Recognition: 2 theorem links

· Lean TheoremOptimal Pricing with Unreliable Signals

Pith reviewed 2026-05-13 18:41 UTC · model grok-4.3

The pith

Private unreliable signals enable strictly better consistency-robustness tradeoffs in single-buyer pricing than any public benchmark.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

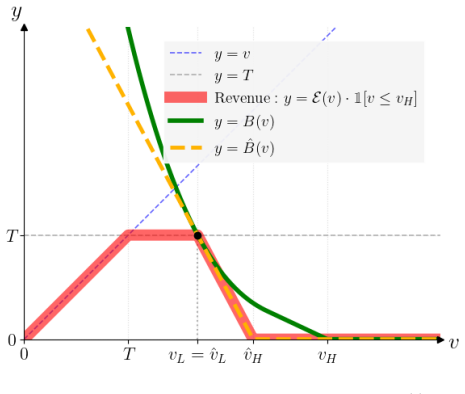

The exact Pareto frontier between consistency and robustness is characterized for mechanisms that keep the unreliable sample private; these mechanisms strictly dominate any public-signal benchmark, achieve perfect consistency with a nontrivial robustness guarantee of 1/2 for every prior, and achieve simultaneous 1-consistency and 1-robustness when the prior has infinite mean or mean at most the monopoly price.

What carries the argument

Mechanisms that treat the reliability of the seller's private sample as the buyer's private information and optimize the consistency-robustness frontier directly.

If this is right

- Private retention of the unreliable signal generates strictly better consistency-robustness pairs than any public-signal mechanism.

- Perfect consistency is compatible with a robustness guarantee of exactly 1/2 for every prior.

- Simultaneous 1-consistency and 1-robustness is achievable when the prior has infinite mean or mean at most the monopoly price.

- Mechanisms can be designed to exploit the buyer's knowledge of signal reliability rather than only the seller's direct information.

Where Pith is reading between the lines

- The same reliability-as-private-information device could be applied to multi-buyer auctions or contract design with unreliable AI predictions.

- Repeated interaction might allow buyers to develop strategies for reporting or concealing their knowledge of signal reliability.

- Laboratory experiments with human subjects facing simulated hallucinating predictors could measure whether the theoretical gains materialize in practice.

Load-bearing premise

The buyer knows whether the seller's private sample is accurate or hallucinatory.

What would settle it

A prior distribution and a concrete mechanism pair where no mechanism reaches the claimed frontier point, such as perfect consistency paired with robustness strictly below 1/2.

Figures

read the original abstract

We study a single-buyer pricing problem with unreliable side information, motivated by the increasing use of AI-assisted decision-making and LLM-based predictions. The seller observes a private sample that may be either accurate (coinciding with the buyer's valuation), or hallucinatory (an independent draw from the prior), without knowing which case has realized. The buyer does not observe the realized signal, yet knows whether it is accurate or hallucinatory. This creates a higher-order informational asymmetry: the seller is uncertain about the reliability of his own side information, while the buyer has private information about that reliability. Adopting a consistency-robustness framework, we characterize the exact Pareto frontier of tradeoffs between consistency (performance under an accurate signal) and robustness (performance under a hallucinatory signal). We show that keeping the unreliable signal private generates substantial value, yielding tradeoffs that strictly dominate any public-signal benchmark. We further show that perfect consistency does not preclude meaningful protection against hallucination: for every prior, there exists a mechanism achieving perfect consistency together with a nontrivial robustness guarantee of $\frac{1}{2}$. Moreover, if the prior has an infinite mean or a mean of at most its monopoly price, we provide a mechanism that is simultaneously 1-consistent and 1-robust. Our results illustrate a new mechanism design paradigm: rather than relying only on information directly possessed by the designer, mechanisms can be built to leverage the other side's knowledge about the reliability of the designer's information.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. This paper studies a single-buyer pricing problem with an unreliable private signal observed by the seller that is either accurate (equal to the buyer's valuation) or hallucinatory (an independent draw from the prior). The buyer knows the realized reliability type but not the signal value itself, creating a higher-order asymmetry. The authors characterize the exact Pareto frontier of consistency-robustness tradeoffs, show that private-signal mechanisms strictly dominate public-signal benchmarks, and construct mechanisms achieving 1-consistency together with 1/2-robustness for arbitrary priors (and 1-consistency with 1-robustness when the prior mean is infinite or lies at most at the monopoly price).

Significance. If the derivations hold, the work is significant for mechanism design under unreliable information, especially in AI/LLM settings. The exact Pareto-frontier characterization, the strict dominance result over public benchmarks, and the explicit constructions of mechanisms with strong guarantees (perfect consistency plus nontrivial robustness) constitute a clean contribution that leverages the buyer's knowledge of signal reliability rather than only the designer's own information.

minor comments (2)

- [Abstract] The abstract states that private-signal mechanisms 'strictly dominate' public benchmarks; a brief quantitative illustration of the frontier shift (e.g., the improvement in robustness for a fixed consistency level) would make this claim more concrete.

- Notation for the two reliability types (accurate vs. hallucinatory) and the associated virtual-valuation expressions should be standardized and introduced once in a dedicated preliminary section to aid readability.

Simulated Author's Rebuttal

We thank the referee for their positive assessment of the manuscript, the clear summary of our contributions, and the recommendation for minor revision. No specific major comments were raised in the report.

Circularity Check

Derivation self-contained in model primitives

full rationale

The paper constructs mechanisms and characterizes the exact Pareto frontier directly from the stated higher-order asymmetry: the seller observes an unreliable private sample while the buyer knows its realized reliability type (accurate vs. hallucinatory) but not the sample value. Type-contingent virtual valuations and posted-price rules follow from standard Myerson-style optimization applied to the induced distributions; the 1-consistent + 1/2-robust guarantee and the dominance over public-signal benchmarks are obtained by explicit construction for arbitrary priors. No equation reduces to a fitted parameter renamed as prediction, no self-citation chain is load-bearing, and no ansatz is smuggled via prior work. The results are therefore independent of the paper's own outputs.

Axiom & Free-Parameter Ledger

axioms (1)

- domain assumption The seller's private sample is either accurate (equals buyer's valuation) or hallucinatory (independent draw from the prior), and the buyer knows which case occurred.

Lean theorems connected to this paper

-

IndisputableMonolith/Cost/FunctionalEquation.leanwashburn_uniqueness_aczel unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

We characterize the exact Pareto frontier of tradeoffs between consistency (performance under an accurate signal) and robustness (performance under a hallucinatory signal) ... R⋆(C)≜inf_β>0[(1+β)−C(β+β²)ln(1+1/β)]

-

IndisputableMonolith/Foundation/RealityFromDistinction.leanreality_from_one_distinction unclear?

unclearRelation between the paper passage and the cited Recognition theorem.

the optimal mechanism ... is obtained by solving an LP over the one-dimensional functional variables x(·) and p(·)

What do these tags mean?

- matches

- The paper's claim is directly supported by a theorem in the formal canon.

- supports

- The theorem supports part of the paper's argument, but the paper may add assumptions or extra steps.

- extends

- The paper goes beyond the formal theorem; the theorem is a base layer rather than the whole result.

- uses

- The paper appears to rely on the theorem as machinery.

- contradicts

- The paper's claim conflicts with a theorem or certificate in the canon.

- unclear

- Pith found a possible connection, but the passage is too broad, indirect, or ambiguous to say the theorem truly supports the claim.

Reference graph

Works this paper leans on

-

[1]

[BDGT25] Eric Balkanski, Nicholas DeFilippis, Vasilis Gkatzelis, and Xizhi Tan. Procurement auc- tions with predictions: Improved frugality for facility location.CoRR, abs/2512.09367,

-

[2]

Optimal stopping with a predicted prior.CoRR, abs/2511.03289,

[BHLL25] Tian Bai, Zhiyi Huang, Chui Shan Lee, and Dongchen Li. Optimal stopping with a predicted prior.CoRR, abs/2511.03289,

-

[3]

Mechanism design with predictions for obnoxious facility location.CoRR, abs/2212.09521,

[IB22] Gabriel Istrate and Cosmin Bonchis. Mechanism design with predictions for obnoxious facility location.CoRR, abs/2212.09521,

-

[4]

Prophet and secretary at the same time

[KK25] Gregory Kehne and Thomas Kesselheim. Prophet and secretary at the same time. CoRR, abs/2511.09531,

-

[5]

Pricing with a hidden sample.arXiv preprint arXiv:2602.18038,

[TTW26] Zhihao Gavin Tang, Yixin Tao, and Shixin Wang. Pricing with a hidden sample.arXiv preprint arXiv:2602.18038,

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.