Recognition: no theorem link

Dynamic Forecasting and Temporal Feature Evolution of Stock Repurchases in Listed Companies Using Attention-Based Deep Temporal Networks

Pith reviewed 2026-05-14 22:02 UTC · model grok-4.3

The pith

A hybrid deep temporal network predicts stock repurchases by distinguishing long-term undervaluation from short-term cash flow increases.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that a hybrid TCN and attention LSTM architecture, trained on rolling windows of Chinese A-share financial ratios from 2014-2024, delivers significantly higher accuracy in forecasting repurchase announcements than static baselines, while XAI analysis shows prolonged undervaluation functions as the long-term underlying motive and a sharp cash-flow increase acts as the immediate short-term trigger.

What carries the argument

Hybrid Temporal Convolutional Network paired with Attention-based LSTM that extracts multi-scale temporal dependencies from corporate financial time series.

If this is right

- Forecasts that update with new financial releases can improve timing of quantitative investment decisions around buybacks.

- Risk models gain earlier signals of potential share-price movements linked to repurchase programs.

- Corporate-finance researchers obtain temporal granularity for testing hypotheses such as signaling versus free-cash-flow explanations.

- Regulators can monitor evolving feature importance for signs of information asymmetry or market timing.

- The rolling-window protocol offers a practical template for other non-stationary financial prediction tasks.

Where Pith is reading between the lines

- The same architecture could be applied to dividend initiations or seasoned equity offerings to test whether similar long- versus short-term motive structures appear.

- If cash-flow spikes dominate short-term triggers, changes in central-bank liquidity policy would be expected to shift repurchase frequencies in measurable ways.

- Cross-market comparisons would reveal whether the undervaluation-then-cash-flow sequence is specific to emerging-market governance or holds more broadly.

- Real-time versions of the model could be embedded in trading systems to generate live signals whenever attention weights on cash-flow features rise sharply.

Load-bearing premise

That the temporal patterns learned by attention on Chinese A-share data correspond to genuine economic motives rather than dataset-specific correlations.

What would settle it

Re-training the same architecture on repurchase data from a later period or non-Chinese market and checking whether prolonged undervaluation followed by cash-flow spikes remain the dominant drivers identified by XAI.

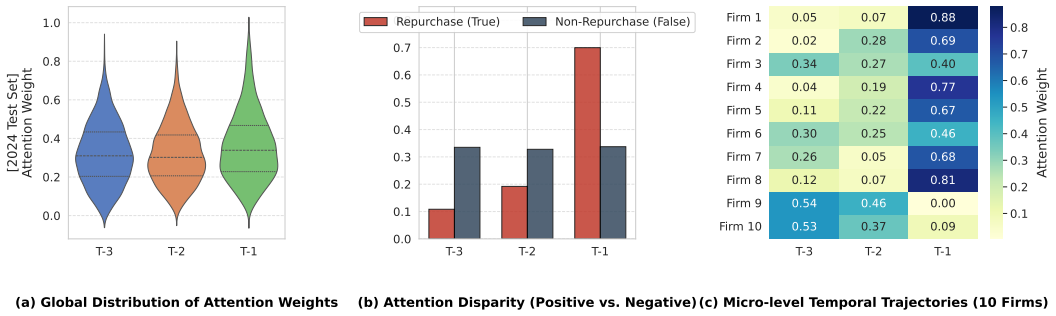

Figures

read the original abstract

Accurately predicting stock repurchases is crucial for quantitative investment and risk management, yet traditional static models fail to capture the complex temporal dependencies of corporate financial conditions. This paper proposes a dynamic early warning system integrating economic theory with deep temporal networks. Using Chinese A-share panel data (2014-2024), we employ a hybrid Temporal Convolutional Network (TCN) and Attention-based LSTM to capture long- and short-term financial evolutionary patterns. Rolling-window cross-validation demonstrates our model significantly outperforms static baselines like Logistic Regression and XGBoost. Furthermore, utilizing Explainable AI (XAI), we reveal the temporal dynamics of repurchase decisions: prolonged "undervaluation" serves as the long-term underlying motive, while a sharp increase in "cash flow" acts as the decisive short-term trigger. This study provides a robust deep learning paradigm for financial forecasting and offers dynamic empirical support for classic corporate finance hypotheses.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a hybrid Temporal Convolutional Network (TCN) and Attention-based LSTM model for dynamic forecasting of stock repurchases using Chinese A-share panel data (2014-2024). It claims that rolling-window cross-validation shows significant outperformance over static baselines such as Logistic Regression and XGBoost, and that XAI analysis reveals interpretable temporal dynamics: prolonged undervaluation as the long-term motive and sharp cash-flow increases as the short-term trigger.

Significance. If validated, the work could contribute a deep-learning framework for capturing temporal evolution in corporate events, offering both improved predictive tools for quantitative finance and dynamic empirical evidence on repurchase motives that complements static corporate-finance theory.

major comments (4)

- [Abstract and §4] Abstract and §4 (empirical results): the claim of significant outperformance is unsupported by error bars, p-values, or ablation experiments isolating the attention mechanism; without these, the incremental value of the hybrid TCN+Attention-LSTM over simpler temporal baselines cannot be assessed.

- [§3.2] §3.2 (validation procedure): rolling-window cross-validation is described but lacks explicit window lengths, leakage safeguards for non-stationary financial series, or tests against label-shuffled controls; this leaves open the possibility that reported gains reflect regime-specific correlations rather than genuine temporal forecasting skill.

- [§5] §5 (XAI analysis): the reported long-term undervaluation and short-term cash-flow triggers are post-hoc attributions from the same fitted model used for prediction; without independent checks such as feature-permutation importance, comparison to a non-temporal baseline achieving similar accuracy, or out-of-sample economic validation, the interpretations risk circularity and may capture spurious co-occurrences in clustered repurchase events.

- [§2] §2 (data and features): no details are supplied on feature construction, handling of rare clustered events, or an external hold-out period beyond 2014-2024; this omission prevents evaluation of whether the temporal patterns generalize or are artifacts of Chinese A-share policy regimes.

minor comments (1)

- [Throughout] Define all acronyms (TCN, LSTM, XAI) at first use and ensure consistent notation for attention scaling parameters across equations and text.

Simulated Author's Rebuttal

We thank the referee for the constructive and detailed comments, which highlight important areas for strengthening the statistical rigor, methodological transparency, and interpretability of our work. We address each major comment point by point below and indicate the revisions we will make.

read point-by-point responses

-

Referee: [Abstract and §4] Abstract and §4 (empirical results): the claim of significant outperformance is unsupported by error bars, p-values, or ablation experiments isolating the attention mechanism; without these, the incremental value of the hybrid TCN+Attention-LSTM over simpler temporal baselines cannot be assessed.

Authors: We agree that the current results section would benefit from additional statistical validation. In the revised manuscript we will report mean performance with standard error bars across five random seeds, include p-values from paired statistical tests (e.g., McNemar or Wilcoxon signed-rank) against each baseline, and add ablation experiments that isolate the contribution of the attention mechanism by comparing the full hybrid model against TCN-only and LSTM-only variants. We will also benchmark against two additional temporal baselines (vanilla LSTM and GRU) to better quantify the hybrid architecture's incremental value. revision: yes

-

Referee: [§3.2] §3.2 (validation procedure): rolling-window cross-validation is described but lacks explicit window lengths, leakage safeguards for non-stationary financial series, or tests against label-shuffled controls; this leaves open the possibility that reported gains reflect regime-specific correlations rather than genuine temporal forecasting skill.

Authors: We acknowledge that §3.2 requires greater specificity. The revised version will explicitly state the window configuration (60-month training windows advancing by 12 months, with the final 12 months of each fold reserved for testing), describe leakage-prevention steps (strict forward-only feature construction and no future information in any rolling fold), and report results on label-shuffled controls to demonstrate that performance degrades substantially when temporal ordering is destroyed, thereby supporting that gains reflect genuine forecasting skill rather than regime artifacts. revision: yes

-

Referee: [§5] §5 (XAI analysis): the reported long-term undervaluation and short-term cash-flow triggers are post-hoc attributions from the same fitted model used for prediction; without independent checks such as feature-permutation importance, comparison to a non-temporal baseline achieving similar accuracy, or out-of-sample economic validation, the interpretations risk circularity and may capture spurious co-occurrences in clustered repurchase events.

Authors: We recognize the potential circularity concern. We will augment §5 with feature-permutation importance rankings computed on held-out folds, direct comparison of the temporal attributions against those obtained from a non-temporal XGBoost model trained on the same features, and an economic validation exercise that simulates a simple trading rule based on the identified long-term undervaluation and short-term cash-flow signals. Full independence from the original model is inherently limited by the single-dataset setting, but the added checks will materially reduce the risk of spurious interpretations. revision: partial

-

Referee: [§2] §2 (data and features): no details are supplied on feature construction, handling of rare clustered events, or an external hold-out period beyond 2014-2024; this omission prevents evaluation of whether the temporal patterns generalize or are artifacts of Chinese A-share policy regimes.

Authors: We will substantially expand §2 to document the full feature-construction pipeline (including lag structures, normalization, and missing-value imputation), describe our handling of rare clustered repurchase events via temporal clustering analysis and class-weighted loss, and clarify that the rolling-window protocol already treats later periods within 2014-2024 as implicit out-of-sample tests. An external hold-out set after 2024 is not available given current data release schedules; we will therefore add an explicit limitations paragraph discussing potential Chinese A-share policy regime effects and the need for future cross-market validation. revision: partial

Circularity Check

No significant circularity in model evaluation or XAI interpretations

full rationale

The paper's core claims rest on training a hybrid TCN + Attention-LSTM on 2014-2024 Chinese A-share panel data, evaluating via rolling-window cross-validation against static baselines (Logistic Regression, XGBoost), and applying post-hoc XAI to surface temporal feature importance. These steps do not reduce to the inputs by construction: the CV performance metric is computed on temporally held-out windows and is not a re-statement of training labels; the XAI attributions (long-term undervaluation, short-term cash-flow spike) are derived interpretations of the fitted attention weights rather than a self-definitional loop or a fitted parameter renamed as a prediction. No load-bearing self-citation, uniqueness theorem, or ansatz smuggling is present in the provided derivation chain. The analysis is therefore self-contained against external benchmarks.

Axiom & Free-Parameter Ledger

free parameters (2)

- TCN kernel sizes and LSTM hidden dimensions

- Attention temperature or scaling factor

axioms (1)

- domain assumption Financial time series contain stable long-range and short-range dependencies that a hybrid TCN-attention architecture can extract without explicit economic modeling.

Reference graph

Works this paper leans on

-

[1]

Theo Vermaelen. Common stock repurchases and market signalling: An empirical study.Journal of fi- nancial economics, 9(2):139–183, 1981

work page 1981

-

[2]

Larry Y Dann. Common stock repurchases: An anal- ysis of returns to bondholders and stockholders.Jour- nal of financial economics, 9(2):113–138, 1981

work page 1981

-

[3]

Michael C Jensen. Agency costs of free cash flow, corporate finance, and takeovers.The American eco- nomic review, 76(2):323–329, 1986

work page 1986

-

[4]

David Ikenberry, Josef Lakonishok, and Theo Ver- maelen. Market underreaction to open market share repurchases.Journal of financial economics, 39(2- 3):181–208, 1995

work page 1995

-

[5]

Clifford P Stephens and Michael S Weisbach. Actual share reacquisitions in open-market repurchase pro- grams.The Journal of finance, 53(1):313–333, 1998

work page 1998

-

[6]

Empirical asset pricing via machine learning.The Review of Financial Studies, 33(5):2223–2273, 2020

Shihao Gu, Bryan Kelly, and Dacheng Xiu. Empirical asset pricing via machine learning.The Review of Financial Studies, 33(5):2223–2273, 2020

work page 2020

-

[7]

Jigar Patel, Sahil Shah, Priyank Thakkar, and Ke- tan Kotecha. Predicting stock and stock price index movement using trend deterministic data preparation and machine learning techniques.Expert systems with applications, 42(1):259–268, 2015

work page 2015

-

[8]

Mitchell A Petersen. Estimating standard errors in finance panel data sets: Comparing approaches.The Review of financial studies, 22(1):435–480, 2008

work page 2008

-

[9]

Thomas Fischer and Christopher Krauss. Deep learn- ing with long short-term memory networks for finan- cial market predictions.European journal of opera- tional research, 270(2):654–669, 2018

work page 2018

-

[10]

An Empirical Evaluation of Generic Convolutional and Recurrent Networks for Sequence Modeling

Shaojie Bai, J Zico Kolter, and Vladlen Koltun. An empirical evaluation of generic convolutional and recurrent networks for sequence modeling.arXiv preprint arXiv:1803.01271, 2018

work page internal anchor Pith review Pith/arXiv arXiv 2018

-

[11]

Omer Berat Sezer, Mehmet Ugur Gudelek, and Ah- met Murat Ozbayoglu. Financial time series forecast- ing with deep learning: A systematic literature re- view: 2005–2019.Applied soft computing, 90:106181, 2020

work page 2005

-

[12]

Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Lukasz Kaiser, and Illia Polosukhin. Attention is all you need. volume 30, 2017

work page 2017

-

[13]

Alejandro Barredo Arrieta, Natalia D´ ıaz-Rodr´ ıguez, Javier Del Ser, Adrien Bennetot, Siham Tabik, Al- berto Barbado, Salvador Garc´ ıa, Sergio Gil-L´ opez, Daniel Molina, Richard Benjamins, et al. Explainable artificial intelligence (xai): Concepts, taxonomies, op- portunities and challenges toward responsible ai.In- formation fusion, 58:82–115, 2020

work page 2020

-

[14]

A unified approach to interpreting model predictions

Scott M Lundberg and Su-In Lee. A unified approach to interpreting model predictions. volume 30, 2017

work page 2017

-

[15]

Machine learning explainability in fi- nance: an application to default risk analysis

Philippe Bracke, Anupam Datta, Carsten Jung, and Shayak Sen. Machine learning explainability in fi- nance: an application to default risk analysis. 2019

work page 2019

-

[16]

Why do firms repurchase stock.The journal of Business, 73(3):331–355, 2000

Amy K Dittmar. Why do firms repurchase stock.The journal of Business, 73(3):331–355, 2000

work page 2000

-

[17]

Payout policy in the 21st century

Alon Brav, John R Graham, Campbell R Harvey, and Roni Michaely. Payout policy in the 21st century. Journal of financial economics, 77(3):483–527, 2005

work page 2005

-

[18]

Gustavo Grullon and Roni Michaely. Dividends, share repurchases, and the substitution hypothesis.the Journal of Finance, 57(4):1649–1684, 2002

work page 2002

-

[19]

Market timing and capital structure.The journal of finance, 57(1):1– 32, 2002

Malcolm Baker and Jeffrey Wurgler. Market timing and capital structure.The journal of finance, 57(1):1– 32, 2002

work page 2002

-

[20]

The cash flow sensitivity of cash.The jour- nal of finance, 59(4):1777–1804, 2004

Heitor Almeida, Murillo Campello, and Michael S Weisbach. The cash flow sensitivity of cash.The jour- nal of finance, 59(4):1777–1804, 2004

work page 2004

-

[21]

Joan Farre-Mensa and Alexander Ljungqvist. Do measures of financial constraints measure financial constraints?The review of financial studies, 29(2):271–308, 2016. 15

work page 2016

-

[22]

Chih-Fong Tsai and Yu-Chieh Hsiao. Combining multiple feature selection methods for stock predic- tion: Union, intersection, and multi-intersection ap- proaches.Decision support systems, 50(1):258–269, 2010

work page 2010

-

[23]

Support-vector networks.Machine learning, 20(3):273–297, 1995

Corinna Cortes and Vladimir Vapnik. Support-vector networks.Machine learning, 20(3):273–297, 1995

work page 1995

-

[24]

Random forests.Machine learning, 45(1):5–32, 2001

Leo Breiman. Random forests.Machine learning, 45(1):5–32, 2001

work page 2001

-

[25]

Xgboost: A scal- able tree boosting system

Tianqi Chen and Carlos Guestrin. Xgboost: A scal- able tree boosting system. InProceedings of the 22nd acm sigkdd international conference on knowledge dis- covery and data mining, pages 785–794, 2016

work page 2016

-

[26]

Christopher Krauss, Xuan Anh Do, and Nicolas Huck. Deep neural networks, gradient-boosted trees, random forests: Statistical arbitrage on the s&p 500.European journal of operational research, 259(2):689–702, 2017

work page 2017

-

[27]

Universal features of price formation in financial markets: perspectives from deep learning

Justin Sirignano and Rama Cont. Universal features of price formation in financial markets: perspectives from deep learning. pages 5–15, 2021

work page 2021

-

[28]

Hanyao Gao, Gang Kou, Haiming Liang, Hengjie Zhang, Xiangrui Chao, Cong-Cong Li, and Yucheng Dong. Machine learning in business and finance: a lit- erature review and research opportunities.Financial Innovation, 10(1):86, 2024

work page 2024

-

[29]

Alex Graves. Long short-term memory.Supervised se- quence labelling with recurrent neural networks, pages 37–45, 2012

work page 2012

-

[30]

Bryan Lim, Sercan ¨O Arık, Nicolas Loeff, and Tomas Pfister. Temporal fusion transformers for inter- pretable multi-horizon time series forecasting.Inter- national journal of forecasting, 37(4):1748–1764, 2021

work page 2021

-

[31]

WaveNet: A Generative Model for Raw Audio

Aaron Van Den Oord, Sander Dieleman, Heiga Zen, Karen Simonyan, Oriol Vinyals, Alex Graves, Nal Kalchbrenner, Andrew Senior, Koray Kavukcuoglu, et al. Wavenet: A generative model for raw audio. arXiv preprint arXiv:1609.03499, 12(1), 2016

work page internal anchor Pith review Pith/arXiv arXiv 2016

-

[32]

Shiyang Li, Xiaoyong Jin, Yao Xuan, Xiyou Zhou, Wenhu Chen, Yu-Xiang Wang, and Xifeng Yan. En- hancing the locality and breaking the memory bottle- neck of transformer on time series forecasting. vol- ume 32, 2019

work page 2019

-

[33]

Scott M Lundberg, Gabriel Erion, Hugh Chen, Alex DeGrave, Jordan M Prutkin, Bala Nair, Ronit Katz, Jonathan Himmelfarb, Nisha Bansal, and Su-In Lee. From local explanations to global understanding with explainable ai for trees.Nature machine intelligence, 2(1):56–67, 2020

work page 2020

-

[34]

Niklas Bussmann, Paolo Giudici, Dimitri Marinelli, and Jochen Papenbrock. Explainable machine learn- ing in credit risk management.Computational Eco- nomics, 57(1):203–216, 2021

work page 2021

-

[35]

Shachar Kaufman, Saharon Rosset, Claudia Perlich, and Ori Stitelman. Leakage in data mining: Formula- tion, detection, and avoidance.ACM Transactions on Knowledge Discovery from Data (TKDD), 6(4):1–21, 2012

work page 2012

-

[36]

Yann LeCun, Yoshua Bengio, and Geoffrey Hinton. Deep learning, volume 521. Nature Publishing Group UK London, 2015

work page 2015

-

[37]

Neural Machine Translation by Jointly Learning to Align and Translate

Dzmitry Bahdanau, Kyunghyun Cho, and Yoshua Bengio. Neural machine translation by jointly learning to align and translate.arXiv preprint arXiv:1409.0473, 2014

work page internal anchor Pith review Pith/arXiv arXiv 2014

-

[38]

Focal loss for dense object de- tection

Tsung-Yi Lin, Priya Goyal, Ross Girshick, Kaiming He, and Piotr Doll´ ar. Focal loss for dense object de- tection. InProceedings of the IEEE international con- ference on computer vision, pages 2980–2988, 2017. 16

work page 2017

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.