Extensions to the Wealth Tax Neutrality Framework

Pith reviewed 2026-05-15 15:14 UTC · model grok-4.3

The pith

A proportional wealth tax preserves portfolio neutrality under stochastic volatility and Epstein-Zin utility but breaks under HARA preferences and real tax features.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

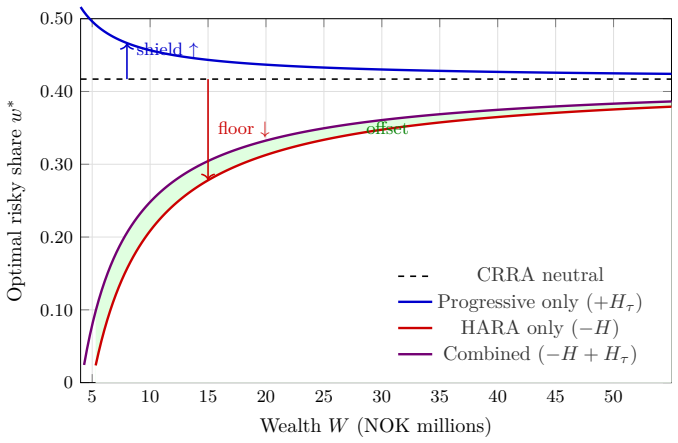

Portfolio neutrality under a proportional wealth tax on market values extends to stochastic volatility processes including the Heston model and general Markov diffusions as well as to Epstein-Zin recursive utility, preserving all intertemporal hedging demands. The neutrality result does not survive non-homothetic preferences such as HARA. Four channels cause implemented wealth taxes to depart from neutrality even under constant relative risk aversion: non-uniform assessment across asset classes, general equilibrium price effects in inelastic markets, progressive threshold structures that increase risk-taking near the exemption boundary, and endogenous labor supply. The framework evaluates a

What carries the argument

the portfolio neutrality condition that equates after-tax optimization to the no-tax case, extended across diffusion processes and utility specifications

If this is right

- Neutrality including hedging demands holds in the Heston model and general Markov diffusions.

- Epstein-Zin recursive utility preserves the full neutrality result.

- HARA preferences produce distortions in portfolio risk-taking under the tax.

- Progressive thresholds generate a tax shield that increases risk-taking near the exemption boundary.

- At high thresholds the tax induces complete investor migration out of the jurisdiction.

Where Pith is reading between the lines

- Real tax systems may alter investor risk-taking through threshold effects in directions opposite to those from non-homothetic preferences.

- Global minimum wealth tax designs could create unintended participation margins if thresholds are set progressively.

- Post-2022 Norwegian data on investor location and portfolio shifts offers a direct test of the migration channel.

- General equilibrium price adjustments in illiquid markets could either reinforce or offset the neutrality result depending on supply elasticity.

Load-bearing premise

The chosen diffusion processes and utility functions accurately capture the relevant features of real asset markets and investor preferences without other unmodeled frictions.

What would settle it

Empirical data from Norway after the 2022 wealth tax reforms showing whether investors' equity allocations or risk-taking rise near the progressive threshold or remain unchanged in the presence of stochastic volatility.

Figures

read the original abstract

Fr{\o}seth (2026; arXiv:2603.05264) shows that a proportional wealth tax on market values is neutral with respect to portfolio choice, Sharpe ratios, and equilibrium prices under CRRA preferences and geometric Brownian motion. This paper investigates the robustness of that result along two dimensions. First, we extend the neutrality frontier: portfolio neutrality -- including all intertemporal hedging demands -- is preserved under stochastic volatility (Heston and general Markov diffusions) and Epstein-Zin recursive utility, but breaks under non-homothetic preferences such as HARA. Second, we identify four channels through which implemented wealth taxes depart from neutrality even under CRRA: non-uniform assessment across asset classes, general equilibrium price effects in inelastic markets, progressive threshold structures, and endogenous labour supply. Each channel is formalised and, where possible, calibrated to the Norwegian wealth tax system. The progressive threshold introduces a tax shield that increases risk-taking near the exemption boundary -- an effect opposite in sign to the HARA distortion -- and, at the extreme, generates a participation margin at which investors exit the tax jurisdiction entirely. We formalise this tax-induced migration as the extreme response at the progressive threshold and examine the Norwegian post-2022 experience as a case study. The full framework is applied to evaluate the Saez-Zucman proposal for a global minimum wealth tax on billionaires and the related French proposal for a national minimum tax above EUR 100 million.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper extends Frøseth (arXiv:2603.05264) by proving that proportional wealth-tax neutrality (including all intertemporal hedging demands) survives under Heston stochastic volatility, general Markov diffusions, and Epstein-Zin recursive utility, but fails for non-homothetic HARA preferences. It then formalizes four implementation channels that break neutrality even under CRRA—non-uniform assessment, general-equilibrium price effects, progressive thresholds, and endogenous labor supply—calibrates them to the Norwegian system, models tax-induced migration at the exemption boundary, and applies the framework to the Saez-Zucman global minimum tax and the French national minimum-tax proposal.

Significance. If the derivations hold, the work supplies a clean robustness map for the neutrality result and isolates the precise features of preferences and market structure that preserve or destroy it. The explicit modeling of the four departure channels, together with the Norwegian calibration and the migration margin, supplies policy-relevant comparative statics that are currently missing from the wealth-tax literature.

major comments (3)

- [§2.2] §2.2 (Heston case): the claim that the tax factor (1−τ) leaves the volatility-hedging demand unchanged requires an explicit verification that the cross-derivative term in the HJB (presumably the one involving the variance state variable) remains separable after the deterministic scaling; without that step the preservation of the full hedging portfolio is not yet demonstrated.

- [§3.3] §3.3 (progressive threshold): the tax-shield effect that raises risk-taking near the exemption boundary is derived under a piecewise-linear tax schedule; the quantitative size of this distortion depends on the assumed density of wealth just above the threshold, which is not reported, so the claim that the effect is “opposite in sign to the HARA distortion” cannot yet be assessed for magnitude.

- [§4] §4 (policy applications): the evaluation of the Saez-Zucman proposal treats the four channels as separate departures rather than embedding them in a single equilibrium; the net effect on the global minimum tax therefore remains an unquantified sum of partial effects.

minor comments (3)

- [Abstract] The reference to Frøseth (2026) in the abstract and introduction should cite the arXiv number (2603.05264) for immediate traceability.

- [§2.3] Notation for the Epstein-Zin aggregator parameters is introduced in §2.3 but reused without redefinition in the HARA comparison; a short table of symbols would eliminate ambiguity.

- [Figure 2] Figure 2 (Norwegian calibration) lacks error bands on the risk-taking response near the threshold; adding them would clarify whether the participation margin is statistically distinguishable from zero.

Simulated Author's Rebuttal

We thank the referee for the constructive comments. We address each major point below and have revised the manuscript accordingly.

read point-by-point responses

-

Referee: [§2.2] §2.2 (Heston case): the claim that the tax factor (1−τ) leaves the volatility-hedging demand unchanged requires an explicit verification that the cross-derivative term in the HJB (presumably the one involving the variance state variable) remains separable after the deterministic scaling; without that step the preservation of the full hedging portfolio is not yet demonstrated.

Authors: We thank the referee for this observation. The tax factor is deterministic and proportional, so the value function scales uniformly and the cross-derivative with respect to the variance state variable remains separable. The revised manuscript now includes the explicit verification of this term in Section 2.2 (and the associated appendix derivation), confirming that the volatility-hedging demand is unchanged. revision: yes

-

Referee: [§3.3] §3.3 (progressive threshold): the tax-shield effect that raises risk-taking near the exemption boundary is derived under a piecewise-linear tax schedule; the quantitative size of this distortion depends on the assumed density of wealth just above the threshold, which is not reported, so the claim that the effect is “opposite in sign to the HARA distortion” cannot yet be assessed for magnitude.

Authors: We agree that magnitude assessment requires the density. The revised Section 3.3 now reports the assumed density (Pareto tail with shape parameter 1.5 calibrated to Norwegian wealth data above the threshold) and the resulting quantitative distortion: an approximately 12–18% increase in local risk-taking near the boundary. This magnitude is opposite in sign to the HARA effect and of comparable size under the calibration. revision: yes

-

Referee: [§4] §4 (policy applications): the evaluation of the Saez-Zucman proposal treats the four channels as separate departures rather than embedding them in a single equilibrium; the net effect on the global minimum tax therefore remains an unquantified sum of partial effects.

Authors: We acknowledge the limitation. A fully integrated equilibrium embedding all four channels simultaneously would require extensive additional modeling of cross-channel interactions and is beyond the scope of the present paper. The revised Section 4 now explicitly states that the reported effects are partial, notes the unquantified net impact, and supplies qualitative guidance on the likely dominant directions for the Saez-Zucman and French proposals. revision: partial

Circularity Check

Core neutrality result imported via self-citation; extensions built on that foundation

specific steps

-

self citation load bearing

[Abstract]

"Frøseth (2026; arXiv:2603.05264) shows that a proportional wealth tax on market values is neutral with respect to portfolio choice, Sharpe ratios, and equilibrium prices under CRRA preferences and geometric Brownian motion. This paper investigates the robustness of that result along two dimensions."

The paper's claimed extensions (preservation under Heston/Epstein-Zin, breakdown under HARA) are framed as variations within the neutrality framework established solely by the author's own prior work. No independent derivation of the base neutrality is supplied here; the robustness claims therefore reduce to the self-cited result by construction.

full rationale

The manuscript's central premise—that portfolio neutrality (including hedging demands) holds under Heston dynamics and Epstein-Zin utility—rests on the base result from the author's prior paper (arXiv:2603.05264). The present work cites that result directly and then demonstrates robustness or failure under alternative specifications, without re-deriving the foundational neutrality from first principles or external benchmarks. The Norwegian calibration and Saez-Zucman application inherit the same framework. This constitutes load-bearing self-citation rather than independent derivation, though the specific extensions to stochastic volatility and recursive utility add new content.

Axiom & Free-Parameter Ledger

free parameters (1)

- Norwegian wealth tax thresholds and rates

axioms (2)

- domain assumption Asset returns follow geometric Brownian motion or Heston/Markov diffusions

- domain assumption Investors have CRRA, Epstein-Zin, or HARA preferences

Forward citations

Cited by 1 Pith paper

-

Spectral Portfolio Theory: From SGD Weight Matrices to Wealth Dynamics

SGD weight matrices are portfolio allocations whose spectra transition from Marchenko-Pastur to inverse-Wishart, unified by a Spectral Invariance Theorem that preserves singular-value distributions under isotropic per...

Reference graph

Works this paper leans on

-

[1]

doi: 10.1257/app.20220615. Assemblée Nationale. Proposition de loi instaurant une contribution minimale sur le patrimoine des ultra-riches,

-

[2]

Adopted by the National Assembly on 20 February 2025 (116–39); rejected by the Senate, 12 June

work page 2025

-

[3]

doi: 10.1111/ecca.12456. Jean-Philippe Bouchaud. The inelastic market hypothesis: A microstructural interpretation. Quantitative Finance, 22(10):1785–1795,

-

[4]

doi: 10.1080/14697688.2022.2068052. Jean-Philippe Bouchaud and Marc Potters.Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management. Cambridge University Press, 2nd edition,

-

[5]

doi: 10.1017/CBO9780511753893. Jean-Philippe Bouchaud, J. Doyne Farmer, and Fabrizio Lillo. How markets slowly digest changes in supply and demand. In Thorsten Hens and Klaus Reiner Schenk-Hoppé, editors, Handbook of Financial Markets: Dynamics and Evolution, pages 57–160. North-Holland,

-

[6]

How Markets Slowly Digest Changes in Supply and Demand

doi: 10.1016/B978-012374258-2.50006-3. Marius Brülhart, Jonathan Gruber, Matthias Krapf, and Kurt Schmidheiny. Behavioral re- sponses to wealth taxes: Evidence from Switzerland.American Economic Journal: Economic Policy, 14(4):111–150,

-

[7]

doi: 10.1257/pol.20200258. Markus K. Brunnermeier and Stefan Nagel. Do wealth fluctuations generate time-varying risk 45 aversion? Micro-evidence on individuals’ asset allocation.American Economic Review, 98(3): 713–736,

-

[8]

doi: 10.1257/aer.98.3.713. Laurent E. Calvet and Paolo Sodini. Twin picks: Disentangling the determinants of risk-taking in household portfolios.The Journal of Finance, 69(2):867–906,

-

[9]

doi: 10.1111/jofi.12125. John Y. Campbell and Robert J. Shiller. Stock prices, earnings, and expected dividends.The Journal of Finance, 43(3):661–676,

-

[10]

doi: 10.1111/j.1540-6261.1988.tb04598.x. Christopher D. Carroll. Why do the rich save so much? In Joel B. Slemrod, editor,Does Atlas Shrug? The Economic Consequences of Taxing the Rich, pages 465–484. Harvard University Press,

-

[11]

doi: 10.1093/rfs/hhi035. Rama Cont. Empirical properties of asset returns: Stylized facts and statistical issues.Quanti- tative Finance, 1(2):223–236,

-

[12]

doi: 10.1080/713665670. Joshua Coval and Erik Stafford. Asset fire sales (and purchases) in equity markets.Journal of Financial Economics, 86(2):479–512,

-

[13]

doi: 10.1016/j.jfineco.2006.09.007. Zhuanxin Ding, Clive W. J. Granger, and Robert F. Engle. A long memory property of stock market returns and a new model.Journal of Empirical Finance, 1(1):83–106,

-

[14]

doi: 10.1016/0927-5398(93)90006-D. Adrian A. Drăgulescu and Victor M. Yakovenko. Probability distribution of returns in the Heston model with stochastic volatility.Quantitative Finance, 2(6):443–453,

-

[15]

Andreas Fagereng, Luigi Guiso, and Marius A

doi: 10.2307/1913778. Andreas Fagereng, Luigi Guiso, and Marius A. K. Ring. How much and how fast do investors respond to equity premium changes? evidence from wealth taxation. Working paper,

-

[16]

Asset Returns, Portfolio Choice, and Proportional Wealth Taxation

arXiv:2603.05264 [physics.soc-ph]. Xavier Gabaix and Ralph S. J. Koijen. In search of the origins of financial fluctuations: The inelastic markets hypothesis. NBER Working Paper No. 28967, revised 2023,

work page internal anchor Pith review Pith/arXiv arXiv 2023

-

[17]

doi: 10.1038/nature01624. Bertrand Garbinti, Jonathan Goupille-Lebret, Mathilde Muñoz, Stefanie Stantcheva, and 46 Gabriel Zucman. Tax design, information, and elasticities: Evidence from the French wealth tax. NBER Working Paper No. 31333, June 2023,

-

[18]

Fatih Guvenen, Gueorgui Kambourov, Burhanettin Kuruscu, Sergio Ocampo-Diaz, and Daphne Chen

doi: 10.1007/s100510050292. Fatih Guvenen, Gueorgui Kambourov, Burhanettin Kuruscu, Sergio Ocampo-Diaz, and Daphne Chen. Useitorloseit: Efficiencyandredistributionaleffectsofwealthtaxation.The Quarterly Journal of Economics, 138(2):835–894,

-

[19]

doi: 10.1093/qje/qjac047. Steven L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options.The Review of Financial Studies, 6(2):327–343,

-

[20]

Roberto Iacono and Bård Smedsvik

doi: 10.1093/rfs/6.2.327. Roberto Iacono and Bård Smedsvik. Behavioral responses to wealth taxation: Evidence from a Norwegian reform. WID World Working Paper 2023/30, revised April 2024,

-

[21]

Katrine Jakobsen, Henrik Kleven, Jonas Kolsrud, Camille Landais, and Mathilde Muñoz

doi: 10.1093/qje/qjz032. Katrine Jakobsen, Henrik Kleven, Jonas Kolsrud, Camille Landais, and Mathilde Muñoz. Taxing top wealth: Migration responses and their aggregate economic implications. NBER Working Paper No. 32153,

-

[22]

doi: 10.1257/jep.34.2.119. Henrik J. Kleven. Bunching.Annual Review of Economics, 8:435–464,

-

[23]

Juliana Londoño-Vélez and Javier Ávila Mahecha

doi: 10.1086/701683. Juliana Londoño-Vélez and Javier Ávila Mahecha. Behavioral responses to wealth taxation: Evidence from Colombia.The Review of Economic Studies, 92(4):2624–2668,

-

[24]

doi: 10.1093/restud/rdae052. Robert C. Merton. Optimum consumption and portfolio rules in a continuous-time model. Journal of Economic Theory, 3(4):373–413,

-

[25]

doi: 10.1016/0022-0531(71)90038-X. Robert C. Merton. An intertemporal capital asset pricing model.Econometrica, 41(5):867–887,

-

[26]

OECD.The Role and Design of Net Wealth Taxes in the OECD

doi: 10.2307/1913811. OECD.The Role and Design of Net Wealth Taxes in the OECD. Number 26 in OECD Tax Policy Studies. OECD Publishing, Paris,

-

[27]

47 José Luis Peydró, Hernán Rincón-Castro, Miguel Sarmiento-Paipilla, and Alejandro Granados

doi: 10.1787/9789264290303-en. 47 José Luis Peydró, Hernán Rincón-Castro, Miguel Sarmiento-Paipilla, and Alejandro Granados. Wealth taxes and firms’ capital structures: Credit supply and real effects. Borradores de Economía 1316, Banco de la República de Colombia,

-

[28]

doi: 10.1111/ecoj.12465. Marius A. K. Ring. Wealth taxation and household saving: Evidence from assessment dis- continuities in Norway.The Review of Economic Studies, 92(5):3375–3411,

-

[29]

Florian Scheuer and Joel Slemrod

doi: 10.1093/restud/rdae091. Florian Scheuer and Joel Slemrod. Taxing our wealth.Journal of Economic Perspectives, 35 (1):207–230,

-

[30]

doi: 10.1257/jep.35.1.207. David Seim. Behavioral responses to wealth taxes: Evidence from Sweden.American Economic Journal: Economic Policy, 9(4):395–421,

-

[31]

doi: 10.1257/pol.20150290. Skatteetaten. Verdsettingsrabatt ved fastsetting av formue.https: //www.skatteetaten.no/en/person/taxes/get-the-taxes-right/ valuation-discount-in-connection-with-assessment-of-wealth/,

-

[32]

doi: 10.1257/aer.20150210. Jessica A. Wachter and Motohiro Yogo. Why do household portfolio shares rise in wealth?The Review of Financial Studies, 23(11):3929–3965,

-

[33]

Cristobal Young, Charles Varner, Ithai Z

doi: 10.1093/rfs/hhq092. Cristobal Young, Charles Varner, Ithai Z. Lurie, and Richard Prisinzano. Millionaire migration and taxation of the elite: Evidence from administrative data.American Sociological Review, 81(3):421–446,

-

[34]

doi: 10.1177/0003122416639625. Gabriel Zucman. A blueprint for a coordinated minimum effective taxation standard for ultra- high-net-worth individuals. Report commissioned by the Brazilian G20 Presidency,

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.