred-resolution features for event markets suggest the environment can handle delayed-outcome forecasts that current single-task setups rarely test.

Load-bearing premise

The automated task-construction pipeline and single execution/verification interface can faithfully represent interdependent multi-stage financial workflows without introducing simplifications or biases that affect agent evaluation.

What would settle it

A side-by-side test in which agents achieve comparable generalization scores and success rates on OpenFinGym as they do on existing single-task platforms, or concrete evidence that the verifier permits detectable train-test leakage.

Figures

read the original abstract

Although large language model agents are increasingly applied to quantitative-finance workflows, their evaluation remains fragmented across isolated tasks, while the financial relevance of benchmark tasks is often overlooked. Yet financial workflows are inherently multi-stage, spanning interdependent tasks such as forecasting, strategy construction, risk management, and trading. Existing platforms typically focus on a single task, and can therefore overstate agent competence and fail to reveal weaknesses in generalization, real-market interaction, and financially meaningful decision-making. We introduce OpenFinGym, a unified gym environment for quantitative-finance agent development that covers forecasting, market generation, real-time trading, and fraud detection under a single execution and verification interface. OpenFinGym additionally provides an automated task-construction pipeline that turns quantitative finance publications into executable task packages; a containerised runtime with a host-side verifier service that supports scalable agent rollouts and prevents runtime train-test leakage; a paper trading engine with a low-latency data-stream design; deferred-resolution support for long-horizon and event-market forecasts; and integration for SFT and RL post-training

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper introduces OpenFinGym, a unified Gym environment for quantitative-finance agent development that integrates forecasting, market generation, real-time trading, and fraud detection under a single execution and verification interface. It additionally provides an automated pipeline to convert quantitative finance publications into executable tasks, a containerized runtime with a host-side verifier to support scalable rollouts and prevent train-test leakage, a paper trading engine with low-latency data streams, deferred-resolution support for long-horizon forecasts, and integration for SFT and RL post-training.

Significance. If the implementation faithfully delivers on multi-stage workflow representation and leakage prevention without introducing simplifications that bias agent evaluation, the environment could meaningfully advance standardized, financially relevant benchmarking for LLM agents in quant finance by exposing generalization failures that single-task platforms obscure. The automated publication-to-task pipeline and verifiable runtime are engineering strengths that, if validated, would support reproducible agent assessment.

major comments (1)

- [Abstract] Abstract: the central claims rest on the automated task-construction pipeline and verifier service faithfully representing interdependent financial workflows and preventing leakage, yet the provided manuscript text contains no implementation details, validation experiments, ablation studies, or empirical evidence demonstrating these properties. This leaves the weakest assumption untested and prevents assessment of whether the multi-task design actually reveals weaknesses in generalization or real-market interaction.

Simulated Author's Rebuttal

We thank the referee for their review and for highlighting the need for concrete evidence supporting the core claims. We address the single major comment below.

read point-by-point responses

-

Referee: [Abstract] Abstract: the central claims rest on the automated task-construction pipeline and verifier service faithfully representing interdependent financial workflows and preventing leakage, yet the provided manuscript text contains no implementation details, validation experiments, ablation studies, or empirical evidence demonstrating these properties. This leaves the weakest assumption untested and prevents assessment of whether the multi-task design actually reveals weaknesses in generalization or real-market interaction.

Authors: We agree that the current manuscript provides insufficient implementation details and empirical validation for the automated task-construction pipeline and host-side verifier. The abstract and design overview alone do not allow readers to evaluate leakage prevention or workflow fidelity. In the revised manuscript we will add a new section (approximately 1.5 pages) that (i) specifies the pipeline's publication-parsing rules, container packaging format, and verification steps, (ii) describes the verifier's runtime isolation and train-test separation mechanisms, and (iii) reports preliminary validation results including leakage-detection tests on held-out publications and rollout latency measurements. These additions will directly address the concern about untested assumptions. revision: yes

Circularity Check

No significant circularity; engineering contribution with no derivation chain

full rationale

The paper presents OpenFinGym as a software platform and automated pipeline for multi-task quant-finance agent evaluation. The provided abstract and description contain no equations, predictions, fitted parameters, or claimed first-principles derivations. No load-bearing steps exist that could reduce to self-definition, fitted inputs, or self-citation chains. The contribution is an engineering artifact whose value rests on implementation and interface design rather than any mathematical reduction to its own inputs.

Axiom & Free-Parameter Ledger

Reference graph

Works this paper leans on

-

[1]

Aho and Jeffrey D

Alfred V. Aho and Jeffrey D. Ullman , title =. 1972

1972

-

[2]

TimeSeriesGym: A Scalable Benchmark for (Time Series) Machine Learning Engineering Agents , year =

Yifu Cai and Xinyu Li and Mononito Goswami and Micha. TimeSeriesGym: A Scalable Benchmark for (Time Series) Machine Learning Engineering Agents , year =. 2505.13291 , archivePrefix =

-

[3]

2025 , eprint =

Lingfei Qian and Xueqing Peng and Yan Wang and Vincent Jim Zhang and Huan He and Hanley Smith and Yi Han and Yueru He and Haohang Li and Yupeng Cao and Yangyang Yu and Alejandro Lopez-Lira and Peng Lu and Jian-Yun Nie and Guojun Xiong and Jimin Huang and Sophia Ananiadou , title =. 2025 , eprint =

2025

-

[4]

2025 , eprint =

Yanxu Chen and Zijun Yao and Yantao Liu and Jin Ye and Jianing Yu and Lei Hou and Juanzi Li , title =. 2025 , eprint =

2025

-

[5]

2025 , eprint =

Haofei Yu and Fenghai Li and Jiaxuan You , title =. 2025 , eprint =

2025

-

[6]

2026 , eprint =

Mostapha Benhenda , title =. 2026 , eprint =

2026

-

[7]

2025 , eprint =

Xiangyu Li and Yawen Zeng and Xiaofen Xing and Jin Xu and Xiangmin Xu , title =. 2025 , eprint =

2025

-

[8]

arXiv preprint arXiv:2604.18292 , year=

Agent-world: Scaling real-world environment synthesis for evolving general agent intelligence , author=. arXiv preprint arXiv:2604.18292 , year=

-

[9]

arXiv preprint arXiv:2601.16344 , year=

DSGym: A Holistic Framework for Evaluating and Training Data Science Agents , author=. arXiv preprint arXiv:2601.16344 , year=

-

[10]

Advances in Neural Information Processing Systems , volume=

FinRL-Meta: Market environments and benchmarks for data-driven financial reinforcement learning , author=. Advances in Neural Information Processing Systems , volume=

-

[11]

arXiv preprint arXiv:2009.11189 , year=

Qlib: An ai-oriented quantitative investment platform , author=. arXiv preprint arXiv:2009.11189 , year=

arXiv 2009

-

[12]

Proceedings of the Second ACM International Conference on AI in Finance , pages=

ABIDES-gym: gym environments for multi-agent discrete event simulation and application to financial markets , author=. Proceedings of the Second ACM International Conference on AI in Finance , pages=

-

[13]

Advances in Neural Information Processing Systems , volume=

TradeMaster: a holistic quantitative trading platform empowered by reinforcement learning , author=. Advances in Neural Information Processing Systems , volume=

-

[14]

Publications Manual , year = "1983", publisher =

1983

-

[15]

Ashok K. Chandra and Dexter C. Kozen and Larry J. Stockmeyer , year = "1981", title =. doi:10.1145/322234.322243

-

[16]

Scalable training of

Andrew, Galen and Gao, Jianfeng , booktitle=. Scalable training of

-

[17]

Dan Gusfield , title =. 1997

1997

-

[18]

Tetreault , title =

Mohammad Sadegh Rasooli and Joel R. Tetreault , title =. Computing Research Repository , volume =. 2015 , url =

2015

-

[19]

A Framework for Learning Predictive Structures from Multiple Tasks and Unlabeled Data , Volume =

Ando, Rie Kubota and Zhang, Tong , Issn =. A Framework for Learning Predictive Structures from Multiple Tasks and Unlabeled Data , Volume =. Journal of Machine Learning Research , Month = dec, Numpages =

-

[20]

The Review of Financial Studies , volume=

Empirical asset pricing via machine learning , author=. The Review of Financial Studies , volume=. 2020 , publisher=

2020

-

[21]

Proceedings of the 6th ACM International Conference on AI in Finance , pages=

Structured agentic workflows for financial time-series modelling with llms and reflective feedback , author=. Proceedings of the 6th ACM International Conference on AI in Finance , pages=

-

[22]

arXiv preprint arXiv:2410.16858 , year=

Dynamic graph neural networks for enhanced volatility prediction in financial markets , author=. arXiv preprint arXiv:2410.16858 , year=

-

[23]

arXiv preprint arXiv:2406.02604 , year=

Gated recurrent neural network with TPE Bayesian optimization for enhancing stock index prediction accuracy , author=. arXiv preprint arXiv:2406.02604 , year=

-

[24]

arXiv preprint arXiv:2511.18578 , year=

Re (Visiting) Time Series Foundation Models in Finance , author=. arXiv preprint arXiv:2511.18578 , year=

-

[25]

ASTIN Bulletin: The Journal of the IAA , volume=

Multiple yield curve modeling and forecasting using deep learning , author=. ASTIN Bulletin: The Journal of the IAA , volume=. 2024 , publisher=

2024

-

[26]

Advances in Neural Information Processing Systems , volume=

High rank path development: an approach to learning the filtration of stochastic processes , author=. Advances in Neural Information Processing Systems , volume=

-

[27]

Advances in Neural Information Processing Systems , volume=

PCF-GAN: generating sequential data via the characteristic function of measures on the path space , author=. Advances in Neural Information Processing Systems , volume=

-

[28]

Management Science , volume=

Tail-gan: Learning to simulate tail risk scenarios , author=. Management Science , volume=. 2026 , publisher=

2026

-

[29]

Advances in neural information processing systems , volume=

Time-series generative adversarial networks , author=. Advances in neural information processing systems , volume=

-

[30]

Bao, Yifan and Xi, Xinyu and Liu, Xinyu and Ge, Wen and Jiang, Lei and Zhang, Kevin and Khraishi, Raad and Ang, Yihao and Tung, Anthony KH and Szpruch, Lukasz and Hao Ni , journal=

-

[31]

International journal of forecasting , volume=

Another look at measures of forecast accuracy , author=. International journal of forecasting , volume=. 2006 , publisher=

2006

-

[32]

Journal of Business & Economic Statistics , volume=

Comparing predictive accuracy , author=. Journal of Business & Economic Statistics , volume=. 1995 , publisher=

1995

-

[33]

1986 , publisher=

A simple, positive semi-definite, heteroskedasticity and autocorrelationconsistent covariance matrix , author=. 1986 , publisher=

1986

-

[34]

The Journal of business , volume=

Mutual fund performance , author=. The Journal of business , volume=. 1966 , publisher=

1966

-

[35]

1995 , publisher=

Techniques for verifying the accuracy of risk measurement models , author=. 1995 , publisher=

1995

-

[36]

Mathematical finance , volume=

Coherent measures of risk , author=. Mathematical finance , volume=. 1999 , publisher=

1999

-

[37]

IEEE transactions on neural networks , volume=

Lower upper bound estimation method for construction of neural network-based prediction intervals , author=. IEEE transactions on neural networks , volume=. 2010 , publisher=

2010

-

[38]

International Journal of forecasting , volume=

Better to give than to receive: Predictive directional measurement of volatility spillovers , author=. International Journal of forecasting , volume=. 2012 , publisher=

2012

-

[39]

Journal of Machine Learning Research , volume=

Signature moments to characterize laws of stochastic processes , author=. Journal of Machine Learning Research , volume=

-

[40]

arXiv preprint arXiv:1706.02633 , year=

Real-valued (medical) time series generation with recurrent conditional gans , author=. arXiv preprint arXiv:1706.02633 , year=

-

[41]

arXiv preprint arXiv:2306.05443 , year=

Pixiu: A large language model, instruction data and evaluation benchmark for finance , author=. arXiv preprint arXiv:2306.05443 , year=

-

[42]

Advances in Neural Information Processing Systems , volume=

Finben: A holistic financial benchmark for large language models , author=. Advances in Neural Information Processing Systems , volume=

-

[43]

arXiv preprint arXiv:2311.11944 , year=

Financebench: A new benchmark for financial question answering , author=. arXiv preprint arXiv:2311.11944 , year=

-

[44]

arXiv preprint arXiv:2304.07619 , year=

Can chatgpt forecast stock price movements? return predictability and large language models , author=. arXiv preprint arXiv:2304.07619 , year=

-

[45]

arXiv preprint arXiv:2404.18824 , year=

Benchmarking benchmark leakage in large language models , author=. arXiv preprint arXiv:2404.18824 , year=

-

[46]

Conference on Empirical Methods in Natural Language Processing , year=

NLP Evaluation in trouble: On the Need to Measure LLM Data Contamination for each Benchmark , author=. Conference on Empirical Methods in Natural Language Processing , year=

-

[47]

International Conference on Learning Representations , volume=

Swe-bench: Can language models resolve real-world github issues? , author=. International Conference on Learning Representations , volume=

-

[48]

International Conference on Learning Representations , volume=

Gaia: a benchmark for general ai assistants , author=. International Conference on Learning Representations , volume=

-

[49]

International Conference on Learning Representations , volume=

Webarena: A realistic web environment for building autonomous agents , author=. International Conference on Learning Representations , volume=

-

[50]

International Conference on Learning Representations , volume=

Agentbench: Evaluating llms as agents , author=. International Conference on Learning Representations , volume=

-

[51]

Proceedings of the ACM on Web Conference 2025 , pages=

Cluster aware graph anomaly detection , author=. Proceedings of the ACM on Web Conference 2025 , pages=

2025

-

[52]

Historical Market Data , year =

-

[53]

Risk-free Interest Rate Term Structures , year =

-

[54]

arXiv preprint arXiv:2505.09388 , year=

Qwen3 technical report , author=. arXiv preprint arXiv:2505.09388 , year=

-

[55]

Edward J Hu and yelong shen and Phillip Wallis and Zeyuan Allen-Zhu and Yuanzhi Li and Shean Wang and Lu Wang and Weizhu Chen , booktitle=. Lo. 2022 , url=

2022

-

[56]

arXiv preprint arXiv:2402.03300 , year=

Deepseekmath: Pushing the limits of mathematical reasoning in open language models , author=. arXiv preprint arXiv:2402.03300 , year=

-

[57]

SkyRL-v0: Train Real-World Long-Horizon Agents via Reinforcement Learning , author =

-

[58]

Proceedings of the 30th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

Macrohft: Memory augmented context-aware reinforcement learning on high frequency trading , author=. Proceedings of the 30th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

-

[59]

Knowledge-Based Systems , volume=

LSTM-ARIMA as a hybrid approach in algorithmic investment strategies , author=. Knowledge-Based Systems , volume=. 2025 , publisher=

2025

-

[60]

Proceedings of the 30th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

Sefraud: Graph-based self-explainable fraud detection via interpretative mask learning , author=. Proceedings of the 30th ACM SIGKDD Conference on Knowledge Discovery and Data Mining , pages=

-

[61]

Proceedings of the 2024 8th International Conference on Cloud and Big Data Computing , pages =

jun Gu, Wen and hao Zhong, Yi and zun Li, Shi and song Wei, Chang and ting Dong, Li and yue Wang, Zhuo and Yan, Chao , title =. Proceedings of the 2024 8th International Conference on Cloud and Big Data Computing , pages =. 2024 , isbn =. doi:10.1145/3694860.3694870 , abstract =

-

[62]

Proceedings of the 2024 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies (Volume 6: Industry Track) , pages=

AMA-LSTM: Pioneering robust and fair financial audio analysis for stock volatility prediction , author=. Proceedings of the 2024 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies (Volume 6: Industry Track) , pages=

2024

-

[63]

arXiv preprint arXiv:2512.21798 , year=

Deep Generative Models for Synthetic Financial Data: Applications to Portfolio and Risk Modeling: Applications of synthetic financial data in portfolio and risk modeling , author=. arXiv preprint arXiv:2512.21798 , year=

-

[64]

Proceedings of the 63rd Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers) , pages=

Investorbench: A benchmark for financial decision-making tasks with llm-based agent , author=. Proceedings of the 63rd Annual Meeting of the Association for Computational Linguistics (Volume 1: Long Papers) , pages=

-

[65]

Proceedings of the 30th acm sigkdd conference on knowledge discovery and data mining , pages=

A multimodal foundation agent for financial trading: Tool-augmented, diversified, and generalist , author=. Proceedings of the 30th acm sigkdd conference on knowledge discovery and data mining , pages=

-

[66]

IEEE Transactions on Big Data , year=

Finmem: A performance-enhanced llm trading agent with layered memory and character design , author=. IEEE Transactions on Big Data , year=

-

[67]

Advances in Neural Information Processing Systems , volume=

Fincon: A synthesized llm multi-agent system with conceptual verbal reinforcement for enhanced financial decision making , author=. Advances in Neural Information Processing Systems , volume=

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.