Recognition: unknown

Latent community paths in VAR-type models via dynamic directed spectral co-clustering

Pith reviewed 2026-05-10 14:57 UTC · model grok-4.3

The pith

Embedding a degree-corrected stochastic co-blockmodel into VAR transition matrices lets directed spectral co-clustering recover evolving sending and receiving communities with explicit error bounds.

A machine-rendered reading of the paper's core claim, the machinery that carries it, and where it could break.

Core claim

The central claim is that embedding a degree-corrected stochastic co-blockmodel into the transition matrices of VAR-type systems separates sending and receiving roles at the node level, reduces complex directional dependence to an interpretable low-dimensional form, and permits consistent recovery of latent community paths via directed spectral co-clustering plus eigenvector smoothing, with non-asymptotic misclassification bounds holding for both periodic VAR and generalized VHAR specifications.

What carries the argument

Directed spectral co-clustering with eigenvector smoothing applied to transition matrices that arise from a degree-corrected stochastic co-blockmodel.

If this is right

- The same embedding and smoothing procedure yields consistent community recovery for both cyclical PVAR models and multi-horizon VHAR models.

- Node-level separation of sending and receiving roles produces an interpretable low-dimensional representation of directional dependence.

- Non-asymptotic misclassification bounds quantify the finite-sample reliability of the recovered paths.

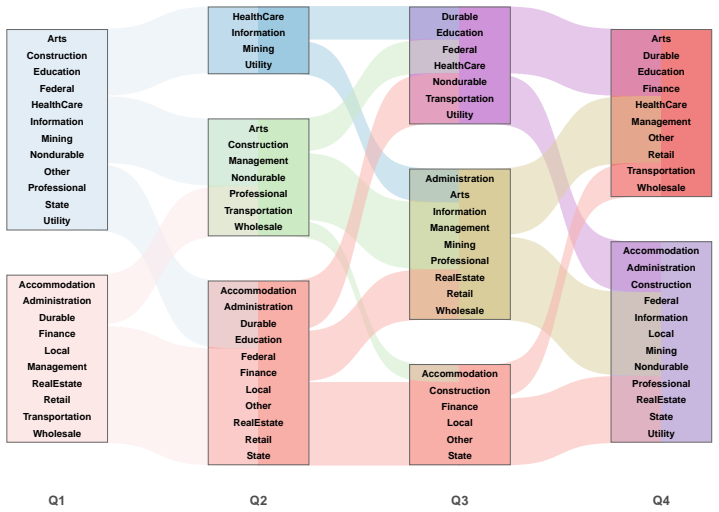

- Applications to U.S. nonfarm payrolls and global stock volatilities distinguish stable core blocks from seasonally mobile or re-allocating sectors.

Where Pith is reading between the lines

- The framework could be applied to other linear multivariate time-series specifications whose coefficient matrices admit a low-rank block approximation.

- The recovered sending and receiving labels might serve as time-varying covariates in subsequent regression or policy models.

- Relaxing the smoothness assumption on community evolution would require alternative smoothing operators or change-point detection steps.

- The method's performance on networks with heavy-tailed degree distributions could be checked by varying the degree-correction parameters in simulation.

Load-bearing premise

The transition matrices of the observed VAR-type process are generated from or well approximated by a degree-corrected stochastic co-blockmodel whose community labels change smoothly enough for eigenvector smoothing to recover them.

What would settle it

A controlled simulation in which community labels are forced to jump discontinuously or the transition matrices are generated from a non-block structure, after which the misclassification rate of the recovered paths exceeds the derived bound.

Figures

read the original abstract

This paper proposes a dynamic network framework for uncovering latent community paths in high-dimensional VAR-type models. By embedding a degree-corrected stochastic co-blockmodel (ScBM) into the transition matrices of VAR-type systems, we separate sending and receiving roles at the node level and summarize complex directional dependence in an interpretable low-dimensional form. Our method integrates directed spectral co-clustering with eigenvector smoothing to track how directional groups split, merge, or persist over time. This framework accommodates both periodic VAR (PVAR) models for cyclical seasonal evolution and generalized VHAR models for structural transitions across ordered dependence horizons. We establish non-asymptotic misclassification bounds for both procedures and provide supporting evidence through Monte Carlo experiments. Applications to U.S.\ nonfarm payrolls distinguish a recurrent business-centered core from more mobile, seasonally sensitive sectors. In global stock volatilities, the results reveal a compact U.S.-centered long-horizon block, a Europe-heavy developed core, and a more dynamic short-horizon reallocation of peripheral and bridge markets.

Editorial analysis

A structured set of objections, weighed in public.

Referee Report

Summary. The manuscript proposes a dynamic network framework for uncovering latent community paths in high-dimensional VAR-type models. By embedding a degree-corrected stochastic co-blockmodel (ScBM) into the transition matrices, it separates sending and receiving roles at the node level via directed spectral co-clustering combined with eigenvector smoothing. The approach handles periodic VAR (PVAR) and generalized VHAR models, establishes non-asymptotic misclassification bounds for the procedures, and provides Monte Carlo experiments along with applications to U.S. nonfarm payrolls and global stock volatilities.

Significance. If the central claims hold, the work provides an interpretable low-dimensional summary of complex directional dependencies in multivariate time series while separating node roles and tracking dynamic community evolution. The non-asymptotic bounds and Monte Carlo support could advance network analysis in econometrics and statistics, particularly for time-varying structures.

major comments (1)

- Abstract and theoretical results on misclassification bounds: The non-asymptotic misclassification bounds are stated for the spectral co-clustering and smoothing steps under the assumption that the transition matrices are known and close to the degree-corrected ScBM. However, these matrices must be estimated from finite-length time series in the VAR-type model, and the paper does not incorporate the additional finite-sample estimation error (e.g., from least-squares or regularized estimators) into the perturbation analysis or bounds. This is load-bearing for the central claim, as the eigenvector perturbation guarantees may fail to control the final misclassification rate when VAR estimation perturbations exceed the assumed separation.

minor comments (2)

- Monte Carlo experiments: The description lacks explicit details on data generation, exact exclusion rules for time series, hyperparameter selection (including number of communities), and code availability, which would aid reproducibility.

- Notation and implementation: The choice of the number of communities (a free parameter) and the precise smoothing procedure for eigenvector paths across time could be clarified with pseudocode or additional equations.

Simulated Author's Rebuttal

We thank the referee for the careful and constructive review of our manuscript. We address the major comment below.

read point-by-point responses

-

Referee: The non-asymptotic misclassification bounds are stated for the spectral co-clustering and smoothing steps under the assumption that the transition matrices are known and close to the degree-corrected ScBM. However, these matrices must be estimated from finite-length time series in the VAR-type model, and the paper does not incorporate the additional finite-sample estimation error (e.g., from least-squares or regularized estimators) into the perturbation analysis or bounds. This is load-bearing for the central claim, as the eigenvector perturbation guarantees may fail to control the final misclassification rate when VAR estimation perturbations exceed the assumed separation.

Authors: We thank the referee for highlighting this important point. The non-asymptotic misclassification bounds (Theorems 3.1 and 3.2) are indeed derived under the assumption that the transition matrices are observed and lie close to a degree-corrected stochastic co-blockmodel with sufficient separation; the perturbation analysis for the directed spectral co-clustering and eigenvector smoothing steps is conditional on this. The manuscript does not fold the finite-sample estimation error arising from least-squares or regularized estimation of the VAR-type coefficients into these bounds. This is a genuine limitation of the current theoretical results. We will revise the paper to (i) explicitly state the conditional nature of the bounds in the theoretical section, (ii) add a remark outlining how existing high-dimensional consistency results for VAR estimators can be combined with the existing perturbation bounds via a triangle inequality argument on the eigenvector error (provided the estimation error is of smaller order than the separation), and (iii) clarify that the Monte Carlo experiments already use estimated transition matrices and demonstrate practical robustness. This partial revision will make the scope of the guarantees transparent without requiring a complete re-derivation of the non-asymptotic bounds. revision: partial

Circularity Check

No significant circularity; bounds derived independently under stated ScBM assumption

full rationale

The paper embeds a degree-corrected stochastic co-blockmodel into VAR transition matrices and derives non-asymptotic misclassification bounds for the directed spectral co-clustering and eigenvector smoothing steps. These bounds are established conditionally on the transition matrices being close to the ScBM structure, without reducing the community path recovery to a fitted parameter by construction or relying on load-bearing self-citations for the core uniqueness or separation arguments. The VAR estimation step is treated as a separate preprocessing stage whose error is not folded into the clustering bounds, but this is an assumption limitation rather than a definitional loop. The derivation chain remains self-contained against external spectral clustering theory and blockmodel results.

Axiom & Free-Parameter Ledger

free parameters (1)

- number of communities

axioms (1)

- domain assumption Transition matrices of the VAR-type process are generated from a degree-corrected stochastic co-blockmodel whose community structure evolves over time.

invented entities (1)

-

latent community paths

no independent evidence

Reference graph

Works this paper leans on

-

[1]

Abbe, E. (2018). Community detection and stochastic block models: recent developments. Journal of Machine Learning Research , 18(177):1--86

2018

-

[2]

G., Bollerslev, T., Diebold, F

Andersen, T. G., Bollerslev, T., Diebold, F. X., and Labys, P. (2003). Modeling and forecasting realized volatility. Econometrica , 71(2):579--625. DOI: https://doi.org/10.1111/1468-0262.00418

-

[3]

Baek, C., Davis, R. A., and Pipiras, V. (2018). Periodic dynamic factor models: Estimation approaches and applications. Electronic Journal of Statistics , 12(2):4377--4411. DOI: 10.1214/18-EJS1518

-

[4]

Baek, C. and Park, M. (2021). Sparse vector heterogeneous autoregressive modeling for realized volatility. Journal of the Korean Statistical Society , 50(2):495--510. DOI: 10.1007/s42952-020-00090-5

-

[5]

Bai, J. and Ng, S. (2007). Determining the number of primitive shocks in factor models. Journal of Business & Economic Statistics , 25(1):52--60. DOI: 10.1198/073500106000000413

-

[6]

Barigozzi, M., Cho, H., and Owens, D. (2024). FNETS: factor-adjusted network estimation and forecasting for high-dimensional time series. Journal of Business & Economic Statistics , 42(3):890--902. DOI: 10.1080/07350015.2023.2257270

-

[7]

Basu, S., Das, S., Michailidis, G., and Purnanandam, A. (2024). A high-dimensional approach to measure connectivity in the financial sector. The Annals of Applied Statistics , 18(2):922--945. DOI: 10.1214/22-AOAS1702

-

[8]

Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics , 43(4):1535--1567. DOI: 10.1214/15-AOS1315

-

[9]

A fast iterative shrinkage-thresholding algorithm for linear inverse problems

Beck, A. and Teboulle, M. (2009). A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences , 2(1):183--202. DOI: 10.1137/080716542

-

[10]

Boubacar Ma \" nassara, Y. and Ursu, E. (2023). Estimating weak periodic vector autoregressive time series. Test , 32(3):958--997. DOI: 10.1007/s11749-023-00859-w

-

[11]

Brownlees, C., Gu mundsson, G. S., and Lugosi, G. (2022). Community detection in partial correlation network models. Journal of Business & Economic Statistics , 40(1):216--226. DOI: 10.1080/07350015.2020.1798241

-

[12]

Brownlees, C., Nualart, E., and Sun, Y. (2018). Realized networks. Journal of Applied Econometrics , 33(7):986--1006. DOI: 10.1002/jae.2642

-

[13]

Chaudhuri, K., Chung, F., and Tsiatas, A. (2012). Spectral clustering of graphs with general degrees in the extended planted partition model. In Proceedings of the 25th Annual Conference on Learning Theory , volume 23 of JMLR Workshop and Conference Proceedings , pages 35.1--35.23

2012

-

[14]

Corsi, F. (2009). A simple approximate long-memory model of realized volatility. Journal of Financial Econometrics , 7(2):174--196. DOI: 10.1093/jjfinec/nbp001

-

[15]

Davis, C. and Kahan, W. M. (1970). The rotation of eigenvectors by a perturbation. iii. SIAM Journal on Numerical Analysis , 7(1):1--46. DOI: 10.1137/0707001

-

[16]

Granger, C. W. (1969). Investigating causal relations by econometric models and cross-spectral methods. Econometrica , 37(3):424--438. DOI: 10.2307/1912791

-

[17]

Gu mundsson, G. S. (2025). Detecting giver and receiver spillover groups in large vector autoregressions. Journal of Business & Economic Statistics , pages 1--12. DOI: 10.1080/07350015.2025.2526430

-

[18]

Gu mundsson, G. S. and Brownlees, C. (2021). Detecting groups in large vector autoregressions. Journal of Econometrics , 225(1):2--26. DOI: 10.1016/j.jeconom.2021.03.012

-

[19]

Lee, S. and Baek, C. (2023). Volatility changes in cryptocurrencies: evidence from sparse VHAR - MGARCH model. Applied Economics Letters , 30(11):1496--1504. DOI: 10.1080/13504851.2022.2064417

-

[20]

Liu, F., Choi, D., Xie, L., and Roeder, K. (2018). Global spectral clustering in dynamic networks. Proceedings of the National Academy of Sciences , 115(5):927--932. DOI: 10.1073/pnas.1718449115

-

[21]

L \"u tkepohl, H. (2005). New Introduction to Multiple Time Series Analysis . Springer Science & Business Media. DOI: 10.1007/978-3-540-27752-1

-

[22]

GICS: global industry classification standard

MSCI (2025). GICS: global industry classification standard. Accessed: 8 January 2025

2025

-

[23]

u ller, U. A., Dacorogna, M. M., Dav \'e , R. D., Olsen, R. B., Pictet, O. V., and Von Weizs \

M \"u ller, U. A., Dacorogna, M. M., Dav \'e , R. D., Olsen, R. B., Pictet, O. V., and Von Weizs \"a cker, J. E. (1997). Volatilities of different time resolutions—analyzing the dynamics of market components. Journal of Empirical Finance , 4(2-3):213--239. DOI: 10.1016/S0927-5398(97)00007-8

-

[24]

and Rohe, K

Qin, T. and Rohe, K. (2013). Regularized spectral clustering under the degree-corrected stochastic blockmodel. In Advances in Neural Information Processing Systems , volume 26, pages 3120--3128

2013

-

[25]

Rohe, K., Chatterjee, S., and Yu, B. (2011). Spectral clustering and the high-dimensional stochastic blockmodel. The Annals of Statistics , 39(4):1878--1915. DOI: 10.1214/11-AOS887

-

[26]

Rohe, K., Qin, T., and Yu, B. (2016). Co-clustering directed graphs to discover asymmetries and directional communities. Proceedings of the National Academy of Sciences , 113(45):12679--12684. DOI: 10.1073/pnas.1525793113

-

[27]

Sch \"o nemann, P. H. (1966). A generalized solution of the orthogonal Procrustes problem. Psychometrika , 31(1):1--10. DOI: 10.1007/BF02289451

-

[28]

Ursu, E. and Duchesne, P. (2009). On modelling and diagnostic checking of vector periodic autoregressive time series models. Journal of Time Series Analysis , 30(1):70--96. DOI: 10.1111/j.1467-9892.2008.00601.x

-

[29]

Vershynin, R. (2018). High-Dimensional Probability: An Introduction with Applications in Data Science , volume 47. Cambridge University Press. DOI: 10.1017/9781108231596

-

[30]

Vinh, N. X., Epps, J., and Bailey, J. (2009). Information theoretic measures for clusterings comparison: Is a correction for chance necessary? In Proceedings of the 26th Annual International Conference on Machine Learning , pages 1073--1080. DOI: 10.1145/1553374.1553511

-

[31]

Wang, Z., Liang, Y., and Ji, P. (2020). Spectral algorithms for community detection in directed networks. Journal of Machine Learning Research , 21(153):1--45

2020

-

[32]

Wong, K. C., Li, Z., and Tewari, A. (2020). Lasso guarantees for -mixing heavy-tailed time series. The Annals of Statistics , 48(2):1124--1142. DOI: 10.1214/19-AOS1840

-

[33]

Ye, C., Wilson, R. C., Comin, C. H., Costa, L. d. F., and Hancock, E. R. (2014). Approximate von Neumann entropy for directed graphs. Physical Review E , 89(5):052804. DOI: 10.1103/PhysRevE.89.052804

-

[34]

Yin, H., Safikhani, A., and Michailidis, G. (2023). A general modeling framework for network autoregressive processes. Technometrics , pages 1--11. DOI: 10.1080/00401706.2023.2203184

discussion (0)

Sign in with ORCID, Apple, or X to comment. Anyone can read and Pith papers without signing in.