Recognition: unknown

Emergence of Statistical Financial Factors by a Diffusion Process

Pith reviewed 2026-05-10 14:32 UTC · model grok-4.3

The pith

Financial factors arise as stable co-movement patterns from a diffusion process on asset interaction networks.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

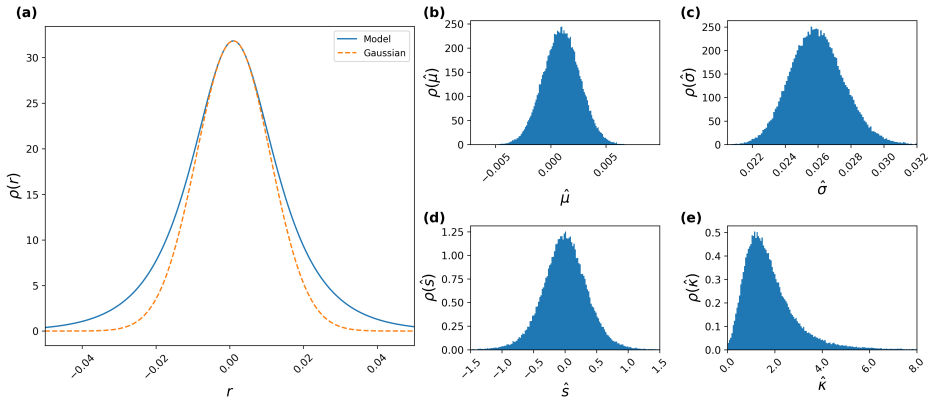

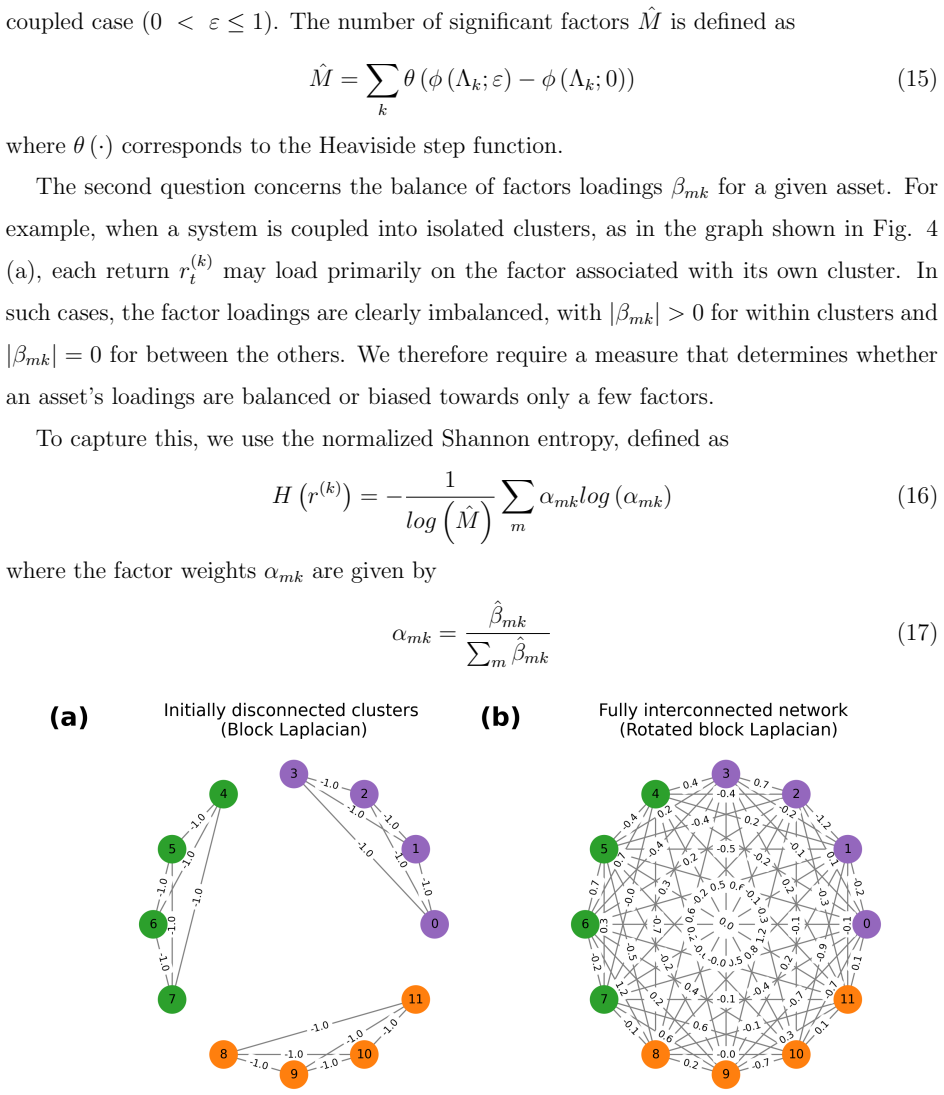

In a network of coupled iterated maps for asset returns, with the interaction structure given by a coupling matrix from an orthogonal transformation of the Laplacian matrix that links initial isolated clusters into a fully connected network, stable co-movement patterns emerge and function as financial factors. The relation between the number of initial clusters and the number of observed factors is consistent with a center manifold reduction, and there is an optimal regime in which the factors produced by the network explain the variance of the assets.

What carries the argument

The coupling matrix derived from an orthogonal transformation of the Laplacian matrix, which defines the interaction structure among assets and drives the emergence of co-movement patterns.

If this is right

- Stable patterns of co-movement arise and function as financial factors.

- The number of observed factors is consistent with a center manifold reduction from the initial clustering.

- Assets' variance is effectively explained by the network-produced factors in an optimal regime.

- Factor models can be derived from the structure of asset interactions rather than imposed statistically.

Where Pith is reading between the lines

- Real market factors may be predictable from the topology of influence networks without needing historical returns data.

- Changes in initial clustering could correspond to shifts between market regimes or sector structures.

- The framework could be tested by comparing emergent factors from varied clusterings against standard empirical factor models.

Load-bearing premise

That the specific construction of the coupling matrix via orthogonal transformation of the Laplacian, together with the iterated-map dynamics, produces realistic factor emergence without requiring post-hoc statistical fitting or additional assumptions about trader behavior.

What would settle it

Simulate the iterated-map dynamics on a network with a known number of initial clusters; if the number of stable co-movement patterns that emerge does not match the initial cluster count and fail to explain asset variance optimally, the claim of natural factor emergence is falsified.

Figures

read the original abstract

Factor models characterize the joint behavior of large sets of financial assets through a smaller number of underlying drivers. We develop a network-based framework in which factors emerge naturally from the structure of interactions among assets rather than being imposed statistically. The market is modeled as a system of coupled iterated maps, where assets' return depends on its own past returns and those of related assets. Effectively modeling the influence of irrational traders whose decisions are based on the past movements of a collection of stocks. The interaction structure between stock returns is defined by a coupling matrix derived from an orthogonal transformation of a Laplacian matrix that gradually links initially isolated clusters into a fully connected network. Within this structure, stable patterns of co-movement arise and can be interpreted as financial factors. The relationship between the initial clustering and the number of observed factors is consistent with a center manifold reduction. We identify an optimal regime in which assets' variance is effectively explained by the set of factors produced by the network. Our framework offers a structural perspective based on interaction-based factor formation and dimension reduction in financial markets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The paper proposes a network-based framework in which financial factors emerge from a system of coupled iterated maps modeling asset returns. The interaction structure is defined by a coupling matrix obtained via orthogonal transformation of a Laplacian matrix that gradually connects initially isolated clusters into a connected network. The central claims are that stable co-movement patterns arise naturally and can be interpreted as factors, that the relationship between initial clustering and observed factor count is consistent with center manifold reduction, and that an optimal regime exists in which the network-produced factors effectively explain asset variance.

Significance. If the missing derivations, spectral analysis, and validation were supplied, the work would provide a mechanistic, interaction-driven account of factor emergence that complements purely statistical factor models and links dynamical systems ideas (center manifold reduction) to financial networks. This could be significant for understanding dimension reduction in markets without post-hoc statistical imposition.

major comments (3)

- [Abstract] Abstract: The claim that 'the relationship between the initial clustering and the number of observed factors is consistent with a center manifold reduction' is asserted without any derivation, eigenvalue calculation, or reference to specific equations or sections showing that the slow modes of the transformed Laplacian correspond to the cluster count.

- [Abstract] Abstract: The iterated-map dynamics governing asset returns (how each return depends on its own past and those of related assets) and the explicit construction of the coupling matrix via orthogonal transformation of the Laplacian are not specified, which is load-bearing for the claim that stable co-movement patterns arise automatically without additional assumptions or fitting.

- [Abstract] Abstract: No simulation results, eigenvalue spectra, or quantitative evidence is provided to demonstrate the 'optimal regime' in which assets' variance is explained by the set of factors produced by the network, leaving the central empirical claim unsupported.

minor comments (1)

- [Abstract] The sentence 'Effectively modeling the influence of irrational traders whose decisions are based on the past movements of a collection of stocks' is grammatically incomplete and should be rephrased for clarity.

Simulated Author's Rebuttal

We thank the referee for their constructive and detailed comments. We agree that the abstract is highly condensed and that several claims would be strengthened by explicit references to derivations, equations, and results from the main text. We will revise the manuscript to address these points directly.

read point-by-point responses

-

Referee: [Abstract] Abstract: The claim that 'the relationship between the initial clustering and the number of observed factors is consistent with a center manifold reduction' is asserted without any derivation, eigenvalue calculation, or reference to specific equations or sections showing that the slow modes of the transformed Laplacian correspond to the cluster count.

Authors: We acknowledge that the abstract asserts this consistency without supporting details. The manuscript contains the relevant spectral analysis of the transformed Laplacian, showing that the multiplicity of the zero eigenvalue matches the initial cluster count and aligns with the slow modes expected under center manifold reduction. We will revise the abstract to include a brief reference to this analysis and add a short outline of the eigenvalue argument in the introduction. revision: yes

-

Referee: [Abstract] Abstract: The iterated-map dynamics governing asset returns (how each return depends on its own past and those of related assets) and the explicit construction of the coupling matrix via orthogonal transformation of the Laplacian are not specified, which is load-bearing for the claim that stable co-movement patterns arise automatically without additional assumptions or fitting.

Authors: We agree that the abstract does not spell out the governing equations. The full manuscript defines the iterated-map update rule for asset returns and gives the explicit orthogonal transformation used to obtain the coupling matrix from the Laplacian. We will update the abstract to include these specifications or direct references to the relevant equations and sections. revision: yes

-

Referee: [Abstract] Abstract: No simulation results, eigenvalue spectra, or quantitative evidence is provided to demonstrate the 'optimal regime' in which assets' variance is explained by the set of factors produced by the network, leaving the central empirical claim unsupported.

Authors: We accept that the abstract presents the optimal-regime claim without accompanying evidence. The manuscript reports simulation results, including eigenvalue spectra and variance-explained metrics, that identify this regime. We will revise the abstract to reference the relevant figures and quantitative findings from the results section. revision: yes

Circularity Check

Factor count equals initial cluster count by construction of Laplacian-based coupling matrix

specific steps

-

self definitional

[Abstract]

"The interaction structure between stock returns is defined by a coupling matrix derived from an orthogonal transformation of a Laplacian matrix that gradually links initially isolated clusters into a fully connected network. Within this structure, stable patterns of co-movement arise and can be interpreted as financial factors. The relationship between the initial clustering and the number of observed factors is consistent with a center manifold reduction."

The Laplacian is built directly from the chosen initial clusters; its spectrum has multiplicity of the zero eigenvalue equal to the number of components. The orthogonal transformation and subsequent center-manifold reduction therefore yield slow modes whose count equals the input cluster count by algebraic construction. Declaring this relationship 'consistent' and interpreting the modes as emergent factors is tautological rather than a derived result.

full rationale

The derivation begins by positing isolated clusters, constructs the interaction matrix explicitly from an orthogonal transform of the Laplacian on those clusters, then asserts that the resulting slow modes (factors) match the cluster count via center-manifold reduction. This relationship is not an independent prediction but follows directly from the spectral properties of the disconnected Laplacian (zero eigenvalues equal to component count) preserved under orthogonal transformation. The 'emergence' and 'consistency' therefore reduce to the model's structural inputs rather than arising from trader dynamics or external data. The optimal-regime selection for variance explanation further indicates post-hoc tuning. The central claim remains partially independent in its iterated-map dynamics but the load-bearing dimension-reduction step is circular.

Axiom & Free-Parameter Ledger

free parameters (1)

- coupling strength

axioms (2)

- domain assumption Asset returns follow coupled iterated maps that depend on own past returns and those of related assets.

- ad hoc to paper Interaction structure is given by a coupling matrix obtained from orthogonal transformation of a Laplacian matrix that gradually connects clusters.

invented entities (1)

-

Evolving network of coupled asset returns

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Capital asset prices: A theory of market equilibrium under conditions of risk,

1B. Malkiel,A Random Walk Down Wall Street: The Best Investment Guide That Money Can Buy(W. W. Norton, 2023). 2W. F. Sharpe, “Capital asset prices: A theory of market equilibrium under conditions of risk,” The journal of finance19, 425–442 (1964). 3M. C. Jensen, F. Black, and M. S. Scholes, “The capital asset pricing model,” Some empirical tests (1972). 1...

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.